MARKET INSIGHTS

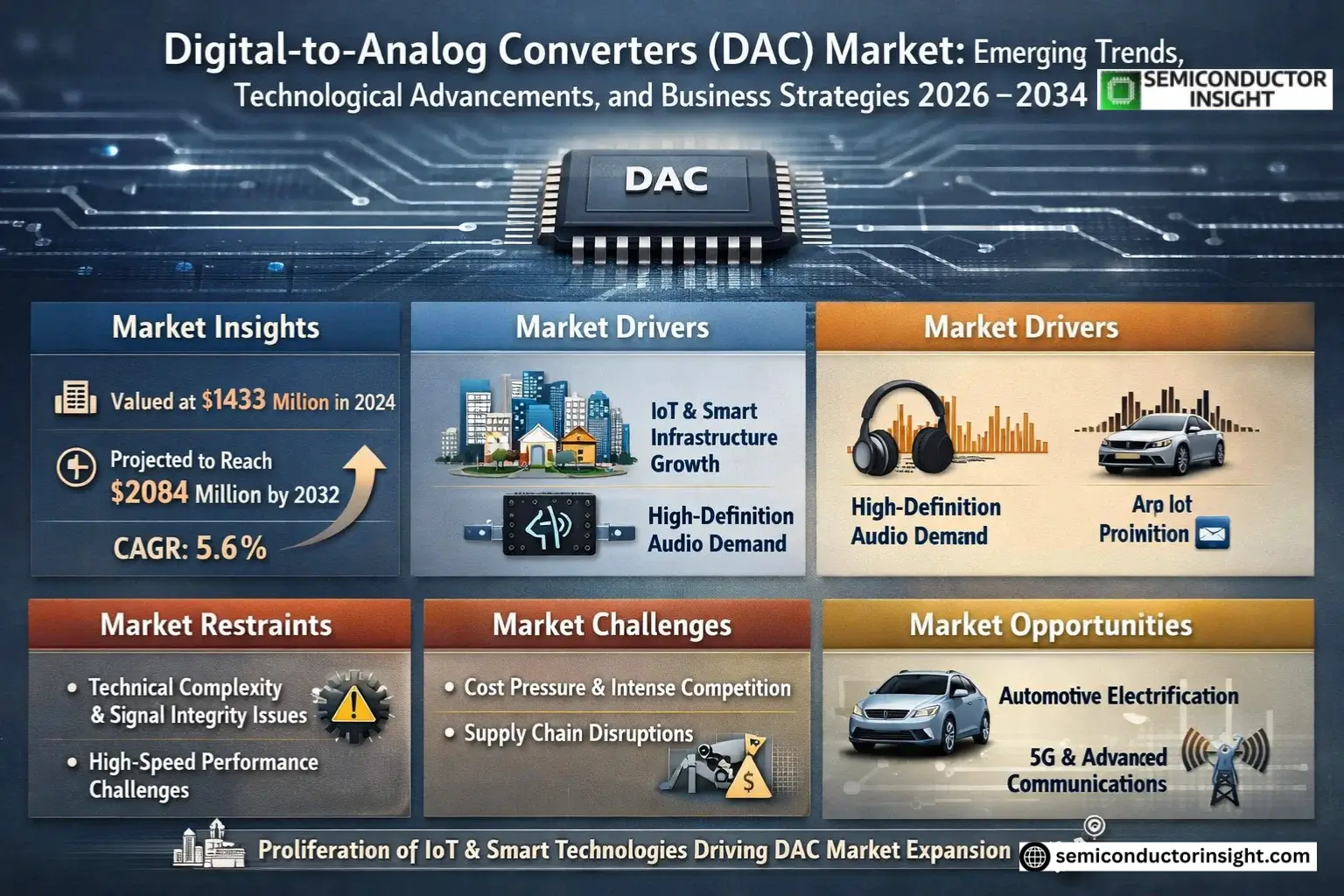

Global Digital-to-Analog Converters (DAC) Market was valued at 1433 million in 2024 and is projected to reach USD 2084 million by 2032, at a CAGR of 5.6% during the forecast period.

