MARKET INSIGHTS

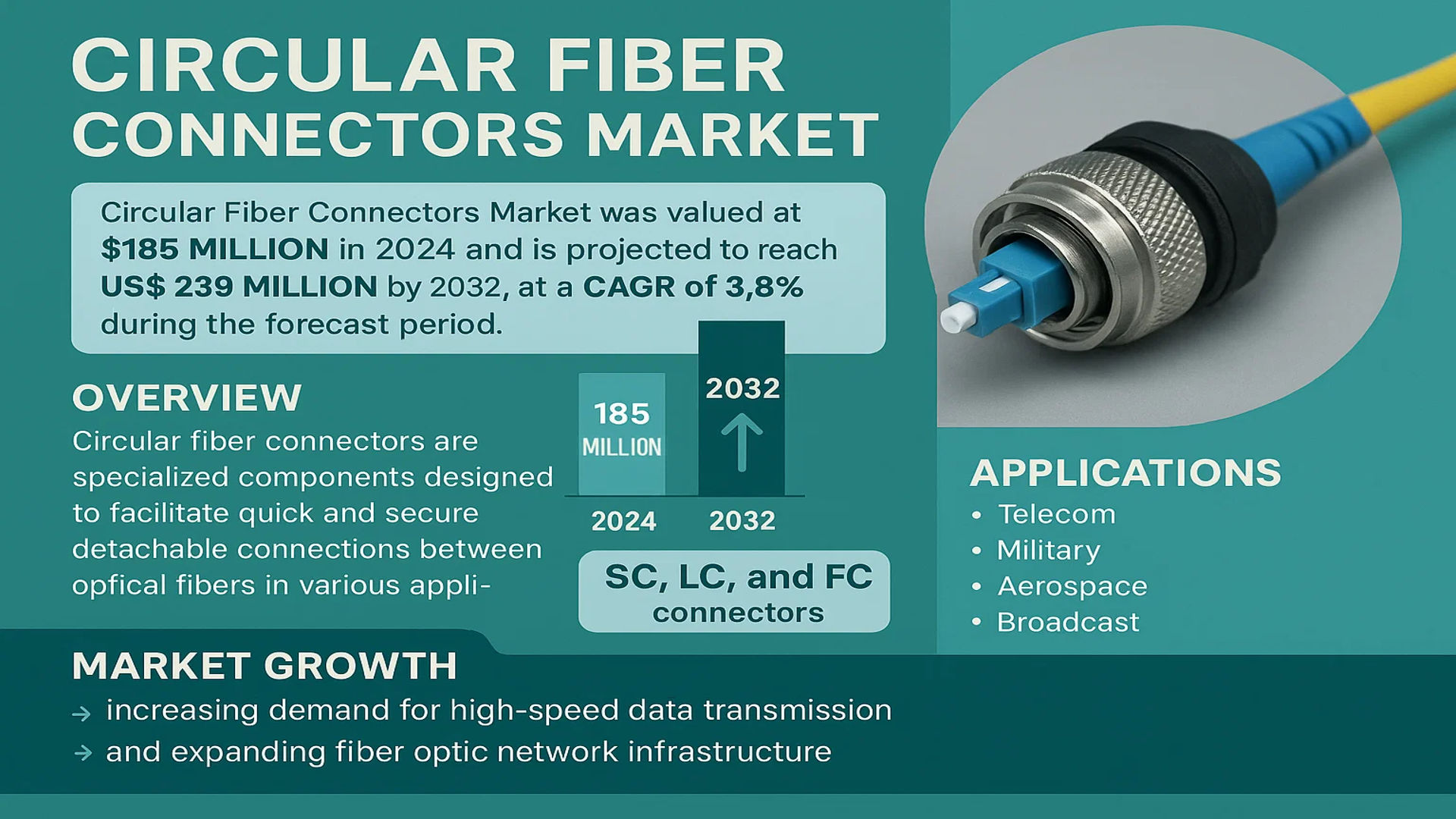

The global Circular Fiber Connectors Market was valued at 185 million in 2024 and is projected to reach US$ 239 million by 2032, at a CAGR of 3.8% during the forecast period.

