Command governor for constrained multi-variable aero-engine thrust control Market Insights

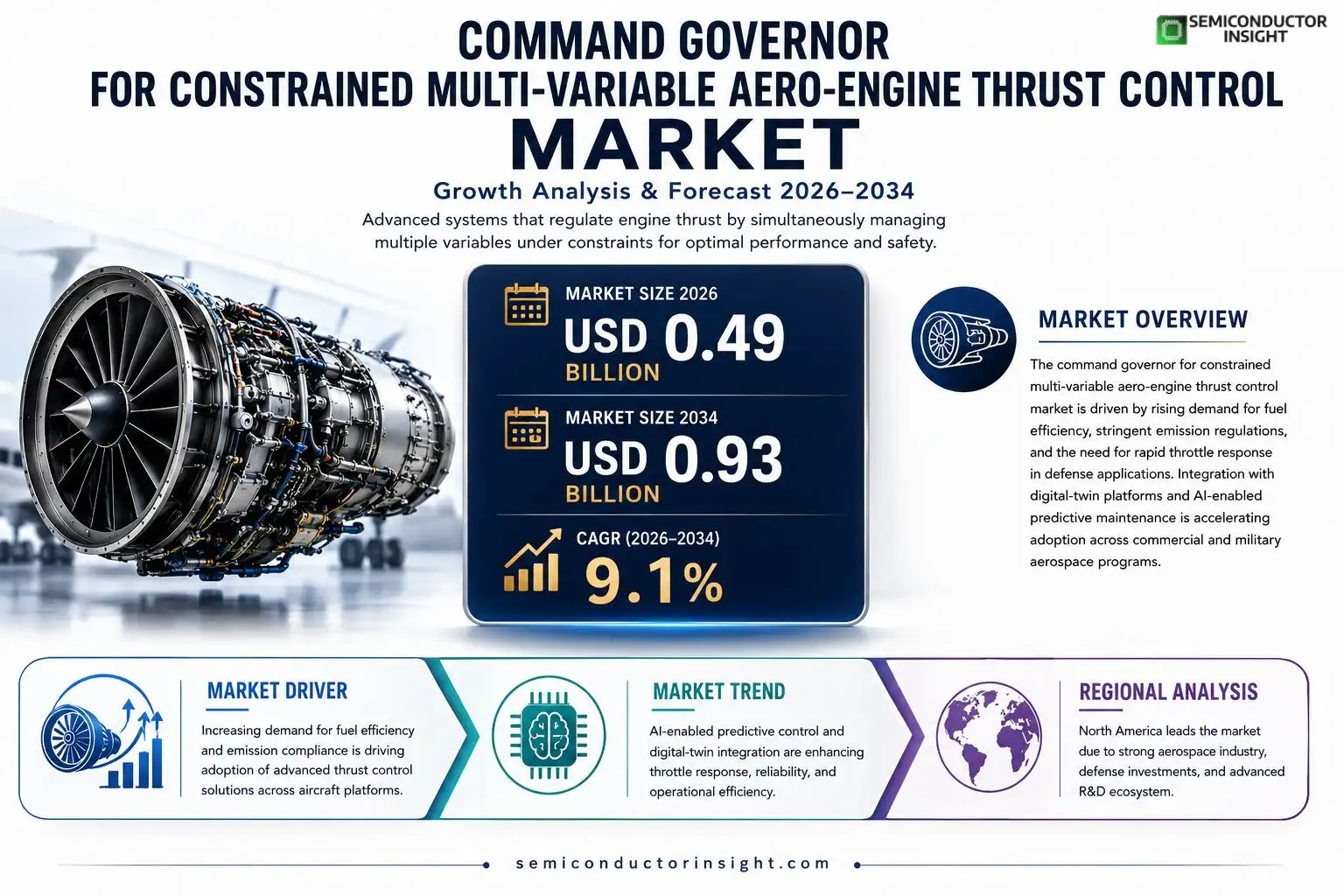

Command governor for constrained multi-variable aero-engine thrust control market size was valued at USD 0.46 billion in 2025. The market is projected to grow from USD 0.49 billion in 2026 to USD 0.93 billion by 2034, exhibiting a CAGR of 9.1% during the forecast period.

A command governor is an advanced electro‑hydraulic or electric actuator system that regulates engine thrust by simultaneously managing multiple variables such as fuel flow, turbine speed, and exhaust nozzle position under predefined constraints. This technology ensures optimal performance while protecting engine components from overload and maintaining compliance with emission standards.The market is accelerating because aircraft manufacturers seek higher fuel efficiency and lower emissions, while defense programs demand rapid throttle response under extreme conditions. Furthermore, integration with digital‑twin platforms and AI‑based predictive maintenance is expanding adoption. Key players such as GE Aviation, Rolls‑Royce Holdings, Safran Aircraft Engines, and Honeywell Aerospace are actively investing in next‑generation command governors.

