MARKET INSIGHTS

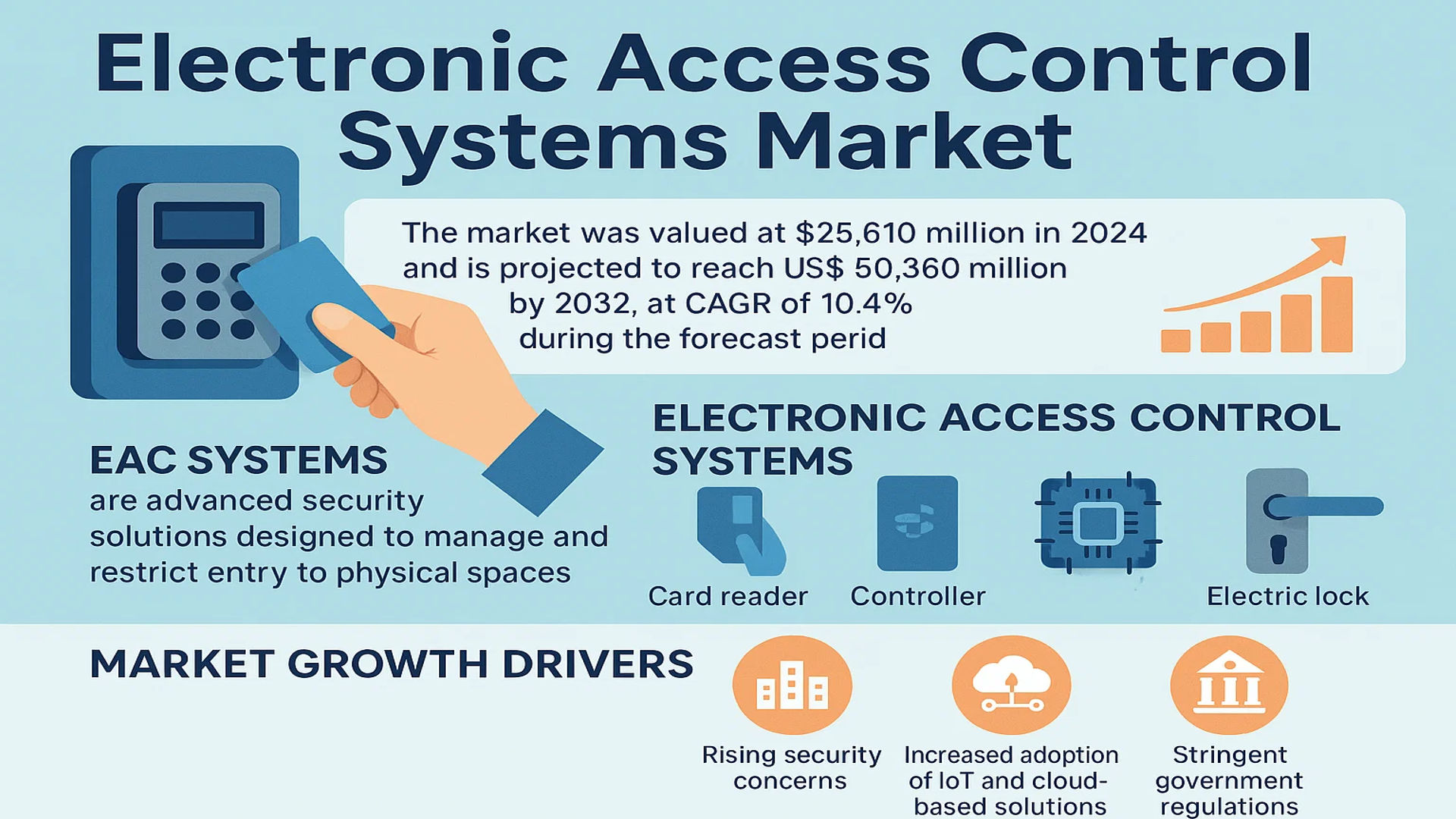

The global Electronic Access Control Systems Market was valued at 25610 million in 2024 and is projected to reach US$ 50360 million by 2032, at a CAGR of 10.4% during the forecast period.

