MARKET INSIGHTS

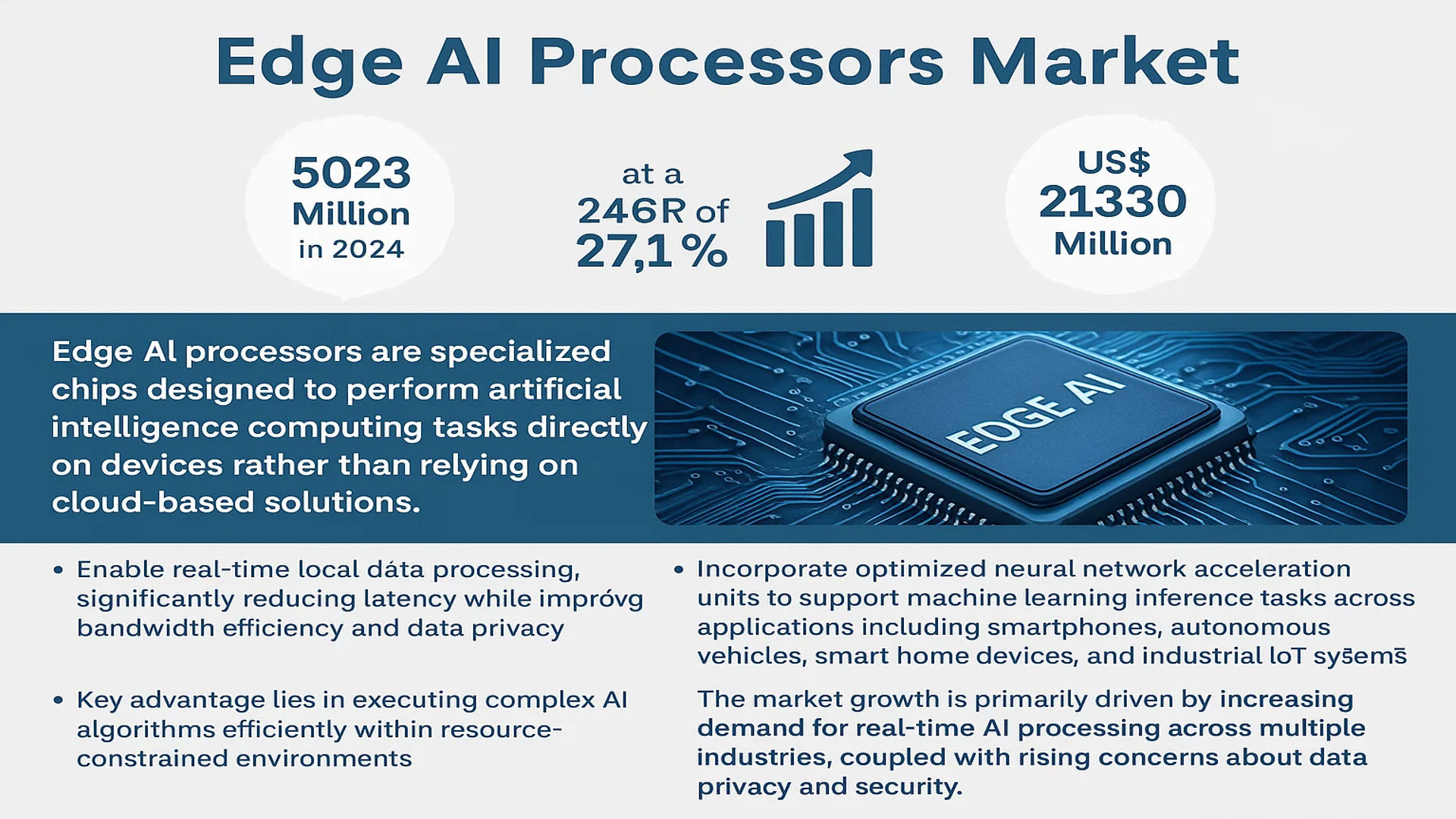

The global Edge AI Processors Market was valued at 5023 million in 2024 and is projected to reach US$ 21330 million by 2032, at a CAGR of 27.1% during the forecast period.

