MARKET INSIGHTS

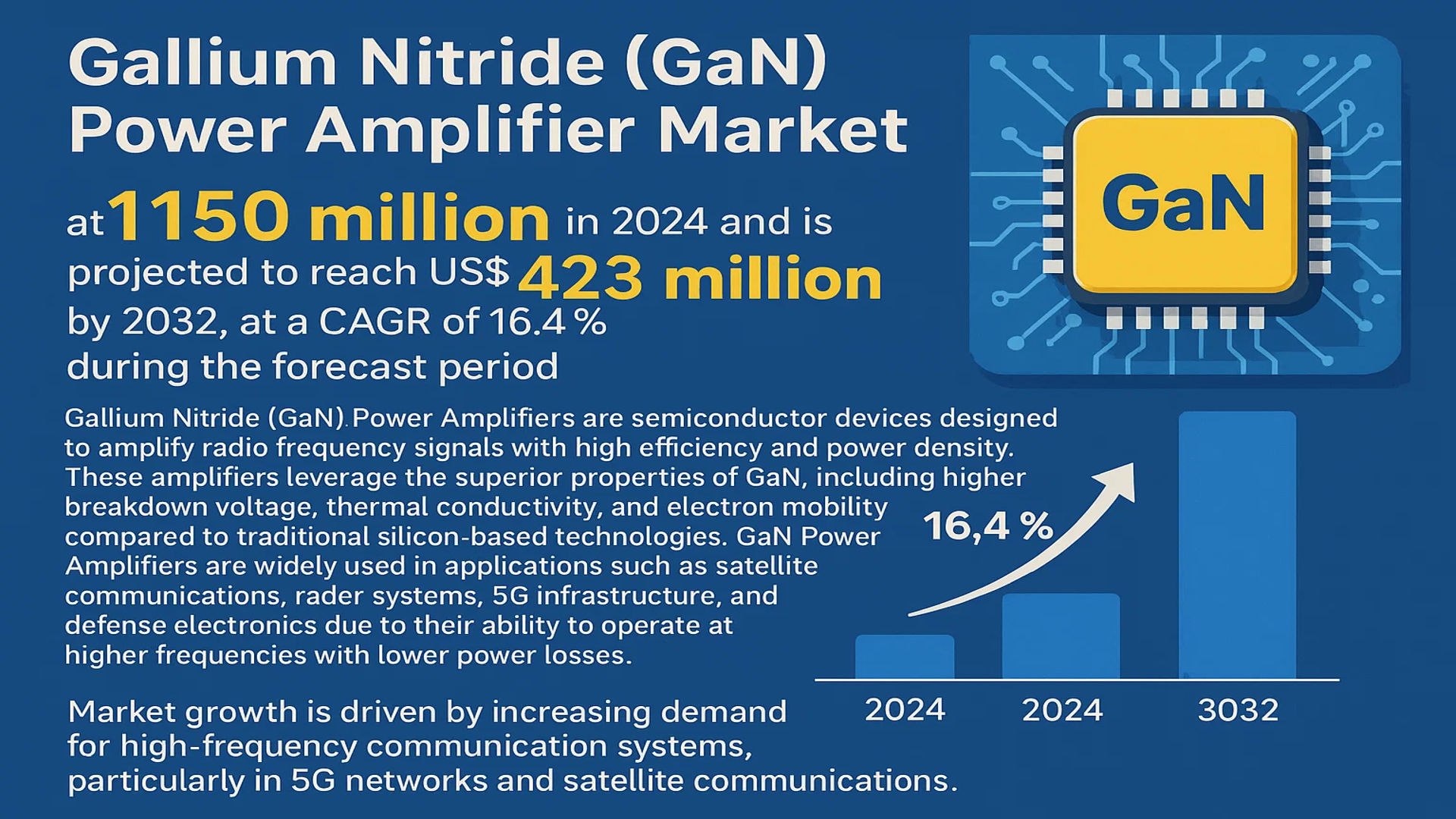

The global Gallium Nitride (GaN) Power Amplifier Market was valued at 150 million in 2024 and is projected to reach US$ 423 million by 2032, at a CAGR of 16.4% during the forecast period.