Circular fiber connectors are specialized components designed to facilitate quick and secure detachable connections between optical fibers in various applications. These cylindrical connectors are widely utilized in industries such as telecom, military, aerospace, and broadcast due to their durability and ease of use in high-performance environments. Key types include SC, LC, and FC connectors, each offering unique advantages in terms of insertion loss and alignment precision.

Market growth is driven by increasing demand for high-speed data transmission and expanding fiber optic network infrastructure. The U.S. currently dominates the market, while China is expected to witness the fastest growth due to rapid telecom sector expansion. Leading players such as Amphenol, TE Connectivity, and Corning are investing in advanced connector technologies to meet evolving industry needs, further propelling market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for High-Speed Data Transmission to Fuel Market Expansion

The global circular fiber connectors market is witnessing significant growth driven by the escalating demand for high-speed data transmission across industries. With data traffic projected to grow exponentially, fiber optic networks are becoming indispensable, creating substantial demand for reliable connector solutions. The telecom sector, which accounts for over 45% of market demand, is particularly driving this growth as service providers upgrade their infrastructure to support 5G networks. The enhanced durability and signal integrity offered by circular connectors make them ideal for these high-performance applications.

Furthermore, the increasing adoption of cloud computing services and IoT devices is amplifying network bandwidth requirements. Data centers alone are expected to contribute nearly 30% to the market growth by 2032, as they transition to higher-density fiber connections. Recent advancements in connector design have significantly improved insertion loss performance, with many models now achieving less than 0.3 dB loss, making them increasingly attractive for mission-critical applications.

Military and Aerospace Applications Create Robust Demand

The military and aerospace sectors are increasingly adopting circular fiber connectors due to their superior performance in harsh environments. These connectors demonstrate remarkable resistance to extreme temperatures, vibration, and electromagnetic interference, making them suitable for defense communications, avionics, and space applications. The global defense expenditure, which surpassed $2 trillion in 2024, continues to drive substantial investments in advanced communication systems that utilize these connectors.

Modern military aircraft increasingly rely on fiber optic networks for their superior bandwidth and immunity to electromagnetic interference. For instance, next-generation fighter jets incorporate hundreds of fiber optic connections, each requiring robust circular connectors. The space sector is also emerging as a significant adopter, with connector requirements for satellite communications growing at over 6% annually. These applications demand connectors that can withstand radiation, extreme temperatures, and mechanical stress while maintaining signal integrity.

MARKET RESTRAINTS

High Installation and Maintenance Costs Limit Market Penetration

While circular fiber connectors offer superior performance, their adoption is hampered by significant installation and maintenance expenses. The specialized equipment and skilled labor required for proper installation can increase deployment costs by up to 40% compared to traditional copper connectors. This cost factor is particularly challenging in price-sensitive markets and developing regions where budget constraints often dictate technology choices.

The precision alignment required for optimal fiber connector performance demands specialized testing equipment and trained technicians. Many organizations find the total cost of ownership prohibitive, especially when considering the need for regular inspections and cleaning to maintain signal quality. These economic barriers slow adoption rates, particularly among small and medium-sized enterprises that lack the resources for substantial infrastructure investments.

Competition from Alternative Connectivity Solutions Presents Challenges

The market faces growing competition from emerging wireless technologies and alternative fiber connector designs. While circular connectors dominate rugged applications, rectangular fiber connectors are gaining traction in data center environments due to their higher port density. The development of advanced wireless solutions, including millimeter-wave technology, also threatens to displace fiber in certain applications where mobility is prioritized over ultimate bandwidth.

Moreover, the industry is witnessing a shift toward more compact form factors, with miniature circular connectors competing against the standard sizes. This fragmentation in product offerings creates confusion among end-users and complicates standardization efforts. The lack of universal standards for certain emerging applications forces manufacturers to develop application-specific solutions, increasing R&D costs and potentially limiting market scalability.

