MARKET INSIGHTS

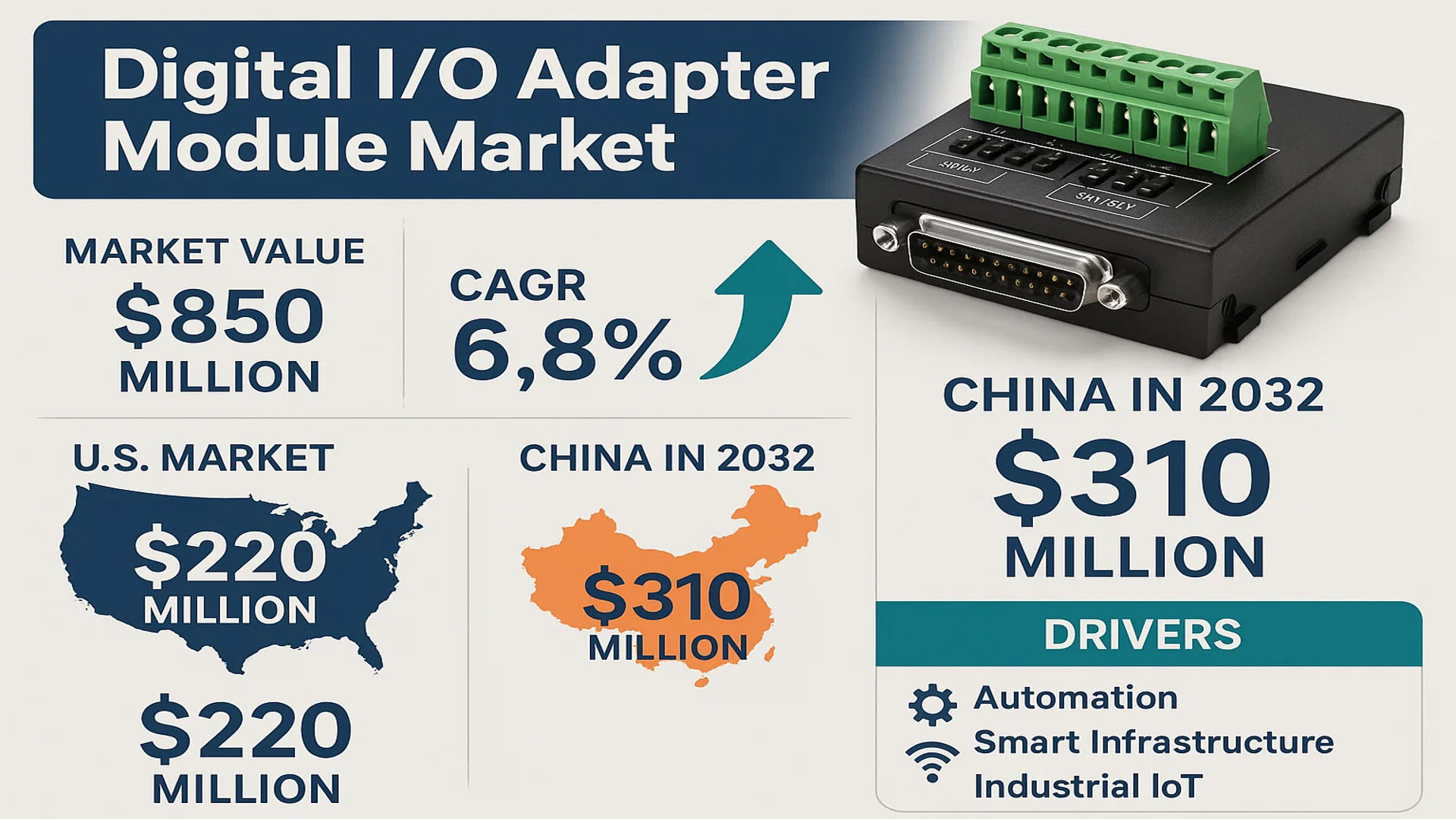

The global Digital I/O Adapter Module Market was valued at 850 million in 2024 and is projected to reach US$ 1344 million by 2032, at a CAGR of 6.8% during the forecast period. The U.S. market is estimated at USD 220 million in 2024, while China is expected to account for USD 310 million by 2032, driven by rapid industrialization and automation.

