MARKET INSIGHTS

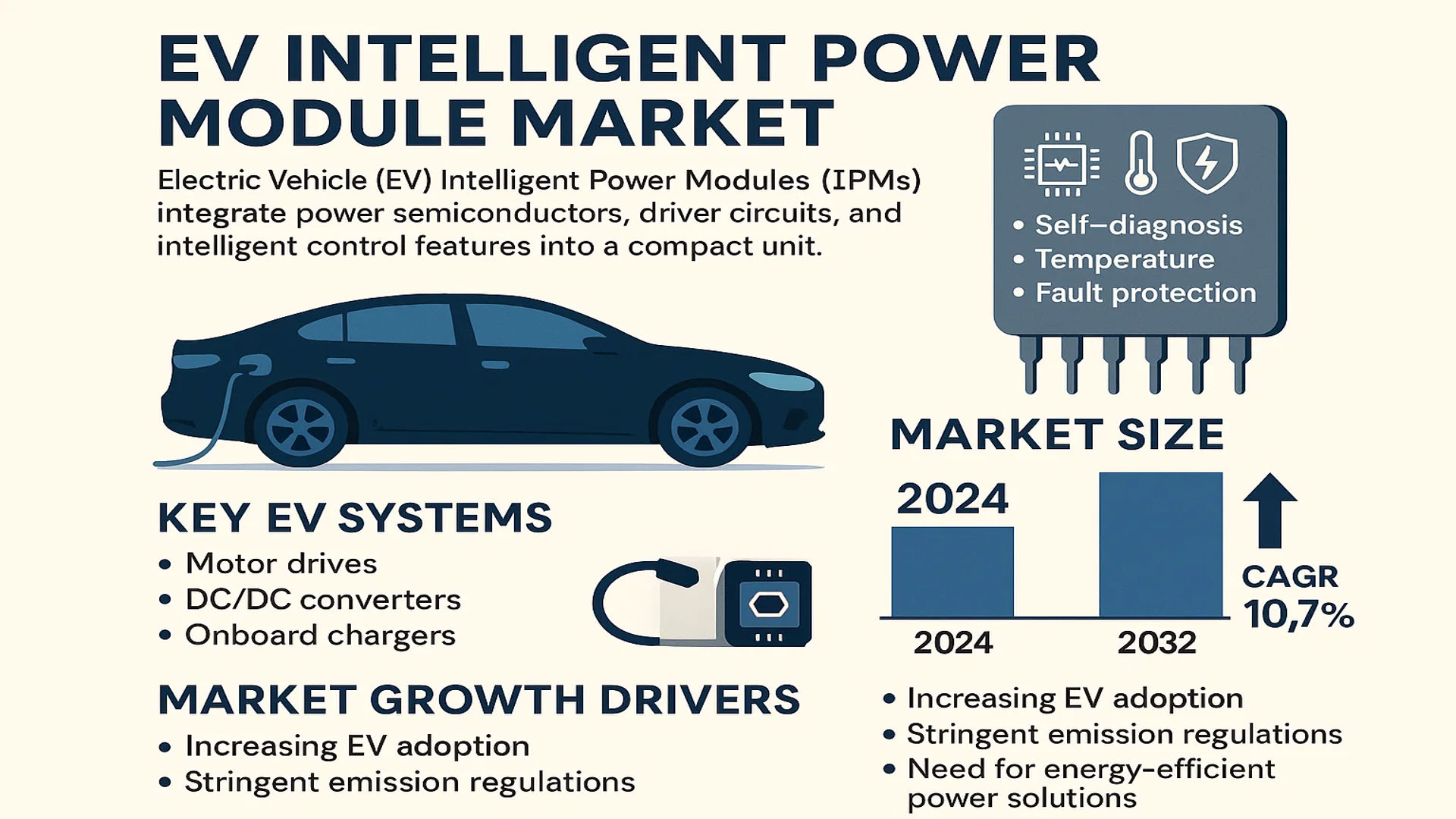

The global EV Intelligent Power Module Market was valued at 1527 million in 2024 and is projected to reach US$ 3096 million by 2032, at a CAGR of 10.7% during the forecast period.

