Chiplets for graph neural network training accelerator Market Insights

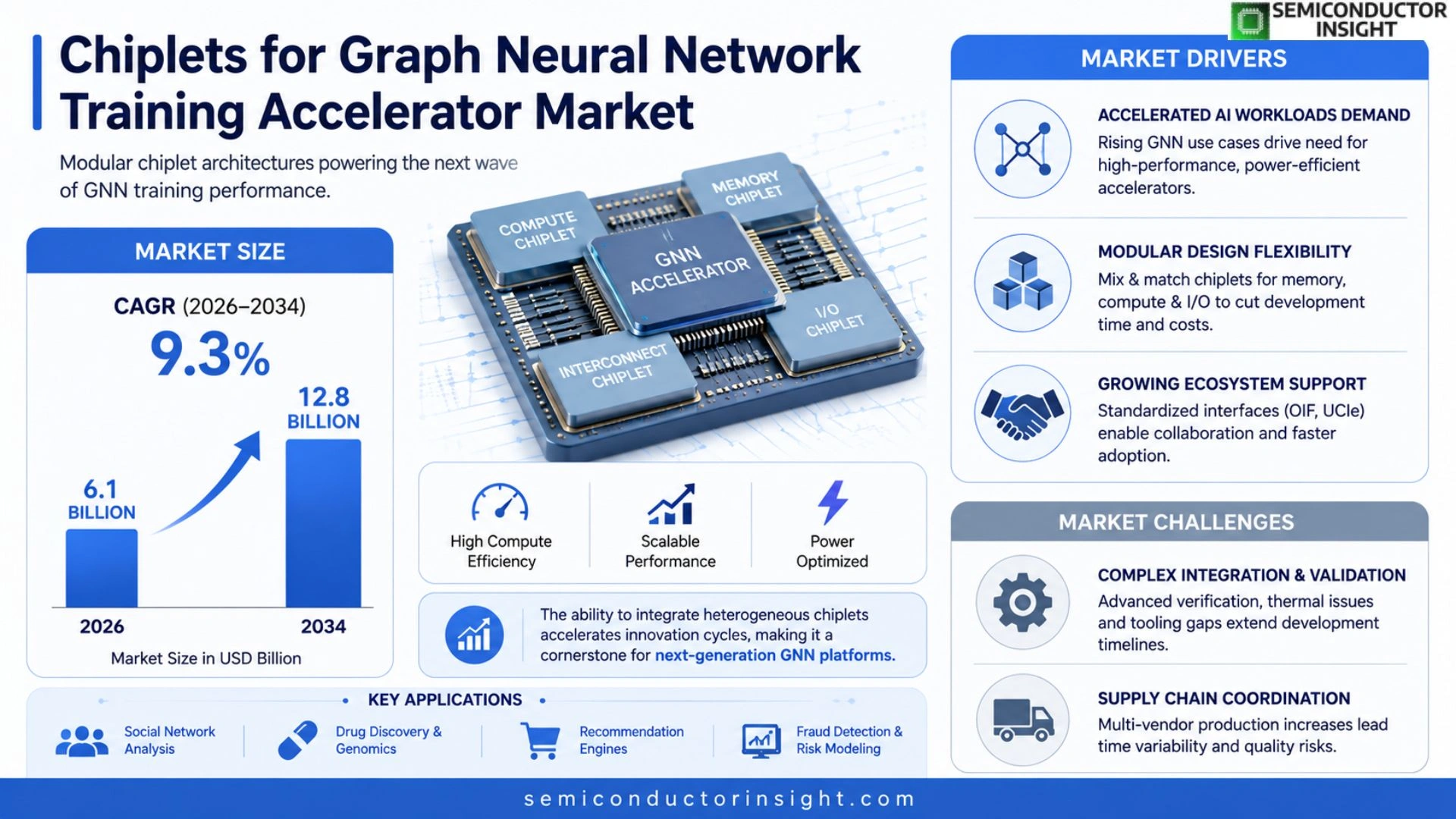

Global Chiplets for graph neural network training accelerator market size was valued at USD 5.3 billion in 2025. The market is projected to grow from USD 6.1 billion in 2026 to USD 12.8 billion by 2034, exhibiting a CAGR of 9.3% during the forecast period.

Chiplets are modular semiconductor building blocks that can be combined to form high‑performance accelerators tailored for graph neural network (GNN) workloads. By integrating specialized compute cores, high‑bandwidth interconnects and memory subsystems on a single package, these chiplets enable scalable training of large‑scale graphs while reducing power consumption and time‑to‑market.

The market is experiencing rapid expansion because AI‑driven applications such as drug discovery, fraud detection and recommendation systems increasingly rely on GNNs. Furthermore, rising venture capital funding for AI hardware startups and strategic alliances,e.g., Intel’s partnership with Graphcore announced in March 2024,are accelerating adoption. Key players including Intel, AMD, Nvidia, Samsung Electronics and Graphcore are actively developing next‑generation chiplet solutions to meet escalating demand.