Digital-to-analog converters (DACs) are critical semiconductor devices that translate digital signals into precise analog voltages or currents. These components are fundamental to processing and control systems across a vast array of applications, offering high speed, resolution, and accuracy in various package options. Their functionality is essential for bridging the digital world with analog outputs in industrial automation, automotive systems, communication infrastructure, and consumer electronics.

The market’s expansion is underpinned by the relentless proliferation of Internet of Things (IoT) devices and the advancement of smart technologies, which demand high-performance, low-power DAC solutions. This is further accelerated by upgrade cycles in consumer electronics, particularly the integration of high-definition audio into smartphones and tablets. In industrial settings, the push for greater automation and precision measurement is creating a significant need for high-accuracy DACs. The market is highly concentrated, with the top four companies ADI, TI, Microchip, and Renesas Electronics collectively holding over 95% of the market share, underscoring a competitive landscape dominated by established technological leaders.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of IoT Devices and Smart Infrastructure to Accelerate DAC Adoption

The rapid expansion of Internet of Things (IoT) ecosystems is significantly driving demand for digital-to-analog converters. With over 15 billion active IoT devices globally and projections indicating growth to exceed 29 billion by 2030, the need for high-performance DAC technology has become critical. These devices require precise analog signal generation for sensors, actuators, and control systems across smart homes, industrial automation, and urban infrastructure. The transition toward Industry 4.0 has further intensified this demand, as manufacturing facilities increasingly rely on DACs for precision motion control, process automation, and real-time monitoring systems. The automotive sector’s evolution toward electric vehicles and advanced driver-assistance systems (ADAS) has created additional momentum, with modern vehicles incorporating numerous DACs for infotainment systems, battery management, and sensor interfaces.

Consumer Electronics Upgrade Cycle and High-Definition Audio Demand to Fuel Market Growth

The continuous innovation in consumer electronics represents a substantial driver for the DAC market. Global smartphone market, exceeding 1.4 billion units annually, increasingly incorporates high-quality audio DACs to support premium sound experiences. The trend toward wireless audio accessories, including true wireless stereo earbuds and headphones, has created massive demand for compact, low-power DAC solutions. High-resolution audio standards have become a differentiating factor in consumer devices, prompting manufacturers to integrate advanced DAC architectures that support sampling rates up to 384kHz and bit depths of 32 bits. The gaming industry’s growth has further stimulated demand, with gaming consoles, PCs, and peripherals requiring high-performance audio conversion for immersive experiences. Virtual and augmented reality applications are emerging as additional growth vectors, demanding ultra-low latency and high-resolution DAC performance.

Furthermore, the integration of voice assistant technologies across multiple device categories has created new requirements for high-quality audio conversion.

Additionally, the convergence of multiple functionalities in portable devices has driven the development of highly integrated DAC solutions that combine digital processing with analog conversion capabilities.

MARKET RESTRAINTS

Technical Complexity and Signal Integrity Challenges to Constrain Market Expansion

Despite strong market growth, digital-to-analog converters face significant technical constraints that impact widespread adoption. The increasing demand for higher resolution and faster conversion speeds introduces complex design challenges related to signal integrity, noise reduction, and power consumption. As DAC resolutions advance beyond 16 bits and sampling rates exceed several hundred megahertz, maintaining signal purity becomes increasingly difficult. Jitter effects, clock synchronization issues, and electromagnetic interference can degrade performance in high-speed applications. These technical hurdles are particularly pronounced in communication systems where 5G infrastructure requires DACs capable of handling multi-gigahertz bandwidths while maintaining exceptional linearity and dynamic range. The automotive industry presents additional challenges, where extreme temperature variations and harsh operating environments demand robust DAC solutions that maintain performance across demanding conditions.

Furthermore, the integration of multiple DAC channels within single packages creates thermal management challenges that can affect long-term reliability and performance consistency.

