Chiplet-Based Semiconductor Market Insights

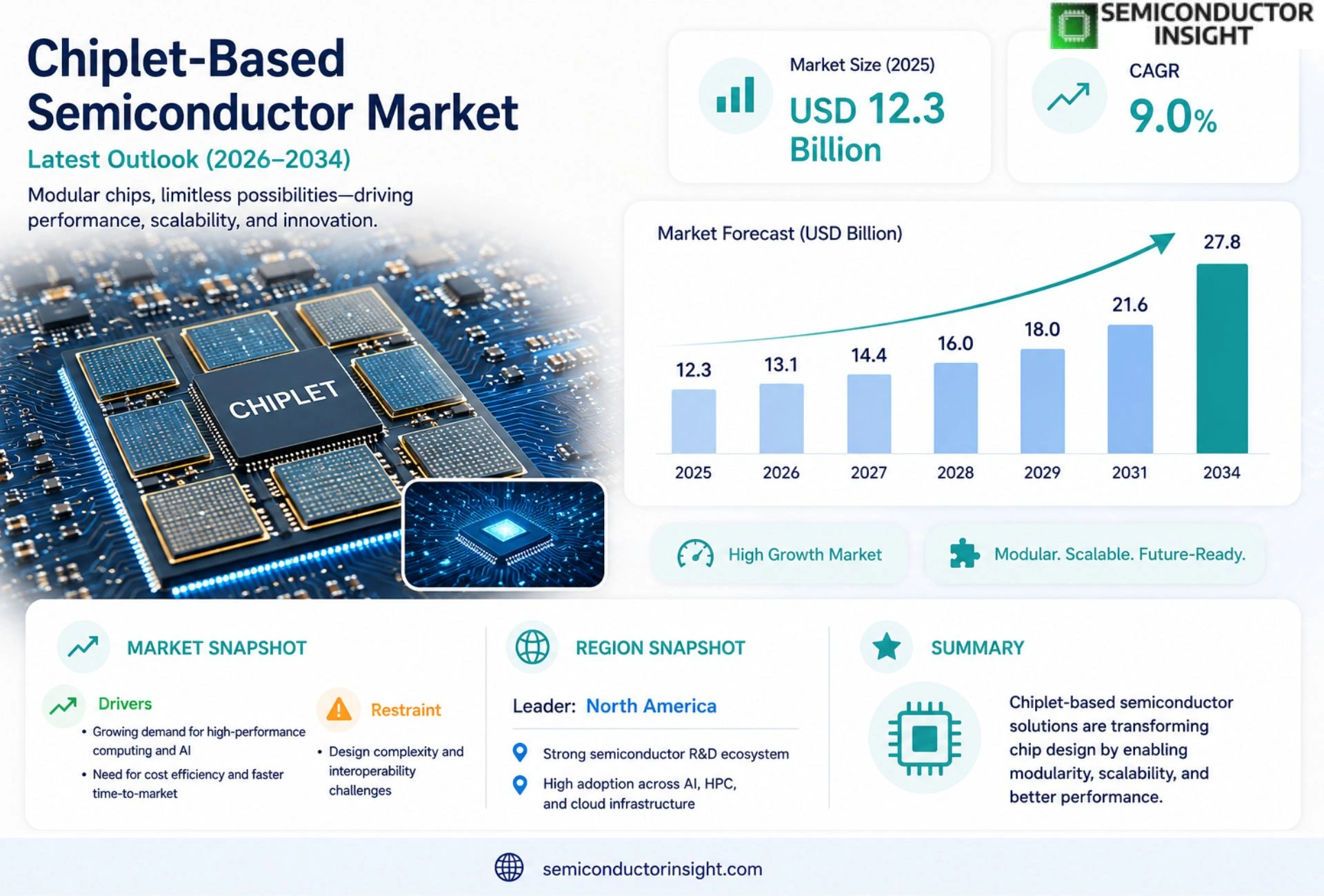

Global Chiplet-Based Semiconductor Market size was valued at USD 12.3 billion in 2025. The market is projected to grow from USD 13.1 billion in 2026 to USD 27.8 billion by 2034, exhibiting a CAGR of 9.0% during the forecast period.