Edge AI processors are specialized chips designed to perform artificial intelligence computing tasks directly on devices rather than relying on cloud-based solutions. These processors enable real-time local data processing, significantly reducing latency while improving bandwidth efficiency and data privacy. They incorporate optimized neural network acceleration units to support machine learning inference tasks across applications including smartphones, autonomous vehicles, smart home devices, and industrial IoT systems. Their key advantage lies in executing complex AI algorithms efficiently within resource-constrained environments.

The market growth is primarily driven by increasing demand for real-time AI processing across multiple industries, coupled with rising concerns about data privacy and security. The automotive sector shows particularly strong adoption for autonomous driving applications, while industrial IoT deployments are accelerating processor demand for predictive maintenance and quality control systems. Key industry players like NVIDIA, Intel, and Qualcomm continue to innovate, with recent advancements focusing on energy-efficient architectures and enhanced neural processing capabilities. For instance, in 2023, NVIDIA introduced its next-generation Edge AI platform featuring significant improvements in power efficiency and processing throughput.

MARKET DYNAMICS

MARKET DRIVERS

Smart Device Proliferation and IoT Expansion Accelerating Edge AI Adoption

The exponential growth of smart devices and IoT ecosystems is driving unprecedented demand for edge AI processors. With over 29 billion connected IoT devices projected globally by 2027, the need for real-time, localized processing has become critical. Edge AI processors enable devices to perform complex computations like facial recognition, natural language processing, and predictive maintenance without cloud dependency. This shift significantly reduces latency from 100+ milliseconds in cloud-based systems to under 10 milliseconds with edge processing. The automotive industry’s rapid adoption of advanced driver assistance systems (ADAS) demonstrates this trend, where edge processors enable split-second decision making for collision avoidance.

Data Privacy Regulations Fueling On-Device Processing Needs

Increasingly stringent data privacy laws worldwide are compelling organizations to process sensitive information locally rather than transmitting it to centralized clouds. The European Union’s GDPR and similar regulations in other regions have made edge-based AI processing essential for industries handling personal data. Financial institutions deploying edge AI for fraud detection can analyze transactions on-site while complying with data sovereignty requirements. Healthcare providers are adopting edge processors for medical imaging analysis directly on diagnostic equipment, keeping patient records within facility boundaries. This regulatory environment has created a 74% increase in demand for secure edge processing solutions since 2022.

5G Network Rollouts Enabling Distributed AI Architectures

The global deployment of 5G infrastructure is removing bandwidth limitations that previously constrained edge computing capabilities. With 5G’s ultra-low latency and high throughput, edge AI solutions can now function as part of distributed intelligence networks while maintaining real-time performance. Telecommunications companies are investing heavily in edge data centers equipped with AI processors to support emerging applications like augmented reality, industrial automation, and smart city infrastructure. The synergy between 5G and edge AI is particularly evident in manufacturing, where predictive maintenance systems using edge processors have reduced equipment downtime by up to 45% in early implementations.

MARKET RESTRAINTS

High Development Costs and Design Complexity Slowing Market Penetration

While edge AI processors offer compelling advantages, their development presents significant technical and financial challenges. Designing chips that deliver high-performance AI acceleration within strict power budgets requires specialized expertise that remains scarce. The average development cost for a new edge AI processor architecture exceeds $50 million, creating barriers for smaller players. Furthermore, optimizing neural network models for diverse edge use cases demands extensive co-development between hardware engineers and AI specialists. This complexity has limited widespread adoption, particularly among small and medium enterprises lacking necessary technical resources.

Fragmented Standards and Compatibility Issues Hindering Deployment

The absence of universal standards for edge AI architectures creates interoperability challenges that restrain market growth. With major tech companies developing proprietary frameworks and instruction sets, organizations face difficulties integrating different edge processing solutions. This fragmentation is most evident in the industrial IoT sector, where equipment from multiple vendors must work together seamlessly. The lack of standardized benchmarking methods also complicates performance comparisons, making it challenging for buyers to evaluate solutions objectively. While industry consortia are working toward standardization, current inconsistencies continue to slow large-scale edge AI adoption.

