MARKET INSIGHTS

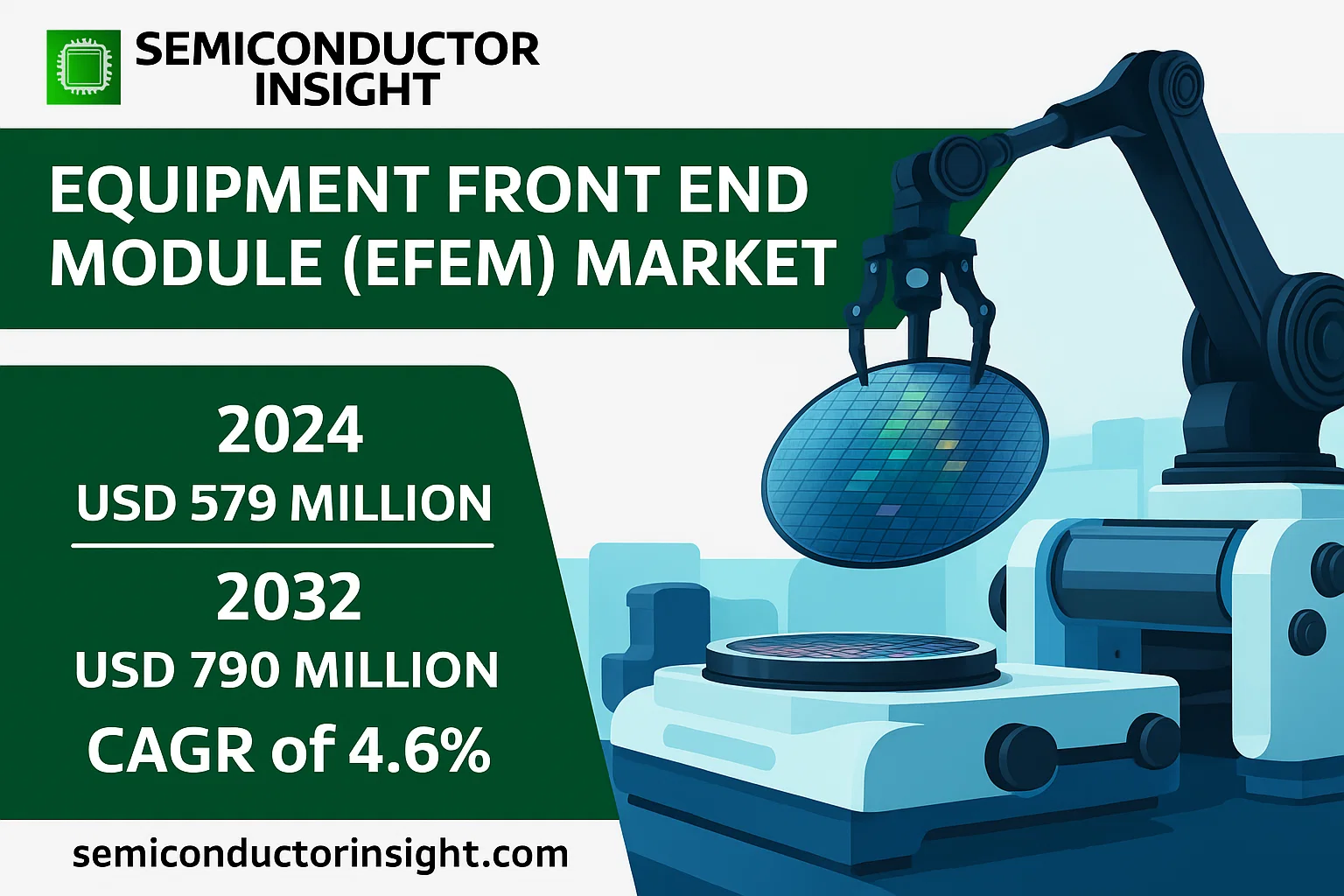

Global Equipment Front End Module (EFEM) Market was valued at USD 579 million in 2024 and is projected to reach USD 790 million by 2032, exhibiting a CAGR of 4.6% during the forecast period. This growth is primarily attributed to the increasing adoption of automation in semiconductor manufacturing, the rising demand for higher precision in wafer handling, and the expansion of the semiconductor industry across emerging economies.

Equipment Front End Modules (EFEM) are critical components in semiconductor fabrication facilities, responsible for the automated handling, alignment, and transfer of silicon wafers between processing equipment and storage units. These systems ensure contamination-free transport and precise positioning, which is crucial for maintaining yield rates in advanced semiconductor manufacturing. The market encompasses various types including 2-port, 3-port, and 4-port configurations, with the 3-port segment holding the largest market share of approximately 50% due to its balanced functionality between loading and processing requirements.