Gallium Nitride (GaN) Power Amplifiers are semiconductor devices designed to amplify radio frequency signals with high efficiency and power density. These amplifiers leverage the superior properties of GaN, including higher breakdown voltage, thermal conductivity, and electron mobility compared to traditional silicon-based technologies. GaN Power Amplifiers are widely used in applications such as satellite communications, radar systems, 5G infrastructure, and defense electronics due to their ability to operate at higher frequencies with lower power losses.

The market growth is driven by increasing demand for high-frequency communication systems, particularly in 5G networks and satellite communications. The defense sector’s growing adoption of GaN-based amplifiers for radar and electronic warfare systems is another key factor. Additionally, advancements in GaN fabrication technologies and investments by major players like MACOM, Qorvo, and Wolfspeed are accelerating market expansion. For instance, in 2023, Qorvo introduced a new line of GaN amplifiers targeting 5G base stations, reinforcing its position in the competitive landscape.

MARKET DYNAMICS

MARKET DRIVERS

Accelerated 5G Deployment to Propel GaN Power Amplifier Demand

The global rollout of 5G networks continues to gain momentum, driving substantial demand for GaN power amplifiers in base stations and small cell infrastructure. As 5G requires higher frequency bands and improved power efficiency, GaN-based solutions outperform traditional silicon alternatives with superior thermal conductivity and higher power density. With telecom operators worldwide investing over $300 billion annually in 5G infrastructure, the need for efficient RF power components is creating sustained market growth. Recent advancements in millimeter-wave technology further enhance GaN’s value proposition for 5G applications, with major network equipment providers increasingly adopting these solutions for next-generation installations.

Defense Sector Modernization Boosts Military Applications

Military modernization programs across major economies are significantly contributing to GaN power amplifier adoption. These components are becoming indispensable for advanced radar systems, electronic warfare equipment, and secure communication networks due to their ability to operate at higher frequencies with greater reliability. Global defense spending exceeding $2 trillion annually demonstrates the scale of opportunity, with defense agencies prioritizing technologies that enhance situational awareness and communication capabilities. The inherent advantages of GaN – including its radiation hardness and ability to function in extreme environments – make it particularly suitable for aerospace and defense applications that demand rugged, high-performance solutions.

➤ The U.S. Department of Defense has identified GaN as a critical technology, significantly increasing procurement budgets for GaN-based systems in recent years.

Furthermore, the growing integration of GaN amplifiers in satellite communications is expanding market potential. With the space economy projected to reach over $1 trillion by 2040, satellite operators require power-efficient amplifiers that can handle high-frequency transmissions while minimizing size and weight constraints.

MARKET RESTRAINTS

High Production Costs and Yield Challenges Limit Market Penetration

Despite technological advantages, GaN power amplifiers face significant cost barriers compared to established silicon-based alternatives. The complex manufacturing process and specialized equipment required for GaN semiconductor production contribute to unit costs that can be 30-50% higher than equivalent silicon solutions. Yield rates in GaN wafer production also lag behind more mature technologies, creating supply chain bottlenecks that hinder widespread adoption. These economic factors make price-sensitive applications hesitant to transition from silicon-based amplifiers, particularly in consumer electronics and automotive sectors where cost considerations often outweigh performance benefits.

Other Restraints

Thermal Management Complexities

While GaN offers superior thermal performance compared to silicon, managing heat dissipation in high-power applications remains technically challenging. The high power densities achievable with GaN devices require advanced packaging solutions and cooling mechanisms, adding to system complexity and cost. These thermal considerations are particularly critical in space-constrained applications where traditional cooling methods may not be viable.

Supply Chain Vulnerabilities

The GaN supply chain faces concentration risks with limited sources for high-quality GaN wafers and substrate materials. Geopolitical tensions affecting rare earth material exports and specialized manufacturing equipment further amplify these vulnerabilities, potentially disrupting production capacity during periods of peak demand.

MARKET CHALLENGES

Reliability Concerns in High-Power Applications Create Adoption Barriers

As GaN power amplifiers push into higher power ranges, reliability becomes a growing concern for mission-critical applications. While laboratory tests demonstrate impressive performance metrics, real-world deployment under continuous operation reveals potential failure modes related to electron trapping and gate degradation. These reliability challenges are particularly problematic for aerospace and defense applications where component failures can have catastrophic consequences. Manufacturers must invest heavily in accelerated life testing and reliability engineering to build confidence among conservative industries that typically prefer proven silicon-based solutions with established track records.