MARKET OPPORTUNITIES

Autonomous Vehicle Development Creating Massive Demand for Edge AI Chips

The race toward fully autonomous vehicles represents a transformative opportunity for edge AI processor manufacturers. Modern autonomous driving systems require multiple high-performance processors to handle simultaneous tasks like object detection, path planning, and sensor fusion with millisecond-level latency. Leading automotive manufacturers are partnering with semiconductor companies to develop specialized edge AI processors capable of delivering over 100 TOPS (tera operations per second) while consuming minimal power. These collaborations have already yielded dedicated automotive AI processors that outperform traditional GPUs in efficiency by up to 60%, showcasing the potential for edge AI in next-generation transportation.

AI-Powered Healthcare Diagnostics Driving Innovation in Medical Edge Computing

Healthcare’s digital transformation is creating significant opportunities for edge AI processors in medical diagnostics. Portable imaging devices equipped with AI processors can now provide preliminary diagnoses in remote locations without internet connectivity. Recent studies show AI-enabled edge devices achieving 93% accuracy in detecting abnormalities from medical scans, comparable to specialist radiologists. Pharmaceutical companies are also adopting edge AI for real-time quality control in drug manufacturing, reducing inspection times by 80% while improving detection rates. As regulatory approvals for AI-assisted diagnostics accelerate, the healthcare sector is projected to account for over 20% of edge AI processor revenues by 2027.

MARKET CHALLENGES

Thermal Management Issues Constraining Performance in Compact Devices

Edge AI processors face significant thermal challenges when deployed in space-constrained devices like smartphones and wearables. High-performance AI computations generate substantial heat that must be dissipated without active cooling systems. Thermal throttling currently reduces effective processing power by 30-40% in many edge devices during sustained AI workloads. This limitation is particularly problematic for always-on applications such as voice assistants or continuous health monitoring. Manufacturers are exploring innovative packaging techniques and advanced materials to improve thermal efficiency, but fundamental physics constraints continue to challenge performance scaling in compact form factors.

Security Vulnerabilities in Distributed AI Systems Require New Approaches

The distributed nature of edge computing introduces unique security challenges that differ from centralized cloud architectures. Edge AI processors deployed in field environments are vulnerable to physical tampering, side-channel attacks, and adversarial machine learning exploits. Recent research has demonstrated successful attacks that manipulate edge AI model behavior through subtle input perturbations. Developing robust hardware-level security features without significantly increasing chip area or power consumption remains an ongoing challenge. The industry is responding with new secure enclave architectures and homomorphic encryption capabilities, but comprehensive solutions still require further development and standardization.

EDGE AI PROCESSORS MARKET TRENDS

Surging Demand for Low-Latency AI Processing Drives Market Growth

The Edge AI Processor market is experiencing significant growth, driven by the increasing need for real-time data processing across industries. The global market, valued at $5,023 million in 2024, is projected to reach $21,330 million by 2032, growing at a CAGR of 27.1% during the forecast period. This rapid expansion is fueled by the demand for AI-driven applications in autonomous vehicles, smart devices, and industrial IoT, where latency and bandwidth constraints make cloud-based solutions impractical. Companies like NVIDIA, Intel, and Qualcomm dominate the market, collectively holding a substantial revenue share.

Other Trends

Integration of Neural Processing Units (NPUs) in Edge Devices

As AI workloads become more complex, manufacturers are increasingly incorporating specialized NPUs into edge processors to enhance efficiency. Unlike conventional GPUs, NPUs are designed to accelerate machine learning tasks while consuming minimal power, making them ideal for battery-operated devices. This trend aligns with the rising adoption of edge AI in wearables, drones, and surveillance systems. Manufacturers like Hailo and Kinara have introduced dedicated NPUs that outperform traditional processors in AI inference tasks by up to 30% in latency reduction.