The market’s expansion is further driven by substantial investments in semiconductor capacity expansion globally, particularly in regions like Taiwan, South Korea, and China. For instance, Taiwan Semiconductor Manufacturing Company (TSMC) alone has allocated over USD 28 billion in capital expenditure for 2024, focusing on advanced process nodes which require sophisticated EFEM solutions. Similarly, Samsung Electronics and SK Hynix are accelerating their investments in semiconductor fabrication facilities, further propelling demand for wafer handling automation equipment including EFEMs.

Regionally, Asia Pacific dominates the market, accounting for over 65% of global revenue, followed by North America and Europe. This distribution aligns with the concentration of semiconductor fabrication plants (fabs) in these regions, with Taiwan, South Korea, and China being the primary contributors. Recent data from SEMI indicates that global semiconductor equipment spending will reach USD 100 billion in 2024, a 15% increase year-over-year, further substantiating the growth prospects for ancillary equipment like EFEMs.

In terms of competitive landscape, Japanese manufacturers continue to lead in precision and reliability, with companies like RORZE Corporation and Hirata Corporation holding significant market shares. RORZE alone holds approximately 35% of the global market, attributed to its comprehensive product portfolio and strong presence across major semiconductor manufacturing regions. Other key players include Brooks Automation (US), Nidec (Genmark Automation, Japan), and Siasun Robot & Automation (China), each bringing innovations in robotics, precision engineering, and integration capabilities.

The market also sees increasing integration with Industry 4.0 technologies, including IoT-enabled monitoring and AI-driven predictive maintenance, which enhance operational efficiency and reduce downtime. The integration of these technologies is expected to be a key differentiator among manufacturers in the coming years.

However, the market faces challenges such as the high cost of advanced EFEM systems, which can exceed USD 250,000 per unit for high-end models, and the need for continuous technological upgrades to handle next-generation wafers. Additionally, geopolitical factors affecting semiconductor supply chains may impact investment cycles, though the long-term outlook remains positive due to sustained demand for electronics and ongoing digital transformation globally.

MARKET DRIVERS

Surge in Global Semiconductor Manufacturing

The global demand for semiconductors across consumer electronics, automotive, and industrial applications continues to rise exponentially. This directly fuels investments in new fabrication facilities and the expansion of existing ones, which in turn drives the demand for Equipment Front End Modules (EFEMs) that are essential for wafer handling automation. The market is experiencing a compound annual growth rate of approximately 9%, propelled by the continuous miniaturization of semiconductor devices and the transition to larger wafer sizes like 300mm, which necessitates advanced EFEM solutions for precise and contamination-free handling.

Advancements in Wafer Fabrication Technology

Technological progression towards smaller process nodes, such as 5nm and 3nm, demands ultra-clean manufacturing environments with minimal contamination. EFEMs play a critical role by creating a mini-environment that protects wafers from particulates, humidity, and other contaminants during loading and unloading from process tools. The integration of advanced robotics and real-time monitoring sensors within EFEMs has become a key driver, enabling higher throughput and improved yield for semiconductor manufacturers, making them indispensable in modern fabs.

➤ The adoption of Industry 4.0 principles, incorporating IoT connectivity and data analytics into EFEMs, is a significant factor enhancing operational efficiency and predictive maintenance capabilities.

Furthermore, government initiatives and substantial investments in domestic semiconductor production capabilities in regions like North America and Europe are creating a robust pipeline for capital equipment, including EFEMs, securing long-term market growth.

MARKET CHALLENGES

High Cost and Complexity of Advanced EFEM Systems

One of the primary challenges for the EFEM market is the significant capital expenditure required for state-of-the-art modules. These systems incorporate sophisticated robotics, precision alignment mechanisms, and stringent contamination control features, which escalate their cost. This high cost can be a barrier to adoption for smaller fabrication facilities or foundries operating with tighter budgets. Additionally, the complexity of integrating these modules with various process tools from different manufacturers requires specialized expertise and can lead to extended installation and qualification times.

Other Challenges

Maintaining Ultra-Low Levels of Contamination

As wafer geometries shrink, the acceptable level of particulate contamination becomes increasingly stringent, measured in fractions of a micron. Designing and maintaining EFEMs that consistently achieve and sustain these ultra-clean environments is a major technical hurdle, requiring advanced filtration systems and materials that do not outgas, adding to both cost and operational complexity.

