Market Insights

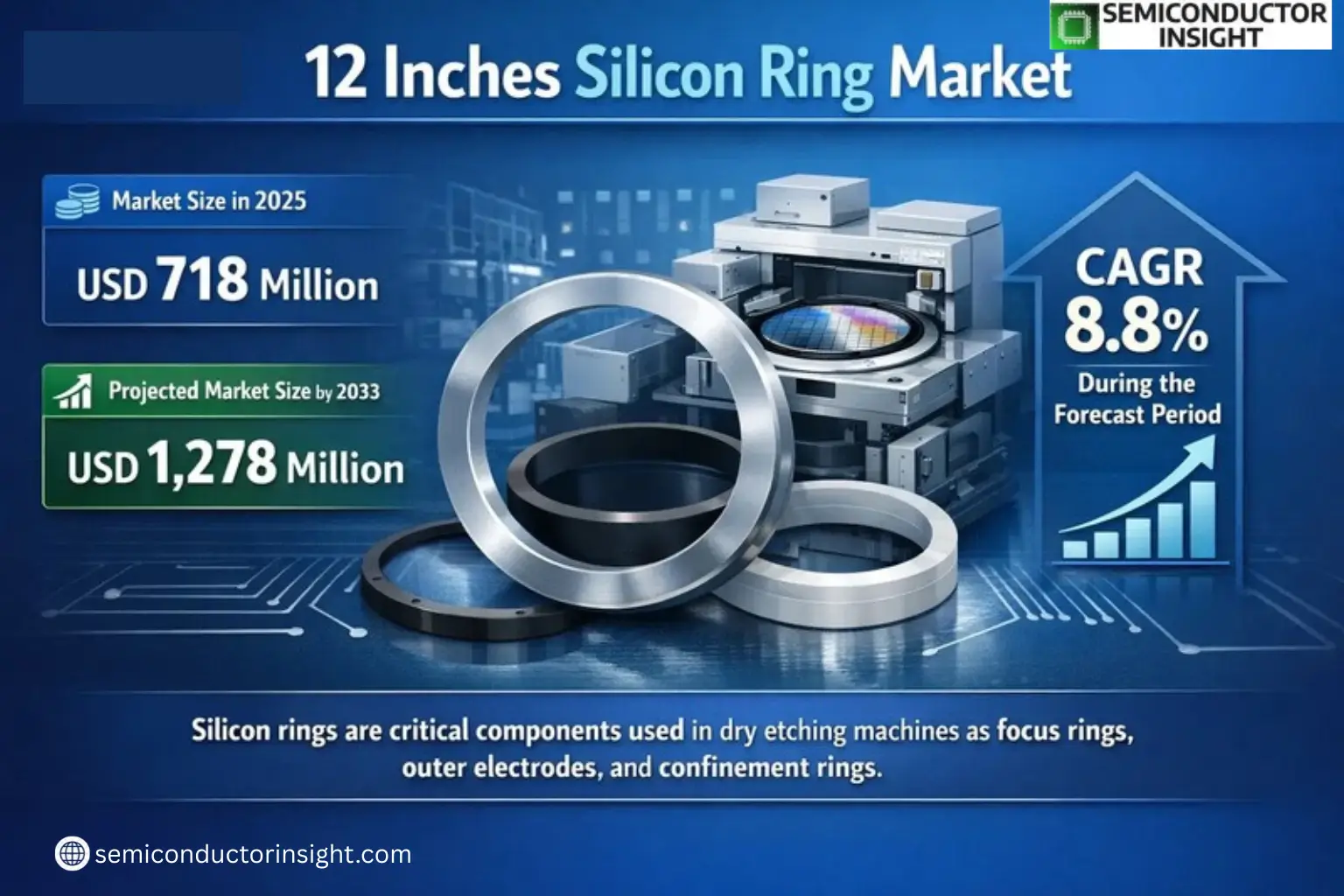

Global 12 Inches Silicon Ring Market was valued at USD 718 million in 2025 and is projected to reach USD 1,278 million by 2033, exhibiting a CAGR of 8.8% during the forecast period.

Silicon rings are critical components used in dry etching machines as focus rings, outer electrodes, and confinement rings. These high-purity silicon components are primarily utilized in 8-12 inch (200mm-300mm) plasma etchers for semiconductor manufacturing. Their electrical properties ensure uniform etching performance, making them indispensable in wafer processing. Due to wear and tear, silicon rings require periodic replacement typically after processing approximately 200 wafers driving consistent demand from semiconductor fabrication plants.

