MARKET INSIGHTS

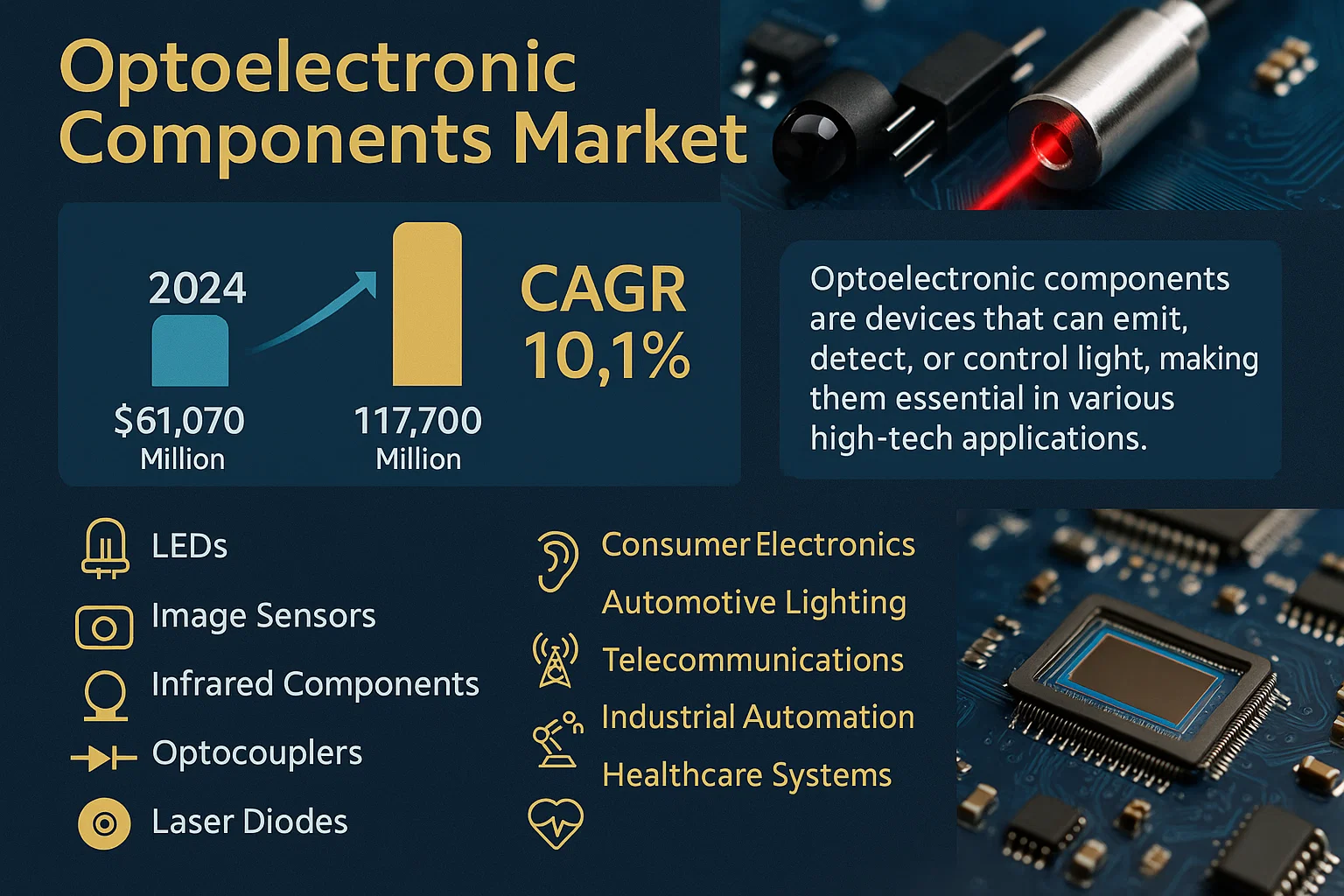

Global Optoelectronic Components Market size was valued at USD 61,070 million in 2024 to USD 117,700 million by 2032, exhibiting a CAGR of 10.1% during the forecast period.

