Semiconductor Backend Equipment Market Overview

Semiconductor Front-end includes silicon-wafer fabrication, photolithography, deposition, etching, ion implantation and mechanical polishing machines, and Semiconductor Backend Equipment includes the machinery for assembly, packaging and testing of integrated circuits.Semiconductor backend equipment refers to the machinery, tools, and systems used in the backend manufacturing process of semiconductor devices. It involves the assembly, packaging, and testing of individual semiconductor components, such as integrated circuits (ICs), into complete functional devices.

This report provides a deep insight into the global Semiconductor Backend Equipment market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and accessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Semiconductor Backend Equipment Market, this report introduces in detail the market share, market performance, product situation, operation situation, etc. of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Semiconductor Backend Equipment market in any manner.

Semiconductor Backend Equipment Market Analysis:

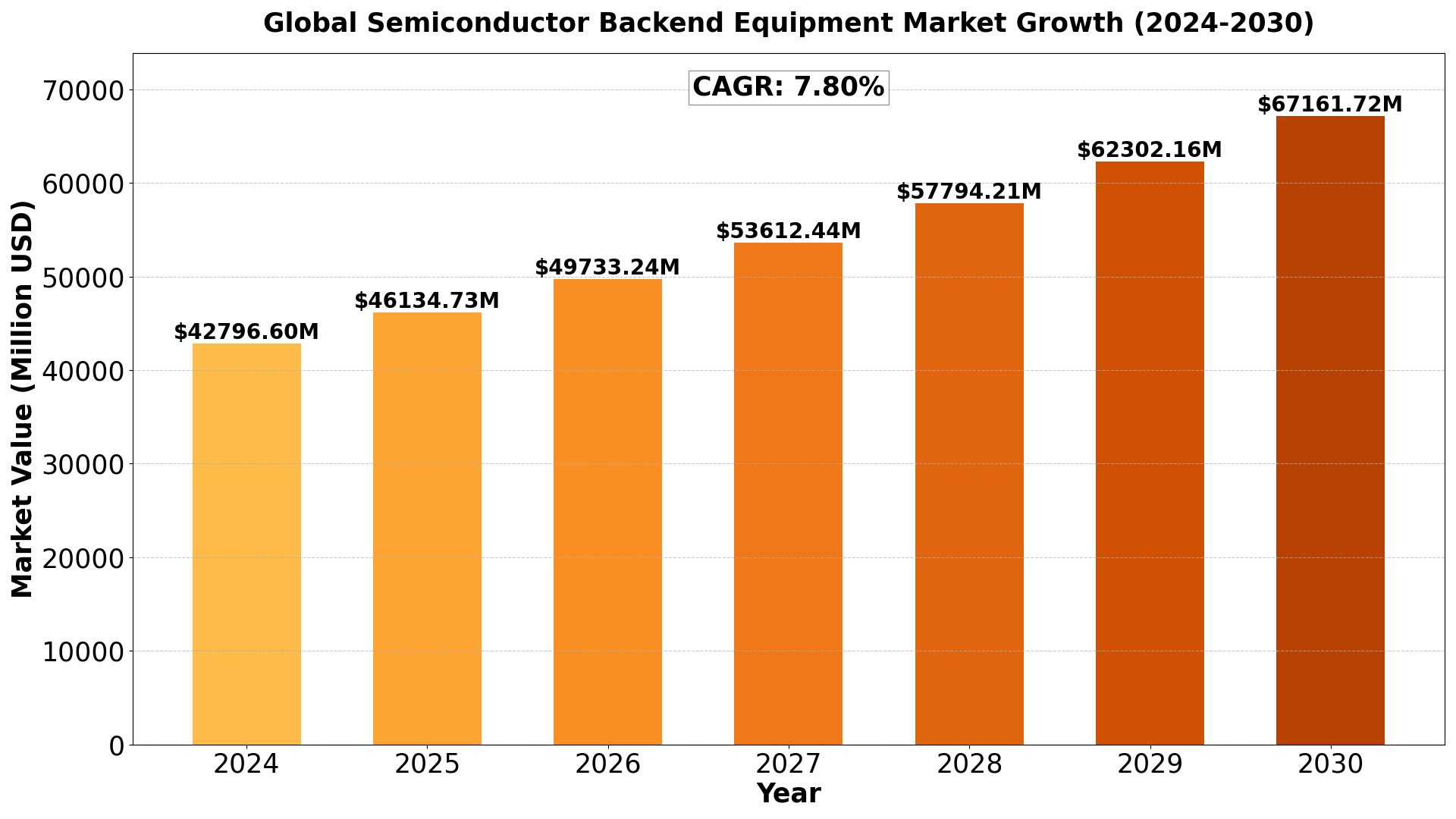

The Global Semiconductor Backend Equipment Market size was estimated at USD 39700 million in 2023 and is projected to reach USD 67161.72 million by 2030, exhibiting a CAGR of 7.80% during the forecast period.

North America Semiconductor Backend Equipment market size was USD 10344.69 million in 2023, at a CAGR of 6.69% during the forecast period of 2024 through 2030.

Access Your Free Sample Report Now

Semiconductor Backend Equipment Key Market Trends :

1. Growing Demand for Advanced Packaging Technologies

- Advanced packaging technologies such as 3D packaging, system-in-package (SiP), and fan-out wafer-level packaging (FO-WLP) are becoming increasingly popular. These technologies are required to meet the demands for higher performance, miniaturization, and multi-functional integration in semiconductors.

- The trend toward smaller, faster, and more power-efficient devices has led to the development of more sophisticated backend equipment capable of handling complex packaging processes. This includes machines for flip-chip bonding, die attach, molding, and wafer thinning.

- Chip-on-chip, chip-on-board, and heterogeneous integration are also gaining momentum in the packaging segment, requiring advanced backend solutions.

2. Increased Focus on Automation and AI Integration