A Digital I/O (Input/Output) Adapter Module is a hardware interface that facilitates digital signal communication between computer systems or test equipment and external devices. These modules are essential for connecting and controlling peripherals such as sensors, actuators, switches, and LEDs across industries like industrial automation, aerospace, and automotive electronics. Key functionalities include signal conditioning, isolation, and protocol conversion, ensuring seamless integration with control systems.

Market expansion is fueled by rising demand for automation in manufacturing, smart infrastructure development, and advancements in Industrial IoT (IIoT). The General Purpose segment dominates applications, while the Industrial Automation sector holds the largest market share. Leading players like NI, Keysight Technologies, and Advantech collectively held a significant revenue share in 2024, supported by innovations in high-speed and ruggedized modules for harsh environments.

MARKET DYNAMICS

MARKET DRIVERS

Accelerating Industrial Automation Adoption Boosts Digital I/O Module Demand

The global push towards Industry 4.0 is driving unprecedented demand for digital I/O adapter modules as manufacturing facilities worldwide modernize their operations. Automation investments reached $48 billion globally in 2024, with manufacturing accounting for 58% of these expenditures. Digital I/O modules serve as critical interfaces between control systems and field devices, enabling real-time monitoring and control in smart factories. The automotive sector alone has increased adoption rates by 19% year-over-year, using these modules for robotic assembly lines and quality control systems. As factories transition to interconnected production environments, the need for reliable digital signal conversion continues to expand across multiple industry verticals.

Expansion of IoT Infrastructure Creates New Integration Needs

With over 75 billion IoT devices projected to be in operation by 2032, digital I/O modules play a pivotal role in bridging legacy equipment with modern networked systems. These modules enable seamless data acquisition from sensors and control signals to actuators in smart buildings, energy grids, and transportation systems. The commercial building automation sector has shown particularly strong growth, with digital I/O implementations increasing by 27% annually. Recent technological advances have produced modules with enhanced noise immunity and higher channel density, making them ideal for handling the complex signal requirements of large-scale IoT deployments while maintaining backward compatibility.

Advancements in Medical Equipment Technology Spur Module Innovation

The medical device sector’s rapid digital transformation is creating specialized opportunities for high-reliability digital I/O solutions. New diagnostic imaging systems and patient monitoring equipment require modules that meet stringent electromagnetic compatibility standards while delivering ultra-low latency signal processing. The global medical electronics market is projected to grow at 6.3% CAGR through 2032, with digital interface components representing approximately 18% of total system costs. Recent product launches featuring isolated digital I/O channels and medical-grade certifications demonstrate manufacturers’ responses to these emerging requirements in healthcare applications.

MARKET RESTRAINTS

Legacy System Integration Challenges Hamper Market Penetration

While digital I/O modules offer clear benefits, many industrial facilities face significant hurdles when retrofitting these components into existing control architectures. Compatibility issues with vintage Programmable Logic Controllers (PLCs) create complex engineering challenges that can increase total implementation costs by 35-45%. Older manufacturing plants often require custom interface solutions and extended validation periods, resulting in project delays that deter potential adopters. The aerospace sector, where equipment lifecycles routinely exceed 30 years, illustrates this challenge with digital I/O adoption rates lagging behind other industries by nearly a decade.

Increasing Cybersecurity Risks Limit Critical Infrastructure Adoption

The convergence of Operational Technology (OT) and Information Technology (IT) networks has exposed digital I/O systems to sophisticated cyber threats. Industrial facilities report that security concerns delay or prevent approximately 22% of planned digital transformation projects involving I/O modules. Highly regulated industries such as power generation and water treatment require extensive third-party certification of interface components, adding months to procurement cycles. Recent firmware vulnerabilities discovered in common industrial protocols have further heightened security awareness among potential buyers.

