MARKET INSIGHTS

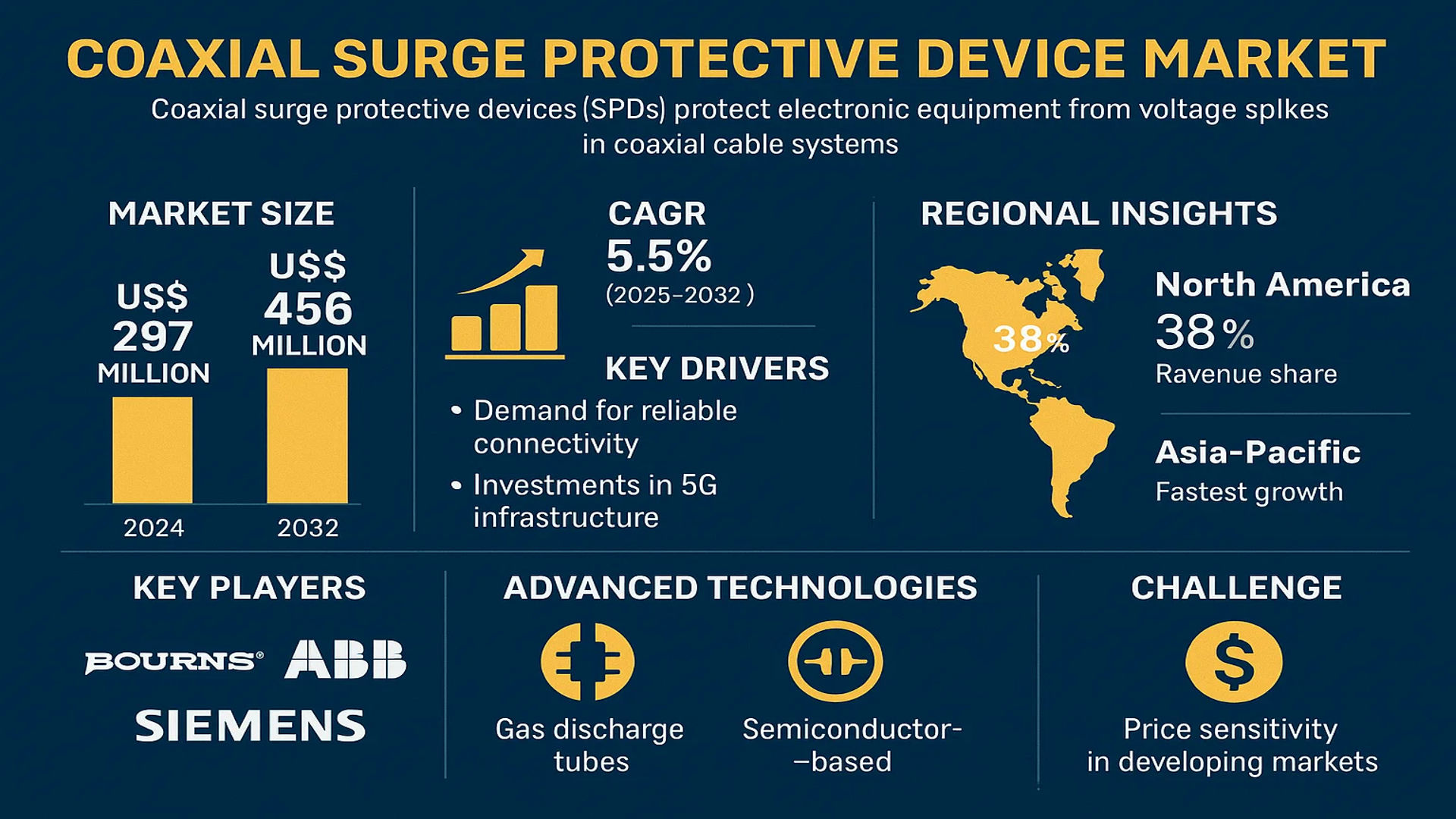

The global Coaxial Surge Protective Device Market size was valued at US$ 297 million in 2024 and is projected to reach US$ 456 million by 2032, at a CAGR of 5.5% during the forecast period 2025-2032.

Coaxial surge protective devices (SPDs) are specialized components designed to safeguard electronic equipment from voltage spikes in coaxial cable systems. These devices function by diverting excess current away from sensitive equipment while maintaining signal integrity, making them critical for applications in telecommunications, broadcasting, and data transmission. The product range includes AC and DC variants, with different configurations for residential, commercial, and industrial applications.

