MARKET INSIGHTS

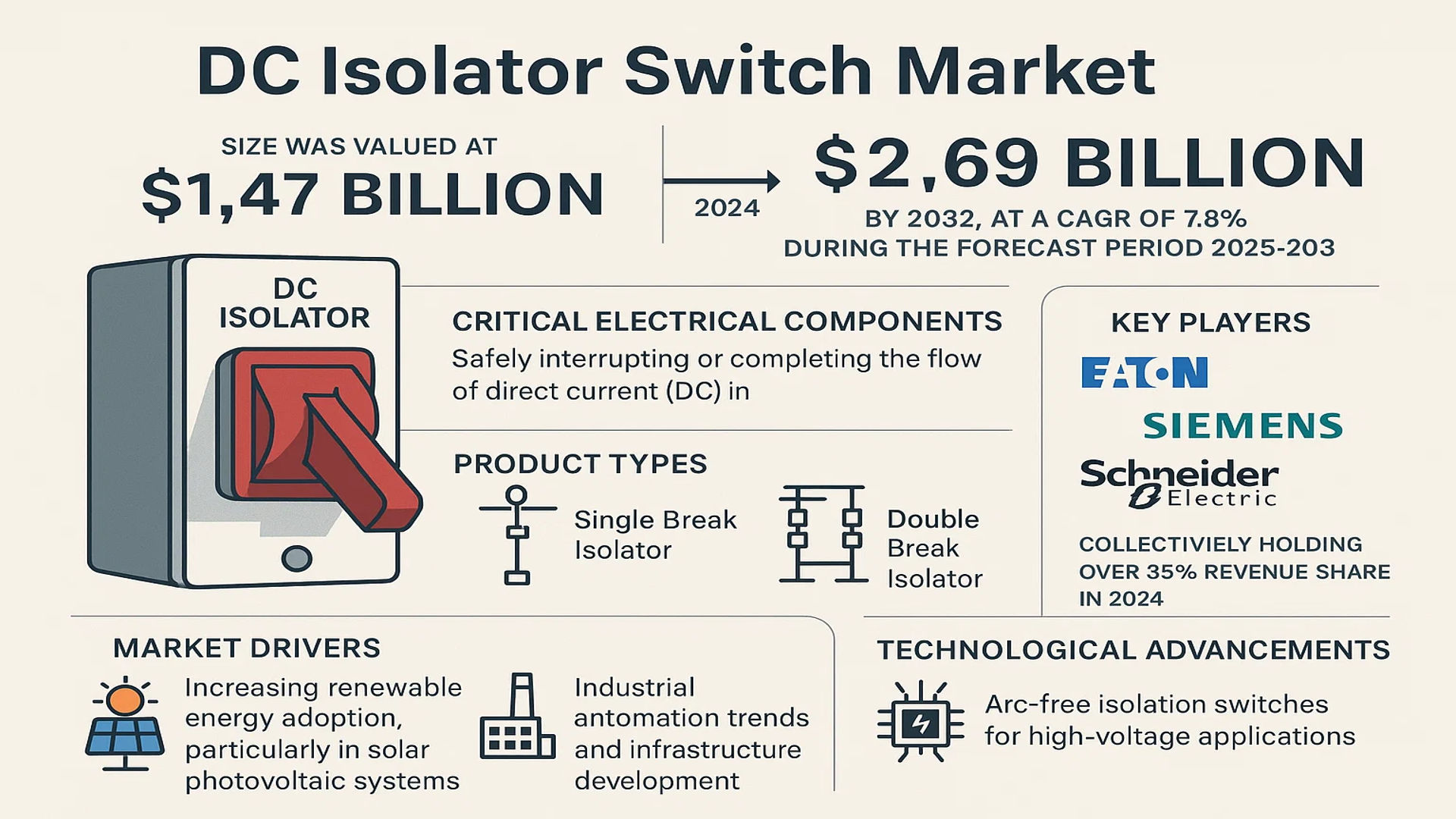

The global DC Isolator Switch Market size was valued at US$ 1.47 billion in 2024 and is projected to reach US$ 2.69 billion by 2032, at a CAGR of 7.8% during the forecast period 2025-2032.