Chiplets are modular silicon building blocks that can be assembled into heterogeneous system‑in‑package solutions, enabling designers to mix‑and‑match logic, memory, analog and RF functions while reducing time‑to‑market and development cost.

The market is experiencing rapid expansion due to surging demand for AI accelerators and high‑performance computing, although design complexity remains a challenge. Key players such as AMD (Infinity Fabric), Intel (Foveros), TSMC (CoWoS), Samsung (X‑Cube) and GlobalFoundries are accelerating adoption through strategic collaborations; for instance, AMD announced in March 2024 a joint development program with TSMC to advance advanced chiplet interconnect technologies.

MARKET DRIVERS

Scalable Architecture Adoption

Chiplet-Based Semiconductor Market is propelled by the ability of chiplets to enable highly modular designs, allowing manufacturers to mix and match functional blocks. This modularity supports rapid scaling of performance without redesigning the entire die, which is especially valuable for heterogeneous computing workloads.

Cost‑Efficiency and Time‑to‑Market

By reusing validated chiplet IP, companies reduce non‑recurring engineering costs and accelerate product introductions. The resulting cost efficiencies translate into more competitive pricing for end‑users, driving broader adoption across data‑center and consumer segments.

➤ Industry analysts note that the modular nature of chiplets shortens development cycles by up to several months, reshaping traditional semiconductor roadmaps.

Additionally, the ecosystem of standardized interconnects and packaging technologies reinforces confidence in chiplet solutions, reinforcing the growth trajectory of Chiplet‑Based Semiconductor Market.

MARKET CHALLENGES

Design Complexity Integration

Integrating multiple chiplets onto a single package introduces routing and timing challenges that require sophisticated design tools. Engineers must manage power distribution and signal integrity across heterogeneous building blocks, which can extend verification timelines.

Other Challenges

Supply Chain Constraints

The reliance on advanced packaging facilities creates bottlenecks, as capacity for high‑density interposers and fan‑out wafer‑level packaging is limited. These constraints can delay volume production and affect market momentum.

MARKET RESTRAINTS

Standardization Gaps

While progress has been made, the absence of universally accepted standards for chiplet interfaces hampers seamless integration across vendors. This fragmentation can discourage smaller players from committing to chiplet strategies, restraining overall market expansion.

MARKET OPPORTUNITIES

Emerging AI and Edge Computing Demands

AI accelerators and edge devices require highly customized compute blocks that benefit from chiplet modularity. As demand for low‑power, high‑performance AI inference grows, Chiplet‑Based Semiconductor Market is well positioned to deliver tailored solutions that meet these niche requirements.

Chiplet-Based Semiconductor Market Trends

AI‑Accelerated Growth as Primary Trend

In recent years, Chiplet-Based Semiconductor Market has been propelled by the escalating need for high‑performance computing platforms that support artificial‑intelligence workloads. Modular chiplet architectures enable designers to combine specialised cores, memory, and analog components in a single package, shortening time‑to‑market while containing development expenses. The flexibility of heterogeneous integration has become a decisive factor for manufacturers seeking to meet the performance targets of next‑generation data‑center and edge‑AI applications. Because chiplets can be sourced from multiple vendors, supply‑chain resilience improves, allowing OEMs to diversify sources without redesigning entire die footprints. Additionally, the ability to reuse proven building blocks reduces silicon risk and accelerates the rollout of new products in fast‑moving markets such as autonomous vehicles and 5G infrastructure.