Rise of AI in Automotive and Industrial Applications

The automotive and industrial sectors are emerging as key adopters of edge AI processors, particularly for applications like autonomous driving and predictive maintenance. Tier-1 suppliers and OEMs are collaborating with chipmakers to develop custom AI processors capable of handling complex sensor fusion and real-time decision-making. The Industrial Internet of Things (IIoT) segment alone is projected to contribute over 25% of the market revenue by 2026, as factories increasingly deploy AI-powered quality control and operational analytics systems.

While these trends highlight the market’s momentum, challenges such as fragmented standardization and high R&D costs continue to hinder widespread adoption among smaller enterprises. However, ongoing advancements in chip miniaturization and energy efficiency are expected to lower entry barriers, further accelerating market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Giants and AI Specialists Compete for Edge Computing Dominance

The global Edge AI processor market features a dynamic mix of established semiconductor manufacturers and innovative AI-focused startups. NVIDIA and Intel currently lead the market, leveraging their expertise in GPU and CPU architectures to deliver high-performance AI acceleration solutions. NVIDIA’s Jetson platform for edge computing and Intel’s AI-focused Movidius VPUs demonstrate their commitment to this growing sector.

Qualcomm has emerged as a key contender in mobile edge AI with its Snapdragon processors, while startups like Hailo and EdgeCortix are gaining traction with specialized AI chips designed specifically for edge applications. The competition intensified in 2024 as these companies ramped up production of energy-efficient processors capable of handling complex neural networks at the edge.

Recent developments show increasing vertical integration among major players. Google and Meta have entered the market with custom TPU designs optimized for their respective AI workloads, potentially disrupting traditional chip suppliers. Meanwhile, AMD has leveraged its acquisition of Xilinx to expand its edge AI offerings with adaptive computing solutions.

The landscape is expected to grow more competitive as automotive and industrial applications drive demand. Companies like Texas Instruments and Ambarella are well-positioned in these verticals, while specialist firms such as Kinara focus on ultra-low-power AI processing for IoT devices.

List of Key Edge AI Processor Companies Profiled

- NVIDIA Corporation (U.S.)

- Intel Corporation (U.S.)

- Qualcomm Technologies, Inc. (U.S.)

- Hailo (Israel)

- EdgeCortix Inc. (Japan/U.S.)

- Kinara, Inc. (U.S.)

- Texas Instruments (U.S.)

- Advanced Micro Devices (AMD) (U.S.)

- Google AI (U.S.)

- Meta Platforms (U.S.)

- Axelera AI (Netherlands)

- AONDevices, Inc. (U.S.)

- Murata Manufacturing Co., Ltd. (Japan)

- DEEPX (South Korea)

- Ambarella (U.S.)

Segment Analysis:

By Type

GPU Segment Leads the Market Due to High Parallel Processing Capabilities

The market is segmented based on type into:

- GPU

- Subtypes: Discrete GPUs, Integrated GPUs, and others

- NPU

- TPU

- DPU

- Others

By Application

Automotive Field Emerges as Key Segment with Adoption of Autonomous Driving Technologies

The market is segmented based on application into:

- Automotive Field

- Subtypes: ADAS, autonomous vehicles, in-vehicle infotainment

- Electronic Field

- Industrial Internet of Things Field

- Others

By End User

Enterprise Segment Drives Demand for Edge AI Processors in Industrial Automation

The market is segmented based on end user into:

- Enterprise

- Consumer

- Government

- Others

By Architecture

SoC Architecture Gains Prominence for Compact Edge AI Implementations

The market is segmented based on architecture into:

- System-on-Chip (SoC)

- System-in-Package (SiP)

- Discrete

- Others

Regional Analysis: Edge AI Processors Market

Asia-Pacific

The Asia-Pacific region leads the global Edge AI Processors market, driven by high-volume manufacturing, rapid adoption of smart devices, and strong government initiatives in AI development. China holds the dominant position with tech giants like Huawei and Alibaba investing heavily in edge AI infrastructure to support smart cities and IoT deployments. India is emerging as a key player due to its growing startup ecosystem and increasing integration of AI in automotive and industrial automation. Countries like South Korea and Japan contribute significantly through advancements in semiconductor fabrication and innovative applications in robotics and autonomous vehicles. Despite cost sensitivity in some segments, the region benefits from economies of scale and a robust electronics supply chain.

