Data Center AI Chip Market Insights

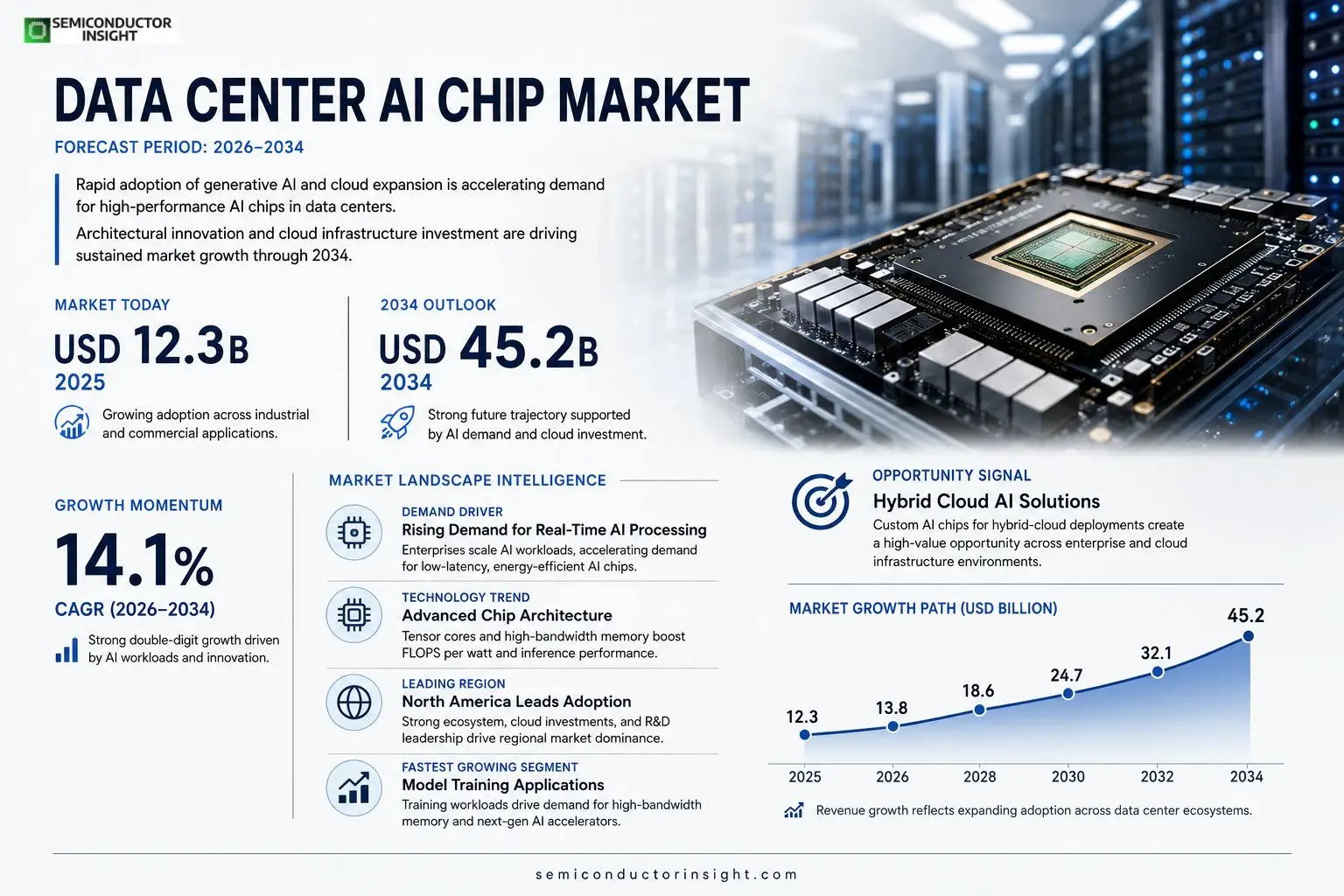

Data Center AI Chip Market size was valued at USD 12.3 billion in 2025. The market is projected to grow from USD 13.8 billion in 2026 to USD 45.2 billion by 2034, exhibiting a CAGR of approximately 14.1% during the forecast period.

Data center AI chips are specialized processors engineered to accelerate machine‑learning workloads, inference, and training within high‑density server environments. These chips integrate tensor cores, high‑bandwidth memory interfaces, and optimized interconnects to deliver superior performance‑per‑watt compared with traditional CPUs or GPUs.The market is experiencing rapid growth because hyperscale cloud providers are expanding capacity, enterprises are adopting generative‑AI services, and edge‑to‑cloud architectures demand low‑latency inference. However, supply‑chain constraints for advanced semiconductors pose challenges, while continued R&D investments from leading vendors such as NVIDIA, AMD, Intel, and emerging ASIC designers are expected to sustain momentum.