- As the demand for high throughput, precision, and efficiency in semiconductor production grows, backend equipment is being increasingly automated. This includes the use of robotic arms, automated testing systems, and AI-based systems for inspection and quality control.

- Artificial intelligence (AI) and machine learning are being integrated into backend processes for tasks such as predictive maintenance, real-time monitoring, and automated defect detection. These technologies allow for better process optimization, higher yields, and reduced downtime by enabling manufacturers to identify potential issues before they impact production.

3. Increasing Demand for Test Equipment

- With the rapid growth in 5G, IoT, and automotive electronics, there is a growing need for advanced testing capabilities for semiconductor devices. Backend test equipment, such as automated test equipment (ATE) and optical inspection systems, are in high demand to ensure the performance and reliability of semiconductors before they are shipped to customers.

- Burn-in testing, electrical testing, and functional testing are key processes, especially for chips used in critical applications such as automotive systems, mobile devices, and medical electronics. These testing systems must handle increasingly complex chips with faster speeds and higher density while maintaining high levels of accuracy.

4. Miniaturization and Need for Precision Handling Equipment

- As semiconductor devices continue to shrink in size, the demand for precision handling equipment has increased. Smaller and more intricate devices require equipment capable of handling wafers, chips, and packages with ultra-fine precision without introducing contamination or damaging the components.

- There is also a growing need for high-precision bonding and flip-chip bonding equipment that can handle fine-pitch components in packaging. This trend is supported by advanced laser systems, automated wire bonding, and pick-and-place machines designed for handling small-scale parts and ensuring minimal mechanical stress during handling.

5. Sustainability and Environmental Considerations

- Environmental sustainability is becoming a critical consideration in the semiconductor backend industry. Manufacturers are focusing on energy-efficient equipment, reduced chemical usage, and minimized waste generation to meet both regulatory standards and the demand for eco-friendly manufacturing.