DC isolator switches are critical electrical components designed to safely interrupt or complete the flow of direct current (DC) in various applications. These devices play a vital role in renewable energy systems, industrial setups, and commercial installations where circuit isolation is required for maintenance or emergency shutdowns. The market primarily consists of two product types: Single Break Isolators and Double Break Isolators, each serving different voltage and application requirements.

The market growth is driven by increasing renewable energy adoption, particularly in solar photovoltaic systems where DC isolation is mandatory for safety compliance. Furthermore, industrial automation trends and infrastructure development in emerging economies are creating substantial demand. Key players like Eaton, Siemens, and Schneider Electric dominate the market, collectively holding over 35% revenue share in 2024. Recent technological advancements include the development of arc-free isolation switches for high-voltage applications, addressing critical safety concerns in the industry.

MARKET DYNAMICS

MARKET DRIVERS

Exponential Growth in Renewable Energy Installations Fueling Market Demand

The global shift toward renewable energy sources is creating unprecedented demand for DC isolator switches. Solar photovoltaic installations alone are projected to grow at a CAGR of 8% through 2030, requiring robust safety components like DC isolators. These devices play a critical role in photovoltaic systems by enabling safe maintenance and emergency shutdowns, with installation mandates increasing across commercial and utility-scale projects. Regions leading the solar boom, particularly Asia-Pacific and North America, are driving significant market expansion through renewable energy policies and incentives.

Stringent Safety Regulations Accelerating Product Adoption

Electrical safety standards worldwide are becoming more rigorous, particularly for DC applications in renewable energy systems. The International Electrotechnical Commission (IEC) has implemented updated guidelines requiring mandatory isolation in DC circuits above 120V. This regulatory push has increased adoption across residential solar installations where safety concerns are paramount. Manufacturers are responding with innovative designs that meet IEC 60947-3 and other regional certifications, creating opportunities for premium, compliant products in both developed and emerging markets.

Technological Advancements in Switch Design Driving Performance Standards

Innovation in DC isolator technology is revolutionizing market potential. New arc-fault detection capabilities and integrated monitoring systems are becoming industry standards, with the latest models offering remote operation and smart grid compatibility. Leading manufacturers are developing switches with higher voltage ratings (up to 1500V DC) and improved durability (50,000+ operations), addressing the needs of next-generation solar farms and battery storage systems. These technological leaps are enabling safer, more efficient power management in critical energy infrastructure.

MARKET RESTRAINTS

High Initial Costs and Price Sensitivity Restricting Market Penetration

While DC isolator switches are essential safety components, their premium pricing poses challenges in cost-sensitive markets. High-quality industrial-grade switches can cost 40-60% more than basic models, creating resistance in price-driven segments. This is particularly evident in developing economies where solar adopters prioritize affordability over advanced safety features. The situation is compounded by the need for certified installers, adding 15-20% to total system costs in regulated markets. Manufacturers face ongoing pressure to reduce production costs without compromising critical safety standards.

Technical Complexities in High-Voltage Applications Creating Adoption Barriers

As solar systems transition to higher voltages (1000V+), DC isolators face mounting technical challenges. Arcing phenomena become more severe at elevated voltages, requiring advanced materials and designs that can safely interrupt DC currents. Field data indicates that nearly 30% of premature isolator failures occur in systems operating above 800V DC. Manufacturers must invest heavily in R&D to develop reliable high-voltage solutions, while end-users grapple with compatibility issues when upgrading existing infrastructure. These technical hurdles are slowing adoption rates in cutting-edge renewable energy projects.

Other Restraints

Supply Chain Vulnerabilities

The global nature of the photovoltaic industry creates dependencies on international supply chains for critical components. Recent disruptions have caused lead times for specialty DC components to extend by 25-30 weeks, forcing project delays. This fragility is particularly problematic for markets requiring region-specific certifications, where alternative suppliers are limited.

Installation Complexity

Proper DC isolator integration requires specialized knowledge of both electrical systems and local regulations. The scarcity of certified installers in emerging markets is causing inconsistent implementation, sometimes compromising system safety and performance.