MARKET DRIVERS

Rising Demand for Real‑Time AI Processing

Enterprises are scaling up AI workloads such as generative models and computer‑vision services, prompting data‑center operators to seek processors that can deliver sub‑second inference. This surge directly fuels growth in Data Center AI Chip Market, as operators prioritize chips that reduce latency while maintaining energy efficiency.

Advancements in Chip Architecture

Recent architectural breakthroughs, including heterogeneous integration of tensor cores and on‑die high‑bandwidth memory, enable higher FLOPS per watt. Companies that adopt these designs gain a competitive edge, driving broader adoption across hyperscale cloud providers.

➤ Integration of high‑bandwidth memory accelerates AI inference, shrinking model execution time by up to 30 % without additional power draw.

Overall, the convergence of workload intensity and architectural innovation creates a robust foundation for sustained expansion of Data Center AI Chip Market.

MARKET CHALLENGES

Thermal Management Constraints

AI chips generate concentrated heat zones that exceed traditional cooling capacities. Data‑center facilities must invest in advanced liquid‑cooling or immersion‑cooling solutions, raising operational complexity and cost.

Other Challenges

Supply Chain Volatility

semiconductor shortages, amplified by geopolitical tensions, limit the availability of advanced nodes. This disrupts production schedules and can delay deployments of next‑generation AI accelerators.

MARKET RESTRAINTS

High Capital Expenditure

Designing and manufacturing cutting‑edge AI chips requires multi‑billion‑dollar investments in fab capacity, R&D, and validation equipment. For many data‑center operators, the upfront spend creates a financial barrier that can slow adoption despite clear performance benefits.

MARKET OPPORTUNITIES

Emergence of Hybrid Cloud AI Solutions

Enterprises are increasingly adopting hybrid‑cloud models that blend on‑premise data‑center resources with public‑cloud AI services. This trend opens a niche for customizable AI chips that can be tightly integrated with private infrastructure while maintaining compatibility with major cloud providers, presenting a sizable growth avenue for Data Center AI Chip Market.

Data Center AI Chip Market Trends

Accelerated Adoption of Specialized AI Processors

Data Center AI Chip Market is being reshaped by processors that are purpose‑built for machine‑learning workloads. These chips embed tensor cores, high‑bandwidth memory, and optimized interconnects, delivering a markedly higher performance‑per‑watt ratio than traditional CPUs or GPUs. Hyperscale cloud operators are expanding server capacity to support generative‑AI services, while enterprises are integrating AI inference into core business applications. The convergence of these forces creates a sustained demand premium for chips that can handle intensive training and low‑latency inference within dense rack environments.

Other Trends

Supply‑Chain Constraints and Vendor Competition

Advanced semiconductor fabrication remains a bottleneck, limiting the speed at which new AI‑focused designs can reach volume production. Leading vendors,including NVIDIA, AMD, Intel, and emerging ASIC developers,are intensifying R&D spend to secure architectural advantages, yet the finite number of leading‑edge fabs imposes a hard ceiling on short‑term supply. This dynamic translates into longer order‑to‑delivery cycles and prompts data‑center operators to diversify their chip portfolios, balancing performance needs with availability risks.

Emerging Edge‑to‑Cloud AI Chip Deployments

Beyond the core of massive data centers, the market is extending toward edge‑to‑cloud topologies that require localized inference capabilities. Low‑latency demands of real‑time analytics and autonomous systems are driving the placement of compact AI chips at the network edge, while still maintaining seamless integration with central cloud resources. This hybrid approach fosters a new layer of demand for chips that combine power efficiency with the ability to operate in constrained environments, signaling a broadened scope for Data Center AI Chip Market as it supports both centralized and distributed compute models.