- Water recycling systems, energy-saving technologies, and low-emission equipment are being developed to reduce the environmental footprint of semiconductor backend processes. Furthermore, cleanroom technology and environmental monitoring systems are increasingly integrated into backend equipment to ensure compliance with environmental and safety standards.

Semiconductor Backend Equipment Market Regional Analysis :

1. North America (USA, Canada, Mexico)

- USA: The largest market in the region due to advanced infrastructure, high disposable income, and technological advancements. Key industries include technology, healthcare, and manufacturing.

- Canada: Strong market potential driven by resource exports, a stable economy, and government initiatives supporting innovation.

- Mexico: A growing economy with strengths in automotive manufacturing, agriculture, and tourism, benefitting from trade agreements like the USMCA.

2. Europe (Germany, UK, France, Russia, Italy, Rest of Europe)

- Germany: The region’s industrial powerhouse with a focus on engineering, automotive, and machinery.

- UK: A hub for financial services, fintech, and pharmaceuticals, though Brexit has altered trade patterns.

- France: Strong in luxury goods, agriculture, and aerospace with significant innovation in renewable energy.

- Russia: Resource-driven economy with strengths in oil, gas, and minerals but geopolitical tensions affect growth.

- Italy: Known for fashion, design, and manufacturing, especially in luxury segments.

- Rest of Europe: Includes smaller yet significant economies like Spain, Netherlands, and Switzerland with strengths in finance, agriculture, and manufacturing.

3. Asia-Pacific (China, Japan, South Korea, India, Southeast Asia, Rest of Asia-Pacific)

- China: The largest market in the region with a focus on technology, manufacturing, and e-commerce. Rapid urbanization and middle-class growth fuel consumption.

- Japan: Technological innovation, particularly in robotics and electronics, drives the economy.

- South Korea: Known for technology, especially in semiconductors and consumer electronics.

- India: Rapidly growing economy with strengths in IT services, agriculture, and pharmaceuticals.

- Southeast Asia: Key markets like Indonesia, Thailand, and Vietnam show growth in manufacturing and tourism.

- Rest of Asia-Pacific: Emerging markets with growing investment in infrastructure and services.

4. South America (Brazil, Argentina, Colombia, Rest of South America)

- Brazil: Largest economy in the region, driven by agriculture, mining, and energy.

- Argentina: Known for agriculture exports and natural resources but faces economic instability.

- Colombia: Growing economy with strengths in oil, coffee, and flowers.

- Rest of South America: Includes Chile and Peru, which have strong mining sectors.

5. The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, South Africa, Rest of MEA)

- Saudi Arabia: Oil-driven economy undergoing diversification with Vision 2030 initiatives.

- UAE: Financial hub with strengths in tourism, real estate, and trade.

- Egypt: Growing infrastructure development and tourism.

- Nigeria: Largest economy in Africa with strengths in oil and agriculture.

- South Africa: Industrialized economy with strengths in mining and finance.

- Rest of MEA: Includes smaller yet resource-rich markets like Qatar and Kenya with growing infrastructure investments.

Semiconductor Backend Equipment Market Segmentation :

The research report includes specific segments by region (country), manufacturers, Type, and Application. Market segmentation creates subsets of a market based on product type, end-user or application, Geographic, and other factors. By understanding the market segments, the decision-maker can leverage this targeting in the product, sales, and marketing strategies. Market segments can power your product development cycles by informing how you create product offerings for different segments.

Market Segmentation (by Type)

- Metering Equipment

- Testing Equipment

- Cutting Equipment

- Bonding Equipment

- Assembly and Packaging Equipment

- Others

Market Segmentation (by Application)

- Automotive

- Healthcare

- Consumer Electronics

- Aerospace and Defense

- Others

Semiconductor Backend Equipment Market Competitive landscape :

- Applied Materials

- ASM Pacific Technology

- Tokyo Electron Limited (TEL)

- KLA-Tencor Corporation.