North America

North America remains a technology innovation hub for Edge AI Processors, fueled by substantial R&D investments from both established tech companies and startups. The U.S. accounts for the majority of regional market share with companies like NVIDIA, Intel, and Qualcomm driving architecture innovations and deployment in data-sensitive sectors such as healthcare and defense. Regulatory focus on data privacy (e.g., through initiatives like the AI Bill of Rights) accelerates local processing requirements. Canadian AI research institutions and government funding programs further bolster regional growth, particularly in industrial automation and edge computing applications. The presence of hyperscalers developing custom AI chips creates additional demand.

Europe

Europe shows steady growth in Edge AI adoption, championed by stringent data protection laws (GDPR) that incentivize localized processing. Germany leads in industrial applications, integrating AI processors into Industry 4.0 smart factories and automotive manufacturing. The EU’s coordinated approach to AI regulation and funding (through programs like Horizon Europe) supports cross-border innovation while maintaining ethical standards. While slightly lagging in semiconductor fabrication capabilities compared to Asia and the U.S., European firms excel in specialized applications including medical devices, smart energy systems, and secure edge computing architectures. Sustainability concerns are driving R&D into energy-efficient AI processor designs.

South America

Edge AI adoption in South America remains nascent but shows promising growth in specific sectors. Brazil leads with pilot projects in agricultural technology (AgTech), leveraging edge processing for real-time crop monitoring and equipment automation. Economic constraints and limited local semiconductor production create dependency on imported components, though governments are beginning to support tech innovation through tax incentives. Smart city initiatives in major urban centers are deploying edge AI for traffic management and public safety applications. The lack of comprehensive AI governance frameworks currently limits widespread enterprise adoption compared to more developed markets.

Middle East & Africa

This region presents a mixed landscape for Edge AI Processors, with Gulf nations demonstrating the most advanced adoption. UAE and Saudi Arabia are investing heavily in smart infrastructure and AI governance frameworks as part of broader economic diversification strategies. Edge processing supports applications ranging from oil/gas predictive maintenance to surveillance systems. Sub-Saharan Africa is exploring AI processors for financial inclusion and telemedicine solutions, though infrastructure gaps constrain deployment. While the region currently represents a small market share, strategic partnerships with global tech firms and improving connectivity signal long-term potential in edge computing applications.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Edge AI Processors markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Edge AI Processors market was valued at USD 5,023 million in 2024 and is projected to reach USD 21,330 million by 2032, growing at a CAGR of 27.1%.

- Segmentation Analysis: Detailed breakdown by product type (GPU, NPU, TPU, DPU), application (Automotive, Electronics, Industrial IoT), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis of key markets like the U.S., China, Japan, and Germany.

- Competitive Landscape: Profiles of leading market participants including Qualcomm, NVIDIA, Intel, AMD, and Google, covering their product portfolios, R&D investments, and strategic partnerships.

- Technology Trends & Innovation: Assessment of emerging edge computing architectures, AI acceleration techniques, power efficiency improvements, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors such as growing AI adoption, 5G deployment, data privacy concerns, along with challenges like high development costs and technical complexities.

- Stakeholder Analysis: Insights for semiconductor manufacturers, OEMs, system integrators, and investors regarding the evolving edge computing ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Edge AI Processors Market?

-> Edge AI Processors market was valued at 5023 million in 2024 and is projected to reach US$ 21330 million by 2032, at a CAGR of 27.1% during the forecast period.

Which key companies operate in Global Edge AI Processors Market?

-> Key players include Qualcomm, NVIDIA, Intel, AMD, Google, Meta, Hailo, EdgeCortix, and TI, among others.

What are the key growth drivers?

-> Key growth drivers include increasing AI adoption, demand for real-time processing, 5G network expansion, and growing IoT applications.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is expected to show the highest growth rate during the forecast period.

What are the emerging trends?

-> Emerging trends include heterogeneous computing architectures, energy-efficient designs, on-device learning capabilities, and specialized AI accelerators.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...