MARKET OPPORTUNITIES

Emerging 5G Infrastructure Deployment Creates Significant Growth Potential

The global rollout of 5G networks presents substantial opportunities for circular fiber connector manufacturers. As telecom operators worldwide invest heavily in next-generation infrastructure, the demand for robust connectivity solutions at cell sites and throughout the backhaul network is increasing dramatically. The small cell deployment alone is expected to require millions of fiber connections by 2032, many utilizing circular connectors for their reliability in outdoor environments.

5G’s stringent latency and bandwidth requirements make fiber optics the only viable medium for most connections beyond the final wireless hop. The enhanced performance characteristics of circular connectors – including their superior dust and moisture resistance – make them particularly suitable for the challenging environments where many 5G components are deployed. Industry projections suggest the 5G infrastructure market will generate over $12 billion in fiber optic component demand by 2030.

Industrial Automation and Smart Manufacturing Drive New Applications

The rapid advancement of Industry 4.0 technologies is creating new application areas for circular fiber connectors. Modern manufacturing facilities increasingly rely on fiber optic networks for their immunity to electromagnetic interference in electrically noisy environments. The industrial segment is projected to grow at over 5% CAGR through 2032 as factories adopt more connected automation systems.

Robotic systems, in particular, benefit from the lightweight and flexible nature of fiber optic cables with circular connectors. The ability to maintain signal integrity despite constant movement makes them ideal for robotic arms and automated guided vehicles. Emerging smart factory initiatives worldwide are expected to drive significant demand, with the industrial automation market projected to exceed $300 billion by 2030.

MARKET CHALLENGES

Precision Manufacturing Requirements Create Supply Chain Complexities

The production of high-quality circular fiber connectors demands extremely precise manufacturing processes and specialized materials. Maintaining micron-level tolerances for fiber alignment requires advanced machining capabilities and rigorous quality control measures. These technical requirements create significant barriers to entry and can lead to supply chain vulnerabilities when demand spikes occur.

The ceramic and specialized polymer materials used in ferrule manufacturing require careful handling and processing. Recent disruptions in the global supply of high-purity ceramics have highlighted the fragility of certain component supply chains. Manufacturers must maintain substantial inventories of these critical materials to ensure production continuity, increasing working capital requirements and potentially impacting profitability.

Field Installation Challenges Hinder Widespread Adoption

Despite technological advancements, field installation of circular fiber connectors remains technically challenging compared to traditional copper connections. The need for precise cleaving, polishing, and alignment requires trained personnel and specialized tools that are not always available at installation sites. These technical demands contribute to higher operational costs and can lead to inconsistent performance when installations are not performed correctly.

Environmental factors such as dust, moisture, and temperature extremes can complicate field terminations. Unlike factory-prepared connectors, field-installed versions often show higher insertion losses and greater variability in performance. The industry continues to work on more field-friendly termination techniques, but current methods still require substantial skill and care to achieve optimal results.

CIRCULAR FIBER CONNECTORS MARKET TRENDS

Industrial Automation and 5G Expansion to Drive Adoption of Circular Fiber Connectors

The demand for circular fiber connectors is increasing due to their robust design, which ensures reliable high-speed data transmission in harsh environments. Industries such as telecom, military, and aerospace are leveraging these connectors for secure and efficient fiber optic communication. With the global market for circular fiber connectors valued at approximately $185 million in 2024, growth is projected at a CAGR of 3.8% through 2032, reaching $239 million. This upward trend is fueled by the expansion of 5G networks, which require high-performance optical connectors to support ultra-low latency and high bandwidth applications, particularly in densely populated urban areas where signal reliability is critical.

Other Trends

Rising Defense and Aerospace Investments

Military and aerospace sectors are increasingly deploying circular fiber connectors for secure, high-speed communication in mission-critical systems. As defense budgets rise globally, particularly in the U.S. and China, investments in next-gen tactical networks and avionics are accelerating. The ruggedized nature of circular fiber connectors ensures durability under extreme conditions, making them indispensable in defense applications. Additionally, advancements in unmanned systems and satellite communications further drive adoption, reinforcing the demand for high-precision optical connectors.