The market growth is fueled by expanding semiconductor production capacity worldwide, particularly for advanced logic and memory ICs. While the U.S., South Korea, Japan, and China dominate production, rising investments in AI, electric vehicles, and IoT applications continue to accelerate adoption. Key players such as Silfex Inc., Hana Materials Inc., and Mitsubishi Materials lead the industry with specialized manufacturing capabilities tailored for next-generation chip fabrication.

MARKET DRIVERS

Growing Semiconductor Manufacturing Demand

Global 12 Inches Silicon Ring Market is experiencing steady growth driven by the expanding semiconductor industry. As wafer sizes increase to improve production efficiency, the demand for larger diameter silicon rings has risen significantly. Foundries are adopting 12-inch wafers as the industry standard, creating consistent demand for compatible silicon rings.

Technological Advancements in Chip Production

Advancements in semiconductor manufacturing processes, including the transition to smaller node sizes, require high-precision 12 inches silicon rings. These components play a critical role in maintaining dimensional stability during wafer processing. The market benefits from increased R&D investments in semiconductor equipment.

The push for domestic semiconductor production in various regions is creating additional growth opportunities for 12 inches silicon ring manufacturers.

MARKET CHALLENGES

High Manufacturing Precision Requirements

Producing 12 inches silicon rings requires extremely tight tolerances and specialized manufacturing capabilities. The challenge of maintaining consistent quality across large-diameter products increases production complexity and costs. Even minor defects can render these components unusable in precision applications.

Other Challenges

Supply Chain Constraints

Disruptions in the global supply chain for high-purity silicon materials impact the production capacity and lead times for 12 inches silicon rings. Manufacturers must navigate complex logistics while maintaining material quality standards.

MARKET RESTRAINTS

High Capital Investment Requirements

The specialized equipment needed for 12 inches silicon ring manufacturing requires significant capital expenditure. This creates barriers to entry for new market players and limits production capacity expansions among existing manufacturers. The high initial costs also impact pricing structures across the supply chain.

MARKET OPPORTUNITIES

Emerging Applications in Advanced Packaging

The growth of advanced packaging technologies, including 2.5D and 3D IC packaging, presents new opportunities for 12 inches silicon ring applications. These rings are increasingly used in temporary bonding and debonding processes for wafer-level packaging solutions. The market stands to benefit from the semiconductor industry’s shift toward heterogeneous integration.

12 Inches Silicon Ring Market Trends

Global Market Growth and Projections

Global 12 Inches Silicon Ring Market was valued at USD 718 million in 2025 and is projected to reach USD 1,278 million by 2033, growing at a CAGR of 8.8%. This growth is driven by increasing semiconductor wafer production, particularly for applications in logic ICs, memory ICs, and other advanced processes. The periodic replacement nature of silicon rings in wafer fabrication creates consistent demand, with each ring typically requiring replacement after processing approximately 200 wafers.

Other Trends

Regional Production and Supply Chain Dynamics

Major production of 12-inch silicon rings is concentrated in the United States, South Korea, Japan, and China. Key players including Silfex Inc., Hana Materials Inc., and Mitsubishi Materials dominate the market. The semiconductor equipment industry’s expansion, coupled with emerging applications in AI and electric vehicles, is driving wafer fab construction globally and subsequently increasing silicon ring demand.

Technological Advancements and Industry Demand

As semiconductor manufacturing processes advance with smaller node sizes, the requirements for silicon ring precision and durability continue to increase. Global semiconductor market reached USD 627.6 billion in sales in 2025, with the Americas showing particularly strong growth at 44.8%. This market expansion directly correlates with increased demand for semiconductor manufacturing components including 12-inch silicon rings.

Market Segmentation and Competitive Landscape

The market is segmented into OEM and wafer fabs, with applications divided between logic IC (56%), memory IC (32%), and other processes (12%). The competitive landscape features over 20 major manufacturers, with the top five companies holding approximately 38% market share. Regional analysis shows Asia leading in consumption due to concentrated semiconductor manufacturing facilities.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Positioning in the 12-Inch Silicon Ring Market

Global 12 Inches Silicon Ring Market is dominated by established semiconductor materials specialists, with Silfex Inc. (a subsidiary of Lam Research) and Hana Materials Inc. leading the competitive landscape. These industry leaders hold significant market share due to their proprietary manufacturing technologies and direct supply relationships with major semiconductor equipment manufacturers. The market structure shows vertical integration trends, with several players expanding from silicon components into complete consumable solutions for plasma etching systems.