Electronic Access Control (EAC) Systems are advanced security solutions designed to manage and restrict entry to physical spaces. A basic EAC system comprises three core components: a reader, a controller, and an electric lock. These systems provide granular control over facility access by defining specific parameters regarding who can enter, where they can go, and when access is permitted, thereby significantly enhancing physical security for businesses and organizations.

The market is experiencing robust growth driven by several key factors, including rising security concerns across commercial and residential sectors, increased adoption of IoT and cloud-based solutions, and stringent government regulations for critical infrastructure protection. Furthermore, technological advancements in biometrics and mobile-based access are contributing to market expansion. The competitive landscape is concentrated, with key players such as Honeywell, ASSA Abloy, and SIEMENS collectively holding a significant market share of approximately 70%, underscoring the high technical barriers and established nature of this industry.

MARKET DYNAMICS

MARKET DRIVERS

Rising Security Concerns and Increased Adoption of Smart Infrastructure to Drive Market Growth

The global electronic access control systems market is experiencing robust growth driven by escalating security concerns across commercial, industrial, and residential sectors. Increasing incidents of unauthorized access and security breaches have prompted organizations to invest heavily in advanced security solutions. The commercial segment, particularly in banking, healthcare, and corporate environments, has witnessed a significant uptake of these systems, with biometric access control solutions growing at approximately 15% annually. The transition towards smart cities and intelligent building management systems has further accelerated adoption, as integrated security solutions become essential components of modern infrastructure projects. Government regulations mandating enhanced security measures in critical infrastructure facilities have created a substantial demand for electronic access control systems globally.

Technological Advancements and Integration with IoT to Boost Market Expansion

Technological innovation represents a major growth driver for the electronic access control systems market. The integration of Internet of Things (IoT) technologies has transformed traditional access control into intelligent, connected systems capable of real-time monitoring and automated responses. Cloud-based access control solutions have gained significant traction, offering remote management capabilities and reducing the need for on-premise hardware. The adoption of mobile access credentials has grown substantially, with many organizations transitioning from physical cards to smartphone-based authentication. Recent developments in artificial intelligence and machine learning have enabled predictive security analytics, allowing systems to identify potential security threats before they materialize. The convergence of physical security systems with other building management functions has created comprehensive security ecosystems that offer both protection and operational efficiency.

Growing Demand for Contactless Solutions Post-Pandemic to Accelerate Market Development

The COVID-19 pandemic has fundamentally altered security requirements, driving increased demand for contactless access control solutions. Health and safety concerns have accelerated the adoption of touchless authentication methods, particularly biometric systems with advanced hygiene features. Facial recognition technology has seen remarkable growth, with installations increasing by over 40% in the healthcare and corporate sectors since 2020. The emphasis on minimizing physical contact points has also driven innovation in mobile access solutions and automatic door opening systems. This shift towards contactless technologies is not merely a temporary response but represents a permanent transformation in security preferences, with organizations prioritizing both security and health considerations in their access control strategies.

MARKET CHALLENGES

High Implementation and Maintenance Costs to Challenge Market Penetration

Despite strong growth prospects, the electronic access control systems market faces significant cost-related challenges that impact widespread adoption. The initial investment required for comprehensive system implementation remains substantial, particularly for advanced biometric and integrated solutions. Small and medium-sized enterprises often find the upfront costs prohibitive, limiting market penetration in this segment. Maintenance expenses add to the total cost of ownership, with regular software updates, hardware replacements, and technical support contributing to ongoing operational costs. The requirement for specialized installation professionals further increases implementation expenses, particularly in regions with limited technical expertise. These financial barriers are particularly pronounced in developing economies where budget constraints often prioritize basic security measures over advanced electronic systems.

