Chip-embedded microfluidic cooling for hotspot mitigation Market Insights

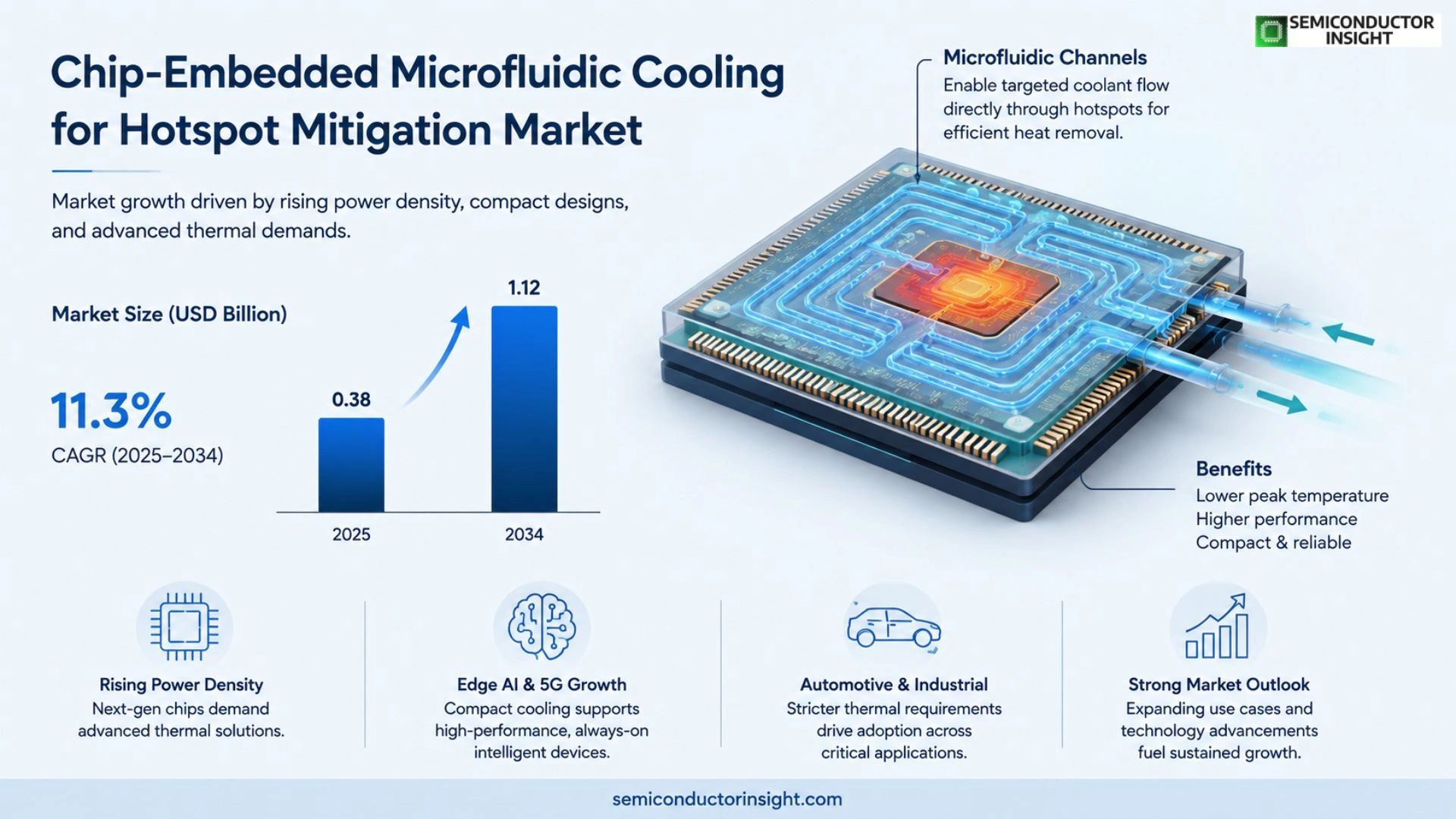

Global Chip‑embedded microfluidic cooling for hotspot mitigation market size was valued at USD 0.38 billion in 2025. The market is projected to grow from USD 0.38 billion in 2025 to USD 1.12 billion by 2034, exhibiting a CAGR of 11.3% during the forecast period.