MARKET DRIVERS

Accelerated AI Workloads Demand

The surge in graph neural network (GNN) applications across social network analysis, drug discovery, and recommendation engines is driving the need for specialized accelerators. Companies are increasingly turning to Chiplets for graph neural network training accelerator Market solutions to meet the high computational intensity while maintaining power efficiency.

Modular Design Flexibility

Chiplet‑based architectures enable modular scaling, allowing designers to mix and match functional blocks such as memory, compute, and interconnect units. This flexibility reduces time‑to‑market and lowers development costs, a critical advantage in the fast‑moving AI hardware sector.

➤ The ability to integrate heterogeneous chiplets accelerates innovation cycles, making it a cornerstone for next‑generation GNN training platforms.

Additionally, the growing ecosystem of standardized chiplet interfaces (e.g., OIF, UCIe) fosters broader industry collaboration, further reinforcing adoption trends in Chiplets for graph neural network training accelerator Market.

MARKET CHALLENGES

Complex Integration and Validation

Integrating multiple chiplets into a cohesive accelerator requires sophisticated design‑for‑test and verification methodologies. The lack of mature tooling can increase development risk and extend product timelines.

Thermal management also becomes more challenging as dense chiplet packs concentrate power density, necessitating advanced cooling solutions to maintain performance stability.

Other Challenges

Supply Chain Coordination

Coordinating production across multiple vendors introduces variability in lead times and quality assurance, potentially constraining large‑scale deployments.

MARKET RESTRAINTS

High Initial Capital Outlay

Investments in advanced packaging facilities and specialized testing equipment are required to support chiplet‑based designs, creating a financial barrier for smaller players.

Regulatory scrutiny over emerging AI hardware, particularly in safety‑critical domains, can slow adoption cycles and limit market expansion.

MARKET OPPORTUNITIES

Emerging Edge AI Deployments

Deploying GNN accelerators at the edge,such as in autonomous vehicles and IoT gateways,requires compact, power‑efficient solutions. Chiplet architectures provide the necessary scalability without compromising performance, creating a strong growth avenue.

Strategic partnerships between semiconductor foundries and AI software firms are fostering co‑design initiatives, enabling optimized chiplet stacks tailored for graph processing workloads.

Finally, the ongoing standardization of inter‑chip communication protocols opens new markets for interoperable chiplet ecosystems, positioning Chiplets for graph neural network training accelerator Market for sustained expansion.

Chiplets for graph neural network training accelerator Market Trends

Modular Chiplet Architecture Enables Scalable GNN Training

Chiplets for graph neural network training accelerator Market is being reshaped by a shift toward modular semiconductor building blocks. By assembling specialized compute cores, dedicated memory subsystems, and high‑bandwidth interconnects within a single package, designers can rapidly prototype accelerators that match the irregular data patterns of graph neural networks. This approach shortens development cycles, lowers power draw, and supports the expanding size of graph datasets used in drug discovery, fraud detection, and recommendation engines. Early adopters report up to a 30% reduction in training time compared with monolithic ASIC solutions, underscoring the competitive advantage of chiplet‑based designs.

Other Trends

Strategic Alliances Accelerate Ecosystem Growth

Collaboration between leading silicon vendors and AI‑focused startups is a defining factor for Chiplets for graph neural network training accelerator Market. Partnerships such as Intel’s alliance with Graphcore, announced in March 2024, combine Intel’s advanced packaging expertise with Graphcore’s graph‑optimized IP cores. Similar joint ventures among AMD, Nvidia, and Samsung Electronics are creating shared reference designs that simplify integration for downstream manufacturers. These alliances accelerate time‑to‑market for new chiplet solutions and foster a broader ecosystem of software tools, compiler support, and verification frameworks, which collectively reduce barriers for emerging AI hardware firms.

Emerging Applications Push Performance Boundaries

Beyond traditional AI workloads, Chiplets for graph neural network training accelerator Market is benefiting from the rise of edge‑centric analytics and real‑time knowledge graphs. Enterprises are deploying chiplet‑based accelerators in data‑center clusters to handle dynamic graph updates with millisecond latency, enabling use cases such as live cybersecurity threat mapping and adaptive recommendation pipelines. The need for higher throughput and lower latency drives continuous innovation in inter‑chiplet communication standards, prompting vendors to adopt silicon‑photonic links and advanced TSV technologies. As these performance demands solidify, the market is expected to sustain robust growth driven by tangible customer deployments rather than speculative forecasts.

COMPETITIVE LANDSCAPE

Key Industry Players

Chiplets for Graph Neural Network Training Accelerator Market Overview

The market is currently dominated by a handful of large semiconductor firms that integrate chiplet‑based architectures into their AI accelerator portfolios. Intel leads the space by leveraging its Advanced Packaging Roadmap and the recent Intel‑Graphcore partnership, which combines Intel’s silicon interconnect expertise with Graphcore’s IPU‑centric chiplet designs. Nvidia’s acquisition of Arm‑based chiplet assets and AMD’s 3D‑V-Cache strategy further intensify competition, as each player seeks to deliver higher bandwidth, lower latency inter‑chip communication crucial for large‑scale GNN training workloads. Samsung Electronics complements this tier with its advanced silicon‑on‑insulator (SOI) processes, offering high‑density, power‑efficient chiplets that are increasingly adopted in data‑center accelerators.

