Data Center Processor Market Insights

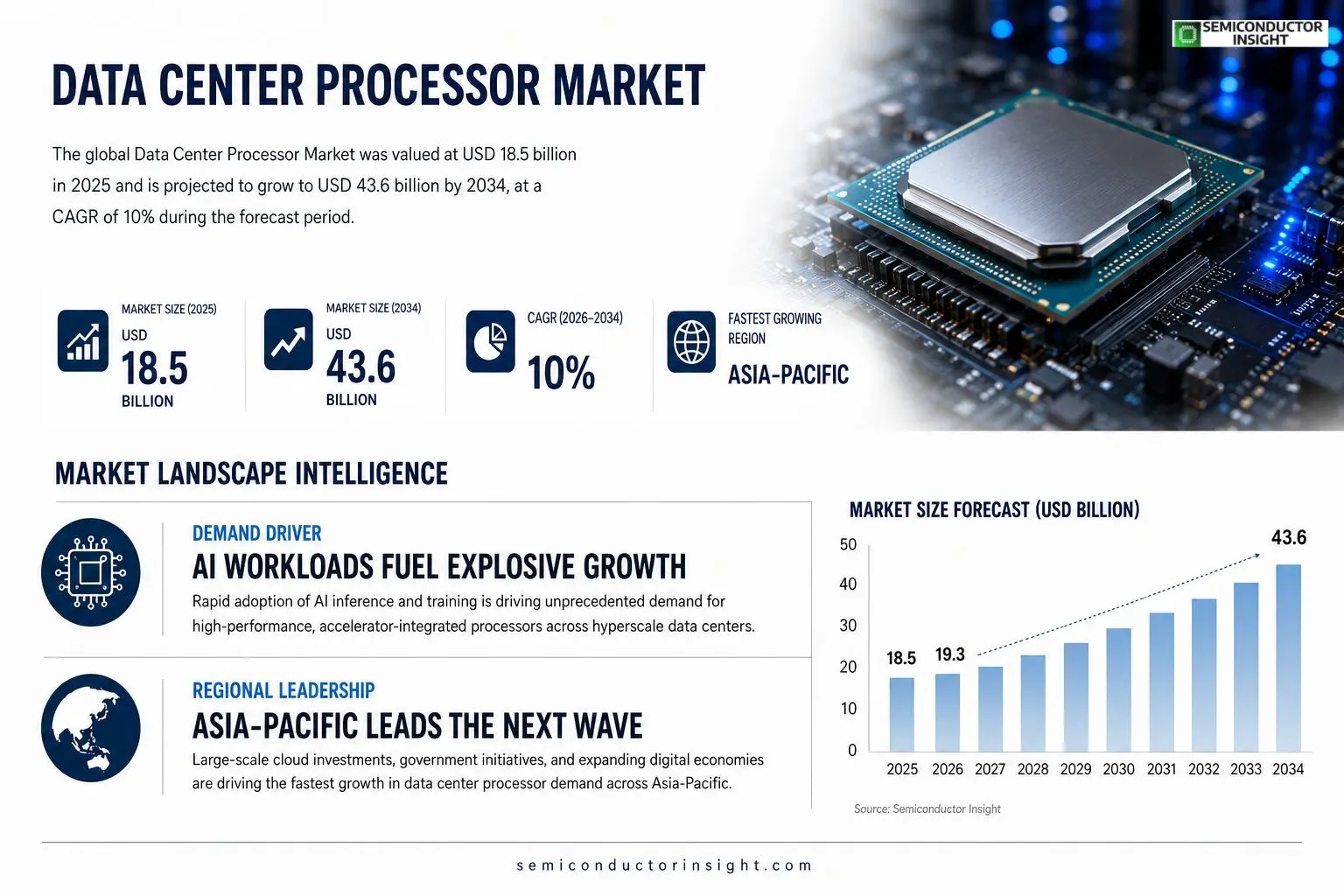

Data Center Processor Market size was valued at USD 18.5 billion in 2025. The market is projected to grow from USD 19.3 billion in 2026 to USD 43.6 billion by 2034, exhibiting a CAGR of 10% during the forecast period.

