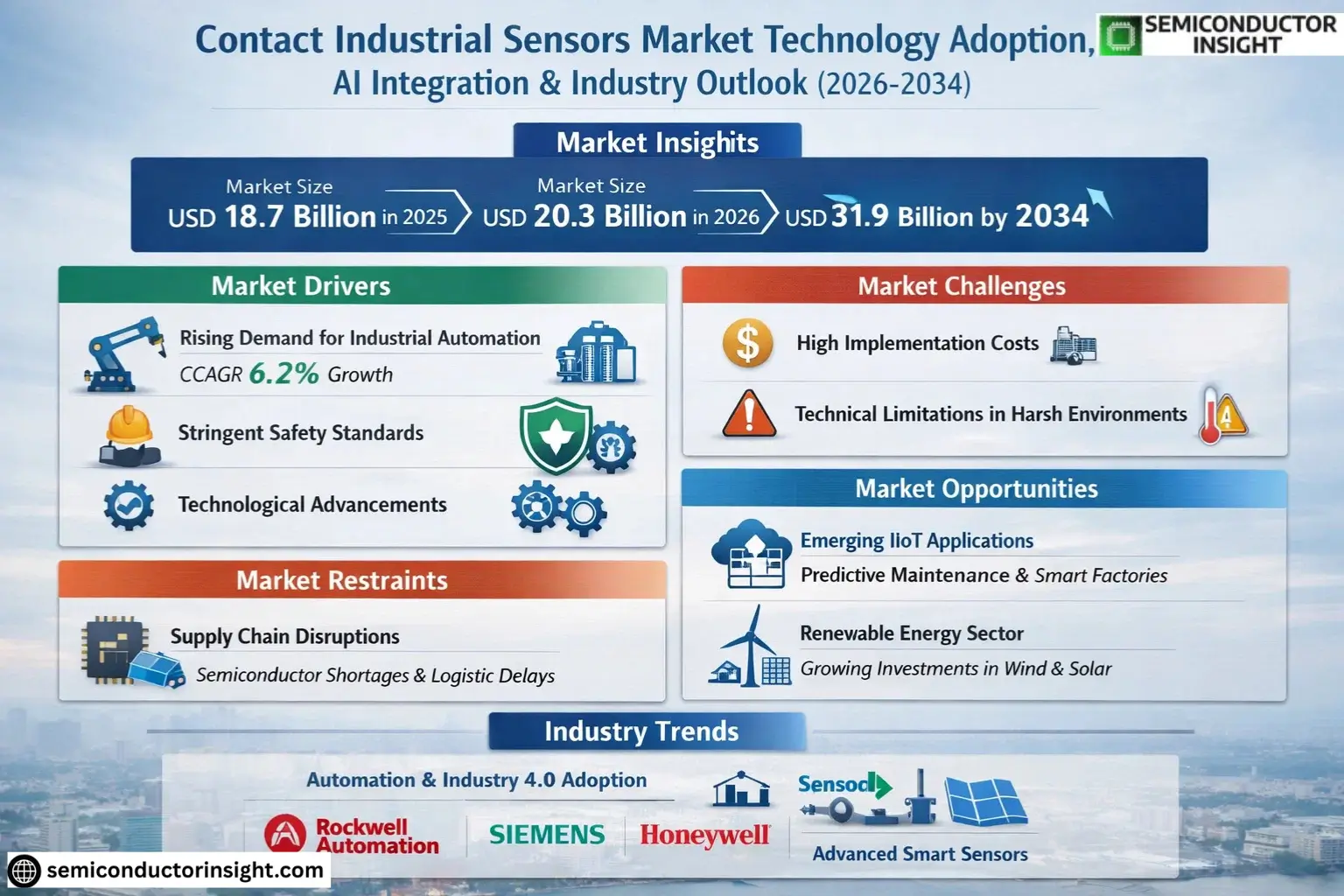

Market Insights

Global Contact Industrial Sensors Market size was valued at USD 18.7 billion in 2025. The market is projected to grow from USD 20.3 billion in 2026 to USD 31.9 billion by 2034, exhibiting a CAGR of 5.8% during the forecast period.

Contact industrial sensors are critical components used for monitoring and controlling physical parameters such as temperature, pressure, level, and position in industrial environments. These sensors ensure operational efficiency, safety, and automation across sectors like manufacturing, oil & gas, chemicals, and energy. Key types include level sensors, temperature sensors, gas sensors, pressure sensors, position sensors, and humidity & moisture sensors.