Other Challenges

Cybersecurity Vulnerabilities

The increasing connectivity of access control systems introduces significant cybersecurity risks that challenge market confidence. Networked systems are vulnerable to hacking attempts, data breaches, and unauthorized remote access. Instances of credential theft and system manipulation have raised concerns about the reliability of electronic access control, particularly in high-security environments. The complexity of securing interconnected systems against evolving cyber threats requires continuous investment in security protocols and regular vulnerability assessments.

System Integration Complexities

Integrating electronic access control systems with existing security infrastructure and other building management systems presents substantial technical challenges. Compatibility issues between different manufacturers’ products often necessitate custom integration solutions, increasing both cost and implementation time. The lack of standardized communication protocols across the industry creates interoperability problems that can limit system functionality and scalability.

MARKET RESTRAINTS

Privacy Concerns and Regulatory Compliance to Deter Market Growth

Electronic access control systems, particularly those utilizing biometric data, face significant restraints due to growing privacy concerns and stringent regulatory requirements. The collection and storage of personal identification data, including fingerprints, facial recognition patterns, and other biometric information, have raised serious privacy issues among consumers and regulatory bodies. Data protection regulations such as the General Data Protection Regulation in Europe impose strict requirements on how personal data is handled, stored, and processed. Compliance with these regulations adds substantial complexity and cost to system implementation and operation. Recent legal challenges regarding facial recognition technology have created uncertainty in several markets, causing some organizations to delay or scale back their adoption plans. These privacy considerations are particularly impactful in the residential and healthcare sectors, where sensitivity regarding personal data is highest.

Technical Reliability Issues and System Downtime to Limit Market Adoption

Technical reliability concerns present significant restraints for electronic access control system adoption across various sectors. System failures or malfunctions can result in complete access denial, creating operational disruptions and security vulnerabilities. Power outages continue to affect system performance, despite advancements in backup power solutions. Environmental factors such as extreme temperatures, humidity, and physical damage can impact the reliability of readers and controllers, particularly in outdoor installations. False rejection rates in biometric systems, though improving, still present operational challenges that affect user experience and system efficiency. These reliability issues are particularly critical in high-security environments where system failure is not an option, leading some organizations to maintain mechanical backup systems alongside electronic solutions.

Limited Technical Expertise and Training Requirements to Restrain Market Expansion

The sophistication of modern electronic access control systems requires specialized technical expertise for proper installation, configuration, and maintenance, creating a significant restraint on market growth. The shortage of qualified professionals capable of designing and implementing complex integrated security systems affects implementation quality and system performance. Training requirements for end-users have increased with system complexity, particularly for administrative functions and emergency operation procedures. The rapid pace of technological advancement means that technical knowledge quickly becomes outdated, requiring continuous training and certification programs. This expertise gap is particularly evident in emerging markets where technical education infrastructure may not keep pace with technological developments, limiting the effective deployment of advanced access control solutions.

MARKET OPPORTUNITIES

Emerging Markets and Infrastructure Development to Provide Significant Growth Opportunities

Developing economies present substantial growth opportunities for electronic access control system providers as infrastructure development and urbanization accelerate. Increasing investments in smart city projects across Asia, Latin America, and the Middle East are creating new demand for advanced security solutions. Government initiatives aimed at modernizing public infrastructure often include electronic access control as a key component of security upgrades. The growing commercial real estate sector in emerging markets is adopting modern security standards that increasingly incorporate electronic access control systems. These markets offer the potential for significant volume growth, particularly as economic development increases the affordability of advanced security solutions for a broader range of organizations and applications.