COMPETITIVE LANDSCAPEKey Industry Players

Data Center AI Chip Market Competitive Overview

Data Center AI Chip Market is dominated by a handful of vertically integrated vendors that combine advanced semiconductor design, large‑scale manufacturing, and extensive cloud platform ecosystems. NVIDIA leads the segment with its Hopper‑based GPUs, which deliver industry‑leading tensor‑core density and software stack integration through CUDA and the NVIDIA AI Enterprise suite. Intel follows closely, leveraging its Xeon processor line while expanding its Habana Labs ASIC portfolio to address inference workloads at scale. AMD has accelerated its presence with the MI300 series, offering high‑bandwidth memory and competitive price‑performance ratios that attract hyperscale operators seeking alternatives to NVIDIA. Additionally, Google’s Tensor Processing Units (TPUs) continue to secure a sizable share of internal cloud workloads, thanks to custom ASIC design optimized for matrix multiplication and low‑latency inference. These leaders benefit from deep R&D pipelines, strategic cloud partnerships, and the ability to secure advanced process nodes, positioning them as the primary drivers of market growth through 2034.Beyond the dominant tier, a diverse set of niche innovators is reshaping specialized segments of the Data Center AI Chip ecosystem. Graphcore’s intelligence‑processing units focus on graph‑centric workloads, while Cerebras Systems differentiates with its wafer‑scale engine that consolidates billions of transistors into a single chip to eliminate inter‑die latency. Emerging players such as Tenstorrent and Habana Labs (now part of Intel) target high‑throughput training and inference with energy‑efficient architectures. Samsung Electronics, Fujitsu, and Qualcomm are investing in AI‑optimized ASICs for edge‑to‑cloud integration, and cloud‑native vendors like Amazon Web Services (Inferentia) and Microsoft (Project Brainwave) deliver custom silicon tightly coupled with their service stacks. This breadth of specialization enhances overall market resilience and drives continued innovation across the AI data‑center value chain.

List of Key Data Center AI Chip Companies Profiled

- NVIDIA

- Intel

- AMD

- Google (TPU)

- Amazon Web Services (Inferentia)

- Microsoft (Project Brainwave)

- Graphcore

- Cerebras Systems

- Habana Labs

- Tenstorrent

- Samsung Electronics

- Alibaba Cloud (DAMO Academy)

- Qualcomm (AI Engine)

- IBM (Power AI)

- Fujitsu (A64FX)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

GPU‑based AI chips are perceived as the leading type because:

|

| By Application |

|

Model Training commands the primary focus because:

|

| By End User |

|

Cloud Service Providers dominate adoption because:

|

| By Architecture |

|

Tensor Processing Units are the favored architecture because:

|

| By Deployment Scale |

|

Hyperscale Data Centers lead deployment because:

|

Regional Analysis: North America

North America

The United States continues to lead in AI chip development and deployment. Significant government initiatives and private sector investments are fueling innovation in this sector, particularly in areas like cloud computing and edge AI. The strong presence of major technology companies and research centers makes the US a key driver of Data Center AI Chip Market.

Canada is emerging as a significant player in Data Center AI Chip Market, leveraging its strong research capabilities and government support for technology innovation. The country’s focus on sustainable data centers aligns well with the energy efficiency demands of advanced AI chips.

Mexico is witnessing growing interest in Data Center AI Chip Market, driven by its strategic location and increasing adoption of cloud services. The region’s cost-effectiveness and proximity to the US are attracting investments in data center infrastructure, creating demand for AI chip solutions.

Guatemala presents a developing market for Data Center AI Chips, primarily supporting regional data center growth and cloud adoption. While smaller than other North American nations, it represents a potential area for future expansion and investment.

Europe

Europe is experiencing substantial expansion in Data Center AI Chip Market, propelled by the increasing adoption of AI across various industries, including automotive, healthcare, and finance. The region’s emphasis on data sovereignty and security is influencing the development and deployment of AI chip solutions tailored to specific European needs. Several countries are actively investing in AI research and development to enhance their competitiveness in this rapidly evolving market.

Asia-Pacific

Asia-Pacific is a dynamic and rapidly growing market for Data Center AI Chip Market. Countries like China, Japan, and South Korea are leading the way in AI adoption, driving demand for high-performance computing resources. The region’s robust manufacturing capabilities and large data center build-out are contributing to the expansion of the AI chip market.

South America

South America represents an emerging market for Data Center AI Chips, with increasing data center investments and growing demand for AI-powered solutions. The region’s diverse economies and expanding digital infrastructure are creating opportunities for growth in this sector.

Middle East & Africa

The Middle East & Africa is witnessing a gradual but steady growth in Data Center AI Chip Market, driven by investments in cloud computing and digital transformation initiatives. The region’s expanding data center footprint and increasing adoption of AI-powered applications are fueling demand for specialized AI chip solutions.

Report Scope

This market research report provides a comprehensive analysis of the Data Center AI Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Data Center AI Chip Market?

-> Data Center AI Chip Market was valued at USD 12.3 billion in 2025 and is expected to reach USD 45.2 billion by 2034, reflecting strong growth potential.

Which key companies operate in Data Center AI Chip Market?

-> Key players include NVIDIA, AMD, Intel, and emerging ASIC designers, among others.

What are the key growth drivers?

-> Key growth drivers include expansion by hyperscale cloud providers, adoption of generative‑AI services by enterprises, and demand for low‑latency inference in edge‑to‑cloud architectures.

Which region dominates the market?

-> The reference does not specify a single dominant region; growth is observed ly, with significant activity in North America and Asia‑Pacific.

What are the emerging trends?

-> Emerging trends include increased R&D investments from leading vendors, development of specialized ASICs, and supply‑chain strategies to mitigate semiconductor shortages.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...