MARKET CHALLENGES

Maintaining Safety Standards Amid Rapid Technological Evolution

The DC isolator market faces significant challenges in keeping pace with evolving safety requirements while supporting next-generation energy systems. New battery storage configurations and hybrid renewable installations are testing traditional isolation approaches. Emerging standards for DC arc fault protection and rapid shutdown are driving costly redesign cycles, with certification processes often taking 12-18 months per product iteration. This creates a challenging environment where technological advancement must balance with rigorous safety validation.

Intense Competition from Alternative Isolation Technologies

Traditional mechanical DC isolators face growing competition from solid-state alternatives and integrated protection devices. These alternatives promise longer lifetimes and reduced maintenance, though currently at higher price points. The competitive landscape is further complicated by increasing vertical integration in the solar sector, where major panel manufacturers are developing proprietary DC safety solutions. Traditional isolator suppliers must differentiate through reliability, certification breadth, and system-level value propositions to maintain market position.

Other Challenges

Skills Gap in Installation Workforce

The specialized nature of DC system installation requires continuous training to address evolving technologies and standards. Industry surveys indicate that only 40% of solar installers receive annual training on updated electrical safety practices, creating potential safety gaps in the field.

Environmental Durability Concerns

Outdoor DC isolators must withstand extreme weather conditions while maintaining reliable operation. Field failures due to moisture ingress or thermal stress remain a significant concern, particularly in harsh climatic regions where maintenance access is limited.

MARKET OPPORTUNITIES

Emerging Markets Present Untapped Potential for Growth

Developing economies represent a significant growth frontier for DC isolator switches as they expand renewable energy infrastructure. Countries in Southeast Asia and Africa are implementing ambitious solar programs with local content requirements, creating opportunities for regional partnerships. The commercial and industrial segment is particularly promising, with projected growth rates exceeding 15% annually in these markets. Strategic localization of manufacturing and distribution can capture this potential while addressing cost sensitivities through regional supply chain optimization.

Integration with Smart Grids and IoT Creating New Applications

The digital transformation of energy systems is opening new possibilities for intelligent DC isolation solutions. Next-generation switches with embedded sensors and communication capabilities can provide real-time system diagnostics, enabling predictive maintenance. This evolution aligns with the broader Industry 4.0 movement in energy infrastructure, where data-driven decision making is becoming standard. Early adopters are developing cloud-connected isolators that integrate with energy management systems, creating additional value for large-scale commercial and utility installations.

Innovation in Materials and Design Paving Way for Next-Generation Products

Material science breakthroughs are enabling significant product advancements in the DC isolator space. New conductive polymers and ceramic composites are extending product lifetimes while reducing maintenance requirements. Simultaneously, modular designs are simplifying installation and replacement procedures in the field. These innovations are particularly valuable for offshore solar applications and other challenging environments where reliability is paramount. Forward-looking manufacturers investing in these technologies will gain competitive advantage as performance expectations continue to rise.

DC ISOLATOR SWITCH MARKET TRENDS

Expansion of Renewable Energy Infrastructure Driving Market Growth

The rapid growth of renewable energy installations, particularly solar photovoltaic (PV) systems, is significantly boosting demand for DC isolator switches. As solar capacity expands globally—projected to reach over 2,300 GW by 2027—the need for reliable DC switching solutions has intensified. These devices play a critical role in PV system safety by enabling rapid shutdown during maintenance or emergencies. The increasing adoption of smart grid technologies further accelerates this trend, as modern grids require more sophisticated isolation mechanisms to manage bidirectional power flows from distributed generation sources. Furthermore, stringent government regulations mandating safety disconnects in solar installations continue to shape market requirements.

Other Trends

Technological Advancements in Switching Mechanisms

Manufacturers are focusing on developing more durable and efficient DC isolator switches capable of handling higher voltage ratings up to 1500V DC. Recent innovations include arc-quenching technologies that improve switch longevity in high-current applications, along with compact modular designs that simplify installation in space-constrained environments. The integration of IoT-enabled monitoring capabilities represents another key development, allowing remote status checks and predictive maintenance—features particularly valuable in large-scale commercial solar farms where manual inspections are impractical. These technological improvements are driving premium product adoption in industrial and utility-scale applications.