Miniaturization and High-Density Connectivity Needs

The push for miniaturization in fiber optic components has led to the development of more compact yet resilient circular connectors, particularly in industries where space constraints are a challenge. The telecom sector, in particular, benefits from high-density configurations that allow for efficient cable management in data centers and network hubs. Innovations such as multi-fiber push-on (MPO) variations of circular connectors are gaining traction, offering improved scalability for infrastructure upgrades. Furthermore, the rise of IoT and Industry 4.0 has intensified the need for dependable fiber connectivity in automated manufacturing environments, where real-time data transfer is non-negotiable.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Leverage Innovation and Strategic Partnerships to Maintain Dominance

The global circular fiber connectors market features a moderately competitive landscape dominated by established players with strong technological capabilities. With the market projected to grow at 3.8% CAGR through 2032, companies are aggressively expanding their product portfolios through R&D investments and strategic acquisitions.

Amphenol Corporation and TE Connectivity currently lead the market, collectively accounting for over 30% of total revenue in 2024. Their dominance stems from comprehensive product offerings across multiple connector types (SC, LC, FC) and applications from telecom to aerospace. Both companies have recently introduced next-generation connectors with enhanced durability and signal integrity to address evolving industry needs.

Corning Incorporated maintains significant market share through its vertically integrated optical solutions. The company’s circular connectors benefit from proprietary glass technologies that enable superior performance in harsh environments. Meanwhile, Infinite Electronics has gained traction through its fast-shipping program for standard and custom connector solutions, particularly in North American markets.

Asian manufacturers like Yamaichi Electronics and Fujikura are emerging as formidable competitors, leveraging cost advantages and localized production to capture growing demand in the APAC region. Their expanding portfolios and partnerships with regional telecom providers are expected to drive significant market share gains by 2032.

List of Key Circular Fiber Connector Companies Profiled

- Amphenol Corporation (U.S.)

- TE Connectivity (Switzerland)

- Corning Incorporated (U.S.)

- Infinite Electronics (U.S.)

- Eaton Corporation (Ireland)

- Yamaichi Electronics (Germany)

- Fujikura Ltd. (Japan)

- ITT Cannon (U.S.)

- CommScope (U.S.)

Segment Analysis:

By Type

SC Connectors Lead the Market Owing to Widespread Adoption in Telecom and Data Centers

The Circular Fiber Connectors market is segmented based on connector types:

- SC connectors

- LC connectors

- FC connectors

- Others (including ST, MTP/MPO, etc.)

By Application

Telecom Sector Dominates Market Share Due to Expanding Fiber Optic Network Infrastructure

The application segments in the Circular Fiber Connectors market include:

- Telecom

- Broadcast

- Military

- Aerospace

- Others (including medical, industrial, etc.)

By End User

Enterprise Segment Shows Robust Growth Fueled by Increasing Data Center Deployments

The market segmentation by end users comprises:

- Telecom service providers

- Data centers

- Government & defense

- Enterprise networks

- Others

By Material

Metal-Bodied Connectors Preferred for Harsh Environment Applications

The material-based segmentation includes:

- Metal-bodied connectors

- Plastic-bodied connectors

- Hybrid-material connectors

Regional Analysis: Circular Fiber Connectors Market

Asia-Pacific

The Asia-Pacific region dominates the global Circular Fiber Connectors market, accounting for the largest share by volume and value. This leadership position is driven by rapid digital transformation, massive investments in 5G infrastructure, and expanding data center deployments across China, Japan, and India. China alone contributes over 40% of regional demand due to its aggressive fiber optic network expansions under national broadband initiatives. Japan and South Korea follow closely, with advanced telecom sectors demanding high-performance connectors for next-generation networks. While price sensitivity remains a challenge for premium products, increasing adoption in industrial automation and smart city projects continues to propel market growth across the region.

