MARKET INSIGHTS

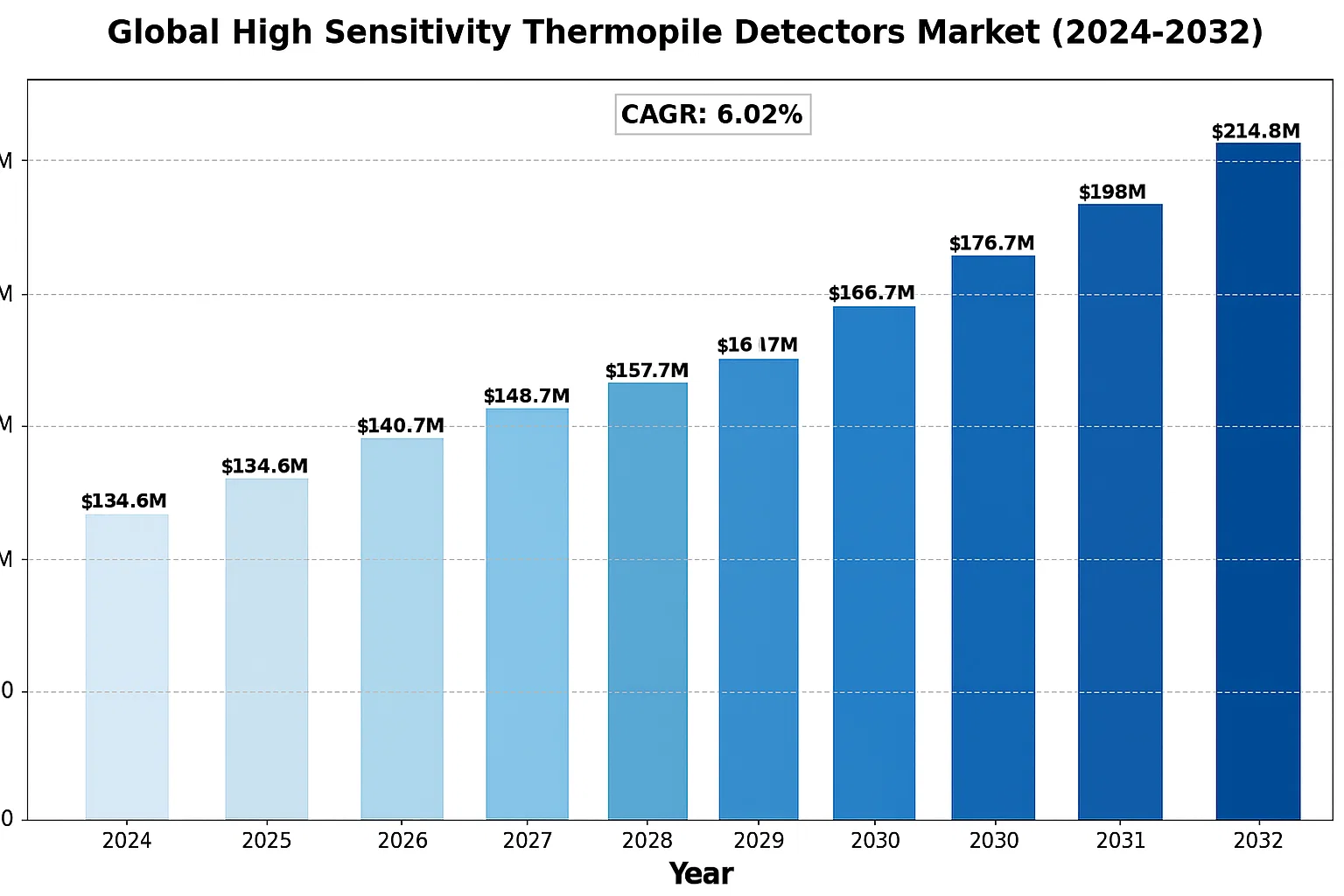

The global High Sensitivity Thermopile Detectors Market was valued at US$ 134.6 million in 2024 and is projected to reach US$ 214.8 million by 2032, at a CAGR of 6.02% during the forecast period 2025-2032.

High sensitivity thermopile detectors are infrared sensors that convert thermal energy into electrical signals with exceptional precision. These devices utilize thermoelectric principles through multiple thermocouples connected in series (thermopile), enabling detection of minute temperature changes. Key applications include non-contact temperature measurement, gas analysis, flame detection, and medical diagnostics, with growing adoption in industrial automation and consumer electronics.

