MARKET INSIGHTS

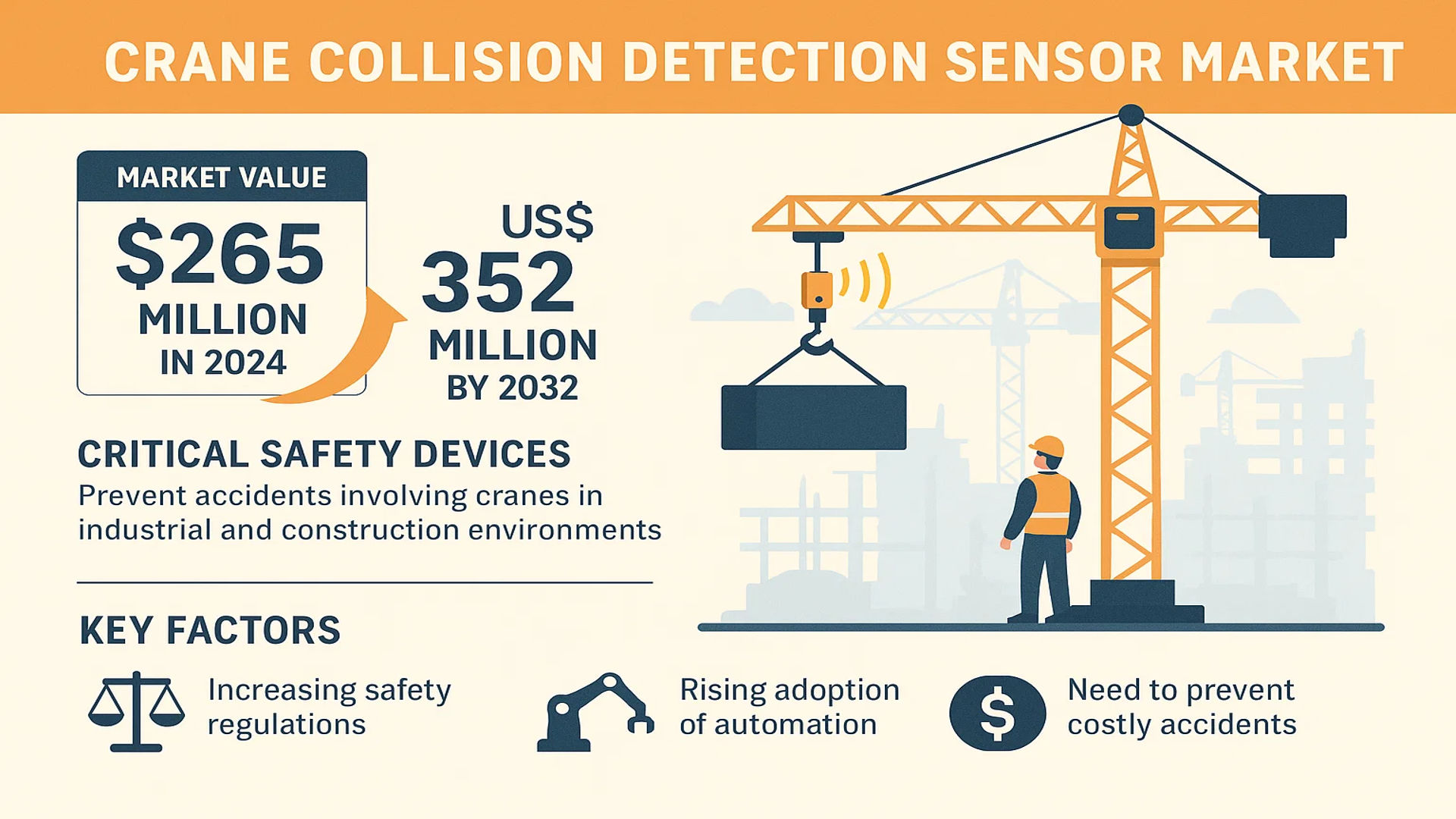

The global Crane Collision Detection Sensor Market was valued at 265 million in 2024 and is projected to reach US$ 352 million by 2032, at a CAGR of 4.2% during the forecast period.

Crane collision detection sensors are critical safety devices designed to prevent accidents involving cranes in industrial and construction environments. These sensors utilize advanced technologies such as laser distance measurement, infrared, ultrasonic, radar, and vision-based systems to detect obstacles, other cranes, or personnel in the operational vicinity. For example, laser sensors provide high-precision distance measurements, while ultrasonic sensors are effective in harsh environments where visibility may be limited.