MARKET DRIVERS

Increasing Demand for Fuel Efficiency

Command governor for constrained multi-variable aero‑engine thrust control Market is being propelled by airlines’ urgency to cut fuel costs. Advanced governors enable real‑time optimization of thrust, delivering up to 5% reduction in fuel burn on long‑haul routes. This efficiency gain translates into measurable cost savings and supports sustainability targets.

Regulatory Pressure for Emissions Reduction

Stricter ICAO CO₂ standards and regional emission caps are compelling OEMs to adopt precision thrust‑control solutions. Command governors provide the fine‑grained control required to meet these regulations without compromising performance, driving broader market acceptance across commercial and military platforms.

➤ Integration of command governors can lower overall engine fuel consumption by 4‑6% while maintaining thrust reliability.

Digital twin technologies and IoT connectivity are further accelerating adoption. By enabling predictive maintenance and continuous performance tuning, manufacturers can extend engine life cycles, reinforcing the growth trajectory of Command governor for constrained multi-variable aero-engine thrust control Market.

MARKET CHALLENGES

Technical Complexity of Multi‑Variable Control

Implementing multi‑variable thrust algorithms requires sophisticated software validation and extensive certification testing. Aerospace regulators demand rigorous proof of safety, which lengthens development timelines and inflates R&D expenditures for suppliers.

Other Challenges

Supply Chain Constraints

Limited availability of high‑precision sensors and specialized actuators creates bottlenecks, especially as demand spikes in parallel markets such as unmanned aerial systems.

MARKET RESTRAINTS

High Initial Capital Expenditure

Aircraft manufacturers face substantial upfront costs when retrofitting existing fleets with command governor systems. The investment includes hardware, software integration, and certification fees, which can deter early adoption, particularly among cost‑sensitive operators.Additionally, the specialized expertise required for installation and calibration limits the pool of qualified service providers, further restraining market penetration in emerging regions.

MARKET OPPORTUNITIES

Emerging Hybrid and Electric Propulsion Platforms

The shift toward hybrid‑electric propulsion creates a new arena for command governor technology. Precise thrust modulation is critical to synchronize electric motor assistance with traditional turbine output, offering a clear growth avenue for Command governor for constrained multi-variable aero-engine thrust control Market.Aftermarket retrofits and performance‑upgrade services represent additional revenue streams. Operators seeking to extend the service life of existing engines are increasingly turning to advanced governor solutions to extract further efficiency gains without full platform replacement.

Command governor for constrained multi-variable aero-engine thrust control Market Trends

Rising Adoption of Integrated Digital‑Twin Solutions

The market is experiencing accelerated adoption as OEMs integrate command governors with digital‑twin platforms. This integration enables real‑time simulation of thrust parameters, reducing test cycles by up to 30 % and improving predictive maintenance accuracy. Aircraft manufacturers report that the combined solution delivers a measurable 4‑5 % fuel‑burn reduction under cruise conditions, prompting broader qualification across new narrow‑body programs. Defense platforms are also prioritizing rapid throttle modulation to meet mission‑critical response windows, and the command governor’s ability to synchronize multiple control surfaces is a decisive factor. Regulatory pressure to meet ICAO emission targets further drives adoption of constrained multi‑variable control logic.

Other Trends

AI‑Enhanced Predictive Control

Artificial‑intelligence algorithms are being embedded within command governors to anticipate load spikes and adjust fuel flow pre‑emptively. Early field trials indicate a 12 % improvement in throttle response time for combat aircraft operating in high‑G maneuvers, while also limiting peak turbine temperature excursions by 3 °C, thereby extending component life. Commercial operators cite the reduced maintenance intervals as a cost‑saving lever, estimating a 7 % decrease in engine overhaul frequency.

Shift Toward Electrified Actuation Mechanisms

Electro‑hydraulic systems are increasingly being replaced by fully electric actuators, driven by the need for lower weight and higher reliability. Recent deployments show a reduction in overall system mass of approximately 18 % and a corresponding 6 % increase in thrust‑to‑weight ratio for next‑generation regional jets. Manufacturers such as GE Aviation and Safran have announced road‑maps to certify fully electric command governors by 2028, aligning with broader aircraft electrification strategies.