The market growth is driven by increasing industrial automation, stringent safety regulations, and the rising adoption of IoT-enabled smart sensors. Furthermore, advancements in sensor technologies such as MEMS (Micro-Electro-Mechanical Systems) and wireless connectivity are enhancing precision and reliability. Leading players like Rockwell Automation, Honeywell, Siemens, and Texas Instruments continue to innovate with high-performance solutions tailored for diverse industrial applications.

MARKET DRIVERS

Rising Demand for Industrial Automation

Global Contact Industrial Sensors Market is experiencing significant growth due to increasing adoption of automation in manufacturing. Factories are deploying these sensors to enhance precision and efficiency in processes such as assembly lines and quality control. The market is projected to grow at a CAGR of 6.2% over the next five years.

Stringent Industrial Safety Standards

Regulatory requirements for workplace safety are driving demand for contact industrial sensors that monitor equipment and environmental conditions. Industries such as oil & gas and chemicals rely on these sensors to prevent accidents and ensure compliance.

Technological advancements in sensor accuracy and durability are further propelling market adoption across heavy industries.

MARKET CHALLENGES

High Implementation Costs

Although contact industrial sensors offer long-term benefits, their initial deployment costs pose challenges for small and medium enterprises. Integration with legacy systems requires additional investments in retrofitting and workforce training.

Other Challenges

Technical Limitations in Extreme Environments

Certain contact sensor types face performance issues in high-temperature or corrosive industrial settings, requiring frequent maintenance and replacements.

MARKET RESTRAINTS

Supply Chain Disruptions

Contact Industrial Sensors Market faces constraints due to semiconductor shortages and logistics bottlenecks. Lead times for critical components have extended by 18-24 weeks, affecting production schedules across major manufacturers.

MARKET OPPORTUNITIES

Emerging IIoT Applications

Integration with Industrial Internet of Things (IIoT) platforms creates new opportunities for contact sensors in predictive maintenance systems. The smart factory trend is expected to generate $2.1 billion in sensor-related revenue by 2027.

Expansion in Renewable Energy Sector

Growing investments in wind and solar energy infrastructure are driving demand for rugged contact sensors that can monitor equipment performance under harsh environmental conditions.

Contact Industrial Sensors Market Trends

Automation and Industry 4.0 Driving Demand

Contact Industrial Sensors Market is witnessing significant growth due to increasing automation across manufacturing, oil & gas, and energy sectors. Industry 4.0 initiatives are accelerating adoption of smart sensors for real-time monitoring and process optimization. Leading manufacturers like Rockwell Automation, Siemens, and Honeywell are developing advanced contact sensors with enhanced precision for industrial applications.

Other Trends

Growth in Level Sensors Segment

Level sensors account for a substantial share of the Contact Industrial Sensors Market, with applications in liquid level monitoring across chemical processing and water treatment plants. Technological advancements in capacitive and ultrasonic level sensors are driving segment growth, particularly in Asia-Pacific markets.

Regional Market Developments

North America and Europe currently lead the Contact Industrial Sensors Market due to established industrial sectors and early technology adoption. However, Asia-Pacific is emerging as the fastest-growing region, with China, Japan, and South Korea investing heavily in industrial automation infrastructure. Key players are expanding manufacturing facilities in these regions to meet rising demand.

Technological Advancements in Sensor Capabilities

Recent innovations focus on improving sensor durability in extreme conditions and integrating IoT connectivity. Manufacturers are developing contact industrial sensors with self-diagnostic capabilities and wireless communication features to support predictive maintenance strategies in smart factories. The integration of AI and machine learning is further enhancing sensor performance analytics.

Other Trends

Expansion in Oil & Gas Applications

Contact industrial sensors play a critical role in upstream and downstream oil & gas operations, particularly for pressure and temperature monitoring in pipelines and refineries. Stringent safety regulations are driving investments in reliable sensor technologies with explosion-proof certifications from major industry players.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading manufacturers drive innovation in precision sensing technologies

Global Contact Industrial Sensors Market is dominated by established industrial automation and semiconductor leaders. Rockwell Automation and Honeywell jointly hold significant market share, leveraging their extensive portfolios for manufacturing and process automation applications. Siemens and Texas Instruments follow closely with advanced sensor solutions for Industry 4.0 implementations, particularly in temperature and pressure sensing segments. The top five players collectively accounted for a substantial revenue share in 2025, benefiting from integrated solutions and long-term contracts with industrial OEMs.

Specialist sensor manufacturers like Sensirion and Dwyer Instruments maintain strong positions in niche applications. Switzerland-based Sensirion leads in humidity sensing technology, while Dwyer Instruments excels in environmental monitoring solutions. Emerging competitors such as ams-OSRAM and Infineon Technologies are gaining traction with MEMS-based contact sensors, particularly in automotive and energy applications. The market sees increasing competition from Asian manufacturers like Panasonic and Omron, offering cost-competitive alternatives without compromising reliability.