Electric Vehicle (EV) Intelligent Power Modules (IPMs) are advanced power electronics components that integrate power semiconductors, driver circuits, and intelligent control features into a single compact unit. These modules enhance system efficiency and reliability in EVs by enabling functions such as self-diagnosis, temperature monitoring, and fault protection. IPMs play a critical role in key EV systems including motor drives, DC/DC converters, and onboard chargers.

The market growth is driven by increasing EV adoption, stringent emission regulations, and the need for energy-efficient power solutions. However, high manufacturing costs and thermal management challenges may restrain expansion. Key players like Infineon, STMicroelectronics, and Renesas dominate the market with their innovative IPM solutions. For instance, in 2023, Infineon launched its latest CoolSiC™ MOSFET-based IPM series, optimized for high-performance EV applications, demonstrating the industry’s focus on technological advancements.

MARKET DYNAMICS

MARKET DRIVERS

Accelerated Adoption of Electric Vehicles to Fuel Demand for Intelligent Power Modules

The global transition toward electric vehicles is creating unprecedented demand for intelligent power modules (IPMs). With electric vehicle sales projected to grow at a compound annual growth rate of over 25% through 2030, automotive manufacturers are increasingly relying on IPMs to enhance vehicle performance and efficiency. These modules play a critical role in power conversion and motor control systems, offering superior thermal management and energy efficiency compared to conventional power components. As governments worldwide implement stricter emission regulations, automakers are accelerating their EV production schedules, directly boosting IPM adoption.

Advancements in Semiconductor Technology Driving Innovation in IPM Design

Recent breakthroughs in semiconductor materials and packaging technologies are enabling significant improvements in IPM performance. Wide-bandgap semiconductors like silicon carbide (SiC) and gallium nitride (GaN) are being increasingly integrated into IPMs, delivering higher switching frequencies and reduced energy losses. Modern IPMs now feature advanced functionalities including real-time temperature monitoring, adaptive gate drivers, and fault detection capabilities. Leading manufacturers have successfully reduced module sizes by nearly 30% while increasing power density – a critical factor for space-constrained EV applications.

Growing Investment in EV Infrastructure Creating Expansion Opportunities

The rapid expansion of EV charging infrastructure worldwide is generating substantial demand for IPMs in DC fast charging stations and onboard charging systems. With annual investments in charging infrastructure exceeding $20 billion globally, IPM manufacturers are developing specialized modules optimized for high-power applications. These modules enable faster charging times while maintaining system reliability, addressing one of the key concerns in EV adoption. The integration of smart grid technologies with charging stations further increases the value proposition of intelligent power solutions.

MARKET RESTRAINTS

High Manufacturing Costs and Complex Supply Chains Limiting Market Penetration

While IPM technology offers significant advantages, its adoption faces challenges due to complex manufacturing processes and associated costs. The production of advanced power modules requires specialized fabrication facilities and stringent quality control measures, resulting in premium pricing that can be 40-50% higher than conventional power components. The current global semiconductor shortage has further exacerbated supply chain constraints, with lead times for certain IPM components extending beyond six months in some cases. These factors create barriers to entry for smaller EV manufacturers and aftermarket suppliers.

Thermal Management Challenges in High-Power Applications

Thermal performance remains a critical constraint for IPMs in demanding EV applications. As power density requirements increase, managing heat dissipation becomes increasingly challenging. Operating temperatures above 150°C can significantly reduce module lifespan and reliability. While advanced cooling solutions are being developed, the additional costs and packaging complexity they introduce present trade-offs for designers. This thermal limitation is particularly evident in commercial vehicle applications where power demands are substantially higher than passenger vehicles.

Design Complexity and Integration Hurdles in Next-Generation EVs

The integration of IPMs into sophisticated EV powertrain systems requires extensive engineering expertise and specialized design tools. Vehicle manufacturers often face challenges in optimizing the interaction between power modules, control algorithms, and vehicle architecture. The lack of standardized interfaces across different OEM platforms further complicates system integration. These technical complexities extend development timelines and increase validation costs, potentially slowing the pace of innovation in some market segments.

MARKET OPPORTUNITIES

Emergence of 800V Vehicle Architectures Creating New Market Potential

The shift toward 800V electrical systems in premium EVs represents a significant growth opportunity for IPM manufacturers. These high-voltage architectures require fundamentally different power module designs capable of handling increased voltage stresses while maintaining efficiency. Early adopters of 800V technology have demonstrated charging times under 20 minutes, addressing a key consumer concern. As more automakers transition to higher voltage platforms, specialized IPMs optimized for these applications will command premium pricing and higher margins.