Advancements in Artificial Intelligence and Predictive Analytics to Create New Market Opportunities

Technological innovations in artificial intelligence and data analytics are creating new opportunities for enhanced functionality and value creation in electronic access control systems. AI-powered systems can analyze access patterns to identify anomalies and potential security threats, adding intelligent monitoring capabilities to traditional access control. Predictive maintenance features enabled by machine learning algorithms can reduce system downtime and improve reliability. Integration with other building systems allows for comprehensive analytics regarding space utilization, movement patterns, and operational efficiency. These advanced capabilities transform access control from a simple security function to a valuable source of business intelligence, creating additional value propositions that justify investment in more sophisticated systems.

Subscription-Based Models and Cloud Services to Open New Revenue Streams

The shift towards service-oriented business models presents significant opportunities for market expansion and revenue diversification. Cloud-based access control solutions offered through subscription models reduce upfront costs for customers while providing providers with recurring revenue streams. Managed service offerings that include monitoring, maintenance, and system updates create long-term customer relationships and stable income sources. The flexibility of cloud-based systems allows for easier scaling and upgrades, addressing some of the cost concerns associated with traditional implementations. These service-based approaches particularly benefit small and medium-sized businesses that may lack the technical resources to manage complex security systems independently, potentially expanding the addressable market substantially.

ELECTRONIC ACCESS CONTROL SYSTEMS MARKET TRENDS

Integration of Artificial Intelligence and Cloud-Based Solutions to Emerge as a Trend in the Market

The integration of Artificial Intelligence (AI) and cloud computing is fundamentally reshaping the Electronic Access Control (EAC) landscape, driving a shift from traditional standalone systems to intelligent, networked solutions. AI-powered analytics are enabling predictive threat detection by identifying anomalous access patterns in real-time, significantly enhancing security postures beyond simple credential verification. This is complemented by the rapid adoption of cloud-based access control, which offers unparalleled scalability and remote management capabilities. The flexibility of Software-as-a-Service (SaaS) models allows businesses of all sizes to deploy sophisticated security without substantial upfront investment in on-premise servers. Furthermore, the convergence of EAC with other building systems, such as video surveillance and fire alarms, into unified security platforms is creating a more holistic and responsive environment. This trend is accelerating as organizations prioritize not just physical security but also data-driven insights for operational efficiency and compliance reporting.

Other Trends

Biometric Authentication Proliferation

The demand for highly secure and convenient authentication methods is fueling the proliferation of biometric technologies within access control systems. While fingerprint recognition remains widely used, more advanced modalities like facial recognition, iris scanning, and vein pattern authentication are gaining significant traction due to their enhanced security and contactless nature. The adoption of multi-modal biometrics, which combines two or more authentication methods, is also rising to bolster security against spoofing attempts. This trend is particularly dominant in high-security applications across government facilities, financial institutions, and critical infrastructure, where the imperative to prevent unauthorized access is paramount. The technology’s integration with mobile credentials is further streamlining user experience, allowing for seamless and secure access without the need for physical cards or keys.

Rise of Mobile-First and Touchless Access Solutions

Accelerated by global health concerns and the pursuit of greater convenience, the market is experiencing a pronounced shift towards mobile-first and completely touchless access solutions. The use of smartphones as digital keys is becoming mainstream, leveraging technologies like Bluetooth Low Energy (BLE) and Near Field Communication (NFC) to grant access. This trend dovetails with the growing Internet of Things (IoT) ecosystem, where access control readers and locks are becoming interconnected nodes within a smarter building infrastructure. This connectivity enables features such as remote access granting, real-time permission updates, and detailed audit trails accessible from anywhere. The demand for these solutions is robust across the commercial and residential sectors, as they offer a superior user experience, reduce the costs associated with physical credential management, and provide a more hygienic alternative to traditional touch-based readers.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Acquisitions Drive Market Leadership

The global Electronic Access Control Systems (EACS) market exhibits a semi-consolidated structure, characterized by the presence of several dominant multinational corporations alongside numerous specialized regional players. The market’s competitive intensity is high, primarily because of the significant technical barriers to entry and the critical need for robust, reliable security solutions. Honeywell International Inc. and ASSA Abloy AB are universally recognized as market leaders, commanding substantial shares due to their extensive, diversified product portfolios that span card-based systems, advanced biometrics, and integrated software platforms. Their dominance is further cemented by a powerful global distribution network and a strong brand reputation built on decades of delivering mission-critical security infrastructure.