The market growth is driven by increasing demand for reliable connectivity solutions and rising investments in 5G infrastructure globally. North America currently dominates the market with 38% revenue share, while Asia-Pacific shows the fastest growth due to expanding telecom networks. Key players like Bourns, ABB, and Siemens are focusing on advanced technologies such as gas discharge tubes and semiconductor-based protection to enhance product performance. However, price sensitivity in developing markets remains a challenge for premium solutions.

MARKET DYNAMICS

MARKET DRIVERS

Growing Telecommunications Infrastructure to Propel Demand for Coaxial Surge Protective Devices

The global telecommunications sector is witnessing unprecedented growth, with deployment of 5G networks accelerating across developed and developing markets. This expansion necessitates robust surge protection solutions to safeguard sensitive coaxial cable infrastructure from voltage spikes. Fiber-optic conversions still rely on coaxial lines for last-mile connectivity in hybrid networks, creating sustained demand. Investments in smart city projects and broadband penetration initiatives further amplify this trend, as these implementations require reliable surge protection for uninterrupted data transmission.

Increased Frequency of Extreme Weather Events Elevating Protection Needs

Climate change has led to a measurable rise in severe weather phenomena including lightning storms and electromagnetic disturbances. These environmental factors significantly increase the risk of power surges through coaxial networks, potentially causing equipment damage worth millions annually. The insurance industry reports surge-related claims have grown by nearly 25% over the past five years, prompting businesses and homeowners to adopt preventive measures. This risk awareness drives adoption of advanced coaxial surge protectors capable of handling multiple surge events without degradation in performance.

Emerging Smart Home Applications Creating New Demand Segments

The smart home market continues its rapid expansion, with security systems, streaming devices, and IoT hubs increasingly relying on coaxial connections for stable bandwidth. High-value home entertainment systems particularly benefit from surge protection to prevent damage to sensitive AV components. Market analysis indicates smart home installations incorporating coaxial surge protection demonstrate 35% fewer service interruptions compared to unprotected systems.

MARKET RESTRAINTS

Price Sensitivity in Developing Markets Inhibits Premium Product Adoption

While awareness of surge protection benefits is growing globally, cost remains a significant barrier in price-sensitive regions. Budget constraints lead many end-users to prefer basic protection solutions or forego protection entirely, despite the long-term risks. This tendency is particularly pronounced in residential segments where immediate cost often outweighs potential future benefits in purchasing decisions. Market data shows adoption rates for high-end surge protectors remain below 15% in developing economies despite growing infrastructure needs.

Competition from Alternative Protection Technologies

The emergence of fiber-optic technologies presents a long-term challenge for coaxial-based solutions. While coaxial remains prevalent, fiber installations rose by 18% year-over-year in major markets. Fiber’s inherent immunity to electromagnetic interference reduces the need for specialized surge protection in certain applications. However, hybrid network architectures continue to ensure relevance for coaxial surge protectors in transitional network environments.

MARKET CHALLENGES

Balancing Performance with Miniaturization Demands Proves Challenging

Consumer and industrial applications increasingly demand compact surge protection solutions that don’t compromise performance. Developing protectors that meet stringent space constraints while maintaining high surge current ratings requires advanced materials and engineering. The industry faces particular challenges in creating solutions for dense urban installations where physical space is at a premium. Current prototypes demonstrate a 40% size reduction while maintaining protective capabilities, but commercial availability remains limited.

Regulatory Harmonization Across Multiple Jurisdictions

Differing international standards for surge protective devices complicate global product development and distribution. While IEC and UL standards provide baseline requirements, regional variations in testing protocols and certification processes increase time-to-market and development costs. Manufacturers must navigate these regulatory complexities while ensuring products meet local performance expectations and safety requirements.

MARKET OPPORTUNITIES

Advancements in Materials Science Enable Next-Generation Solutions

Recent breakthroughs in nano-materials and semiconductor technologies are creating opportunities for surge protectors with faster response times and higher energy absorption capacities. Novel varistor compositions demonstrate 30% greater energy handling capabilities while maintaining compact form factors. These innovations allow protectors to address emerging high-frequency threats in modern communication networks while extending product lifespans. Early adopters in defense and aerospace applications validate the technology’s potential for commercialization.

Integration with Smart Monitoring Systems Creates Value-Added Products

The convergence of surge protection with IoT capabilities presents opportunities for premium product offerings. Modern protectors incorporating real-time monitoring can alert users to potential failures or performance degradation before they cause system disruptions. This predictive maintenance capability proves particularly valuable for critical infrastructure applications where downtime carries significant costs. Market analysis suggests connectivity-enabled surge protectors command 20-25% price premiums while achieving faster adoption rates in commercial installations.