Data center processors are high‑performance computing units,including CPUs, GPUs, and specialized ASICs,designed to handle massive workloads such as cloud services, artificial‑intelligence inference, and large‑scale virtualization. These chips deliver high core counts, advanced memory bandwidth, and energy‑efficient architectures that enable hyperscale data centers to meet latency‑critical demands while optimizing power consumption.The market is accelerating because enterprises are rapidly expanding cloud infrastructure and AI workloads are driving demand for more capable silicon. Furthermore, hyperscale operators are investing heavily in next‑generation architectures that integrate accelerators directly onto server boards. However, supply‑chain constraints and rising semiconductor costs pose challenges. Recent developments include Nvidia’s Grace CPU‑GPU superchip launch in March 2024, Intel’s Sapphire Rapids Xeon rollout Q2‑2024, AMD’s Genoa EPYC series release late 2023, and Arm’s partnership with AWS for custom data‑center cores announced early 2024. Key players such as Intel Corp., Advanced Micro Devices Inc., Nvidia Corp., and Arm Holdings continue to expand their portfolios through innovation and strategic collaborations.

MARKET DRIVERS

Growing Demand for AI‑Optimized Compute

Data Center Processor Market is being propelled by an unprecedented surge in AI workloads, where hyperscale operators require processors that can handle massive parallel inference and training tasks. Enterprises are migrating legacy applications to AI‑enabled platforms, creating a clear upward trend in processor orders.

Energy Efficiency and Consolidation

Data center operators are consolidating workloads onto fewer, more power‑efficient chips to cut OPEX. Modern silicon delivers up to 30% better performance per watt, directly influencing capacity planning and driving higher adoption rates across cloud providers.

➤ “Edge‑driven AI workloads are reshaping processor architectures, making low‑latency designs a top priority for Data Center Processor Market.”

In addition, the rollout of 5G and the rise of real‑time analytics are expanding the need for high‑throughput processors, reinforcing growth momentum for the sector.

MARKET CHALLENGES

Supply Chain Disruptions

semiconductor shortages have introduced lead‑time extensions of up to 24 weeks for critical CPU and GPU dies. This bottleneck constrains the ability of data center owners to scale infrastructure in line with demand forecasts.

Other Challenges

Regulatory & Compliance Pressures

Increasing data‑sovereignty laws require processors to embed encryption and audit capabilities, adding design complexity and lengthening development cycles.Geopolitical tensions also affect cross‑border component sourcing, requiring vendors to diversify manufacturing footprints, which can increase costs and delay new product introductions.

MARKET RESTRAINTS

High Capital Expenditure

Deploying next‑generation processors often requires substantial upfront investment in cooling, power, and rack infrastructure. Many mid‑size data centers face budgetary constraints that delay migration to newer, higher‑density silicon solutions.Furthermore, legacy compatibility concerns force operators to retain older hardware generations, compressing total addressable market growth for cutting‑edge processor offerings.

MARKET OPPORTUNITIES

Rise of ARM‑Based Solutions

ARM architectures are gaining traction as they deliver superior scalability for cloud-native workloads while maintaining lower power envelopes. Vendors that successfully integrate ARM cores into server platforms can capture a sizable share of the expanding market.Additionally, the growing emphasis on edge computing opens avenues for low‑power, high‑density processors that can be deployed in micro‑data centers, extending the reach of traditional data center ecosystems.Strategic partnerships between silicon manufacturers and hyperscale cloud providers are expected to accelerate innovation cycles, creating a pipeline of differentiated products that address emerging AI and analytics requirements.