Optoelectronic components are devices that can emit, detect, or control light, making them essential in various high-tech applications. These components include LEDs, image sensors, infrared components, optocouplers, and laser diodes, which are widely used in consumer electronics, automotive lighting, telecommunications, industrial automation, and healthcare systems.

The market growth is driven by increasing demand for energy-efficient lighting solutions, advancements in automotive lighting technologies, and the rapid adoption of smart devices. Key players such as Nichia, Osram, Samsung, and Cree are leading the market with continuous innovations, including high-brightness LEDs and miniaturized optoelectronic sensors. Additionally, the rise in demand for optocouplers in industrial automation and infrared components in security systems further fuels market expansion.

MARKET DRIVERS

Growth in Consumer Electronics

The global demand for smartphones, tablets, and wearable devices continues to drive demand for advanced optoelectronic components including image sensors, OLED displays, and mini-LED backlights. The increasing resolution and functionality requirements of these devices necessitate more sophisticated components with higher efficiency and smaller form factors.

Automotive Innovation

The automotive industry’s shift toward electric and autonomous vehicles is accelerating adoption of LiDAR systems, in-vehicle displays, and advanced driver-assistance systems (ADAS) that rely heavily on optoelectronic components. These applications require components with high reliability and performance under extreme conditions.

➤ The global optoelectronics market is projected to grow at a CAGR of 7.5% from 2023 to 2030, driven by increased adoption across multiple industries.

Energy Efficiency Regulations

Governments worldwide are implementing stricter energy efficiency standards that favor LED lighting over traditional technologies. This creates sustained demand for optoelectronic components in lighting applications, particularly as countries push for net-zero emissions targets.

Industrial Automation Growth

Industry 4.0 initiatives are driving increased adoption of machine vision systems, automated guided vehicles (AGVs), and smart manufacturing equipment that rely on optoelectronic components for precision control and quality assurance. The industrial segment shows the highest growth potential within the optoelectronics market according to recent market analysis.

➤ Industrial automation is expected to grow at 8.2% CAGR through 2030, creating sustained demand for advanced optoelectronic components.

MARKET CHALLENGES

High Manufacturing Complexity

The development and manufacturing of advanced optoelectronic components require significant investment in specialized equipment and highly skilled engineers. This creates significant barriers to entry and can slow down the pace of innovation when companies become risk-averse during economic uncertainty.

Other Challenges

Supply Chain Constraints

The global semiconductor shortage continues to impact the optoelectronics industry, as many components rely on similar materials and manufacturing processes. This has led to extended lead times (up to 52 weeks for some components) and increased costs across the supply chain.

Technical Specialization Requirements

As devices become more complex, manufacturers require increasingly specialized knowledge in areas such as photonics, semiconductor physics, and materials science. This creates a talent gap that can delay project timelines and increase development costs.

MARKET RESTRAINTS

High Initial Investment Requirements

The capital required to establish a new optoelectronics manufacturing facility can reach hundreds of millions of dollars, particularly for advanced components such as those used in semiconductor fabrication. This includes costs for clean rooms, advanced lithography equipment, and specialized testing facilities that create significant barriers to market entry.

MARKET OPPORTUNITIES

Medical Technology Advancements

Optoelectronic components are increasingly critical in medical imaging, surgical robotics, and diagnostic equipment. The global push for better healthcare infrastructure post-pandemic has accelerated investment in these technologies, with the medical optoelectronics segment expected to grow at 9.1% CAGR through 2030.

5G Infrastructure Expansion

The global rollout of 5G networks requires extensive deployment of fiber optics and related optoelectronic components for both infrastructure and end-user devices. This creates sustained demand across multiple sectors including telecommunications, data centers, and consumer electronics.

Optoelectronic Components Market Trends

Rising Demand for Energy-Efficient Lighting Solutions

The global shift toward energy efficiency continues to drive demand for advanced optoelectronic components, particularly Light Emitting Diodes (LEDs). Governments worldwide are implementing stricter energy efficiency regulations, with many countries phasing out traditional incandescent and halogen lighting. This regulatory push has accelerated adoption of LED-based solutions across residential, commercial, and industrial applications. The market has seen particularly strong growth in smart lighting systems that integrate with IoT platforms, enabling both energy savings and advanced control capabilities. Major manufacturers are responding by expanding production capacity and developing next-generation products with higher lumen output and improved thermal management.