Supply Chain Constraints for Critical Components

The EFEM market is susceptible to disruptions in the global supply chain, particularly for specialized components like precision motors, sensors, and high-purity materials. Shortages or delays in procuring these components can impact manufacturing lead times and project schedules for semiconductor equipment manufacturers.

MARKET RESTRAINTS

Capital Intensity and Cyclical Nature of the Semiconductor Industry

The semiconductor equipment market, including EFEMs, is highly cyclical and closely tied to the capital spending patterns of chip manufacturers. During periods of economic downturn or overcapacity, semiconductor companies often delay or cancel new equipment purchases. This cyclicality introduces significant volatility and uncertainty for EFEM suppliers, making long-term planning and capacity investment challenging. The high cost of equipment means that demand can fluctuate sharply with global economic conditions and end-market demand for electronics.

Technical Standardization and Interoperability Issues

While standards like SEMI E standards exist, achieving full interoperability between EFEMs from different vendors and various process tools remains a restraint. Variations in mechanical interfaces, communication protocols, and software integration can lead to compatibility issues, requiring custom engineering solutions that increase total cost of ownership and complicate the equipment selection process for fab operators.

MARKET OPPORTUNITIES

Expansion into Emerging Semiconductor Applications

Beyond traditional logic and memory fabs, significant growth opportunities exist in emerging sectors. The rising production of power semiconductors, MEMS (Micro-Electro-Mechanical Systems), and compound semiconductors (like GaN and SiC) for electric vehicles and 5G infrastructure requires specialized fabrication processes. This creates a demand for EFEMs tailored to handle these specific wafer types and process requirements, opening new market segments for equipment suppliers.

Integration of AI and Machine Learning

The integration of Artificial Intelligence (AI) and Machine Learning (ML) into EFEMs presents a substantial opportunity. These technologies can be used for predictive maintenance, fault detection, and optimizing wafer handling trajectories to maximize throughput and minimize particle generation. EFEMs equipped with smart capabilities can offer higher value propositions by reducing unplanned downtime and improving overall equipment effectiveness (OEE) for manufacturers.

Equipment Front End Module (EFEM) Market Trends

Steady Market Expansion Driven by Semiconductor Demand

The global Equipment Front End Module (EFEM) market is on a trajectory of consistent growth, fueled by the robust demand for semiconductors across various industries. The market, valued at $579 million in 2024, is projected to reach $790 million by 2032, reflecting a compound annual growth rate (CAGR) of 4.6%. This expansion is underpinned by the critical role EFEMs play in wafer handling within semiconductor fabrication facilities, ensuring contamination-free transfer of wafers between process equipment and standardized front-opening unified pods (FOUPs). The increasing complexity and miniaturization of semiconductor devices necessitate highly reliable and precise automation solutions, directly driving demand for advanced EFEMs.

Other Trends

Market Concentration and Regional Production Hubs

A significant trend is the high concentration of the market among a few key players. The top two manufacturers, RORZE and Brooks Automation, collectively account for over 60% of the global market share, with RORZE alone holding a dominant 35% share. This consolidation indicates a mature market where technological expertise and established supply chains are key competitive advantages. Geographically, production is concentrated in specific regions, with Japan being the largest production hub, commanding 40% of the market share. Other significant production areas include the United States, Europe, China, South Korea, and Southeast Asia, reflecting the global nature of the semiconductor supply chain.

Product and Application Preferences Shaping the Landscape

Market dynamics are further defined by clear preferences in product types and applications. In terms of product categories, the 3-port EFEM is the most popular configuration, holding 50% of the market share. The 4-port and 2-port variants follow with 30% and 20% shares, respectively, indicating a balance between flexibility and footprint constraints in fab layouts. The application landscape is overwhelmingly dominated by the 300mm wafer segment, which accounts for 95% of the market, underscoring the industry’s current manufacturing standard. The market for 200mm wafers persists for legacy applications, while the 450mm wafer segment remains minimal, awaiting broader industry adoption.

COMPETITIVE LANDSCAPE

Key Industry Players

Japanese Leader RORZE Commands Over a Third of the EFEM Market, Creating a Highly Concentrated Competitive Environment

The global Equipment Front End Module (EFEM) market is characterized by a significant degree of concentration, with the top two manufacturers collectively accounting for more than 60% of the total market share. RORZE has established itself as the dominant force, holding approximately 35% of the global market. Its strong production base in Japan, the largest production region commanding 40% of the market, provides a strategic advantage. Brooks Automation is another pivotal player, forming the other half of the market’s leading duo. This concentration underscores the high barriers to entry in the EFEM sector, driven by the need for precision engineering, contamination control expertise, and deep integration with semiconductor fabrication equipment.