Component Shortages Disrupt Supply Chain Reliability

Ongoing semiconductor supply chain constraints continue to impact digital I/O module availability, with average lead times increasing from 8 weeks to 24 weeks across the industry. Specialty analog-to-digital converters and opto-isolators remain particularly constrained, forcing manufacturers to redesign boards or accept reduced production volumes. The automation components market saw 93 reported product discontinuations in 2023 due to these supply issues, creating replacement challenges for maintenance applications. These disruptions have pushed module prices up by 11-18% across most product categories since 2021.

MARKET OPPORTUNITIES

Smart City Infrastructure Projects Open New Application Fields

Urban digital transformation initiatives worldwide are creating substantial demand for ruggedized digital I/O solutions. Traffic management systems, environmental sensors, and smart utility networks require modules capable of operating in harsh outdoor conditions while providing deterministic response times. The global smart cities market is projected to invest $1.7 trillion in technology infrastructure between 2024-2032, with 12-15% allocated to edge connectivity components. Innovative products featuring wide-temperature operation (-40°C to +85°C) and ingress protection (IP67) ratings are gaining traction in these municipal applications.

Edge Computing Deployment Drives Need for Intelligent I/O Modules

The shift toward distributed computing architectures is transforming digital I/O modules from simple interfaces into intelligent edge nodes. Modern modules now incorporate local processing capabilities that can perform data filtering, protocol conversion, and basic analytics at the network periphery. This evolution reduces bandwidth requirements by up to 60% in large-scale installations while improving system responsiveness. Leading vendors have begun integrating ARM-based processors and embedded machine learning algorithms into their digital I/O product lines to capitalize on this emerging paradigm.

Renewable Energy Sector Presents Growth Potential

The global transition to clean energy systems is driving innovation in digital I/O solutions for wind turbines, solar farms, and grid-scale storage facilities. These applications demand modules that can withstand high-voltage transients while maintaining precise timing synchronization across distributed assets. The solar energy sector alone is forecast to deploy 4.7 million new digital monitoring points annually by 2026. Specialized products featuring reinforced isolation (3kV+) and precision timestamping capabilities are positioning manufacturers to serve this expanding market segment effectively.

MARKET CHALLENGES

Rapid Technology Obsolescence Requires Continuous R&D Investment

The accelerating pace of industrial communication standards evolution forces digital I/O module manufacturers to maintain substantial engineering budgets simply to remain competitive. Transitioning product lines to support new fieldbus protocols like IO-Link and TSN requires complete hardware redesigns every 4-5 years on average. Smaller vendors report spending 28-35% of annual revenue on R&D to keep pace with these changes, creating financial pressures that can constrain market participation. The automotive industry’s upcoming shift to zonal architectures exemplifies this challenge, requiring entirely new interface approaches for next-generation vehicle networks.

Intense Price Competition Squeezes Profit Margins

Standard digital I/O modules have become increasingly commoditized, with average selling prices declining 7% annually in basic product categories. Asian manufacturers now control 63% of the global market for low-end modules through aggressive pricing strategies. This competitive pressure has forced established vendors to focus on specialized high-value segments, creating market fragmentation. The industrial Ethernet module segment illustrates this trend, where premium products command 3-5x higher prices than basic models despite sharing similar core functionality.

Regulatory Compliance Adds Product Development Complexity

Diverging regional certification requirements for industrial equipment create significant bottlenecks in global product rollouts. A single digital I/O module may require separate approvals for CE, UL, CCC, and other regional standards, each with unique testing protocols. The European Union’s recent updates to the Machinery Directive have added 3-6 months to product development cycles, while China’s evolving cybersecurity laws introduce new data handling requirements. These regulatory demands particularly impact manufacturers attempting to serve both traditional industrial markets and emerging applications with a common product platform.