Niche specialists like KC Parts Tech., Ltd. and RS Technologies Co., Ltd. have gained traction through specialized coating technologies that extend ring lifespan. Emerging Chinese manufacturers such as ThinkonSemi and Chongqing Genori Technology are rapidly expanding capacity to meet domestic semiconductor production needs, though quality consistency remains a competitive differentiator for established players. The industry faces increased consolidation as material science becomes critical for advanced node fabrication.

List of Key 12-Inch Silicon Ring Companies Profiled

- Silfex Inc.

- Hana Materials Inc.

- Worldex Industry & Trading Co., Ltd.

- Mitsubishi Materials

- CoorsTek

- SiFusion

- KC Parts Tech., Ltd.

- RS Technologies Co., Ltd.

- ThinkonSemi (Fujian Dynafine)

- Techno Quartz Inc.

- Chongqing Genori Technology Co., Ltd

- Ruijiexinsheng Electronic Technology (WuXi) Co., Ltd

- One Semicon Co.,Ltd

- DS Techno

- Ronda Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

OEM segment dominates due to:

|

| By Application |

|

Memory IC segment shows strongest growth potential due to:

|

| By End User |

|

Foundries segment leads consumption due to:

|

| By Material Purity |

|

7N purity segment is gaining traction due to:

|

| By Replacement Cycle |

|

Premium replacement cycle products are seeing rising demand due to:

|

Regional Analysis: 12 Inches Silicon Ring Market

China’s Yangtze River Delta and Pearl River Delta regions concentrate the highest density of 12 inches silicon ring suppliers, supported by local quartz raw material availability and proximity to wafer fabs.

Japanese manufacturers lead in producing ultra-high purity 12 inches silicon rings with advanced surface finishing techniques critical for EUV lithography applications.

South Korea’s vertically integrated semiconductor giants drive demand for customized 12 inches silicon rings with stringent flatness requirements for memory chip production.

Malaysia and Singapore are emerging as strategic locations for 12 inches silicon ring manufacturing, benefiting from tax incentives and growing backend semiconductor operations.

North America

The North American 12 inches silicon ring market thrives on advanced semiconductor R&D activities and foundry expansions. Silicon Valley remains influential in setting technical specifications, while Arizona’s semiconductor corridor witnesses growing demand from new wafer fabrication plants. The region shows strong preference for specialty 12 inches silicon rings with coatings for extreme process conditions. Canadian manufacturers focus on niche applications in quantum computing research facilities.

Europe

Europe maintains a specialized position in the 12 inches silicon ring market through precision engineering expertise. Germany leads in supplying rings for automotive semiconductor applications, while France excels in research-grade components. The EU’s Chips Act is stimulating investments in local semiconductor ecosystems, creating opportunities for 12 inches silicon ring suppliers serving advanced packaging applications.

Middle East & Africa

The MEA region is developing semiconductor infrastructure with partnerships importing 12 inches silicon ring technology. Israel’s growing fabless semiconductor industry drives demand for high-end components, while UAE investments in tech hubs create new distribution channels for silicon ring suppliers eyeing future wafer fab projects.

South America

Brazil represents the primary market for 12 inches silicon rings in South America, mainly serving industrial electronics manufacturers. Limited local production capacity creates import opportunities, particularly for cost-competitive Asian suppliers. Chile and Argentina show emerging demand for research-grade silicon rings in academic and scientific institutions.

Report Scope

This market research report provides a comprehensive analysis of the 12 Inches Silicon Ring Market , covering the forecast period 2025–2033. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as AI, automotive, telecommunications, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 12 Inches Silicon Ring Market?

-> 12 Inches Silicon Ring Market was valued at USD 718 million in 2025 and is projected to reach USD 1,278 million by 2033, exhibiting a CAGR of 8.8% during the forecast period.

Which key companies operate in 12 Inches Silicon Ring Market?

-> Key players include Silfex Inc., Hana Materials Inc., Worldex Industry & Trading, Mitsubishi Materials, CoorsTek, SiFusion, KC Parts Tech., Ltd., RS Technologies Co., Ltd., Techno Quartz Inc., and DS Techno, among others.

What are the key growth drivers?

-> Key growth drivers include increasing semiconductor demand, advancements in chip manufacturing technology, and rising wafer fabrication plant construction globally.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by semiconductor industry expansion in China, South Korea, and Japan.

What are the emerging trends?

-> Emerging trends include increased adoption of 300mm wafer technology, AI-driven semiconductor manufacturing, and development of advanced etching techniques.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...