Other Challenges

Design Complexity

The unique characteristics of GaN devices require specialized design expertise that remains scarce in the engineering community. Many system designers accustomed to silicon technologies struggle to fully leverage GaN’s potential due to differing biasing requirements, matching networks, and thermal considerations. This knowledge gap slows adoption as companies must invest in retraining or hiring specialized personnel.

Standardization Gaps

The lack of industry-wide standards for GaN device characterization and qualification complicates system integration efforts. Without standardized testing protocols and performance benchmarks, comparing solutions across vendors becomes challenging, potentially delaying procurement decisions in conservative industries.

MARKET OPPORTUNITIES

Emerging Compound Semiconductor Ecosystem Presents Growth Potential

The development of a robust GaN ecosystem creates multiple growth opportunities across the value chain. Material science advancements are improving substrate quality and reducing defects, while packaging innovations address thermal and reliability concerns. Collaborative research initiatives between academia and industry are accelerating technology maturation, with recent breakthroughs in 200mm GaN-on-silicon production potentially reducing costs by 40% compared to traditional methods. These advancements open new possibilities for GaN power amplifiers in cost-sensitive markets that previously couldn’t justify the premium pricing.

Electrification Wave Creates New Application Verticals

The global transition toward electrification across automotive, industrial, and energy sectors presents significant opportunities for GaN technology. Electric vehicles require efficient power conversion systems where GaN amplifiers can enable faster charging and improved energy management. Similarly, renewable energy systems benefit from GaN’s high-frequency capabilities in power conditioning and grid-tie applications. As industries seek more efficient power electronics solutions to meet sustainability goals, GaN amplifiers are well-positioned to capture share in these emerging high-growth markets.

Furthermore, the expanding Internet of Things (IoT) ecosystem demands compact, energy-efficient RF components for edge devices and sensors. GaN’s ability to deliver high performance in small form factors makes it ideal for next-generation wireless infrastructure supporting massive IoT deployments, potentially creating a multi-billion dollar addressable market in the coming decade.

GALLIUM NITRIDE (GAN) POWER AMPLIFIER MARKET TRENDS

5G Deployment Acceleration Drives GaN Power Amplifier Demand

The global rollout of 5G networks is significantly boosting the Gallium Nitride (GaN) power amplifier market, as these high-frequency components are essential for next-generation communication infrastructure. With over 300 commercial 5G networks launched worldwide by mid-2024, telecom operators increasingly prefer GaN-based solutions over traditional silicon alternatives due to their superior power efficiency at higher frequencies. The 3.5 GHz segment, crucial for 5G implementation, is witnessing particularly strong growth as it offers an optimal balance between coverage and capacity. Furthermore, recent advancements in wideband GaN technology have enabled single amplifiers to cover multiple 5G frequency bands, reducing system complexity while improving performance.

Other Trends

Defense Modernization Programs

Increased defense spending across multiple nations is creating substantial opportunities for GaN power amplifiers in radar and electronic warfare applications. These components are becoming vital for modern phased array radar systems due to their ability to handle high power densities and operate efficiently at microwave frequencies. The U.S. Department of Defense has accelerated its transition from legacy gallium arsenide (GaAs) to GaN-based systems across multiple platforms, including airborne early warning systems and naval radars. Similar modernization initiatives are underway in Europe and Asia-Pacific as defense agencies seek improved reliability and thermal performance in harsh operational environments.

Satellite Communication Expansion

The growing demand for high-throughput satellite (HTS) systems and low Earth orbit (LEO) constellations is fueling adoption of GaN power amplifiers in the space communications sector. Compared to traditional technologies, GaN-based amplifiers offer 30-40% higher power efficiency at frequencies above 12 GHz, making them ideal for satellite payloads where power consumption directly impacts operational costs. Recent developments in radiation-hardened GaN solutions have further strengthened their position in space applications, with several major satellite operators now specifying GaN amplifiers as standard components for new constellations. The commercial space sector alone is projected to require over 50,000 GaN amplifier units annually by 2026 to support ongoing mega-constellation deployments.