MARKET CHALLENGES

Increasing Cost Pressure and Intense Competition to Challenge Profitability

Digital-to-Analog Converters (DAC) Market faces substantial pricing pressures despite growing demand, particularly in consumer applications where cost sensitivity is extreme. Manufacturing advanced DAC chips requires sophisticated semiconductor processes, often utilizing specialized analog/mixed-signal technologies that carry higher production costs compared to digital ICs. The research and development investment required for cutting-edge DAC designs can exceed several million dollars per development cycle, creating significant barriers for new market entrants. Established players maintain cost advantages through economies of scale and vertical integration, but margin erosion remains a persistent challenge across the industry. The consumer electronics segment, accounting for approximately 35% of DAC revenue, exerts particularly strong price pressure, forcing manufacturers to balance performance enhancements against aggressive cost targets.

Other Challenges

Supply Chain Vulnerabilities

Global semiconductor supply chain disruptions continue to impact DAC availability and pricing. The concentration of advanced semiconductor manufacturing in specific geographic regions creates vulnerability to geopolitical tensions, trade restrictions, and production capacity constraints. These factors can lead to extended lead times and price volatility that affect market stability.

Technology Migration Barriers

The transition to more advanced process nodes presents significant technical and financial challenges. While digital circuits benefit from process scaling, analog components often face performance degradation when migrated to smaller geometries, requiring innovative design techniques and additional mask layers that increase development complexity and cost.

MARKET OPPORTUNITIES

Emerging Applications in Automotive Electrification and 5G Infrastructure to Create New Growth Frontiers

The transformation of automotive systems toward electrification and autonomy presents substantial opportunities for DAC manufacturers. Modern electric vehicles incorporate numerous high-precision DAC applications, including battery management systems, motor control, and advanced sensor interfaces. The autonomous driving revolution requires sophisticated LiDAR and radar systems that depend on high-speed, high-resolution DAC technology. The communications infrastructure sector offers parallel growth potential, with 5G network deployments demanding advanced DAC solutions for beamforming, massive MIMO systems, and millimeter-wave applications. These emerging applications typically require higher performance specifications and command premium pricing compared to traditional market segments, providing opportunities for margin improvement and technological differentiation.

Additionally, the industrial automation sector’s digital transformation continues to create demand for precision DAC solutions in robotics, process control, and test and measurement equipment.

Furthermore, the medical electronics segment represents a growing opportunity, with diagnostic imaging, patient monitoring, and therapeutic devices increasingly relying on high-performance data conversion technology.

DIGITAL-TO-ANALOG CONVERTERS (DAC) MARKET TRENDS

Proliferation of IoT and Smart Technologies Driving Market Expansion

The exponential growth of the Internet of Things (IoT) ecosystem is a primary catalyst for the Digital-to-Analog Converters (DAC) Market. With over 15 billion active IoT devices globally, the demand for high-performance, low-power DACs has surged, as these components are fundamental in translating digital sensor data into precise analog control signals. This trend is particularly pronounced in smart city infrastructure and industrial automation, where applications such as environmental monitoring and process control require DACs with high resolution often 16-bit or greater and sampling rates exceeding 1 MSPS to ensure data integrity and system responsiveness. Furthermore, the consumer electronics segment continues to be a major driver, with the integration of high-fidelity audio DACs in smartphones, tablets, and wireless earbuds becoming a standard feature, pushing manufacturers to develop solutions that offer superior signal-to-noise ratios while minimizing power consumption to extend battery life.

Other Trends

Advancements in Automotive Electronics

The automotive industry’s rapid transformation towards electrification and autonomous driving is creating substantial demand for advanced DACs. These converters are critical components in systems like Advanced Driver-Assistance Systems (ADAS), infotainment units, and battery management systems (BMS) for electric vehicles. For instance, the number of sensors in a modern vehicle can exceed 100 units, many of which rely on DACs for actuator control and user interface feedback. The market is responding with products designed for automotive-grade reliability, capable of operating in extended temperature ranges from -40°C to +125°C and offering enhanced electromagnetic compatibility (EMC) to function reliably in the electrically noisy environment of a vehicle.