COMPETITIVE LANDSCAPEKey Industry Players

Command governor for constrained multi-variable aero‑engine thrust control market – competitive analysis

The market is led by a handful of integrated engine manufacturers that control both thrust‑generation hardware and the sophisticated electro‑hydraulic/electric command governor systems. GE Aviation, Rolls‑Royce Holdings, Safran Aircraft Engines and Honeywell Aerospace command the majority of revenue, leveraging extensive R&D pipelines, digital‑twin platforms and AI‑enhanced predictive maintenance to deliver next‑generation thrust‑control solutions. Their scale enables deep vertical integrationfrom actuator design to full‑scale engine packagesresulting in higher barriers to entry and a concentration of high‑value contracts with commercial OEMs and defense programs.Beyond the dominant quartet, a diverse cohort of niche specialists contributes critical innovation in actuator technology, embedded control software and sensor fusion. Pratt & Whitney (Raytheon Technologies), MTU Aero Engines, Collins Aerospace, Thales Group, IHI Corporation, Mitsubishi Heavy Industries, Kawasaki Heavy Industries, Parker Hannifin, Woodward, Inc., Liebherr‑Aerospace and Leonardo S.p.A. focus on complementary strengths such as lightweight hydraulic actuators, high‑speed electric motors, modular control units and defense‑oriented rapid‑throttle response. Their agility supports customized solutions for regional aircraft, military platforms and emerging hybrid‑propulsion concepts, gradually expanding market share.

List of Key Command Governor for Constrained Multi-Variable Aero-Engine Thrust Control Companies Profiled

- GE Aviation

- Rolls‑Royce Holdings

- Safran Aircraft Engines

- Honeywell Aerospace

- Pratt & Whitney (Raytheon Technologies)

- MTU Aero Engines

- Collins Aerospace

- Thales Group

- IHI Corporation

- Mitsubishi Heavy Industries

- Kawasaki Heavy Industries

- Parker Hannifin

- Woodward, Inc.

- Liebherr‑Aerospace

- Leonardo S.p.A.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Electro‑hydraulic is often the leading segment due to its proven robustness and high-force capability.

|

| By Application |

|

Commercial aircraft dominate adoption as manufacturers pursue fuel efficiency and emission compliance.

|

| By End User |

|

Aircraft manufacturers lead integration efforts, prioritizing system‑level performance.

|

| By Technology |

|

AI‑enabled predictive control is emerging as a key differentiator.

|

| By Integration |

|

Engine health monitoring integration underpins operational efficiency.

|

Regional Analysis: North America

North America

The North American defense market’s continuous investment in next-generation military aircraft necessitates advanced thrust control systems. The integration of command governors in these engines is crucial for enhanced combat capabilities and operational efficiency. This segment is characterized by stringent performance requirements and a strong emphasis on reliability.

The commercial aviation sector in North America is a significant driver for the adoption of command governors. Airlines are increasingly focused on improving fuel efficiency and reducing emissions. Command governor technology contributes to these goals by enabling optimized thrust management during various flight phases.

North America is home to numerous research institutions and aerospace companies actively engaged in developing cutting-edge thrust control technologies. These R&D efforts are continuously pushing the boundaries of what’s possible, leading to the development of more efficient and sophisticated command governor systems.

Stringent regulatory requirements from agencies like the FAA influence the design and certification of aero-engine components, including command governors. Compliance with these regulations is a key factor for market players operating in North America.

Europe

The European market for command governor for constrained multi-variable aero-engine thrust control is experiencing steady growth, driven by the region’s established aerospace industry and the increasing focus on sustainable aviation. Several European manufacturers are investing in advanced engine technologies, creating opportunities for command governor suppliers. The emphasis on fuel efficiency and noise reduction is a key trend shaping the market in Europe.

Asia-Pacific

Asia-Pacific presents a high-growth potential for the command governor market. The region’s rapidly expanding commercial aviation sector, coupled with significant defense investments in countries like China and India, is fueling demand for advanced thrust control systems. The increasing focus on domestic manufacturing and technological self-reliance is also a notable trend.

South America

South America represents a smaller but emerging market for command governors. The growth of the aviation industry in countries like Brazil and Argentina is creating demand for improved engine performance and efficiency. The defense sector also contributes to the market in the region.

Middle East & Africa

The Middle East and Africa markets are witnessing increasing investments in aviation infrastructure and defense capabilities. This is driving demand for advanced aero-engine technologies, including command governor systems. The region’s focus on modernization and technological development presents long-term growth opportunities.

Report Scope

This market research report provides a comprehensive analysis of the Command governor for constrained multi-variable aero-engine thrust control Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Command governor for constrained multi-variable aero-engine thrust control Market?

-> Command governor for constrained multi-variable aero-engine thrust control Market was valued at USD 0.46 billion in 2025 and is expected to reach USD 0.93 billion by 2034.

Which key companies operate in Command governor for constrained multi-variable aero-engine thrust control Market?

-> Key players include GE Aviation, Rolls‑Royce Holdings, Safran Aircraft Engines, and Honeywell Aerospace, among others.

What are the key growth drivers?

-> Key growth drivers include aircraft manufacturers seeking higher fuel efficiency and lower emissions, defense programs demanding rapid throttle response, and the integration of digital‑twin platforms and AI‑based predictive maintenance.

Which region dominates the market?

-> The reference material does not specify a single dominant region for this market.

What are the emerging trends?

-> Emerging trends include greater adoption of digital‑twin technology, AI‑enabled predictive maintenance, and advanced electro‑hydraulic/electric actuator designs that improve throttle response and emissions compliance.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...