- Kulicke & Soffa Industries

- Inc.

- Advantest Corporation

- Lam Research Corporation

- Teradyne Inc.

- Hitachi High-Technologies Corporation

- Cohu

- Inc.

- Rudolph Technologies

- Inc.

- FormFactor

- Inc.

- Plasma-Therm

- Toray Engineering Co.

- Ltd.

- SPTS Technologies (an Orbotech Company)

- BE Semiconductor Industries N.V. (Besi)

- ASM International

- Shinkawa Ltd.

- Startup Ecosystem

- Süss MicroTec SE

- EXICON Co.

- Ltd.

- Tokyo Seimitsu Co.

- Ltd. (Accretech)

- Disco Corporation

- Xcerra Corporation

- SCREEN Semiconductor Solutions Co.

- Ltd.

- Daiichi Jitsugyo Co.

- Ltd. (DJK)

- Hitachi Kokusai Electric Inc.

Download Your Complimentary Sample Report

Drivers

- Technological Advancements: The constant evolution of semiconductor technologies, including miniaturization, high performance, and integration, has significantly increased the demand for advanced backend equipment. Equipment for processes like wafer bonding, packaging, and testing plays a crucial role in meeting the requirements of next-gen semiconductors.

- Growing Demand for Consumer Electronics: The increasing demand for consumer electronics such as smartphones, laptops, and wearables is fueling the growth of the semiconductor backend equipment market. These devices require high-performance chips, leading to greater production and packaging of semiconductors.

- Automotive and IoT Growth: With the rise of autonomous vehicles, electric cars, and the Internet of Things (IoT), the need for advanced semiconductors is rising. These sectors require specialized backend processes for high reliability and compact semiconductor designs, driving the market.

- Shift to 5G: The rollout of 5G technology is pushing the demand for faster, smaller, and more efficient chips. As semiconductor production increases to support 5G infrastructure, the demand for backend equipment like testing, sorting, and packaging is also growing.

- Increase in Semiconductor Outsourcing: Outsourcing of semiconductor production to third-party foundries (fabless companies) and assembly houses is becoming more common. This drives the demand for backend equipment, as companies need reliable equipment to package and test the chips produced in large quantities.

Restraints

- High Capital Investment: Semiconductor backend equipment can be expensive, and the cost of setting up and maintaining these facilities can deter new entrants. Smaller companies may find it difficult to make such high capital investments, limiting market participation.

- Supply Chain Disruptions: The semiconductor industry has been plagued by global supply chain disruptions, particularly in the wake of the COVID-19 pandemic. These disruptions impact the availability of raw materials, equipment parts, and semiconductor components, potentially delaying production and affecting the demand for backend equipment.

- Complexity of Semiconductor Packaging: Advanced semiconductor packaging processes are becoming more complex as chips are miniaturized and require multi-functional designs. The evolving technical complexity can make it difficult for equipment manufacturers to keep pace with the innovations required, limiting market growth.

- Regulatory Challenges: Stringent regulations regarding the environment, labor, and safety can raise operational costs for semiconductor companies and their equipment suppliers. These regulations are also subject to frequent updates, adding complexity to market dynamics.

Opportunities

- Emerging Markets: As semiconductor technology spreads globally, emerging markets like Asia-Pacific and Latin America present significant growth opportunities. These regions are investing heavily in infrastructure development, creating demand for advanced semiconductor backend equipment.

- Adoption of AI and Machine Learning: Artificial intelligence (AI) and machine learning are becoming integral to semiconductor production, particularly in the areas of testing and quality control. Integrating AI into backend equipment to improve testing accuracy and speed could revolutionize the industry.

- Advanced Packaging Technologies: With increasing demand for higher-performance chips, new packaging technologies, such as 3D packaging, wafer-level packaging, and system-in-package, offer opportunities for equipment manufacturers to innovate. These technologies require specialized equipment to handle the complexities of new designs.