Expansion of ADAS Features Driving Demand for Auxiliary Power Modules

The proliferation of advanced driver assistance systems (ADAS) in modern vehicles is creating new applications for intelligent power solutions. High-performance computing platforms powering autonomous driving features require sophisticated power management and distribution systems. IPMs designed specifically for ADAS applications are emerging as critical components, providing reliable power conversion while meeting stringent automotive safety standards. With ADAS penetration rates exceeding 60% in new vehicles, this represents a substantial adjacent market for power module suppliers.

Strategic Collaborations Between Semiconductor and Automotive Companies

The EV power electronics market is witnessing increased collaboration between semiconductor manufacturers and automotive OEMs. These partnerships are focused on developing application-specific IPM solutions that optimize performance for particular vehicle platforms. By working directly with automakers, component suppliers can better address unique thermal, packaging, and reliability requirements. Several major automotive groups have recently announced long-term supply agreements with power semiconductor companies, ensuring technology co-development and supply chain stability.

MARKET CHALLENGES

Intense Competition and Price Pressure in Mature Market Segments

The IPM market faces growing price competition as the technology becomes more mainstream in EV applications. Established semiconductor companies are competing with emerging Asian manufacturers who are aggressively pursuing market share through cost-optimized solutions. This competitive dynamic has led to margin compression in certain product categories, particularly for standard IPMs used in entry-level EVs. Manufacturers must balance cost reduction initiatives with continued investment in next-generation technologies to maintain competitiveness.

Rapid Technological Obsolescence and Short Product Lifecycles

The fast pace of innovation in power electronics creates challenges related to product obsolescence. New semiconductor materials and packaging technologies are being introduced at unprecedented rates, making it difficult for manufacturers to recoup development investments. Automotive qualification cycles can extend beyond two years, creating potential mismatches between product availability and evolving technical requirements. Companies must carefully manage their R&D pipelines to ensure timely introduction of competitive solutions while minimizing obsolete inventory risks.

Geopolitical Factors Impacting Semiconductor Supply Chains

Recent geopolitical tensions and trade restrictions have introduced new uncertainties in the power semiconductor supply chain. Export controls on advanced chip manufacturing equipment, combined with regionalization trends in high-tech industries, are forcing IPM manufacturers to reassess their production and sourcing strategies. The concentration of key semiconductor materials and manufacturing capabilities in specific geographic regions creates potential vulnerabilities that could impact product availability and pricing stability.

EV INTELLIGENT POWER MODULE MARKET TRENDS

Rising Electric Vehicle Adoption Driving Demand for Intelligent Power Modules

The global shift toward electric vehicles (EVs) is significantly boosting the demand for Intelligent Power Modules (IPMs) due to their critical role in optimizing energy efficiency and system reliability in EV powertrains. With the EV market projected to grow at a compound annual growth rate (CAGR) of 10.7%, reaching $3096 million by 2032, IPMs are emerging as a cornerstone technology. Their ability to integrate power semiconductors, fault protection, and intelligent control functions makes them indispensable in motor drives, DC/DC converters, and onboard charging systems. Recent advancements in wide-bandgap semiconductors (SiC and GaN) have further enhanced IPM performance, enabling faster switching speeds and reduced energy losses.

Other Trends

Automotive Electrification and Integration of Advanced Driver-Assistance Systems (ADAS)

The rapid expansion of ADAS and infotainment systems in modern EVs is fueling demand for specialized IPMs, particularly Infotainment SiP Modules, which are expected to grow significantly by 2032. As passenger and commercial EV manufacturers prioritize enhanced safety and connectivity, the need for compact, high-efficiency power solutions is accelerating. Furthermore, the increasing deployment of vehicle-to-grid (V2G) technologies is pushing IPM innovation, as these modules must support bidirectional power flow while maintaining thermal stability and fault resilience.