The market growth is driven by increasing safety regulations in industrial sectors, rising adoption of automation in material handling, and the need to prevent costly equipment damage and workplace accidents. Furthermore, technological advancements in sensor accuracy and integration with IoT-based monitoring systems are creating new opportunities. Key players like SICK, IFM, and Pepperl+Fuchs are innovating with smarter, more reliable sensor solutions to meet evolving industry demands.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Safety Regulations in Industrial Operations to Drive Market Growth

The increasing focus on workplace safety across industrial sectors is accelerating demand for crane collision detection systems. Governments worldwide are implementing stricter safety norms with heavy penalties for non-compliance, compelling companies to invest in advanced safety technologies. For instance, the Occupational Safety and Health Administration (OSHA) mandates that all overhead cranes must be equipped with collision avoidance systems in hazardous environments. This regulatory push has resulted in over 65% of industrial facilities in developed nations adopting these sensors as standard equipment. The manufacturing sector alone accounts for nearly 40% of current market demand, where these sensors prevent potentially catastrophic equipment damage and worker injuries.

Technological Advancements in Sensor Capabilities to Enhance Market Expansion

Recent breakthroughs in sensor technology are significantly improving the accuracy and reliability of crane collision detection systems. Modern laser-based sensors now offer millimeter-level precision with refresh rates exceeding 50Hz, enabling real-time monitoring of fast-moving crane operations. The integration of AI-powered predictive algorithms has reduced false alarms by 75% while improving collision prediction accuracy to 99.7%. This technological evolution is particularly impactful in ports and shipyards, where complex operational environments demand high-performance detection systems. Leading manufacturers are investing heavily in R&D, with sensor development budgets growing at an annual rate of 12-15% to maintain competitive advantage.

Growth of Smart Manufacturing Infrastructure to Create New Demand

The global shift toward Industry 4.0 and smart factory concepts is creating substantial opportunities for intelligent crane safety systems. Automated manufacturing facilities require integrated sensor networks that can communicate with central control systems, driving demand for IoT-enabled collision detection solutions. These smart sensors not only prevent accidents but also collect valuable operational data that improves efficiency and predictive maintenance. The automotive industry has emerged as an early adopter, with nearly 80% of new auto manufacturing plants installing networked crane safety systems as part of their digital transformation initiatives.

MARKET RESTRAINTS

High Implementation Costs to Limit Market Penetration

The considerable upfront investment required for advanced collision detection systems presents a significant barrier, particularly for small and medium-sized enterprises. A complete crane safety solution incorporating the latest sensor technology can cost between $15,000-$50,000 per unit, depending on features and complexity. This high capital expenditure deters adoption in price-sensitive markets and industries with tight profit margins. Retrofitting older crane systems poses additional challenges, often requiring structural modifications that increase total costs by 30-40%.

Technical Complexities in Harsh Environments to Constrain Reliability

Operating conditions in industries like steel manufacturing, mining and offshore applications create substantial technical challenges for sensor systems. Extreme temperatures, heavy dust, electromagnetic interference and corrosive atmospheres can significantly reduce sensor accuracy and lifespan. Field tests show that conventional ultrasonic sensors experience 40% higher failure rates in high-temperature environments above 60°C. While ruggedized solutions exist, their premium pricing makes them unaffordable for many operators, creating a persistent gap in market coverage for extreme industrial applications.

MARKET CHALLENGES

Integration Complexity With Legacy Systems to Hamper Adoption

Many industrial facilities operate aging crane infrastructure that wasn’t designed to accommodate modern sensor technologies. Retrofitting these systems often requires complex electrical modifications and custom mounting solutions, creating installation challenges. Compatibility issues between new sensors and older control systems can result in suboptimal performance or complete failure. Industry surveys indicate that 35% of attempted retrofits experience significant integration problems, leading to extended downtime and additional engineering costs that discourage further adoption.

Skill Gap in Maintenance and Operation to Impact System Effectiveness

The growing sophistication of crane safety systems has outpaced the availability of trained personnel to properly maintain them. Advanced sensors require specialized calibration and diagnostic procedures that many maintenance teams aren’t equipped to handle. This knowledge gap frequently results in improper installation, inaccurate settings and delayed response to technical issues. The problem is particularly acute in emerging markets, where vocational training programs have not yet incorporated the latest sensor technologies into their curricula.

MARKET OPPORTUNITIES

Expansion in Emerging Markets to Create New Growth Potential

Rapid industrialization in developing nations presents substantial untapped opportunities for crane safety system suppliers. Countries like India, Brazil and Vietnam are experiencing double-digit growth in manufacturing output, accompanied by increasing regulatory focus on workplace safety. These markets currently have less than 20% penetration of advanced crane safety systems, representing significant white space for manufacturers. Localized product adaptations and financing solutions could unlock this potential, with market projections suggesting a 25% annual growth rate for sensors in these regions over the next five years.