SIEMENS AG and Johnson Controls (which acquired TYCO) also hold considerable market influence. Their growth is largely fueled by a focus on smart building integration and IoT-enabled access control solutions, catering to the rising demand for connected and automated security environments in commercial and industrial sectors. These companies leverage their expertise in building automation to offer seamless, unified systems that combine access control with fire safety, HVAC, and other building management functions.

Furthermore, continuous investment in research and development is a cornerstone of competition. Leading players are aggressively developing next-generation technologies, such as mobile-based access using Bluetooth and NFC, cloud-managed systems, and artificial intelligence for predictive threat detection and behavioral analytics. Recent strategic mergers and acquisitions have been a key tactic for market expansion, enabling companies to rapidly acquire new technologies and gain access to emerging regional markets.

Meanwhile, other significant players like BOSCH Security Systems, Allegion plc, and Gallagher Security are strengthening their positions through specialized, high-security offerings and by forming strategic partnerships with software firms and hardware manufacturers. This ensures they remain agile and responsive to evolving customer needs, from high-risk government facilities to modern residential complexes, securing their growth in an increasingly competitive landscape.

List of Key Electronic Access Control Systems Companies Profiled

- Honeywell International Inc. (U.S.)

- ASSA Abloy AB (Sweden)

- SIEMENS AG (Germany)

- Johnson Controls International plc (Ireland) – formerly Tyco

- BOSCH Security Systems (Germany)

- ADT LLC (U.S.)

- Dormakaba Holding AG (Switzerland) – formerly KABA Group

- Schneider Electric (France)

- Suprema Inc. (South Korea)

- Southco, Inc. (U.S.)

- SALTO Systems S.L. (Spain)

- Nortek Control (U.S.)

- Panasonic Corporation (Japan)

- Digital Monitoring Products (DMP) (U.S.)

- Gallagher Group Limited (New Zealand)

- Allegion plc (Ireland)

Segment Analysis:

By Type

Card-Based Systems Lead the Market Due to Their Established Infrastructure and Cost-Effectiveness

The market is segmented based on type into:

- Card-Based Systems

- Subtypes: Proximity Cards, Smart Cards, and others

- Biometrics

- Subtypes: Fingerprint Recognition, Facial Recognition, Iris Recognition, and others

- Others

- Subtypes: Keypads, Mobile Credentials, and emerging technologies

By Application

Commercial Application Segment Dominates Owing to High Demand for Secure Office and Retail Spaces

The market is segmented based on application into:

- Homeland Security

- Commercial

- Industrial

- Residential

- Others

By Technology

Network-Based Systems are Gaining Traction Due to Integration Capabilities and Remote Management Features

The market is segmented based on technology into:

- Standalone Systems

- Network-Based Systems

- Wireless Systems

By Component

Hardware Components Hold Significant Share as They Form the Physical Foundation of Access Control Infrastructure

The market is segmented based on component into:

- Hardware

- Software

- Services

Regional Analysis: Electronic Access Control Systems Market

North America

North America represents a mature and technologically advanced market for Electronic Access Control Systems, characterized by high adoption rates across commercial, industrial, and government sectors. The United States, in particular, is a major driver, with stringent security regulations and a heightened focus on protecting critical infrastructure post-9/11 fueling consistent demand. The region’s growth is further propelled by the widespread integration of EAC systems with broader building automation and IoT platforms, creating smart, connected security environments. Major players like Honeywell, Allegion, and Johnson Controls (which acquired Tyco) have a strong presence, driving innovation in cloud-based access control and mobile credentials. However, the market faces challenges from the high initial cost of advanced biometric systems and increasing concerns over data privacy associated with these connected solutions.