Other Trends

Strategic Partnerships and Ecosystem Development

Leading companies such as AMD, Intel, TSMC, Samsung and GlobalFoundries are deepening collaboration to standardise interconnect protocols and co‑develop advanced packaging processes. For example, AMD announced a joint development program with TSMC in early 2024 to refine high‑density chiplet‑to‑chiplet communication, while Intel’s Foveros technology continues to expand its footprint across heterogeneous solutions. These alliances accelerate technology readiness and reduce risk for smaller design houses entering the space. Industry groups are also publishing open‑chiplet specifications that promote interoperability, enabling a broader ecosystem of IP providers and design‑tool vendors to contribute to a shared reference model.

Design Complexity Management as Emerging Concern

Although the benefits are clear, the rise of chiplet integration introduces design‑verification challenges, particularly in signal integrity and thermal management across mixed‑technology modules. Vendors are responding with sophisticated design‑automation tools and standardized test‑structures, yet the learning curve remains steep for teams transitioning from monolithic dies. Managing these complexities is becoming a focal point for future roadmap planning within the broader market. Companies are investing in modular verification frameworks that emulate real‑world operating conditions, and academic research is exploring AI‑assisted layout optimisation to mitigate timing closure issues. As designers gain experience, the industry expects a gradual reduction in time and cost penalties associated with chiplet‑level debugging.

COMPETITIVE LANDSCAPE

Key Industry Players

Chiplet‑Based Semiconductor Market: Competitive Landscape Overview

Chiplet ecosystem is anchored by a handful of vertically integrated leaders that shape design standards, supply‑chain logistics, and technology roadmaps. AMD’s Infinity Fabric and Intel’s Foveros platforms remain the most visible reference architectures, driving adoption through extensive software support and large‑scale volume manufacturing. TSMC’s CoWoS and Samsung’s X‑Cube services provide advanced interposer and package‑on‑package capabilities, enabling tier‑one OEMs to assemble heterogeneous substrates at wafer scale. GlobalFoundries contributes a differentiated node portfolio that reduces entry barriers for fabless innovators. Collectively, these players create a three‑tier structure—design IP providers, advanced packaging foundries, and system integrators—that accelerates time‑to‑market for AI accelerators and high‑performance computing solutions while preserving modularity and cost efficiency.

Beyond the core tier, a broad set of niche participants enriches the market with specialized IP, design‑for‑test solutions, and regional manufacturing capacity. Qualcomm leverages its Snapdragon‑based AI accelerators to showcase chiplet‑enabled heterogeneous integration for mobile and edge workloads. Broadcom and Marvell contribute high‑speed Ethernet and PCIe PHYs that are increasingly packaged as discrete chiplet blocks. NXP and Renesas focus on automotive and industrial microcontroller chiplets, aligning with safety‑critical standards. IBM’s research initiatives explore silicon‑photonic interconnects, while Arm supplies the ubiquitous CPU instruction set that underpins many chiplet designs. These companies, although not primary packagers, play crucial roles in expanding the ecosystem and fostering standards that lower design complexity across the value chain.

List of Key Chiplet-Based Semiconductor Companies Profiled

- AMD

- Intel

- TSMC

- Samsung Electronics

- GlobalFoundries

- Qualcomm

- Broadcom

- NXP Semiconductors

- Marvell Technology

- IBM

- Renesas Electronics

- Arm Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Logic Chiplets

|

| By Application |

|

AI Accelerators

|

| By End User |

|

Cloud Service Providers

|

| By Integration Technology |

|

2.5D Interposer

|

| By Market Driver |

|

Performance Scaling

|

Regional Analysis: North America

United States

The US boasts prominent design houses and research centers that are spearheading innovation in chiplet architectures and advanced packaging techniques. This concentrated talent pool fuels the development of next-generation semiconductor solutions.

Government programs and substantial private sector investments are accelerating the adoption of chiplet technologies and supporting the growth of the Chiplet-Based Semiconductor Market. Funding initiatives focus on bolstering domestic manufacturing capabilities and fostering technological advancements.