Data Center Processor Market Trends

Accelerating Cloud and AI Demand

Data Center Processor Market is being reshaped by the rapid expansion of cloud services and the surge in artificial‑intelligence inference workloads. Enterprises are scaling out hyperscale infrastructure to support latency‑critical applications, which drives the adoption of processors with higher core counts, expanded memory bandwidth, and energy‑efficient designs. Recent product introductions such as Nvidia’s Grace superchip and Intel’s Sapphire Rapids Xeon series illustrate how vendors are delivering integrated CPU‑GPU solutions that reduce data movement and improve performance per watt. This trend is reinforcing the shift toward heterogeneous compute platforms that can handle mixed workloads more effectively, positioning the market for sustained growth through 2034.

Other Trends

Supply Chain and Cost Pressures

Despite strong demand, Data Center Processor Market faces notable supply‑chain constraints that affect component availability and pricing. semiconductor shortages, combined with rising material costs, have pressured manufacturers to prioritize high‑margin segments, occasionally limiting the supply of mid‑range silicon. Operators are responding by diversifying their supplier base and extending procurement contracts, but the underlying volatility remains a risk factor for short‑term capacity planning.

Architectural Innovation and Integration

Innovation in processor architecture is another critical driver for Data Center Processor Market. ARM’s partnership with AWS to create custom data‑center cores and AMD’s Genoa EPYC series exemplify a movement toward tightly integrated accelerators and specialized ASICs on server boards. These designs aim to reduce latency, improve power efficiency, and simplify system‑level integration, enabling data‑center operators to achieve higher utilization rates. As major players continue to expand their portfolios through strategic collaborations, the competitive landscape is becoming increasingly dynamic, encouraging faster cycles of technology adoption across the industry.

COMPETITIVE LANDSCAPEKey Industry Players

Data Center Processor Market Overview

Data Center Processor Market is dominated by a few tier‑1 silicon vendors that shape architecture roadmaps for hyperscale operators. Intel remains the largest supplier of server‑class CPUs, leveraging its Xeon Sapphire Rapids platform to deliver high core counts and advanced memory bandwidth. AMD has rapidly closed the performance gap with its Genoa EPYC family, emphasizing energy efficiency and heterogeneous integration. Nvidia, traditionally a GPU specialist, expanded into the CPU space with the Grace CPU‑GPU superchip, positioning itself as a one‑stop solution for AI‑intensive workloads. Arm’s recent partnership with AWS to develop custom data‑center cores reflects a growing trend toward instruction‑set diversification, and its licensing model enables a broad ecosystem of secondary vendors. Collectively, these leaders create a competitive landscape where performance per watt, integration of accelerators, and roadmap clarity are primary differentiators.Beyond the dominant four, several niche and emerging players add depth to the market. Amazon Web Services designs its own Graviton processors to optimize cost and performance for its cloud services. Qualcomm is extending its Snapdragon compute platform to server workloads, targeting edge‑to‑cloud continuity. Google’s Tensor Processing Units (TPUs) and IBM’s Power9/Power10 CPUs serve specialized AI and enterprise segments. Marvell, Samsung, and MediaTek contribute ASIC and SoC expertise for networking‑centric workloads, while Taiwan Semiconductor Manufacturing Company (TSMC) underpins the supply chain for many of these designs. The presence of these diverse players intensifies innovation pressure and widens the choice set for data‑center operators seeking tailored silicon solutions.

List of Key Data Center Processor Companies Profiled

- Intel Corporation

- Advanced Micro Devices (AMD)

- Nvidia Corporation

- Arm Holdings

- Amazon Web Services (AWS)

- Qualcomm Inc.

- Google LLC

- IBM

- Marvell Technology Group Ltd.

- Samsung Electronics

- MediaTek Inc.

- Taiwan Semiconductor Manufacturing Company (TSMC)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

CPU continues to dominate the data‑center processor landscape because of its versatility and mature software ecosystem.

|

| By Application |

|

GPU/Accelerator is the leading segment for AI‑driven workloads, shaping the roadmap of next‑generation data‑centers.

|

| By End User |

|

Cloud Service Providers drive the majority of procurement activity, seeking scale, efficiency and rapid innovation.

|

| By Architecture |

|

ARM‑based processors are gaining momentum as efficiency and custom‑instruction sets align with AI workloads.

|

| By Performance Tier |

|

High‑Performance segment is pivotal for workloads that require intensive parallelism and low latency.

|

Regional Analysis: North America

United States

The US market is at the forefront of innovation in server technologies, with continuous development of new architectures and processor designs to meet the escalating demands of data centers.