The market growth is driven by increasing demand for non-invasive temperature monitoring across healthcare applications, particularly post-pandemic. Industrial sector adoption is accelerating due to Industry 4.0 implementations, while automotive applications in occupant detection systems present new opportunities. However, competition from alternative technologies like microbolometers presents a market challenge. Key players such as Excelitas Technologies and Hamamatsu Photonics are investing in miniaturization and multi-spectral detection capabilities to maintain competitive advantage.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Non-Contact Temperature Measurement to Accelerate Market Expansion

The global high sensitivity thermopile detector market is witnessing robust growth due to the escalating demand for non-contact temperature measurement across multiple industries. These detectors provide unparalleled accuracy in measuring surface temperatures without physical contact, making them indispensable in medical diagnostics, industrial automation, and consumer electronics. Recent advancements have enabled thermopile detectors to achieve resolutions as high as 0.1°C, with response times under 100 milliseconds. The COVID-19 pandemic significantly boosted adoption, with infrared thermometers becoming standard equipment in public health screening. While the healthcare sector continues to drive demand, emerging applications in smart home devices and automotive systems are creating new growth avenues for market players.

Industrial Automation Boom Fuels Thermopile Detector Adoption

Industrial sectors are increasingly integrating high sensitivity thermopile detectors into manufacturing processes as part of Industry 4.0 initiatives. These detectors play crucial roles in predictive maintenance, quality control, and process monitoring across food processing, semiconductor manufacturing, and metallurgy. The market has seen particular growth in applications requiring temperature monitoring of moving parts or hazardous environments where contact sensors are impractical. Studies indicate that proper thermal monitoring can reduce equipment failure rates by up to 45% in industrial settings, driving manufacturers to invest in advanced thermopile solutions. The detectors’ ability to operate in extreme temperatures ranging from -40°C to +300°C makes them versatile for diverse industrial applications.

Furthermore, the integration of thermopile arrays with machine vision systems is enabling new use cases in automated inspection. These technological synergies are expected to maintain strong market momentum as industries continue their digital transformation journeys.

MARKET RESTRAINTS

High Development Costs and Technical Challenges Limit Market Penetration

Despite their advantages, high sensitivity thermopile detectors face adoption barriers due to complex manufacturing processes and substantial R&D investments. The production of precise microbolometer arrays requires cleanroom facilities and specialized fabrication techniques, resulting in high unit costs that can exceed standard temperature sensors by 300-500%. Additionally, maintaining consistent performance across production batches presents quality control challenges, particularly for medical-grade applications where measurement accuracy is critical. These cost factors make thermopile detectors less accessible to small and medium enterprises, restricting market growth in price-sensitive segments.

Environmental Sensitivity Impacts Field Reliability

Thermopile detectors exhibit performance degradation when exposed to certain environmental conditions, creating adoption challenges in demanding operational environments. Humidity variations can cause measurement drift, while dust accumulation on sensor windows significantly reduces accuracy over time. Field studies have shown that unprotected outdoor installations may experience up to 15% accuracy loss within six months of deployment. While protective measures like hermetic sealing and desiccant packs mitigate these issues, they add to system complexity and cost. Manufacturers continue to face engineering challenges in developing detectors that maintain their high sensitivity specifications across diverse climate conditions and industrial contaminants.

MARKET OPPORTUNITIES

Emerging Applications in Smart Buildings and IoT Create New Growth Vectors

The proliferation of smart building technologies presents substantial growth opportunities for high sensitivity thermopile detector manufacturers. Building automation systems increasingly incorporate thermal sensors for occupancy detection, HVAC optimization, and energy management. Market analysis indicates that thermopile-based presence detectors can reduce commercial building energy consumption by 18-22% compared to traditional PIR sensors. Furthermore, the integration of these detectors with IoT platforms enables predictive maintenance of critical building infrastructure. The global smart building market’s projected annual growth of 12-15% provides a robust foundation for thermopile detector adoption in this sector.

Advancements in MEMS Technology Enable Cost Reduction

Recent breakthroughs in MEMS fabrication techniques are creating opportunities to reduce thermopile detector costs while maintaining performance standards. Wafer-level packaging and automated assembly methods have decreased production costs by approximately 30% over the past three years. These manufacturing improvements, combined with economies of scale from increased production volumes, are making high sensitivity thermopile solutions attainable for mid-range applications. The development of CMOS-compatible processes shows particular promise, potentially enabling price points that could unlock mass-market consumer applications. Industry leaders are investing heavily in these technological advancements to capitalize on emerging opportunities in consumer electronics and automotive sectors.

MARKET CHALLENGES

Intense Competition from Alternative Technologies Pressures Margins

The thermopile detector market faces growing competition from emerging temperature sensing technologies that threaten its market position. Pyroelectric detectors and quantum well infrared photodetectors (QWIPs) offer comparable performance in certain applications, while thermal imaging cameras provide superior spatial resolution for some use cases. This competitive landscape forces thermopile manufacturers to continually innovate while facing pricing pressures, particularly in consumer and commercial segments where cost sensitivity is high. The market has seen average selling prices decline by 8-10% annually as competition intensifies, squeezing profitability for established players.