North America

North America represents the second-largest market for Circular Fiber Connectors, characterized by technological sophistication and stringent quality requirements. The United States leads regional demand, with major telecom operators investing billions in fiber-to-the-home (FTTH) rollouts and hyperscale data center construction. Military and aerospace applications contribute significantly to premium connector sales, driven by defense modernization programs. The region’s focus on ruggedized, high-reliability solutions for harsh environments creates opportunities for specialized manufacturers, though supply chain disruptions and trade restrictions occasionally challenge market stability.

Europe

Europe maintains steady demand for Circular Fiber Connectors, supported by comprehensive digital infrastructure policies and growing industrial IoT adoption. Germany and the UK lead in manufacturing automation applications, while France sees increasing deployments in broadcast and medical sectors. EU regulations promoting standardization and interoperability encourage innovation in connector designs, though the market faces pricing pressures from Asian competitors. The region’s emphasis on sustainability is gradually shifting preferences toward eco-friendly connector materials and packaging without compromising performance in critical telecommunications and transportation applications.

Middle East & Africa

The MEA region shows promising growth potential in the Circular Fiber Connectors market, particularly in Gulf Cooperation Council countries investing heavily in smart city projects and digital government initiatives. Fiber network expansions in urban centers drive demand, though market penetration remains limited by budget constraints in other areas. Israel emerges as a technology hub for specialized military-grade connectors, while African nations gradually upgrade legacy systems with improved fiber connectivity. Infrastructure challenges and import dependence currently restrict faster adoption, but long-term prospects appear strong with improving economic conditions.

South America

South America’s Circular Fiber Connectors market grows at a moderate pace, with Brazil and Argentina accounting for most regional demand. Telecom operators focus on network upgrades to support increasing mobile data consumption, though economic fluctuations periodically delay large-scale projects. The mining and energy sectors utilize rugged connectors in harsh environments, while government initiatives to expand broadband access create opportunities in underserved areas. Currency volatility and local manufacturing limitations keep the region dependent on imports, constraining more rapid market expansion despite clear infrastructure needs.

Report Scope

This market research report provides a comprehensive analysis of the global Circular Fiber Connectors market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Circular Fiber Connectors market was valued at USD 185 million in 2024 and is projected to reach USD 239 million by 2032, growing at a CAGR of 3.8%.

- Segmentation Analysis: Detailed breakdown by product type (SC, LC, FC, Others), application (Telecom, Broadcast, Military, Aerospace, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. market size is estimated at USD XX million in 2024, while China is projected to reach USD XX million.

- Competitive Landscape: Profiles of leading market participants including Infinite Electronics, Amphenol, Cinch Connectivity Solutions, Neutrik, Eaton, Yamaichi Electronics, Glenair, ITT Cannon, TE Connectivity, Corning, Fujikura, and CommScope, with their market share, product portfolios, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging connector technologies, miniaturization trends, and evolving industry standards for fiber optic connectivity.

- Market Drivers & Restraints: Evaluation of factors including 5G deployment, data center expansion, and military modernization programs driving growth, along with challenges in supply chain and raw material costs.

- Stakeholder Analysis: Strategic insights for component suppliers, OEMs, system integrators, and investors regarding market opportunities and competitive positioning.

The report employs primary and secondary research methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Circular Fiber Connectors Market?

-> Circular Fiber Connectors Market was valued at 185 million in 2024 and is projected to reach US$ 239 million by 2032, at a CAGR of 3.8% during the forecast period.

Which key companies operate in Global Circular Fiber Connectors Market?

-> Key players include Infinite Electronics, Amphenol, Cinch Connectivity Solutions, Neutrik, Eaton, Yamaichi Electronics, Glenair, ITT Cannon, TE Connectivity, and Corning.

What are the key growth drivers?

-> Key growth drivers include 5G network expansion, increasing data center deployments, rising demand for high-speed connectivity, and growing military and aerospace applications.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth due to telecom infrastructure development, while North America maintains significant market share.

What are the emerging trends?

-> Emerging trends include development of ruggedized connectors for harsh environments, miniaturization of components, and integration with IoT devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...