The US market for chiplets is particularly strong in sectors like high-performance computing, artificial intelligence, and defense applications, which demand cutting-edge semiconductor performance and reliability.

Efforts to strengthen and diversify the semiconductor supply chain within the US are directly impacting the growth of the Chiplet-Based Semiconductor Market, ensuring greater stability and reducing reliance on foreign sources.

Europe

Europe’s Chiplet-Based Semiconductor Market is witnessing increasing interest, particularly in areas like automotive electronics and industrial automation. Several European nations are actively fostering collaborations between research institutions and industry players to drive innovation in advanced packaging. While the region lags behind the US in terms of overall investment, a concerted effort towards strengthening domestic capabilities is gaining momentum. Focus areas include developing specialized chiplets for power management and connectivity, crucial for the evolving automotive landscape. The European Union’s strategic initiatives aim to reduce reliance on external suppliers and establish a more self-sufficient semiconductor ecosystem. This proactive approach is expected to unlock significant growth opportunities for the Chiplet-Based Semiconductor Market within Europe.

Asia-Pacific

Asia-Pacific represents the largest and fastest-growing market for the Chiplet-Based Semiconductor Market, driven primarily by the burgeoning electronics manufacturing hubs of China, Taiwan, and South Korea. The region’s strong consumer electronics sector and increasing demand for advanced computing solutions are fueling demand for chiplet-based architectures. Taiwan, in particular, is a dominant player in the development and manufacturing of advanced packaging technologies essential for chiplet integration. China’s substantial investments in domestic semiconductor manufacturing are also significantly impacting the Chiplet-Based Semiconductor Market in the region. The focus is on reducing dependence on foreign technologies and developing a comprehensive supply chain for chiplet-based solutions. The demand for high-performance computing and AI applications across Asia-Pacific further propels the growth of this market segment.

South America

The Chiplet-Based Semiconductor Market in South America is a nascent but promising area, primarily driven by the expansion of the telecommunications and industrial sectors. Increasing adoption of IoT devices and the growing demand for connected infrastructure are creating opportunities for chiplet-based solutions, particularly in areas requiring power efficiency and specialized functionality. While the market size is currently small compared to other regions, proactive investments in infrastructure and technological development are expected to drive future growth. The region’s focus on enhancing connectivity and digital transformation will be key drivers for the adoption of advanced semiconductor technologies, including chiplets.

Middle East & Africa

The Chiplet-Based Semiconductor Market in the Middle East & Africa is still in its early stages of development, but presents long-term growth potential. The increasing focus on digital transformation initiatives, particularly in sectors like government, healthcare, and energy, is creating demand for advanced semiconductor solutions. The expansion of data centers and the growth of the IoT sector are expected to drive adoption of chiplet-based architectures in the coming years. While investment in semiconductor manufacturing is limited in the region, opportunities exist for specialized applications and the deployment of chiplet-based solutions in niche markets.

Report Scope

This market research report provides a comprehensive analysis of the Chiplet-Based Semiconductor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end‑user industry to identify high‑growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa, including country‑level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market‑entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real‑time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Chiplet-Based Semiconductor Market?

-> Chiplet-Based Semiconductor Market size was valued at USD 12.3 billion in 2025. The market is projected to grow from USD 13.1 billion in 2026 to USD 27.8 billion by 2034.

Which key companies operate in Chiplet-Based Semiconductor Market?

-> Key players include AMD, Intel, TSMC, Samsung, and GlobalFoundries, among others.

What are the key growth drivers?

-> Key growth drivers include surging demand for AI accelerators and high‑performance computing workloads, which are fueling adoption of heterogeneous chiplet architectures.

Which region dominates the market?

-> Adoption is strongest in North America and Asia‑Pacific, where leading semiconductor fabs and system integrators are driving commercialization.

What are the emerging trends?

-> Emerging trends include heterogeneous integration via advanced chiplet interconnects, strategic collaborations among leading vendors, and increased use of AI‑assisted design methodologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...