Europe

Europe’s market is defined by a strong regulatory framework, most notably the General Data Protection Regulation (GDPR), which significantly influences the development and deployment of EAC systems, especially those utilizing biometric data. This has accelerated the demand for privacy-compliant and secure solutions. The region shows a strong preference for high-security, interoperable systems, with significant adoption in the commercial and residential sectors. Countries like Germany, the UK, and France are at the forefront, investing heavily in modernizing security infrastructure for public buildings, transportation hubs, and corporate headquarters. Leading companies such as ASSA Abloy and Bosch Security Systems are key innovators, focusing on seamless integration and cybersecurity. The market’s growth is steady, supported by a culture that highly values both security and data protection.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market for EAC systems globally, driven by rapid urbanization, massive infrastructure development, and increasing security expenditures. China and India are the primary growth engines, with their extensive investments in smart city projects, new commercial real estate, and industrial expansion. While cost sensitivity makes card-based systems prevalent, there is a rapidly accelerating shift towards biometric technologies, particularly in government and high-security commercial applications. The market is highly competitive, with both global giants like Panasonic and SIEMENS and strong local players vying for market share. The sheer scale of development presents immense opportunities, though the market can be fragmented with varying standards and levels of technological adoption across different countries.

South America

The South American market for EAC systems is developing, with growth primarily concentrated in major economic centers within countries like Brazil and Argentina. Demand is largely driven by the commercial and industrial sectors seeking to mitigate rising security threats and protect assets. Economic volatility remains a significant restraining factor, often limiting large-scale investments in advanced, integrated security systems. Consequently, the adoption tends to favor more cost-effective, standalone solutions rather than enterprise-level systems. While the market potential is recognized, its growth trajectory is often uneven, closely tied to regional economic stability and foreign investment flows into infrastructure projects.

Middle East & Africa

The Middle East & Africa region presents a market of contrasts. Wealthier Gulf Cooperation Council (GCC) nations, such as the UAE, Saudi Arabia, and Qatar, are hotspots for growth, driven by visionary projects like NEOM and massive investments in commercial infrastructure, transportation, and hospitality. These projects demand state-of-the-art, integrated EAC solutions. In contrast, other parts of the region face challenges due to political instability and limited investment capital, which slows market development. Nonetheless, across the board, there is a growing recognition of the importance of modern security systems. The long-term outlook is positive, with growth expected to be fueled by ongoing urban development and economic diversification efforts in key Middle Eastern countries.

Report Scope

This market research report provides a comprehensive analysis of the global Electronic Access Control Systems (EACS) market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Card-Based, Biometrics, Others), technology, application (Homeland Security, Commercial, Industrial, Residential, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, mobile access solutions, cloud-based management platforms, and evolving cybersecurity standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Electronic Access Control Systems Market?

-> Electronic Access Control Systems Market was valued at 25610 million in 2024 and is projected to reach US$ 50360 million by 2032, at a CAGR of 10.4% during the forecast period.

Which key companies operate in Global Electronic Access Control Systems Market?

-> Key players include Honeywell, ASSA Abloy, SIEMENS, TYCO, BOSCH Security, DDS, ADT LLC, Dorma, KABA Group, Schneider, Suprema, Southco, SALTO, Nortek Control, Panasonic, Millennium, Digital Monitoring Products, Gallagher, Allegion, and Integrated, among others. These companies collectively hold approximately 70% of the global market share.

What are the key growth drivers?

-> Key growth drivers include increasing security concerns, rising adoption of IoT and cloud-based solutions, stringent government regulations for security infrastructure, and growing demand from commercial and residential sectors.

Which region dominates the market?

-> North America currently holds the largest market share, while Asia-Pacific is expected to be the fastest-growing region due to rapid urbanization and infrastructure development.

What are the emerging trends?

-> Emerging trends include integration of artificial intelligence and machine learning, mobile-based access control, touchless biometric systems, and increased focus on cybersecurity in physical access systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...