Other Trends

Integration with Automotive Advanced Driver Assistance Systems (ADAS)

The automotive industry represents one of the fastest-growing application areas for optoelectronic components, with ADAS systems requiring sophisticated sensor arrays. Image sensors, LiDAR modules, and infrared components are increasingly deployed for obstacle detection, lane departure warning, and autonomous driving functions. The increasing automation levels in vehicles from Level 2 to Level 3 have created substantial demand for high-reliability optoelectronic components that can operate in harsh environments. This trend is further accelerated by the development of electric vehicles, which utilize more electronic systems than traditional vehicles.

Expansion of Fiber Optic Communication Networks

5G network deployment and fiber-to-the-home (FTTH) initiatives continue to drive demand for optoelectronic components in the telecommunications sector. The global push for higher bandwidth and lower latency has accelerated deployment of fiber optic infrastructure, requiring advanced optoelectronic components including laser diodes, photodetectors, and optical transceivers. Investment in data centers and cloud computing infrastructure has similarly driven demand for high-speed optical communication components, with market leaders reporting increased orders for 400G and emerging 800G optical modules. The ongoing rollout of 5G networks requires extensive fiber backhaul, creating sustained demand across developed and developing markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Dominating the Optoelectronic Components Market

The global optoelectronic components market is highly competitive with several key players holding significant market shares. Nichia Corporation leads the market with its extensive product portfolio and strong presence across multiple regions. Osram Opto Semiconductors follows closely with its innovative lighting solutions and strong R&D capabilities. Samsung Electronics leverages its vertical integration and consumer electronics dominance to capture substantial market share in display and lighting applications.

Other notable players include Seoul Semiconductor with its innovative photonic crystal technology, and LG Innotek focusing on high-performance components for automotive and industrial applications. Everlight Electronics maintains strong presence in LED components while Epistar Corporation specializes in high-brightness LEDs. Cree Inc. (now Wolfspeed) maintains strong position in power electronics and optoelectronics. Vishay Intertechnology offers broad portfolio of optoelectronic sensors and components while Lite-On Technology provides reliable solutions for consumer electronics and industrial applications.

List of Key Optoelectronic Components Companies

- Nichia Corporation

- OSRAM Licht AG

- Samsung Electronics Co., Ltd.

- Lumileds Holding B.V.

- Cree, Inc. (now Wolfspeed, Inc.)

- Seoul Semiconductor Co., Ltd.

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Epistar Corporation

- Lite-On Technology Inc.

- Avago Technologies (now Broadcom Inc.)

- Vishay Intertechnology Inc.

- Renesas Electronics Corporation

- MLS Lighting, Inc.

- IPG Photonics Corporation

- Coherent, Inc.

- Jenoptik AG

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Image Sensors dominate due to increasing demand in smartphone and automotive cameras, while Laser Diodes see strong growth from industrial automation and medical applications requiring precise light control. |

| By Application |

|

Consumer Electronics leads due to massive adoption in smartphones and smart devices, while Industrial Automation shows strongest growth as factories increasingly automate with optical sensors and laser guidance systems. |

| By End User |

|

Electronics Manufacturers remain the largest consumers as they integrate optoelectronics into countless consumer devices, while Automotive Companies show fastest growth with increasing adoption of LiDAR and advanced driver assistance systems. |

| By Region |

|

Asia-Pacific dominates production and consumption with extensive electronics manufacturing ecosystems, while North America leads in innovation and specialized applications like autonomous vehicles and advanced robotics. |

| By Technology |

|

CMOS Image Sensors continue to dominate due to lower power consumption and cost efficiency, while Laser Diode Technology advances enable new applications in material processing and medical diagnostics with higher precision and reliability. |

Regional Analysis: Optoelectronic Components Market

Asia-Pacific’s dominance in smartphone, television, and display manufacturing creates massive demand for advanced optoelectronic components including sensors, LEDs, and imaging modules. The region produces over 70% of global consumer electronics, driving continuous innovation in miniaturization and energy efficiency of optoelectronic components through intense R&D competition among market leaders.