Manufacturing and Material Innovations

Breakthroughs in GaN epitaxial growth techniques and device packaging are driving down production costs while improving reliability. The transition from 4-inch to 6-inch wafer processing has increased manufacturing yields by 15-20% since 2022, making GaN amplifiers more cost-competitive with silicon alternatives. At the device level, new monolithic microwave integrated circuit (MMIC) designs integrate multiple amplifier stages into single chips, reducing footprint and improving thermal management. Industry leaders are also developing enhanced thermal interface materials and advanced packaging solutions to address thermal dissipation challenges, a critical factor in high-power RF applications where junction temperatures can exceed 200°C.

COMPETITIVE LANDSCAPE

Key Industry Players

GaN Power Amplifier Market Sees Intensifying Competition as Companies Innovate for 5G and Defense Applications

The global Gallium Nitride (GaN) Power Amplifier market represents a dynamic competitive landscape where established semiconductor giants compete with specialized RF component manufacturers. The market is currently experiencing rapid growth, projected to expand from $150 million in 2024 to $423 million by 2032 at a 16.4% CAGR, driven by surging demand in 5G infrastructure, satellite communications, and defense applications.

MACOM Technology Solutions and Qorvo currently lead the GaN power amplifier segment, particularly in high-frequency applications above 3.5 GHz. Their dominance stems from proprietary GaN-on-SiC (Silicon Carbide) manufacturing processes that deliver superior power density and thermal performance. MACOM’s recent acquisition of OMMIC SAS strengthened its millimeter-wave capabilities, positioning it strongly for emerging 5G mmWave markets.

Meanwhile, Wolfspeed (a Cree company) leverages its vertical integration—from GaN epitaxial wafers to finished amplifiers—to maintain cost advantages. The company continues expanding its 50 GHz product line, targeting satellite payload and radar applications where its low-noise, high-efficiency amplifiers demonstrate competitive differentiation.

Several players are pursuing strategic collaborations to accelerate market penetration. RFHIC recently partnered with a major Korean telecom provider to co-develop GaN amplifiers for Open RAN infrastructure, while Microchip Technology acquired Biorad Haematology Technology to complement its defense-focused amplifier solutions.

List of Key Gallium Nitride (GaN) Power Amplifier Manufacturers

- MACOM Technology Solutions (U.S.)

- Qorvo, Inc. (U.S.)

- Wolfspeed (Cree) (U.S.)

- RFHIC Corporation (South Korea)

- Aethercomm Inc. (U.S.)

- Microchip Technology (U.S.)

- Fraunhofer IAF (Germany)

- Mercury Systems (U.S.)

- CETC13 (China)

- NuWaves Engineering (U.S.)

Mid-sized innovators like Aethercomm and NuWaves Engineering are carving out specialized niches—Aethercomm focusing on high-reliability military communications amplifiers, while NuWaves leads in compact, lightweight designs for UAV payloads. These companies demonstrate how the market accommodates both broad-line suppliers and application-specific specialists.

The competitive landscape continues evolving with Chinese players like CETC13 and CETC55 gaining traction through government-backed 5G infrastructure projects. Their increasing market participation underscores the strategic importance of GaN technology in next-generation wireless and defense systems globally.

Segment Analysis:

By Type

3.5 GHz Frequency Segment Leads Market Due to High Demand in 5G and Satellite Communication

The GaN Power Amplifier market is segmented based on frequency into:

- 3.5 GHz

- 4 GHz

- 12 GHz

- 50 GHz

- Others

By Application

5G Technology Segment Drives Growth with Expanding Telecommunication Infrastructure

The market is segmented based on key application areas into:

- Satellite Communications

- Radar Systems

- 5G Technology

- Electronics and Semiconductors

- Defense and Aerospace

- Others

By End-User

Telecommunication Providers Dominate Adoption Due to Network Expansion Requirements

The market is segmented based on end-users into:

- Telecommunication Service Providers

- Defense Contractors

- Electronics Manufacturers

- Research Institutions

- Others

By Component

Discrete Power Amplifiers Maintain Strong Market Presence Due to Design Flexibility

The market is segmented based on component type into:

- Discrete Power Amplifiers

- Integrated Power Amplifiers

- Power Amplifier Modules

Regional Analysis: Gallium Nitride (GaN) Power Amplifier Market

Asia-Pacific

The Asia-Pacific region dominates the global GaN power amplifier market, driven by rapid 5G infrastructure deployment and robust semiconductor manufacturing in China, South Korea, and Japan. China accounts for over 40% of the regional market share, fueled by government initiatives like “Made in China 2025” that prioritize advanced RF component development. India’s expanding telecom sector and Japan’s leadership in precision electronics further accelerate adoption. While cost sensitivity exists for commercial applications, defense modernization programs across the region are creating high-value opportunities for GaN-based solutions.