- Sustainability Initiatives: Sustainability is an increasing priority for semiconductor manufacturers, creating opportunities for equipment providers to develop energy-efficient and environmentally friendly solutions. Equipment that reduces waste or enhances recyclability will be in high demand as sustainability concerns grow.

- Collaborations and Partnerships: Strategic partnerships between semiconductor manufacturers, equipment suppliers, and R&D institutions can lead to the development of cutting-edge technology and solutions. These collaborations may accelerate the development of next-gen backend equipment.

Challenges

- Technological Obsolescence: The semiconductor industry evolves rapidly, and backend equipment may quickly become obsolete if not updated to keep up with newer technologies. This presents a challenge for equipment suppliers who must continuously innovate to remain competitive.

- Skilled Workforce Shortage: The semiconductor industry requires highly skilled technicians and engineers to operate and maintain advanced equipment. The shortage of such talent could slow down production and increase operational costs, making it harder for companies to scale efficiently.

- Intense Competition: The semiconductor backend equipment market is highly competitive, with several global players vying for market share. Companies face constant pressure to innovate and differentiate their products, which can lead to price wars and lower profit margins.

- Environmental Impact: The environmental impact of semiconductor manufacturing processes, such as the use of hazardous chemicals and high energy consumption, is under increasing scrutiny. Companies may face mounting pressure from governments and the public to adopt greener practices, requiring significant investment in sustainable technologies.

- Trade and Geopolitical Tensions: Trade tensions, particularly between the U.S. and China, can have a profound impact on the semiconductor industry. Restrictions on exports, tariffs, and shifting alliances can disrupt supply chains, impacting the availability and cost of backend equipment.

Key Benefits of This Market Research:

- Industry drivers, restraints, and opportunities covered in the study

- Neutral perspective on the market performance

- Recent industry trends and developments

- Competitive landscape & strategies of key players

- Potential & niche segments and regions exhibiting promising growth covered

- Historical, current, and projected market size, in terms of value

- In-depth analysis of the Semiconductor Backend Equipment Market

- Overview of the regional outlook of the Semiconductor Backend Equipment Market:

Key Reasons to Buy this Report:

- Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

- This enables you to anticipate market changes to remain ahead of your competitors

- You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations, or other strategic documents

- The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

- Provision of market value (USD Billion) data for each segment and sub-segment

- Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

- Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

- Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

- Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

- The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

- Includes in-depth analysis of the market from various perspectives through Porters five forces analysis

- Provides insight into the market through Value Chain

- Market dynamics scenario, along with growth opportunities of the market in the years to come

- 6-month post-sales analyst support

Customization of the Report

In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

FAQs

Q1: What are Semiconductor Backend Equipment?

A1: Semiconductor Backend Equipment refers to tools and machinery used in the final stages of semiconductor manufacturing, including wafer testing, packaging, and assembly processes.

Q2: What is the current market size and forecast for the Semiconductor Backend Equipment market until 2032?

A2: The global Semiconductor Backend Equipment market size was valued at USD 39,700 million in 2023 and is projected to reach USD 67,161.72 million by 2030, growing at a CAGR of 7.80% during the forecast period.

Q3: What are the key growth drivers in the Semiconductor Backend Equipment market?

A3: Key growth drivers include increasing demand for advanced semiconductor packaging, the growth of 5G technology, IoT applications, and the rising demand for consumer electronics.

Q4: Which regions dominate the Semiconductor Backend Equipment market?

A4: Asia-Pacific dominates the Semiconductor Backend Equipment market, particularly China, Japan, and South Korea, due to their strong semiconductor manufacturing and assembly industries.

Q5: What are the emerging trends in the Semiconductor Backend Equipment market?

A5: Emerging trends include the adoption of AI in semiconductor testing, miniaturization of semiconductor devices, and the shift toward 3D packaging and advanced packaging technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...