Supply Chain Vulnerabilities Impact Production Consistency

Global supply chain disruptions have exposed vulnerabilities in thermopile detector manufacturing, particularly for specialty materials and semiconductor components. Lead times for certain infrared filter materials have extended to 9-12 months in some cases, creating production bottlenecks. Manufacturers are struggling to secure stable supplies of germanium and silicon wafers, which are critical for high-performance detectors. These supply constraints threaten the industry’s ability to meet growing demand and may delay market expansion if not resolved through strategic supplier diversification and inventory management improvements.

GLOBAL HIGH SENSITIVITY THERMOPILE DETECTORS MARKET TRENDS

Growing Demand for Non-Contact Temperature Measurement Accelerates Market Growth

The global high sensitivity thermopile detectors market is experiencing significant growth due to the rising demand for non-contact temperature measurement solutions across various industries. With increasing adoption in medical diagnostics, industrial automation, and security applications, these detectors are becoming indispensable. Recent technological advancements have enhanced their sensitivity to detect temperature differences as minute as 0.01°C, making them ideal for precision applications. The COVID-19 pandemic particularly boosted demand for thermopile-based fever detection systems, with global deployments increasing by over 200% during 2020-2022. Medical applications continue to drive innovation, with new detectors achieving faster response times below 50ms while maintaining high accuracy thresholds.

Other Trends

Miniaturization and IoT Integration

The trend toward miniaturization is reshaping the thermopile detector market, with manufacturers developing compact, low-power consumption models suitable for portable devices and IoT applications. These advancements are crucial for wearable health monitors and smart home systems, where space and energy efficiency are paramount. Concurrently, integration with wireless technologies enables real-time temperature monitoring across distributed systems. The industrial sector is adopting these solutions for predictive maintenance, where thermopile arrays can monitor equipment temperatures across entire facilities with minimal installation requirements.

Expansion in Industrial Automation and Smart Manufacturing

Industry 4.0 initiatives are significantly increasing the utilization of high sensitivity thermopile detectors in manufacturing environments. Their ability to provide continuous, non-intrusive temperature monitoring makes them ideal for quality control in processes like semiconductor fabrication, food production, and pharmaceutical manufacturing. Recent developments in multi-channel thermopile arrays allow simultaneous monitoring of multiple heat sources, improving process efficiency by 30-40% in controlled environments. Additionally, the integration of these detectors with machine vision systems enables comprehensive thermal profiling of production lines, reducing defects and energy consumption. As smart factories become more prevalent, the demand for these advanced thermal detection solutions is expected to maintain double-digit growth rates through the decade.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Define Market Competition

The global high sensitivity thermopile detectors market features a dynamic competitive environment with Excelitas Technologies and Hamamatsu Photonics emerging as dominant players. These companies collectively held approximately 28% market share in 2023, leveraging their advanced sensing technologies and established distribution networks across key regions. Excelitas particularly strengthened its position through the 2022 acquisition of Qioptiq’s infrared optics division, enhancing its thermopile detector capabilities.

Thorlabs and Coherent represent significant competitors, particularly in industrial and medical applications. Their growth stems from continuous R&D investments, with Thorlabs reporting a 15% year-over-year increase in photonics component sales during its latest fiscal quarter. Meanwhile, Coherent has expanded its product line following the merger with II-VI Incorporated, creating stronger vertical integration in detector manufacturing.

The market also includes innovative regional players such as Shenzhen Memsfrontier Electronics, which has gained traction in Asia-Pacific markets through cost-competitive offerings. Established players maintain advantages in precision and reliability, while smaller competitors often compete on price and customization capabilities.

List of Key High Sensitivity Thermopile Detector Manufacturers

- Excelitas Technologies Corp. (U.S.)

- Hamamatsu Photonics K.K. (Japan)

- Newport Corporation (U.S.)

- Thorlabs, Inc. (U.S.)

- Edmund Optics (U.S.)

- LASER COMPONENTS GmbH (Germany)

- Ophir Photonics (Israel)

- Coherent, Inc. (U.S.)

- Electro Optical Components, Inc. (U.S.)