Shift Toward Decentralized Energy Systems

The global push toward decentralized power generation is creating new opportunities for DC isolation solutions. With residential and commercial energy storage systems expected to grow at a CAGR of 15% through 2030, there’s increasing demand for robust DC switching in battery management applications. Microgrid deployments—projected to exceed $40 billion in market value by 2027—are further stimulating demand for specialized isolation switches that can handle frequent on-off cycling. While traditional industrial applications remain important, the residential sector is emerging as a high-growth segment due to rising rooftop solar adoption and government incentives for clean energy solutions. Manufacturers are responding with products specifically designed for easier installation and maintenance by non-specialist users.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Innovation and Expansion to Capture Greater Market Share

The global DC isolator switch market features a moderately fragmented competitive landscape, with a mix of established multinational corporations and emerging regional players competing for market dominance. Eaton and Siemens currently hold leading positions, together accounting for approximately 28% of the global market share in 2024. Their dominance stems from extensive product portfolios, technological expertise in power distribution systems, and strong brand recognition in both industrial and commercial segments.

Schneider Electric has emerged as another key competitor, particularly in the European and Asian markets, owing to its strategic focus on renewable energy applications. The company’s recent introduction of smart isolator switches with remote monitoring capabilities has significantly strengthened its market position. Meanwhile, Beny Electric and VoltaconSolar are gaining traction as specialized providers of DC isolation solutions for solar PV systems, capitalizing on the rapid growth of renewable energy infrastructure.

Multinational giants are actively pursuing acquisition strategies to consolidate their market positions, while regional players compete through price competitiveness and customized product offerings. The market has recently witnessed several strategic partnerships between DC isolator switch manufacturers and solar panel producers, creating integrated solutions that simplify installation and improve system safety.

Japanese manufacturers including Mitsubishi Electric and Toshiba maintain strong positions in the high-end industrial segment, leveraging their expertise in precision engineering. These companies are investing heavily in R&D for next-generation isolator switches that can handle higher voltage DC applications, anticipating future market demands in grid-scale energy storage systems.

List of Key DC Isolator Switch Manufacturers

- Beny Electric (China)

- VoltaconSolar (UK)

- IMO Precision Controls (Germany)

- Eaton (Ireland)

- Siemens (Germany)

- Mitsubishi Electric (Japan)

- Dairyland Electrical (U.S.)

- Schneider Electric (France)

- Orient Electric (India)

- Toshiba (Japan)

- GIPRO GmbH (Germany)

- KINTO Electric (Japan)

Segment Analysis:

By Type

Double Break Isolator Gains Traction Due to Enhanced Safety and Reliability in High Voltage Applications

The market is segmented based on type into:

- Single Break Isolator

- Double Break Isolator

- Pantograph Isolator

- Others

By Application

Industrial Segment Holds Majority Share Owing to Widespread Use in Power Distribution Systems

The market is segmented based on application into:

- Industrial

- Commercial

- Residential

- Utility Scale Solar

By Voltage Rating

Medium Voltage Segment Leads with Increased Adoption in Commercial Power Systems

The market is segmented based on voltage rating into:

- Low Voltage (Below 1kV)

- Medium Voltage (1kV-36kV)

- High Voltage (Above 36kV)

By End User

Energy & Power Sector Dominates Due to Critical Switching Requirements in Power Stations

The market is segmented based on end user into:

- Energy & Power

- Railways

- Oil & Gas

- Renewable Energy

Regional Analysis: DC Isolator Switch Market

Asia-Pacific

The Asia-Pacific region dominates the global DC Isolator Switch market, accounting for over 40% of total revenue in 2024. This leadership position stems from robust renewable energy adoption and massive investments in solar power infrastructure, particularly in China and India. China’s National Energy Administration reports over 120 GW of new solar capacity additions in 2023 alone, creating substantial demand for safety components like DC isolators. While cost-sensitive markets continue using standard single-break isolators, industrial-scale solar projects are increasingly adopting advanced double-break models for enhanced safety. The region’s manufacturing prowess also makes it a global export hub, with Chinese producers supplying approximately 35% of worldwide DC isolators.