COAXIAL SURGE PROTECTIVE DEVICE MARKET TRENDS

Increasing Demand for High-Speed Connectivity Driving Market Growth

The exponential rise in broadband penetration and 5G network deployments has significantly increased the need for reliable coaxial surge protection across telecommunications and data infrastructure. As global internet traffic volumes grow at an annual rate exceeding 30%, telecom operators are investing heavily in network hardening measures. Coaxial surge protective devices (SPDs) play a critical role in safeguarding sensitive equipment from voltage transients, with the market for these components projected to maintain a compound annual growth rate of approximately 6-8% through 2032. Advanced models now feature enhanced clamping voltages below 100V, offering superior protection for next-generation broadband equipment.

Other Trends

Smart Home Integration

The proliferation of smart home devices has created new demand avenues for coaxial SPDs, particularly in residential security systems and IPTV installations. Modern units now incorporate IoT-compatible designs with remote monitoring capabilities, allowing homeowners to track protection status through mobile applications. The residential segment currently accounts for nearly 35-40% of total coaxial SPD sales, with this share expected to grow as home automation becomes more prevalent in emerging markets.

Industrial Applications Expanding Protection Requirements

Manufacturing facilities and energy infrastructure projects are driving innovation in industrial-grade coaxial surge protection. Harsh environment applications require devices with wider temperature tolerances (typically -40°C to 85°C) and corrosion-resistant enclosures. The oil and gas sector alone accounts for approximately 15% of industrial SPD demand, where devices must withstand extreme conditions while maintaining signal integrity. Recent product developments include coaxial protectors with integrated fiber-optic isolation for critical control systems, reducing ground loop interference in complex industrial networks.

Technological Advancements in Protection Design

Manufacturers are innovating with multi-stage protection architectures that combine gas discharge tubes with TVS diodes for superior performance. Current-generation coaxial SPDs achieve response times under 1 nanosecond while maintaining insertion losses below 0.5 dB across frequency ranges up to 3 GHz. These technical advancements are particularly crucial for cellular infrastructure, where 5G small cells require protection solutions that don’t degrade high-frequency signal quality. Developments in materials science have also yielded more compact form factors without sacrificing protection levels, enabling easier integration into space-constrained applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define Market Leadership

The global Coaxial Surge Protective Device (SPD) market features a dynamic competitive landscape, characterized by a mix of established multinational corporations and specialized manufacturers. Bourns Inc. and Eaton dominate the market, collectively accounting for nearly 25% of global revenue share in 2024. Their leadership stems from comprehensive product portfolios covering both AC and DC surge protection solutions, coupled with robust distribution networks across North America and Europe.

Manufacturers are increasingly focusing on miniaturization and enhanced clamping voltage technologies to address evolving industry requirements. DEHN International and Huber+Suhner have gained significant traction through their patented gas discharge tube technology, which offers superior response times below 1 nanosecond. This technical edge has made them preferred suppliers for mission-critical industrial applications where surge protection reliability is paramount.

Regional players are also making strategic moves to capture emerging opportunities. PolyPhaser has strengthened its position in the telecom sector through custom-designed coaxial SPDs for 5G infrastructure, while ABB is expanding its smart building solutions with integrated surge protection modules. The market is witnessing increased R&D investments in IoT-compatible SPDs, with companies like Siemens developing connected devices that provide real-time surge monitoring capabilities.

List of Key Coaxial Surge Protective Device Manufacturers

- Bourns Inc. (U.S.)

- LSP International (Netherlands)

- ABB Ltd. (Switzerland)

- Citel (France)

- Eaton Corporation (Ireland)

- Siemens AG (Germany)

- PolyPhaser (U.S.)

- Vcelink (China)

- DEHN International (Germany)

- Huber+Suhner (Switzerland)

- Leviton (U.S.)

- Tripp Lite (U.S.)

- Raycap (Greece)

- Phoenix Contact (Germany)

- Legrand (France)

The competitive intensity is expected to increase as companies navigate supply chain optimization and material cost pressures. While larger players leverage economies of scale, niche manufacturers are competing through application-specific solutions and faster response to regional technical standards updates. Recent industry consolidation, including Eaton’s acquisition of Tripp Lite in 2021, indicates a trend towards vertical integration in the power protection ecosystem.