Beyond the top-tier leaders, a group of specialized and niche players competes for the remaining market share. These companies, including Nidec (through its Genmark Automation division), Hirata, and Siasun Robot & Automation, often focus on specific regions, custom solutions, or particular EFEM configurations like the widely adopted 3-port design which holds 50% of the product market. The competitive dynamics are further influenced by the downstream demand, which is overwhelmingly driven by the 300mm wafer segment, accounting for 95% of the market, pushing manufacturers to continuously innovate in automation, speed, and particle performance to meet the stringent requirements of advanced semiconductor fabs.

List of Key Equipment Front End Module (EFEM) Companies Profiled

- Brooks Automation

- RORZE

- Nidec (Genmark Automation)

- Kensington

- Hirata

- Fala Technologies

- Milara

- Robots and Design

- Siasun Robot & Automation

- Beijing Heqi

- Shanghai Fortrend Technology

- Sineva

- Beijing U-PRECISION TECH

- Beijing REJE

- HongHu (Suzhou) Semiconductor Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

3 Port EFEM is the dominant product category due to its optimal balance between functionality, footprint, and cost-effectiveness, making it the preferred choice for a wide range of semiconductor manufacturing tools that require efficient wafer transfer between a limited number of process modules and the load port. This configuration offers greater flexibility than the 2 Port EFEM while maintaining a more compact and affordable design compared to the 4 Port version, whose adoption is generally reserved for highly complex tools requiring multiple parallel processing paths. The enduring preference for the 3 Port design underscores the industry’s focus on maximizing throughput and operational efficiency within constrained cleanroom spaces. |

| By Application |

|

300mm Wafer production represents the overwhelming application segment for EFEMs, as it constitutes the industry standard for leading-edge semiconductor fabrication. The sheer volume of 300mm wafer fabs globally drives consistent and high demand for EFEMs tailored to handle these larger substrates, which offer superior economies of scale. While 200mm wafer fabs continue to operate, supporting legacy and specialized technologies, their demand for new EFEMs is significantly lower. The 450mm Wafer segment, despite its potential for even greater efficiency, remains a nascent application with very limited commercial deployment due to the immense capital investment required for the transition, resulting in minimal current demand for compatible EFEMs. |

| By End User |

|

Foundries are the leading end-user segment, characterized by their massive scale of operations and continuous investment in new capacity and advanced process technologies to serve a diverse global client base. This drives a very high volume of EFEM procurement. Integrated Device Manufacturers (IDMs) also represent a substantial market, particularly those investing heavily in leading-edge manufacturing for their own products. The demand from OSAT providers, while significant, is generally for EFEMs used in backend packaging and test processes, which may have different specifications and are often tied to different investment cycles compared to the front-end fabs. |

| By Automation Level |

|

Fully Automated EFEMs are the dominant choice in modern high-volume semiconductor manufacturing facilities due to their critical role in enabling uninterrupted 24/7 operations, minimizing human-induced contamination, and maximizing tool uptime and throughput. The integration of sophisticated robotics and software for wafer handling is a fundamental requirement for advanced process nodes. Semi-Automated EFEMs find application in pilot lines, R&D environments, or for processing smaller batch sizes where flexibility is valued over pure speed. Manual Load EFEMs have a very limited presence, primarily in laboratory settings or for legacy equipment where automation is not economically justifiable. |

| By Wafer Handling Environment |

|

Mini-Environment (Isolated) EFEMs are the clear industry standard, as they provide a highly controlled, localized atmosphere that protects wafers from particulates and contaminants. This design is essential for yielding high-performance semiconductors at advanced nodes and allows for significant cost savings by reducing the stringent requirements for the entire surrounding cleanroom. EFEMs designed solely for an open cleanroom environment are far less common today, as the mini-environment approach offers superior contamination control and operational efficiency. The trend is firmly towards EFEMs that create their own pristine micro-environment, making this the leading and most critical segment for ensuring production quality. |

Regional Analysis: Equipment Front End Module (EFEM) Market

Asia-Pacific

The density of leading-edge semiconductor fabs in the Asia-Pacific region is unparalleled. This creates a built-in, high-volume market for EFEMs, as every new fabrication line requires multiple modules. Suppliers are deeply integrated into the local supply chains, fostering close collaboration for developing solutions tailored to the specific needs of complex manufacturing processes, from memory to logic chips.

National strategies across the region prioritize semiconductor self-sufficiency and technological leadership. Substantial government funding, tax incentives, and strategic partnerships are fueling the construction of massive new fabrication facilities. These initiatives directly translate into long-term, predictable demand for EFEMs, providing a stable foundation for market growth and encouraging continuous local innovation in automation.