North America

North America represents the second-largest DC Isolator Switch market, driven by strict electrical safety standards (NEC Article 690) and rapid solar energy deployment. The U.S. market accounts for nearly 80% of regional demand, supported by tax credits under the Inflation Reduction Act which allocated $370 billion for clean energy. Commercial solar installations are particularly active, requiring high-performance isolators with UL certification. Canadian demand focuses on harsh-environment solutions for northern climates, creating opportunities for specialized manufacturers. However, supply chain disruptions and trade tariffs on Chinese components have pressured prices, leading some U.S. distributors to seek alternative suppliers.

Europe

Europe’s market is characterized by sophisticated regulatory requirements (IEC 60947-3) and emphasis on product certifications. Germany and the UK lead adoption, with the former mandating Type-2 isolators for all photovoltaic systems above 30kW. The EU’s REPowerEU plan, targeting 320GW of solar capacity by 2025, is accelerating demand. Manufacturers are responding with smart isolators featuring remote monitoring capabilities, though higher costs limit penetration in Eastern European markets. Scandinavian countries show unique demand for arctic-grade isolators capable of operating in extreme cold, presenting niche opportunities for specialized providers.

South America

South America exhibits growing potential, particularly in Brazil and Chile where utility-scale solar projects are expanding. Brazil’s energy regulator ANEEL reports 15GW of installed solar capacity as of 2024, with distributed generation growing at 40% annually. However, price sensitivity remains pronounced, favoring basic single-break isolator models. Economic instability in Argentina and Venezuela continues to hinder market development, though some multinational suppliers maintain limited operations through local partnerships. The region’s lack of uniform safety standards also creates challenges for manufacturers seeking to implement standardized product lines.

Middle East & Africa

This emerging market is characterized by divergent development patterns. Gulf Cooperation Council countries, particularly UAE and Saudi Arabia, are driving demand through mega-projects like the 2GW Al Dhafra solar plant. These markets prefer premium, durable isolators capable of withstanding desert conditions. Sub-Saharan Africa shows potential but faces infrastructure limitations, with off-grid solar applications often using cost-effective imported Chinese isolators. South Africa remains the most developed market, though political and economic uncertainties have slowed recent growth. Across the region, the absence of localized manufacturing means nearly 90% of DC isolators are imported.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional DC Isolator Switch markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global DC Isolator Switch market was valued at US$ 1.47 billion in 2024 and is projected to reach US$ 2.69 billion by 2032, growing at a CAGR of 7.8%.

- Segmentation Analysis: Detailed breakdown by product type (Single Break Isolator, Double Break Isolator), application (Industrial, Commercial, Residential), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. market size is estimated at USD million in 2024, while China is projected to reach USD million.

- Competitive Landscape: Profiles of leading market participants including Beny Electric, VoltaconSolar, Eaton, Siemens, Mitsubishi Electric, Schneider Electric, and Toshiba, covering their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in DC isolation, integration with renewable energy systems, and evolving safety standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as renewable energy adoption, along with challenges including supply chain constraints and regulatory compliance.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving DC power ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global DC Isolator Switch Market?

-> DC Isolator Switch Market size was valued at US$ 1.47 billion in 2024 and is projected to reach US$ 2.69 billion by 2032, at a CAGR of 7.8% during the forecast period 2025-2032.

Which key companies operate in Global DC Isolator Switch Market?

-> Key players include Beny Electric, VoltaconSolar, Eaton, Siemens, Mitsubishi Electric, Schneider Electric, and Toshiba, among others.

What are the key growth drivers?

-> Key growth drivers include increasing adoption of renewable energy systems, safety regulations, and expansion of solar power infrastructure.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a significant market.

What are the emerging trends?

-> Emerging trends include smart isolator switches, integration with IoT monitoring systems, and higher voltage capacity developments.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...