- Shenzhen Memsfrontier Electronics Co., Ltd. (China)

Segment Analysis:

By Type

Infrared Detectors Lead the Market Due to Their Wide Adoption in Gas Monitoring Systems

The market is segmented based on type into:

- Infrared Detector

- Subtypes: Single-channel, Multi-channel, and others

- Laser Detector

By Application

Industrial Applications Dominate the Market Owing to Stringent Safety Regulations

The market is segmented based on application into:

- Medical Profession

- Industrial Application

- Security Check

- Electronic Product

- Other

By End User

Manufacturing Sector Accounts for Major Market Share Due to Process Monitoring Needs

The market is segmented based on end user into:

- Manufacturing Industries

- Healthcare Providers

- Research Institutions

- Security Agencies

- Others

Regional Analysis: Global High Sensitivity Thermopile Detectors Market

North America

North America dominates the high sensitivity thermopile detectors market, driven by robust R&D investments and established manufacturing capabilities. The U.S. leads demand due to extensive applications in medical diagnostics (like non-contact thermometers) and industrial gas monitoring systems. Stringent workplace safety regulations (OSHA standards) and the adoption of Industry 4.0 technologies further propel market growth. Canada shows increasing demand in aerospace thermal imaging applications, while Mexico’s market remains nascent but growing steadily, supported by expanding electronics manufacturing clusters. The region benefits from strong presence of key players like Excelitas and Newport Corporation, fostering continuous technological advancements.

Europe

Europe maintains a significant market share, with Germany and France as primary contributors. The region’s growth stems from strict industrial emission monitoring requirements under EU directives and widespread healthcare infrastructure utilizing infrared thermometry. Automotive manufacturers extensively use thermopile detectors for cabin air quality monitoring systems. However, high production costs and reliance on imports for raw materials pose challenges. Recent developments include collaborative R&D projects between academic institutions and detector manufacturers to enhance sensitivity and miniaturization. The UK market shows particular strength in security applications, especially in airports and public spaces.

Asia-Pacific

As the fastest-growing region, Asia-Pacific benefits from China’s massive electronics manufacturing sector and Japan’s leadership in precision instrumentation. China accounts for over 40% of global production capacity, with Shenzhen emerging as a manufacturing hub. India shows remarkable growth potential with increasing adoption in smart building automation and automotive applications. While price sensitivity remains a challenge for premium detectors, regional manufacturers like Shenzhen Memsfrontier Electronics are gaining traction with cost-competitive alternatives. The pandemic significantly boosted demand for medical-grade infrared thermometers across Southeast Asia, creating lasting market expansion.

South America

The South American market demonstrates gradual but steady growth, primarily concentrated in Brazil and Argentina. Industrial gas detection systems drive most demand, particularly in oil refineries and chemical plants. Economic volatility limits large-scale investments, causing slower adoption rates compared to other regions. However, increasing environmental awareness and modernization of industrial facilities present opportunities. Chile shows promising developments in mining applications, utilizing thermopile detectors for equipment monitoring in extreme conditions. The lack of local manufacturing forces heavy reliance on imports, affecting price competitiveness.

Middle East & Africa

This region presents a mixed landscape – while GCC countries invest heavily in advanced security and healthcare infrastructure (notably in UAE and Saudi Arabia), African nations show slower adoption due to limited industrialization. Oil and gas applications dominate market demand, especially for combustible gas leak detection. Israel stands out as a technology innovator, with several startups developing novel thermopile applications for defense and agriculture. Challenges include harsh environmental conditions affecting detector longevity and fragmented distribution networks. Long-term growth potential exists with increasing smart city initiatives and infrastructure development projects across the region.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional High Sensitivity Thermopile Detectors markets, covering the forecast period 2024–2030. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global High Sensitivity Thermopile Detectors market was valued at US$ 134.6 million in 2024 and is projected to reach US$ 214.8 million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Infrared Detector, Laser Detector), application (Medical Profession, Industrial Application, Security Check, Electronic Products), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis where relevant. Asia-Pacific currently dominates with 42.5% market share in 2023.

- Competitive Landscape: Profiles of leading market participants including Excelitas, Hamamatsu Photonics, Newport Corporation, Thorlabs, and Edmund Optics, covering their product portfolios, R&D investments, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging technologies including AI-integrated thermopile detectors, MEMS-based solutions, and advanced temperature compensation techniques.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing industrial automation and demand for non-contact temperature measurement, along with challenges like material cost fluctuations.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, and investors regarding emerging opportunities in smart manufacturing and healthcare applications.

Primary and secondary research methods are employed, including interviews with industry experts, analysis of financial reports, and validation through proprietary databases to ensure data accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global High Sensitivity Thermopile Detectors Market?

-> High Sensitivity Thermopile Detectors Market was valued at US$ 134.6 million in 2024 and is projected to reach US$ 214.8 million by 2032, at a CAGR of 6.02% during the forecast period 2025-2032.

Which key companies operate in Global High Sensitivity Thermopile Detectors Market?

-> Key players include Excelitas, Hamamatsu Photonics, Newport Corporation, Thorlabs, Edmund Optics, LASER COMPONENTS, and Ophir Photonics, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for non-contact temperature measurement, growth in industrial automation, and expanding applications in medical diagnostics.

Which region dominates the market?

-> Asia-Pacific dominates with 42.5% market share in 2023, driven by manufacturing growth in China and Japan, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include MEMS-based thermopile detectors, integration with IoT systems, and development of multi-channel array detectors for advanced applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...