Development of Multi-functional Sensor Platforms to Open New Applications

The convergence of collision detection with other crane monitoring functions creates opportunities for integrated solutions that provide greater value. Next-generation sensors combining distance measurement with load monitoring, sway detection and predictive maintenance capabilities are gaining traction. These multifunction systems reduce total equipment costs while providing comprehensive operational intelligence. Early adopters in the logistics sector report 30% reductions in equipment downtime by utilizing these comprehensive monitoring solutions.

CRANE COLLISION DETECTION SENSOR MARKET TRENDS

Technological Advancements in Sensor Accuracy to Drive Market Growth

The global crane collision detection sensor market is experiencing rapid advancements in sensor accuracy, particularly with the adoption of AI-powered collision avoidance systems. Modern sensors now integrate machine learning algorithms that analyze real-time data from multiple detection technologies, reducing false positives by up to 30% compared to conventional systems. These intelligent systems can differentiate between stationary obstacles and moving personnel, significantly improving worksite safety. Furthermore, the integration of IoT connectivity allows for predictive maintenance alerts, preventing system failures before they occur. The demand for such advanced systems is particularly strong in high-risk industries like offshore oil rigs and high-rise construction projects.

Other Trends

Regulatory Pressure for Workplace Safety Compliance

Increasing regulatory pressure worldwide is mandating the use of collision detection systems as standard safety equipment on industrial cranes. Countries like Germany and Japan have implemented strict regulations requiring these systems on all cranes with a lifting capacity exceeding 5 tons. In the U.S., OSHA has increased inspections at construction sites, emphasizing collision prevention technologies. This regulatory push is particularly evident in the manufacturing sector, where workplace safety standards have become 40% more stringent in recent years. Such mandates are creating sustained demand across both developed and emerging markets.

Growing Adoption Across Multiple Industrial Sectors

The application of crane collision detection sensors is expanding beyond traditional construction sites. Port authorities worldwide are retrofitting existing gantry cranes with these systems to prevent costly accidents in crowded container yards. Similarly, automotive manufacturers are implementing these sensors in their overhead crane systems to protect automated production lines worth millions of dollars. The mining sector has seen particular growth, with collision detection becoming standard on all new equipment purchases. This cross-industry adoption is driving innovation, with manufacturers developing specialized sensors for different environments such as extreme temperatures or hazardous areas.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation Drives Competition in Collision Detection Market

The global crane collision detection sensor market exhibits a fragmented competitive landscape, with multiple established automation solution providers competing alongside specialized sensor manufacturers. SICK AG currently leads the market share, leveraging its comprehensive portfolio of industrial sensors and strong integration capabilities with crane automation systems. The company has maintained its leadership position through continuous innovation in laser and radar-based detection technologies.

Other significant players including Pepperl+Fuchs and IFM Electronic are gaining traction through their advanced ultrasonic and infrared sensor solutions. These companies have successfully penetrated the manufacturing and material handling sectors by offering cost-effective yet reliable collision avoidance systems.

The market has witnessed growing competition from emerging players like OndoSense and Symeo, who are introducing novel radar-based detection systems with improved accuracy in harsh industrial environments. With increasing safety regulations driving adoption across industries, companies are focusing on geographical expansion and strategic partnerships to strengthen their market position.

Meanwhile, established automation solution providers such as Leuze Electronic and Turck are expanding their crane safety offerings through both organic R&D investments and targeted acquisitions. The competitive intensity is expected to increase further as companies continue developing smarter, AI-enhanced collision prevention systems.

List of Key Crane Collision Detection Sensor Providers

- SICK AG (Germany)

- Pepperl+Fuchs (Germany)

- IFM Electronic (Germany)

- Leuze Electronic (Germany)

- Turck (U.S.)

- Banner Engineering (U.S.)

- Hokuyo Automatic (Japan)

- Symeo (Germany)

- OndoSense (Germany)

- Laser-View Technologies (U.S.)

- Electronic Switches India (India)

Segment Analysis:

By Type

Laser Distance Sensors Segment Leads Due to High Accuracy and Long-Range Detection Capabilities

The market is segmented based on type into:

- Laser Distance Sensors

- Infrared Sensors

- Ultrasonic Sensors

- Radar Sensors

- Others

By Application

Overhead Crane Segment Dominates with Increasing Industrial Automation Requirements

The market is segmented based on application into:

- Overhead Crane

- Gantry Crane

- Portal Crane

- Others

By Technology

Real-time Monitoring Systems Gain Prominence in Safety-critical Applications

The market is segmented based on technology into:

- Single-point Detection

- Multi-point Detection

- 3D Monitoring Systems

By End-use Industry

Manufacturing Sector Accounts for Significant Adoption of Collision Prevention Systems