DIGITAL I/O ADAPTER MODULE MARKET TRENDS

Industrial Automation Integration Driving Market Expansion

The rapid adoption of Industry 4.0 practices has significantly boosted demand for Digital I/O Adapter Modules, particularly in industrial automation applications. These modules play a crucial role in enabling real-time data communication between PLCs, sensors, and control systems, with the market witnessing a compound annual growth rate (CAGR) of 6.8% from 2024 to 2032. Modern manufacturing facilities are increasingly implementing high-speed digital I/O solutions that support Ethernet/IP and PROFINET protocols, allowing for seamless integration with smart factory ecosystems. While North America currently leads in adoption due to advanced manufacturing infrastructure, Asia-Pacific shows the fastest growth trajectory as regional manufacturers upgrade legacy equipment.

Other Trends

Test & Measurement Applications

Digital I/O Adapter Modules are becoming essential in automated test equipment (ATE) across aerospace, automotive, and semiconductor industries. The ability to provide precise digital signal conditioning at sampling rates exceeding 1 MHz makes these modules ideal for quality assurance processes. Recent developments include PXIe-based modules offering channel densities above 64 I/Os per slot, significantly reducing test system footprints. This trend aligns with the broader market shift toward modular instrumentation, valued at over $2 billion globally, where flexible I/O configurations enable customized test solutions.

Medical Equipment Innovation Creates New Opportunities

The healthcare sector is emerging as a key growth vertical for Digital I/O Adapter Modules, particularly in medical imaging systems and diagnostic equipment. Modules featuring isolated digital channels (up to 2500Vrms) ensure patient safety while maintaining signal integrity in EMV-sensitive environments. Recent FDA approvals for AI-assisted diagnostic devices have further driven demand for high-performance I/O interfaces capable of handling multi-modal data acquisition. Leading manufacturers are responding with medical-grade modules that combine EN 60601-1 certification with enhanced EMC performance, addressing the stringent requirements of Class II medical devices.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Leverage Technological Innovation to Expand Digital I/O Solutions

The global Digital I/O Adapter Module market exhibits a competitive yet fragmented structure, with established technology providers and emerging regional players vying for market share. NI (National Instruments) and Keysight Technologies currently dominate the market, collectively accounting for over 25% of the 2024 global revenue share. Their leadership stems from comprehensive product portfolios spanning industrial automation, aerospace, and automotive electronics applications.

ADLINK Technology has emerged as a formidable competitor through strategic partnerships with industrial automation providers across Europe and Asia-Pacific. Meanwhile, Advantech continues to strengthen its position through robust R&D investments, particularly in high-speed digital I/O modules for machine vision applications.

Market dynamics show increasing competition from specialized manufacturers like Spectrum Instrumentation and Pickering Interfaces, who differentiate through high-performance modular solutions. These players are rapidly gaining traction in test & measurement applications where precision and low-latency signal processing are critical.

The competitive landscape is further evolving through consolidation, as seen in Schneider Electric’s acquisition of niche providers to expand its industrial IoT ecosystem. Such strategic moves are reshaping vendor positioning while driving innovation in modular digital I/O solutions.

List of Key Digital I/O Adapter Module Manufacturers

- NI (National Instruments) (U.S.)

- Keysight Technologies (U.S.)

- ADLINK Technology (Taiwan)

- Advantech (Taiwan)

- Contec (Japan)

- Spectrum Instrumentation (Germany)

- Pickering Interfaces (U.K.)

- Tektronix (U.S.)

- Kontron (Germany)

- Schneider Electric (France)

Segment Analysis:

By Type

General Purpose Segment Leads the Market Due to Versatile Applications Across Industries

The market is segmented based on type into:

- General Purpose

- Special Purpose

- Others

By Application

Industrial Automation Dominates Global Demand Owing to Increased Manufacturing Digitization

The market is segmented based on application into:

- Industrial Automation

- Aerospace

- Automotive Electronics

- Medical Equipment

- Other

By Channel Count

High-Channel Modules Gain Traction for Complex System Integration Needs

The market is segmented based on channel count into:

- Low Channel (1-16)

- Medium Channel (17-64)

- High Channel (65+)

By Interface

USB-based Modules Show Strong Growth Due to Plug-and-Play Convenience

The market is segmented based on interface into:

- USB

- PCI/PCIe

- Ethernet

- Wireless

- Others

Regional Analysis: Digital I/O Adapter Module Market

Asia-Pacific

The Asia-Pacific region dominates the global Digital I/O Adapter Module market, accounting for over 40% of the total market share in 2024. This leadership position stems from rapid industrialization, particularly in China, Japan, and India, where massive investments in industrial automation and smart manufacturing are driving demand. China’s manufacturing sector, which contributes approximately 28% to global manufacturing output, heavily relies on digital I/O modules for factory automation and process control. Japan’s strong automotive electronics sector and India’s growing medical equipment industry further bolster the market. Local manufacturers like Wuxi Lingke Automation Technology and Shanghai Jiaolei Automation Technology are gaining traction by offering cost-effective solutions tailored to regional needs.

North America

North America represents a mature yet growing market for Digital I/O Adapter Modules, characterized by technological innovation and high adoption in aerospace and defense applications. The U.S. accounts for nearly 75% of regional demand, with major players like NI and Keysight Technologies headquartered there. Strict industry standards in sectors such as medical equipment and automotive electronics drive demand for high-precision modules. Furthermore, the increasing integration of Industrial Internet of Things (IIoT) in manufacturing is creating new opportunities for smart digital I/O solutions with advanced diagnostics and remote monitoring capabilities.

Europe

Europe maintains steady growth in the Digital I/O Adapter Module market, supported by its robust industrial automation sector and stringent quality standards. Germany leads regional adoption due to its strong manufacturing base, particularly in automotive production where digital I/O modules are essential for production line automation. The region’s focus on Industry 4.0 initiatives is driving upgrades to smarter, more connected industrial systems. Environmental regulations are also pushing manufacturers toward energy-efficient solutions, benefiting suppliers like Kontron and Schneider Electric that offer eco-conscious product lines.

South America

The South American market is emerging as local industries gradually modernize their manufacturing processes. Brazil shows the most potential, with its growing automotive and food processing sectors adopting digital I/O modules for equipment automation. However, economic instability and reliance on imported technology limit market expansion. Local manufacturers face challenges competing with global brands, though partnerships with international suppliers are beginning to improve product availability and technical support in the region.

Middle East & Africa

This region represents the smallest but fastest growing market for Digital I/O Adapter Modules, with growth driven by oil and gas industry automation and infrastructure development. The UAE and Saudi Arabia lead adoption, particularly in industrial applications related to energy production. While the market remains constrained by limited local manufacturing capabilities and reliance on imports, government initiatives to diversify economies are creating new opportunities in sectors like water treatment and renewable energy that increasingly require industrial automation solutions.

Report Scope

This market research report provides a comprehensive analysis of the Global Digital I/O Adapter Module market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 850 million in 2024 and is projected to reach USD 1,344 million by 2032, growing at a CAGR of 6.8%.

- Segmentation Analysis: Detailed breakdown by product type (General Purpose, Special Purpose), application (Industrial Automation, Aerospace, Automotive Electronics, Medical Equipment), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. and China are key markets with significant growth potential.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Key players include NI, Keysight Technologies, ADLINK, Advantech, and Schneider Electric.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Digital I/O Adapter Module Market?

-> Digital I/O Adapter Module Market was valued at 850 million in 2024 and is projected to reach US$ 1344 million by 2032, at a CAGR of 6.8% during the forecast period..

Which key companies operate in Global Digital I/O Adapter Module Market?

-> Key players include NI, Keysight Technologies, ADLINK, Advantech, Contec, Spectrum Instrumentation, Pickering Interfaces, Tektronix, Kontron, and Schneider Electric, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for industrial automation, advancements in IoT and AI integration, and increasing adoption in automotive and aerospace applications.

Which region dominates the market?

-> North America leads in market share, while Asia-Pacific is the fastest-growing region due to industrial expansion.

What are the emerging trends?

-> Emerging trends include high-speed digital I/O modules, modular and scalable solutions, and integration with smart manufacturing systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...