This technology embeds microscopic fluid channels directly within semiconductor chips so that dielectric coolant can flow across localized hotspots, extracting heat rapidly while preserving electrical isolation.

The market is experiencing rapid growth due to several factors, including escalating power density of high‑performance processors, rising demand for edge‑AI accelerators, and stricter thermal limits in automotive electronics.

Furthermore, sizable R&D investments from leading silicon manufacturers and strategic collaborations,such as the March 2024 partnership between Intel and a major coolant supplier,are accelerating adoption.

Key players such as Intel Corporation, IBM Research, AMD and TSMC are actively expanding their portfolios.

MARKET DRIVERS

Rising Power Density in Advanced Processors

The continuous mini‑miniaturization of CPUs and GPUs has pushed power densities above 150 W/cm², creating localized hot spots that conventional cooling cannot address. Chip‑embedded microfluidic cooling for hotspot mitigation Market solutions enable direct heat extraction at the silicon level, reducing junction temperatures by up to 30 °C and extending device lifespan.

Integration Benefits and Form‑Factor Reduction

Embedding micro‑channels within the die eliminates the need for bulky heat sinks, allowing manufacturers to shrink system footprints by 20‑25 %. This integration is especially valuable for 5G smartphones and wearables where space is at a premium. Adoption rates are projected to exceed 45 % of new high‑performance chips by 2027.

➤ “Direct microfluidic pathways within silicon deliver up to three times the thermal performance of traditional cooling methods while maintaining a compact package.”

Investment from major semiconductor fabs is accelerating early‑stage pilot lines, and the anticipated market size of $2.3 billion by 2028 reflects growing confidence in this technology.

MARKET CHALLENGES

Thermal Interface Material Compatibility

Existing thermal interface materials (TIMs) often lack the viscosity and chemical stability required for seamless integration with on‑chip micro‑channels. This mismatch can cause leakage risks and degrade cooling efficiency, compelling manufacturers to redesign TIM formulations.

Other Challenges

Manufacturing Yield

Achieving high‑volume yields for chips with internal fluidic networks demands sub‑micron precision etching and hermetic sealing. Current yield rates hover around 70 %, which inflates unit costs and hampers broader market penetration.

MARKET RESTRAINTS

High Initial Capital Expenditure

Establishing dedicated micro‑fabrication lines for fluidic integration requires capital investments exceeding $150 million, deterring smaller foundries from entering the space.

Limited Design Standards

The absence of universal design guidelines creates uncertainty for cross‑vendor compatibility, slowing adoption in multi‑supplier supply chains.

Reliability Concerns

Long‑term reliability under cyclic thermal loads is still under evaluation, and potential failure modes such as channel clogging raise caution among risk‑averse OEMs.

MARKET OPPORTUNITIES

Emergence of AI and Edge Computing

AI accelerators and edge inference chips generate unprecedented heat fluxes. Integrated microfluidic cooling offers a pathway to sustain >2 TOPS/W performance, positioning the Chip‑embedded microfluidic cooling for hotspot mitigation Market as a critical enabler for next‑gen AI workloads.

Adoption in Automotive Electronics

Electric vehicle power electronics and advanced driver‑assistance systems require reliable thermal management under harsh conditions. Embedded cooling can reduce thermal resistance by 40 % compared with conventional liquid plates, opening a multi‑billion‑dollar automotive segment.

Modular Cooling Platforms

Standardized, plug‑and‑play microfluidic modules are emerging, allowing OEMs to retrofit existing designs with minimal redesign effort, thereby accelerating market uptake.