Miniaturization and Integration Reshaping Product Design

A significant and persistent trend is the relentless push towards miniaturization and higher levels of integration. As end-products become smaller and more feature-rich, DAC manufacturers are innovating packaging technologies and system-on-chip (SoC) designs to deliver more functionality in a smaller footprint. This is evident in the communications sector, where the rollout of 5G infrastructure requires highly integrated RF DACs that can support massive MIMO antennas and wide bandwidths while being power-efficient. Concurrently, the industry is focusing on reducing power consumption, not just for portable devices but also to align with global sustainability initiatives. Newer DAC architectures are achieving power dissipation figures below 1 mW at lower sampling rates, making them ideal for always-on IoT applications. This trend towards integrated, low-power, and miniature solutions is opening new application areas while simultaneously posing engineering challenges related to heat dissipation and signal integrity in densely packed electronic assemblies.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Dominance Through Technological Innovation and Strategic Expansion

Global Digital-to-Analog Converters (DAC) Market exhibits a highly concentrated structure, dominated by a handful of major semiconductor manufacturers who collectively control over 95% of the market share. This concentration is primarily due to the significant capital investment required for semiconductor fabrication and the complex intellectual property surrounding high-performance DAC designs. While numerous smaller players exist, they typically focus on niche applications or specific regional markets.

Analog Devices, Inc. (ADI) stands as the undisputed market leader, leveraging its extensive portfolio of high-precision and high-speed DACs. Its dominance is reinforced by strategic acquisitions, such as the integration of Linear Technology’s product lines, which expanded its capabilities in industrial and automotive applications. ADI’s global manufacturing footprint and strong R&D focus, with annual investments exceeding D 1.5 billion, allow it to continuously set industry benchmarks for performance and power efficiency.

Texas Instruments (TI) commands a formidable market position, particularly in the consumer electronics and industrial segments. The company’s strength lies in its massive scale and vertical integration, enabling cost-effective production of a broad range of DACs. TI’s extensive distribution network and focus on application-specific solutions, especially for audio and portable devices, have cemented its status as a key supplier to major OEMs worldwide.

These industry giants are continuously strengthening their positions through aggressive research and development initiatives aimed at developing next-generation DACs with higher integration, lower power consumption, and enhanced functionality for emerging applications like 5G infrastructure and autonomous vehicles.

Meanwhile, other significant players like Microchip Technology and Renesas Electronics are carving out strong niches. Microchip has gained considerable traction in the industrial automation and automotive sectors with its robust and reliable DAC solutions, often integrated into larger microcontroller or system-on-chip offerings. Renesas, with its strong presence in the Asia-Pacific region, is capitalizing on the growing automotive electronics market, supplying DACs for advanced driver-assistance systems (ADAS) and in-vehicle infotainment.

The competitive dynamics are further shaped by companies focusing on ultra-high-fidelity audio applications, such as ESS Technology, which is renowned among audiophiles and premium consumer audio brands. Furthermore, Japanese and European semiconductor firms, including ROHM Semiconductor and STMicroelectronics, are strengthening their market presence through innovations in energy efficiency and miniaturization, catering to the stringent requirements of the European and Asian automotive and industrial markets.

List of Key Digital-to-Analog Converter (DAC) Companies Profiled

- Analog Devices, Inc. (ADI) (U.S.)

- Texas Instruments Incorporated (TI) (U.S.)

- Microchip Technology Inc. (U.S.)

- Renesas Electronics Corporation (Japan)

- ESS Technology, Inc. (U.S.)

- Nisshinbo Micro Devices Inc. (Japan)

- ROHM Semiconductor (Japan)

- STMicroelectronics N.V. (Switzerland)

Segment Analysis:

By Type

R-2R Segment Dominates the Market Due to its Superior Linearity and Precision in High-Resolution Applications

The market is segmented based on type into:

- R-2R

- String

- Current Source and Sink

- Others

By Application

Industrial Segment Leads Due to High Adoption in Automation, Process Control, and Measurement Systems

The market is segmented based on application into:

- Industrial

- Communications

- Automotive

- Consumer Electronics

Regional Analysis: Digital-to-Analog Converters (DAC) Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global DAC market, accounting for nearly 45% of total consumption. This dominance is fueled by a massive consumer electronics manufacturing base, particularly in China, South Korea, and Taiwan, which demands high volumes of DACs for smartphones, tablets, and audio equipment. Furthermore, significant government investments in 5G infrastructure across China and India are accelerating the deployment of communication networks, creating robust demand for high-speed, precision DACs. The region’s thriving industrial automation sector, especially in Japan and Southeast Asia, also relies heavily on these components for process control and measurement. While cost-competitive, standard-performance DACs are widely used, there is a clear and accelerating trend toward adopting higher-performance, energy-efficient solutions to meet the requirements of next-generation applications.