Significant investments in cloud infrastructure across the US are driving the need for powerful and efficient data center processors to support cloud services and applications.

Data security and reliability are paramount concerns in the US market, influencing the selection of processors with enhanced security features and robust performance capabilities.

Growing emphasis on energy efficiency is pushing the adoption of low-power processors and optimized data center designs in the US region.

Europe

Europe represents a significant and steadily growing market for Data Center Processor Market. The region is characterized by stringent data privacy regulations and a strong focus on sustainability, influencing processor choices and data center design. While adoption rates may be slightly slower compared to the US, the European market is witnessing substantial investments in cloud computing and high-performance computing (HPC), thereby creating considerable demand for advanced processor technologies. The emphasis on energy efficiency and power consumption further shapes the processor landscape, with a growing preference for processors that minimize environmental impact. The European Union’s initiatives promoting digital transformation and data sovereignty are also contributing to the expansion of Data Center Processor Market within the region.

Asia-Pacific

The Asia-Pacific region is emerging as the fastest-growing market for Data Center Processor Market. Driven by rapid digital transformation, increasing cloud adoption, and expanding data generation, the region presents substantial opportunities for processor vendors. Countries like China, India, and Japan are witnessing significant investments in data center infrastructure, fueling demand for high-performance and energy-efficient processors. The growth of artificial intelligence (AI) and machine learning (ML) applications in the region is also contributing to the increasing need for specialized processors. However, variations in regulatory landscapes and infrastructure development across different countries within the Asia-Pacific region present unique challenges and opportunities for market players.

South America

South America’s Data Center Processor Market is in an early stage of development but holds significant growth potential. The increasing adoption of cloud services, e-commerce, and digital entertainment is driving demand for data center infrastructure and, consequently, for processors. While the market is currently smaller compared to North America and Asia-Pacific, the region’s growing digital economy and expanding internet penetration suggest a promising future for Data Center Processor Market. The focus on cost-effectiveness and scalability is particularly relevant in the South American market, influencing processor selection and deployment strategies.

Middle East & Africa

The Middle East & Africa region represents a nascent yet promising market for Data Center Processor Market. Investments in data center infrastructure are increasing across several countries, driven by growing digital economies, government initiatives promoting technological advancement, and the expansion of cloud services. The region’s unique challenges, such as limited infrastructure in some areas and varying levels of digital literacy, present both hurdles and opportunities for market growth. The demand for processors capable of handling diverse workloads, including those related to oil and gas, financial services, and government operations, is expected to drive future market expansion in Data Center Processor Market.

Report Scope

This market research report provides a comprehensive analysis of the Data Center Processor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: ✅ The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- ✅ Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- ✅ Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- ✅ Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- ✅ Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- ✅ Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- ✅ Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- ✅ Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Data Center Processor Market?

-> Data Center Processor Market was valued at USD 18.5 billion in 2025 and is expected to reach USD 43.6 billion by 2034, exhibiting a CAGR of 10% during the forecast period.

Which key companies operate in Data Center Processor Market?

-> Key players include Intel Corp., Advanced Micro Devices Inc., Nvidia Corp., and Arm Holdings.

What are the key growth drivers?

-> Key growth drivers include rapid expansion of cloud infrastructure, increasing AI workloads, and hyperscale operators investing in next‑generation architectures integrating accelerators.

Which region dominates the market?

-> Demand is strong across North America, Europe, and Asia‑Pacific, with Asia‑Pacific showing the fastest growth due to large hyperscale data‑center deployments.

What are the emerging trends?

-> Emerging trends include integration of CPU‑GPU accelerators, custom silicon designs for AI inference, and collaborations such as Arm’s partnership with AWS for bespoke data‑center cores.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...