Rapid adoption of advanced driver assistance systems (ADAS) and in-vehicle infotainment systems across Japanese and Korean automakers drives demand for specialized optoelectronic components. The region leads in developing integrated optoelectronic systems for autonomous driving technologies, with strong government-industry partnerships accelerating development of LIDAR and sensor technologies for next-generation vehicles.

Massive 5G infrastructure deployment across China, South Korea, and Japan creates unprecedented demand for high-speed optoelectronic components in telecommunications. The region leads in developing integrated optoelectronic systems for smart cities and industrial IoT, with China’s massive IoT deployment creating synergies between consumer electronics and industrial automation optoelectronics markets.

Asia-Pacific’s complete optoelectronics supply chain from semiconductor fabrication to final assembly creates significant cost advantages and faster time-to-market. Concentration of display manufacturers, sensor foundries, and packaging specialists within the region enables continuous improvement in optoelectronic component performance while reducing costs through integrated manufacturing ecosystems and industrial clusters.

North America

North America maintains strong position in specialized and high-end optoelectronic components, particularly for aerospace, defense, and specialized industrial applications. The region benefits from close university-industry collaboration in optoelectronics research, with leading research institutions continuously advancing photonics and integrated optics technologies. The mature regulatory environment and high adoption rate of Industry 4.0 technologies across manufacturing creates sustained demand for advanced optoelectronic components in automation and robotics applications.

Europe

Europe remains a hub for precision optoelectronics with particular strength in industrial automation, automotive, and scientific instrumentation applications. Strict regulatory standards drive innovation in energy-efficient optoelectronic components, with the region leading in photonics research and development. The presence of major automotive manufacturers and industrial automation companies creates stable demand for high-performance optoelectronic components, particularly in Germany, France, and the UK, where government initiatives support photonics research and development through public-private partnerships.

Latin America

Latin America shows growing but fragmented demand for optoelectronic components, primarily driven by consumer electronics imports and gradual industrial modernization. Brazil and Mexico lead in regional manufacturing of electronics, creating steady demand for standard optoelectronic components. The market shows strongest growth in Mexico, where proximity to North American markets drives integration into North American supply chains for automotive and consumer electronics optoelectronics.

Middle East & Africa

Middle East & Africa represent emerging but rapidly growing markets for optoelectronic components, primarily driven by infrastructure development and increasing electronics adoption. The region shows particular strength in LED lighting adoption and basic sensor applications, with Gulf states leveraging oil revenues to invest in smart city technologies that incorporate significant optoelectronic components. South Africa and Nigeria show growing electronics manufacturing capabilities, particularly in automotive and consumer goods, that create sustainable demand for optoelectronic components.

Report Scope

This report provides a comprehensive analysis of the global Optoelectronic Components Market, covering the period 2025-2032. It includes detailed insights into market dynamics, technological advancements, competitive landscape, and regional analysis.

Key focus areas include:

- Market Overview: The report begins with an overview outlining the current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand-supply balance, regulatory landscape, and the strategic role of optoelectronics across various industries.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of IoT/5G, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

The report employs both primary and secondary research methodologies, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Optoelectronic Components Market?

-> Optoelectronic Components Market size was valued at USD 61,070 million in 2024 to USD 117,700 million by 2032, exhibiting a CAGR of 10.1% during the forecast period.

Which key companies operate in Optoelectronic Components Market?

-> Key players include Nichia, Osram, Samsung, Lumileds, Cree, Seoul Semiconductor, Everlight, LG Innoteck, Epister, Liteon, Avago, Vishay, Fairchild, Renesas Electronics, MLS Lighting, IPG, Coherent, and Jenoptik among others.

What are the key growth drivers?

-> Key growth drivers include increasing adoption of IoT and smart devices, growth in telecommunications infrastructure, rising demand for energy-efficient lighting, and advancements in automotive electronics and autonomous vehicles.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing market, driven by strong manufacturing base in China, Japan, and South Korea. North America and Europe also hold significant market shares due to advanced technological adoption.

What are the emerging trends?

-> Emerging trends include miniaturization of components, integration of AI in optoelectronic devices, development of flexible and transparent displays, and increasing adoption of LiDAR technology in autonomous vehicles.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...