North America

North America represents a highly advanced and innovation-driven market for DACs, characterized by stringent performance requirements and early adoption of cutting-edge technologies. The region’s strength lies in its robust semiconductor design ecosystem, led by key players and demanding end-markets in the United States and Canada. Demand is primarily propelled by the communications sector, driven by relentless 5G network rollouts and data center expansions, which require DACs with exceptional speed and signal integrity. Additionally, the automotive industry’s rapid advancement toward electric and autonomous vehicles is creating significant opportunities for high-reliability DACs used in advanced driver-assistance systems (ADAS) and in-vehicle infotainment. The focus is overwhelmingly on high-value, high-performance products that offer superior precision and lower power consumption.

Europe

Europe maintains a strong position in the DAC market, underpinned by its world-leading automotive and industrial manufacturing sectors. German and French automotive OEMs and suppliers are at the forefront of integrating sophisticated electronics, fueling demand for automotive-grade DACs that meet rigorous quality and safety standards, such as AEC-Q100. The region’s industrial landscape, with its emphasis on Industry 4.0 and smart manufacturing, necessitates high-accuracy DACs for precision instrumentation and control systems. While the market is mature, growth is sustained by innovation and a regulatory environment that encourages energy efficiency. European manufacturers often specialize in niche, high-performance segments, differentiating themselves through technical excellence and reliability rather than competing on volume or cost.

South America

Digital-to-Analog Converters (DAC) Market in South America is emerging and presents a landscape of gradual growth potential. Countries like Brazil and Argentina are seeing increased investment in industrial automation and telecommunications infrastructure, which slowly drives demand for these components. However, the market’s expansion is frequently tempered by economic volatility and currency fluctuations, which can constrain capital expenditure on advanced electronic systems. Consequently, price sensitivity often leads to a higher prevalence of cost-effective, mainstream DAC solutions rather than cutting-edge, premium products. While opportunities exist, particularly in modernizing industrial and communication networks, the market’s trajectory is closely tied to regional economic stability and investment climates.

Middle East & Africa

The Middle East and Africa region represents a nascent but promising market for DACs. Development is primarily concentrated in wealthier Gulf Cooperation Council (GCC) nations, such as Saudi Arabia and the UAE, where investments in smart city initiatives, telecommunications, and infrastructure projects are creating new demand. However, the broader region faces challenges, including limited local manufacturing capabilities and fragmented industrial development, which slows the adoption pace. Demand is often project-driven and focused on durability and performance for specific applications in harsh environments. While not yet a major volume driver on the global stage, the region’s long-term growth potential is recognized as urbanization and digitalization efforts continue to gain momentum.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Semiconductor and Electronics markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Digital-to-Analog Converters (DAC) Market?

-> Digital-to-Analog Converters (DAC) Market was valued at 1433 million in 2024 and is projected to reach USD 2084 million by 2032, at a CAGR of 5.6% during the forecast period.

Which key companies operate Global Digital-to-Analog Converters (DAC) Market?

-> Key players include Analog Devices Inc. (ADI), Texas Instruments (TI), Microchip Technology, Renesas Electronics, ESS Technology, Nisshinbo Micro Devices, ROHM Semiconductor, and STMicroelectronics, among others.

What are the key growth drivers?

-> Key growth drivers include the proliferation of IoT devices, advancements in smart home and smart city projects, consumer electronics upgrade cycles, and increased demand for high-precision solutions in industrial automation.

Which region dominates the market?

-> Asia-Pacific is the largest market, accounting for nearly 45% of global revenue, while North America and Europe collectively hold over 45% market share.

What are the emerging trends?

-> Emerging trends include higher integration, lower power consumption, miniaturization, advancements in 5G and autonomous driving technologies, and the development of environmentally friendly and energy-efficient DAC solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...