Beyond the tier‑one giants, a vibrant ecosystem of specialist vendors is shaping the niche segment of GNN‑focused chiplets. Graphcore continues to iterate its Bow IPU chiplets, emphasizing fine‑grained parallelism for graph workloads. Qualcomm’s AI‑focused Snapdragon platforms now incorporate modular compute tiles designed for heterogeneous AI tasks, while Xilinx (now part of AMD) supplies programmable logic chiplets that enable custom data‑flow pipelines. Emerging players such as Cerebras Systems, Tenstorrent, Marvell Technology, Broadcom, and Taiwan Semiconductor Manufacturing Co. (TSMC) contribute differentiated packaging, high‑bandwidth memory interfaces, and silicon‑photonic interconnects that address specific performance‑power trade‑offs demanded by next‑generation GNN training accelerators.

List of Key Chiplet Companies Profiled

- Intel Corporation

- Nvidia Corporation

- Advanced Micro Devices (AMD)

- Samsung Electronics

- Graphcore Ltd.

- Qualcomm Incorporated

- Xilinx Inc.

- Cerebras Systems

- Tenstorrent

- Marvell Technology Group Ltd.

- Broadcom Inc.

- TSMC (Taiwan Semiconductor Manufacturing Co.)

- Huawei Technologies Co., Ltd.

- IBM Research

- MediaTek Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Compute‑focused chiplets

|

| By Application |

|

Fraud detection

|

| By End User |

|

Cloud service providers

|

| By Architecture |

|

Heterogeneous multi‑chiplet systems

|

| By Deployment Model |

|

Managed AI platforms

|

Regional Analysis: North America

North America

The increasing complexity of graph neural networks and the limitations of monolithic chip designs are key drivers for the adoption of chiplets. The ability to integrate specialized chiplets for different functionalities – such as processing, memory, and interconnect – allows for optimized performance and power consumption.

Ongoing innovations in chiplet design, packaging technologies, and interconnect solutions are further boosting market growth. The development of advanced packaging techniques, such as 2.5D and 3D integration, enables higher density and faster communication between chiplets, crucial for efficient graph processing.

The North American market features a highly competitive landscape with established semiconductor companies and emerging chiplet specialists vying for market share. Strategic collaborations and partnerships between these players are instrumental in driving innovation and expanding market reach.

Key end-user industries driving demand include automotive (for autonomous driving systems), healthcare (for drug discovery and personalized medicine), and finance (for fraud detection and risk management). These sectors are increasingly relying on graph neural networks for their complex analytical needs.

Europe

The European market for chiplets in the graph neural network training accelerator sector is experiencing steady growth, driven by a strong emphasis on research and development and a growing AI ecosystem. Government initiatives and funding programs are supporting innovation in semiconductor technologies, particularly in areas related to high-performance computing. The focus is on developing energy-efficient solutions for AI applications, aligning with broader sustainability goals.

Asia-Pacific

Asia-Pacific represents a significant and rapidly expanding market. Countries like China, Japan, and South Korea are investing heavily in AI infrastructure and high-performance computing, creating substantial demand for chiplet-based solutions. The region’s robust manufacturing capabilities and strong electronics industries are also contributing to market growth.

South America

South America is an emerging market with potential for growth, although currently smaller compared to North America, Europe, and Asia-Pacific. Increasing adoption of AI in specific sectors like finance and logistics is expected to drive demand for more powerful computing architectures.

Middle East & Africa

The Middle East & Africa region is in the early stages of adoption but holds long-term growth potential. Investments in digital transformation and the development of AI capabilities are expected to stimulate demand for advanced computing solutions, including chiplets for graph neural network training.

Report Scope

This market research report provides a comprehensive analysis of the Chiplets for graph neural network training accelerator Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Chiplets for graph neural network training accelerator Market?

-> Chiplets for graph neural network training accelerator Market was valued at USD 5.3 billion in 2025 and is expected to reach USD 12.8 billion by 2034.

Which key companies operate in Chiplets for graph neural network training accelerator Market?

-> Key players include Intel, AMD, Nvidia, Samsung Electronics, and Graphcore, among others.

What are the key growth drivers?

-> Key growth drivers include rapid adoption of AI‑driven applications such as drug discovery, fraud detection and recommendation systems, increasing venture capital funding for AI hardware startups, and strategic alliances like Intel’s partnership with Graphcore.

Which region dominates the market?

-> The reference does not specify a single dominant region for this market.

What are the emerging trends?

-> Emerging trends include modular chiplet integration, high‑bandwidth interconnects, specialized compute cores for GNN workloads, and collaborative ecosystem development between semiconductor leaders and AI startups.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...