Proximity to demanding customers pushes EFEM suppliers in Asia-Pacific to be at the forefront of technology. There is a strong focus on developing modules with higher cleanliness standards, increased throughput for larger wafers, and enhanced integration capabilities with other process tools. The ability to provide rapid customization and on-the-ground technical support is a critical competitive advantage in this dynamic market.

A mature and robust ecosystem of component suppliers, subsystem integrators, and service providers has developed around the semiconductor industry in Asia-Pacific. This ecosystem enables EFEM manufacturers to efficiently source high-quality parts, reduce logistical complexities, and maintain competitive production costs, further solidifying the region’s position as the most efficient and responsive market for wafer fab equipment.

North America

North America remains a critical and technologically sophisticated market for EFEMs, anchored by a strong presence of leading semiconductor equipment manufacturers and key IDMs. The market dynamics are heavily influenced by intense research and development activities focused on pioneering next-generation chip architectures and manufacturing processes. Demand is driven by the need for EFEMs that support extreme miniaturization, advanced packaging techniques like chiplets, and compatibility with new materials. While the total number of new mega-fabs is lower than in Asia, the region specializes in high-value, low-volume production of highly complex semiconductors, requiring EFEMs with superior precision, advanced software controls, and exceptional reliability. Strategic initiatives to onshore semiconductor manufacturing are expected to generate new, sustained demand in the coming years.

Europe

The European EFEM market is characterized by a focus on specialization and high-value manufacturing, particularly in the automotive, industrial, and power electronics sectors. The region hosts several major research institutions and equipment suppliers that drive innovation in specific niche areas. Market demand is shaped by the need for EFEMs capable of handling specialized materials, such as silicon carbide and gallium nitride, which are crucial for electric vehicle and renewable energy applications. The European market emphasizes stringent quality standards, long-term equipment reliability, and seamless integration into highly automated production lines. Collaborative projects funded by the European Union aim to strengthen the region’s semiconductor sovereignty, which is likely to foster a more resilient and innovative ecosystem for supporting equipment like EFEMs in the long term.

South America

The EFEM market in South America is nascent but shows potential for gradual growth, primarily driven by investments in regional electronics assembly and packaging facilities. The market is currently characterized by replacement demand and small-scale modernization projects within existing industrial bases, rather than the construction of new greenfield fabs. Key challenges include a less developed local semiconductor supply chain and reliance on imported equipment. However, increasing regional focus on technological development and efforts to attract foreign investment in high-tech industries could create future opportunities. EFEM suppliers operating in this region typically focus on providing robust, cost-effective solutions that offer high reliability with manageable operational complexity for the existing industrial landscape.

Middle East & Africa

The EFEM market in the Middle East & Africa is the smallest globally but is witnessing strategic developments aimed at economic diversification. Certain nations, particularly in the Gulf region, are making significant investments to establish technology hubs and nascent semiconductor manufacturing capabilities as part of long-term visions to move beyond hydrocarbon-based economies. Initial demand is expected to stem from pilot lines, research facilities, and partnerships with established global players. The market dynamics are defined by a long-term strategic build-out rather than immediate high-volume demand. Success in this region for EFEM suppliers will depend on forming strategic partnerships and providing foundational, scalable automation solutions that can support the region’s ambitious technological transformation goals over the next decade.

Report Scope

This market research report provides a comprehensive analysis of the Equipment Front End Module (EFEM) Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Equipment Front End Module (EFEM) Market?

-> Equipment Front End Module (EFEM) Market was valued at USD 579 million in 2024 and is projected to reach USD 790 million by 2032, exhibiting a CAGR of 4.6% during the forecast period.

Which key companies operate in Equipment Front End Module (EFEM) Market?

-> Key players include Brooks Automation, RORZE, Nidec (Genmark Automation), Hirata, Siasun Robot & Automation, Beijing Heqi, and Shanghai Fortrend Technology, among others. RORZE is the largest manufacturer with a 35% market share, and the top two players collectively account for over 60% of the market.

What are the key growth drivers?

-> Key growth drivers include increasing demand for semiconductors, expansion of wafer fabrication facilities, and continuous technological advancements in automation and precision handling for 300mm wafers, which dominate the application segment with a 95% share.

Which region dominates the market?

-> Japan is the largest production region, holding a 40% market share. Global production is also significant in the United States, Europe, China, Korea, and Southeast Asia.

What are the emerging trends?

-> Emerging trends include the dominance of 3-port EFEM systems holding a 50% market share, increasing automation integration, and the focus on enhancing throughput and contamination control in semiconductor manufacturing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...