Regional Growth and Supply Chain Development

Regionally, China and the U.S. are leading the EV IPM market, with China poised to account for a substantial share due to its aggressive EV adoption policies and strong semiconductor manufacturing base. Meanwhile, European nations are investing heavily in localized production to reduce dependency on imports, driven by stringent emission regulations and subsidies for EV components. Key industry players, including Infineon, STMicroelectronics, and Renesas, are expanding their production capacities and forming strategic partnerships to meet rising demand, ensuring a stable supply chain despite geopolitical uncertainties.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Leaders Push Innovation Boundaries in EV Power Electronics

The global EV Intelligent Power Module (IPM) market features a highly competitive ecosystem dominated by semiconductor giants and specialized power electronics firms. Infineon Technologies emerges as the market leader with a 23% revenue share in 2024, driven by its proprietary CoolSiC™ MOSFET technology that enhances power density and thermal efficiency in EV applications. The company maintains strategic partnerships with major automakers including BMW and BYD.

STMicroelectronics follows closely with 19% market share, credited to its SLLIMM™ IPM series that integrates IGBTs with advanced driver ICs. The company recently expanded production capacity in Singapore to meet growing demand from Asian EV manufacturers. Meanwhile, Renesas Electronics captured 15% market share through its innovative IPM solutions featuring built-in self-protection functions and ultra-low power losses.

Japanese players ROHM Semiconductor and Toshiba Electronic Devices collectively account for 22% of the market, leveraging their expertise in high-voltage power modules. ROHM’s SiC-based IPMs demonstrate 30% higher energy efficiency compared to conventional silicon solutions, making them particularly suitable for premium EV models. The company is investing $512 million to double its SiC production capacity by 2026.

While established players dominate, emerging competitors are gaining traction through specialized solutions. onsemi saw 42% year-over-year growth in its EV power module business after introducing the VE-Trac™ Dual platform that reduces system costs by 15% through higher integration. Similarly, Diodes Incorporated made strategic moves by acquiring Taiwan-based industrial power module specialist Lite-On Semiconductor in 2023.

List of Key EV Intelligent Power Module Manufacturers

- Infineon Technologies AG (Germany)

- STMicroelectronics (Switzerland)

- Renesas Electronics Corporation (Japan)

- ROHM Semiconductor (Japan)

- Toshiba Electronic Devices & Storage Corporation (Japan)

- Fuji Electric Co., Ltd. (Japan)

- onsemi (U.S.)

- Diodes Incorporated (U.S.)

- Microchip Technology Inc. (U.S.)

- Texas Instruments Incorporated (U.S.)

The competitive environment continues to intensify as companies expand production capacities and forge alliances with auto OEMs. Strategic collaborations are becoming increasingly common, such as Infineon’s joint development agreement with Hyundai-Kia to co-design next-generation 800V IPMs. Such partnerships are expected to reshape market dynamics as the industry transitions toward higher voltage architectures and wide-bandgap semiconductors.

Segment Analysis:

By Type

Infotainment SiP Modules Lead Due to Increasing Demand for Advanced In-Vehicle Entertainment Systems

The market is segmented based on type into:

- Infotainment SiP Modules

- Driver Assistance SiP Modules

- Voice Control SiP Modules

- Others

By Application

Passenger Cars Dominate the Market With Rising Consumer Preference for Electric Vehicles

The market is segmented based on application into:

- Passenger Cars

- Commercial Cars

By Voltage Level

High-Voltage Modules Capture Significant Share for Their Use in EV Powertrain Systems

The market is segmented based on voltage level into:

- High-Voltage IPMs

- Low-Voltage IPMs

- Medium-Voltage IPMs

By Integration Level

Fully Integrated Modules Gain Traction for Their Space-Saving and Efficiency Benefits

The market is segmented based on integration level into:

- Discrete Modules

- Semi-Integrated Modules

- Fully Integrated Modules

Regional Analysis: EV Intelligent Power Module Market

Asia-Pacific

Asia-Pacific dominates the global EV Intelligent Power Module market, with China leading as the largest producer and consumer of EV components. The region benefits from strong government support for electric vehicle adoption, extensive manufacturing infrastructure, and the presence of major semiconductor companies like ROHM and Toshiba. China’s aggressive EV subsidies and ‘Made in China 2025’ policy are accelerating demand for high-efficiency IPMs, particularly in motor drive and charging applications. Other key markets like Japan and South Korea contribute significantly due to their advanced automotive and electronics industries. Local players are investing heavily in R&D to develop compact, high-power-density modules tailored for next-generation EVs.