North America

Home to semiconductor innovators like Qorvo and MACOM, North America maintains technological leadership in GaN power amplifier design. The U.S. Department of Defense’s $842 billion FY2024 budget allocates significant funding for GaN-based radar and electronic warfare systems. Commercial demand stems from telecom operators accelerating C-band (3.5 GHz) deployments for 5G. Regulatory pressures for energy-efficient RF solutions and strong venture capital investment in GaN startups ($280 million in 2023) position the region for sustained innovation.

Europe

Europe’s GaN amplifier market grows steadily through defense modernization and automotive radar applications, with Germany and the UK leading adoption. The EU’s Horizon Europe program funds GaN research for satellite communications (SATCOM) and 6G development. However, fragmented spectrum allocation policies across member states complicate 5G rollouts affecting commercial demand. Key players like Infineon and NOKIA leverage the region’s strong academic-industrial partnerships to develop next-generation GaN solutions meeting strict EU emissions standards.

Middle East & Africa

This emerging market shows promising growth through satellite communication deployments and oil/gas sector investments. The UAE’s $2 billion investment in Yahsat and Saudi Arabia’s Vision 2030 drive demand for GaN amplifiers in SATCOM ground stations. Limited local manufacturing capabilities create import dependence, though partnerships like Egypt’s cooperation with STMicroelectronics aim to develop regional production. Military modernization programs increasingly specify GaN for electronic warfare systems, albeit constrained by budget limitations.

South America

The region exhibits nascent but growing GaN adoption, primarily in Brazil’s aerospace sector and Argentina’s telecom infrastructure projects. Economic volatility and currency fluctuations hinder large-scale deployments, though foreign direct investment in Brazilian 5G networks presents opportunities. The lack of local semiconductor fabrication forces reliance on imports, creating supply chain vulnerabilities. Emerging applications in satellite-based internet services may drive future growth if political stability improves.

Technology Focus: Across all regions, the 3.5 GHz GaN amplifier segment shows strongest growth (projected 18.2% CAGR) due to 5G mid-band spectrum adoption. Defense applications prefer higher frequency models (12-50 GHz) for radar and electronic warfare systems, maintaining stable demand despite higher costs.

Report Scope

This market research report provides a comprehensive analysis of the Global Gallium Nitride (GaN) Power Amplifier market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global GaN Power Amplifier market was valued at USD 150 million in 2024 and is projected to reach USD 423 million by 2032, growing at a CAGR of 16.4%.

- Segmentation Analysis: Detailed breakdown by product type (3.5 GHz, 4 GHz, 12 GHz, 50 GHz, Others), technology, application (Satellite Communications, Radar, 5G Technology, Electronics and Semiconductors, Defense and Aerospace, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America (U.S., Canada, Mexico), Europe (Germany, France, U.K., Italy, Russia), Asia-Pacific (China, Japan, South Korea, India), Latin America, and Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants including RFHIC, MACOM, Qorvo, Wolfspeed, and Microchip Technology, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT in power amplifier design, semiconductor fabrication techniques, and evolving industry standards in GaN technology.

- Market Drivers & Restraints: Evaluation of factors driving market growth (5G deployment, defense spending, satellite communications) along with challenges (supply chain constraints, regulatory issues, and high manufacturing costs).

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving GaN ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global GaN Power Amplifier Market?

-> Gallium Nitride (GaN) Power Amplifier Market was valued at 150 million in 2024 and is projected to reach US$ 423 million by 2032, at a CAGR of 16.4% during the forecast period.

Which key companies operate in Global GaN Power Amplifier Market?

-> Key players include RFHIC, MACOM, Qorvo, Wolfspeed, Microchip Technology, Aethercomm Inc, API Technologies, and Fairview Microwave, among others.

What are the key growth drivers?

-> Key growth drivers include 5G network deployment, increasing defense applications, satellite communication expansion, and demand for high-frequency electronics.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is projected to be the fastest-growing region due to 5G infrastructure development.

What are the emerging trends?

-> Emerging trends include integration with AI for smart amplification, development of wide-bandgap semiconductors, and miniaturization of GaN components for next-gen applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...