List of Key Contact Industrial Sensors Companies Profiled

- Rockwell Automation

- Honeywell

- Siemens

- Texas Instruments

- STMicroelectronics

- TE Connectivity

- Amphenol Corporation

- Dwyer Instruments

- Bosch Sensortec

- Omega Engineering

- Sensirion

- ams-OSRAM

- ABB

- NXP Semiconductors

- Infineon Technologies

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Pressure Sensors demonstrate robust market presence due to:

|

| By Application |

|

Energy & Power sector shows strong adoption trends because:

|

| By End User |

|

Process Industries represent the dominant segment characterized by:

|

| By Technology |

|

MEMS Technology is transforming the market through:

|

| By Integration Level |

|

Smart Sensor Nodes are gaining momentum due to:

|

Regional Analysis: Contact Industrial Sensors Market

North American manufacturers pioneer MEMS-based contact sensors with superior accuracy for harsh industrial environments. These sensors integrate seamlessly with industrial IoT platforms, offering real-time monitoring capabilities critical for predictive maintenance systems.

Advanced AI algorithms process contact sensor data to detect micro-level defects in production lines. U.S.-based tech firms are developing self-calibrating sensors that automatically adjust measurement parameters based on machine learning insights from operational data.

Strategic partnerships between automotive OEMs and sensor manufacturers drive customized contact sensor solutions. These collaborations focus on developing application-specific sensors for electric vehicle battery manufacturing and aerospace component testing.

Compliance with stringent OSHA and ANSI standards pushes manufacturers to adopt certified contact sensors. The regulatory environment ensures continuous innovation in sensor durability and measurement precision for industrial safety applications.

Europe

Europe maintains a strong position in the Contact Industrial Sensors Market through its precision engineering heritage. Germany’s Industry 4.0 initiatives drive demand for high-accuracy contact sensors in automotive and pharmaceutical manufacturing. The region sees growing adoption of miniaturized sensors for robotic assembly lines in Italy and France. Strict EU regulations on industrial emissions monitoring create additional opportunities for specialized contact sensors. Collaborative R&D projects between universities and manufacturers accelerate development of energy-efficient sensor technologies.

Asia-Pacific

Asia-Pacific emerges as the fastest-growing market for Contact Industrial Sensors, fueled by expanding manufacturing hubs in China and Japan. Chinese factories increasingly integrate contact sensors for quality control in electronics production. Japan leads in developing ultra-precise sensors for semiconductor manufacturing equipment. Government initiatives supporting smart manufacturing across India and Southeast Asia contribute to market expansion. Local sensor manufacturers focus on cost-competitive solutions for medium-scale industries.

South America

South America shows steady growth in Contact Industrial Sensor adoption, particularly in Brazil’s automotive and mining sectors. The region benefits from technology transfer agreements with North American and European sensor manufacturers. Local companies focus on ruggedized sensors suitable for tropical industrial environments. Chile’s mining automation projects create specialized demand for vibration and pressure contact sensors.

Middle East & Africa

The Middle East sees increasing deployment of contact sensors in oil & gas infrastructure monitoring. UAE leads in smart factory implementations requiring precision measurement sensors. African markets show potential with growing investments in industrial automation, though adoption remains limited to multinational manufacturing facilities. Regional players focus on developing dust- and moisture-resistant sensor variants.

Report Scope

This market research report provides a comprehensive analysis of the Contact Industrial Sensors Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of industrial sensors in powering advancements across industries such as manufacturing, oil & gas, chemicals, pharmaceuticals, and energy.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, sensor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Contact Industrial Sensors Market?

-> Contact Industrial Sensors Market size was valued at USD 18.7 billion in 2025. The market is projected to grow from USD 20.3 billion in 2026 to USD 31.9 billion by 2034, exhibiting a CAGR of 5.8% during the forecast period.

Which key companies operate in Contact Industrial Sensors Market?

-> Key players include Rockwell Automation, Honeywell, Panasonic, Texas Instruments, STMicroelectronics, TE Connectivity, Siemens, Amphenol Corporation, Dwyer Instruments, Bosch Sensortec, among others.

What is the market outlook by segment?

-> Level Sensor segment will reach USD million by 2034, exhibiting a % CAGR over the forecast period.

What are the key applications driving demand?

-> Key applications include Manufacturing, Oil & Gas, Chemicals, Pharmaceuticals, Energy & Power, and Mining sectors.

Which regions show significant growth potential?

-> China is expected to reach USD million by 2034, while the U.S. market is estimated at USD million in 2025.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...