North America

Stringent vehicle emission standards and increasing EV adoption are driving robust growth in North America’s IPM market. The U.S. accounts for over 75% of regional demand, supported by federal incentives like the Inflation Reduction Act and investments from automakers transitioning to electrified fleets. Canadian and Mexican markets are emerging, leveraging their proximity to U.S. automotive hubs. Key suppliers like Texas Instruments and onsemi are focusing on silicon carbide (SiC)-based IPMs to meet the growing need for high-voltage applications in premium EVs. However, reliance on Asian semiconductor supply chains presents challenges for manufacturing localization.

Europe

Europe represents a technologically advanced market where strict CO2 emission regulations (95g/km mandate) are accelerating EV production. Germany leads with its strong automotive sector, while Nordic countries show the highest EV penetration rates. The EU’s focus on energy-efficient mobility has spurred development of innovative IPM solutions from European semiconductor leaders like Infineon and STMicroelectronics. These companies are pioneering wide-bandgap semiconductor technologies to enhance power efficiency in European EV platforms. Supply chain localization initiatives under the European Chips Act aim to reduce dependence on external suppliers for critical power electronics components.

South America

The South American EV IPM market remains nascent but shows promising growth potential. Brazil and Argentina are the primary markets, where gradual EV adoption and developing charging infrastructure are creating opportunities. Local production is limited, with most modules imported from Asia and Europe. Economic instability and inconsistent EV policies currently hinder market expansion. However, recent investments in lithium mining for batteries could stimulate regional EV manufacturing, creating long-term demand for power modules. Local automakers are starting strategic partnerships with global IPM suppliers to develop cost-effective solutions for the price-sensitive South American market.

Middle East & Africa

This region represents a minor but rapidly evolving market for EV power modules. Wealthier Gulf nations like UAE and Saudi Arabia are investing in EV infrastructure and local assembly plants as part of economic diversification plans. Africa’s market remains constrained by limited EV adoption outside South Africa and Morocco. While there’s growing interest in electric mobility solutions, the lack of local semiconductor manufacturing means the region will likely remain dependent on imports. Some governments are introducing incentives to attract foreign EV component manufacturers, but widespread IPM adoption faces challenges from inadequate charging networks and electricity reliability issues.

Report Scope

This market research report provides a comprehensive analysis of the Global EV Intelligent Power Module (IPM) market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global EV IPM market was valued at USD 1,527 million in 2024 and is projected to reach USD 3,096 million by 2032, growing at a CAGR of 10.7%.

- Segmentation Analysis: Detailed breakdown by product type (Infotainment SiP Modules, Driver Assistance SiP Modules, Voice Control SiP Modules, Others), application (Passenger Cars, Commercial Cars), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (U.S., Canada, Mexico), Europe (Germany, France, U.K., Italy), Asia-Pacific (China, Japan, South Korea), and other regions.

- Competitive Landscape: Profiles of leading market participants including STMicroelectronics, Infineon, ROHM, Renesas, and Fuji Electric, covering their product portfolios, market share, and strategic developments.

- Technology Trends & Innovation: Assessment of semiconductor integration, intelligent control features, and energy efficiency improvements in EV power modules.

- Market Drivers & Restraints: Evaluation of factors such as EV adoption rates, government regulations, and supply chain challenges impacting market growth.

- Stakeholder Analysis: Strategic insights for automakers, component suppliers, and investors regarding the evolving EV power electronics ecosystem.

The research methodology combines primary interviews with industry experts and analysis of verified market data from reliable sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global EV Intelligent Power Module Market?

-> EV Intelligent Power Module Market was valued at 1527 million in 2024 and is projected to reach US$ 3096 million by 2032, at a CAGR of 10.7% during the forecast period.

Which key companies operate in Global EV Intelligent Power Module Market?

-> Key players include STMicroelectronics, Infineon, ROHM, Renesas, Fuji Electric, Texas Instruments, and Toshiba, among others.

What are the key growth drivers?

-> Key growth drivers include rising EV adoption, government incentives, and demand for energy-efficient power solutions in electric vehicles.

Which region dominates the market?

-> Asia-Pacific leads the market due to strong EV production in China and Japan, while Europe shows rapid growth with stringent emission regulations.

What are the emerging trends?

-> Emerging trends include integration of AI in power management, wide-bandgap semiconductors, and modular IPM designs for enhanced performance.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...