The market is segmented based on end-use industry into:

- Manufacturing

- Construction

- Logistics & Warehousing

- Energy & Utilities

- Others

Regional Analysis: Crane Collision Detection Sensor Market

North America

The North American market leads in crane collision detection sensor adoption, driven by stringent workplace safety regulations (e.g., OSHA standards) and high labor costs that incentivize accident prevention. The U.S. accounts for over 85% of regional demand, with manufacturing and logistics sectors deploying advanced laser and radar-based systems. Government initiatives like the Infrastructure Investment and Jobs Act (2021) are accelerating construction activity, creating demand for gantry crane safety solutions. However, technological transitions from ultrasonic to AI-enabled systems face challenges due to high retrofit costs. Key players like Banner Engineering and Pepperl+Fuchs dominate the premium segment, while mid-market adoption grows through IoT-integrated offerings.

Europe

Europe maintains the second-largest market share, with Germany and France collectively contributing 60% of regional revenue. EU Machinery Directive 2006/42/EC mandates collision prevention systems for all overhead cranes above 5-ton capacity, creating steady demand. The Nordic countries show highest adoption rates (over 75% penetration) due to advanced automation in shipbuilding and forestry sectors. Manufacturers emphasize cyber-secure sensor solutions complying with IEC 62443 standards, particularly for port applications. While Western Europe shows maturity, Eastern European growth trails due to smaller-scale industries favoring cost-effective IR sensors over premium laser alternatives.

Asia-Pacific

APAC demonstrates the fastest growth (CAGR 5.8%) led by China’s manufacturing expansions and India’s logistics infrastructure development. Chinese OEMs dominate ultrasonic sensor production, capturing 40% of global supply, while Japanese firms like Hokuyo lead in laser technology. The region sees divergent adoption patterns – automated factories deploy high-end systems, whereas construction sites still rely on basic proximity sensors. Key challenges include price sensitivity in ASEAN markets and lack of standardized safety protocols in emerging economies. India’s ‘Make in India’ initiative boosts portal crane installations, subsequently driving sensor demand.

South America

Brazil accounts for 65% of the regional market, primarily serving mining and agriculture sectors. Adoption focuses on ruggedized ultrasonic sensors for outdoor gantry cranes, though adoption rates remain below 30% due to economic volatility. Chile and Peru show promise with copper mining expansions, creating niche opportunities for explosion-proof sensor solutions. The lack of localized manufacturing (90% imports) keeps prices elevated, hindering SME adoption. Recent trade agreements may enable Chinese sensor suppliers to increase market penetration through competitive pricing.

Middle East & Africa

The GCC nations drive regional demand, particularly for portal cranes in mega-construction projects like NEOM and Dubai Urban Tech District. UAE and Saudi Arabia mandate ISO 12482-1 compliant systems for all heavy cranes, favoring European suppliers. Sub-Saharan Africa shows nascent growth, with mining operations in South Africa and Nigeria gradually adopting basic collision prevention. The region struggles with after-sales service gaps and harsh environment durability issues, though Turkish sensor manufacturers are making inroads with climate-resistant models.

Report Scope

This market research report provides a comprehensive analysis of the Global Crane Collision Detection Sensor Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 265 million in 2024 and is projected to reach USD 352 million by 2032, growing at a CAGR of 4.2%.

- Segmentation Analysis: Detailed breakdown by product type (Laser Distance Sensors, Infrared Sensors, Ultrasonic Sensors, Radar Sensors, Others) and application (Overhead Crane, Gantry Crane, Portal Crane, Others) to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. and China are key markets with significant growth potential.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Key players include SICK, IFM, Pepperl+Fuchs, Banner Engineering, and Turck.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT in sensor systems, and advancements in detection accuracy and reliability.

- Market Drivers & Restraints: Evaluation of factors driving market growth, such as increasing industrialization and stringent safety regulations, along with challenges like high installation costs.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Crane Collision Detection Sensor Market?

-> Crane Collision Detection Sensor Market was valued at 265 million in 2024 and is projected to reach US$ 352 million by 2032, at a CAGR of 4.2% during the forecast period.

Which key companies operate in Global Crane Collision Detection Sensor Market?

-> Key players include SICK, Laser-View Technologies, IFM, Symeo, Hokuyo, Turck, OndoSense, Leuze, Pepperl+Fuchs, and Banner Engineering, among others.

What are the key growth drivers?

-> Key growth drivers include rising industrialization, increasing adoption of automation, and stringent workplace safety regulations.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market due to high industrial safety standards.

What are the emerging trends?

-> Emerging trends include integration of AI-powered predictive analytics, wireless sensor networks, and IoT-enabled real-time monitoring systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...