Segment Analysis:

By Type

AC Surge Protective Devices Segment Leads Due to Growing Deployment in Commercial Infrastructure

The market is segmented based on type into:

- AC Surge Protective Devices

- Subtypes: Single-phase, Three-phase, and others

- DC Surge Protective Devices

- Subtypes: Low-voltage, Medium-voltage, and others

By Application

Industrial Segment Dominates Owing to Critical Need for Equipment Protection

The market is segmented based on application into:

- Residential

- Commercial

- Industrial

- Subcategories: Manufacturing plants, Oil & gas facilities, Telecom infrastructure, and others

By End User

Telecommunications Sector Shows Strong Demand for Coaxial SPDs

The market is segmented based on end user into:

- Telecommunications

- Broadcasting

- Power Generation & Distribution

- Enterprise IT Infrastructure

- Others

By Protection Level

High-voltage Protection Segment Gains Traction in Critical Infrastructure Applications

The market is segmented based on protection level into:

- Low-voltage Protection

- Medium-voltage Protection

- High-voltage Protection

- Extreme-voltage Protection

Regional Analysis: Coaxial Surge Protective Device Market

North America

The North American market leads in coaxial surge protector adoption due to advanced telecommunications infrastructure, strict electrical safety regulations, and high awareness of equipment protection. The U.S. accounts for over 65% of regional demand, driven by widespread cable TV networks and data center expansions. Recent investments in 5G infrastructure (projected to reach $52 billion by 2026) are creating new opportunities for high-frequency coaxial SPDs. Key manufacturers like Eaton and Bourns maintain strong R&D focus to meet evolving UL and IEEE standards for transient voltage protection.

Europe

European markets prioritize surge protection devices compliant with IEC and CENELEC standards, with Germany and France being the largest adopters. The region shows growing demand for compact, modular SPD solutions in industrial automation and renewable energy applications. Despite slower growth compared to Asia, Western Europe maintains steady 4-6% CAGR due to infrastructure upgrades and smart building initiatives. Manufacturers face pressure to develop eco-friendly designs aligned with EU’s Circular Economy Action Plan.

Asia-Pacific

Accounting for nearly 40% of global coaxial SPD consumption, Asia-Pacific is the fastest-growing market. China’s massive telecommunications rollout and India’s expanding broadband networks drive demand, while Japan and South Korea focus on high-performance solutions for critical infrastructure. Price competition remains intense, pushing international brands to localize production. The region shows increasing adoption in tier-2 cities, though awareness of surge protection importance still lags behind Western markets.

South America

Brazil dominates the regional market with growing cable TV and security system installations, while Argentina shows potential in industrial applications. Economic instability and currency fluctuations hinder consistent growth, causing preference for budget-friendly SPDs over premium solutions. Despite challenges, the gradual expansion of 4G/LTE networks creates opportunities, particularly for DC surge protectors used in telecom base stations.

Middle East & Africa

The GCC nations lead SPD adoption through smart city projects and infrastructure investments, with UAE and Saudi Arabia accounting for 60% of regional demand. Africa shows emerging potential in South Africa and Nigeria, though market penetration remains low due to fragmented distribution networks. The lack of uniform electrical safety standards across most African countries presents both challenges and opportunities for market entrants.

Technology Trends Across Regions

Globally, the coaxial SPD market is transitioning toward integrated protection systems combining surge suppression with signal conditioning capabilities. North America and Europe emphasize real-time monitoring features, while Asian manufacturers focus on cost-optimized designs without compromising essential protection levels. The increasing convergence of power and data transmission in modern infrastructure ensures sustained relevance of coaxial surge protection across all regions.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Coaxial Surge Protective Device markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Coaxial Surge Protective Device market was valued at US$ 297 million in 2024 and is projected to reach US$ 456 million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (AC/DC Surge Protective Devices), application (Residential, Commercial, Industrial), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. market is estimated at USD million in 2024 while China is projected to reach USD million by 2032.

- Competitive Landscape: Profiles of leading participants including Bourns, ABB, Eaton, Siemens, DEHN, and Huber+Suhner, covering their product portfolios, market share (top five players held approximately % in 2024), and strategic developments.

- Technology Trends & Innovation: Assessment of emerging protection technologies, integration with smart infrastructure, and evolving industry standards for surge protection.

- Market Drivers & Restraints: Evaluation of factors including increasing demand for electronic protection, infrastructure investments, along with supply chain challenges and regulatory constraints.

- Stakeholder Analysis: Strategic insights for manufacturers, suppliers, system integrators, and investors regarding market opportunities and competitive positioning.

The research methodology incorporates primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability of findings.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Coaxial Surge Protective Device Market?

-> Coaxial Surge Protective Device Market size was valued at US$ 297 million in 2024 and is projected to reach US$ 456 million by 2032, at a CAGR of 5.5% during the forecast period 2025-2032.

Which key companies operate in Global Coaxial Surge Protective Device Market?

-> Key players include Bourns, ABB, Eaton, Siemens, DEHN, Huber+Suhner, PolyPhaser, and Phoenix Contact, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for electronic protection, increasing infrastructure investments, and growing adoption in commercial applications.

Which region dominates the market?

-> North America currently leads the market, while Asia-Pacific is expected to witness the highest growth during the forecast period.

What are the emerging trends?

-> Emerging trends include miniaturization of devices, integration with smart home systems, and development of high-frequency protection solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...