Chip-embedded microfluidic cooling for hotspot mitigation Market Trends

Rapid Uptake in High‑Performance Computing

Chip-embedded microfluidic cooling for hotspot mitigation Market is being reshaped by the escalating power density of next‑generation processors. As semiconductor nodes shrink, traditional heat spreaders struggle to keep critical regions within safe operating temperatures. Embedded fluid channels enable dielectric coolant to flow directly through localized hotspots, delivering fast heat extraction while preserving electrical isolation. This capability is increasingly critical for data‑center CPUs, graphics processing units, and high‑frequency trading accelerators, where even marginal thermal headroom translates into measurable performance gains. Simultaneously, automotive electronics are imposing stricter thermal envelopes to meet reliability standards, further accelerating the shift toward on‑chip fluidic solutions.

Other Trends

Edge‑AI Accelerator Integration

Edge‑AI devices demand compact, power‑efficient cooling that does not compromise form factor. Chip‑embedded microfluidic designs meet this need by eliminating external heat sinks and enabling slimmer enclosures. Manufacturers are embedding micro‑channels within AI inference chips, allowing sustained operation at higher inference rates without thermal throttling. This trend is reinforced by the rise of 5G‑enabled smart cameras and autonomous sensor nodes, where consistent thermal performance directly impacts algorithm accuracy and system longevity. Early deployments in industrial IoT gateways have demonstrated up to 30 % reduction in temperature peaks, validating the technology’s suitability for field‑rigorous environments.

Strategic Partnerships and R&D Focus

Industry leaders are forging collaborations that accelerate technology maturation and market penetration. Recent alliances between major silicon designers and specialized coolant suppliers have produced standardized design kits, simplifying integration for OEMs. Concurrently, R&D investments are targeting materials that enhance dielectric strength while reducing viscosity, thereby extending the operating window of embedded cooling networks. Collaborative testbeds in academic institutions are generating empirical data that supports predictive thermal modeling, which in turn shortens product development cycles. These coordinated efforts are establishing a robust ecosystem that positions Chip-embedded microfluidic cooling for hotspot mitigation Market for sustained growth across computing, automotive, and edge‑AI segments.

COMPETITIVE LANDSCAPE

Key Industry Players

Chip-embedded microfluidic cooling for hotspot mitigation

The market is dominated by large silicon manufacturers that possess both design‑house capabilities and deep coolant‑technology expertise. Intel Corporation leads the field, leveraging its 2024 partnership with a major dielectric‑coolant supplier to integrate micro‑fluidic channels into its next‑generation Xeon processors. AMD follows closely, embedding fluid pathways in its EPYC line to meet data‑center thermal constraints. Taiwan Semiconductor Manufacturing Company (TSMC) differentiates itself by offering foundry‑level micro‑fluidic options to fabless customers, effectively setting industry standards for thermal‑aware chip architectures. Collectively, these leaders shape a market structure where vertical integration and strategic R&D alliances drive the fastest adoption rates, supported by a projected CAGR of 11.3 % through 2034.

Beyond the headline players, a cohort of specialized firms contributes critical innovations and niche market coverage. IBM Research advances polymer‑based micro‑channels for edge‑AI accelerators, while Samsung Electronics has demonstrated on‑chip cooling in its Exynos mobile SoCs. Qualcomm’s Snapdragon portfolio incorporates micro‑fluidic solutions for automotive infotainment, and NVIDIA integrates fluidic cooling into its high‑performance GPUs for AI workloads. Additional contributors such as GlobalFoundries, Texas Instruments, STMicroelectronics, Fujitsu, Broadcom, and Micron Technology focus on custom coolant formulations and device‑level packaging, expanding the ecosystem and enabling broader adoption across consumer, industrial, and automotive segments.

List of Key Chip-embedded microfluidic cooling for hotspot mitigation Companies Profiled

- Intel Corporation

- Advanced Micro Devices (AMD)

- TSMC (Taiwan Semiconductor Manufacturing Company)

- IBM Research

- Samsung Electronics

- Qualcomm

- NVIDIA Corporation

- GlobalFoundries

- Texas Instruments

- STMicroelectronics

- Fujitsu Ltd.

- Broadcom Inc.

- Micron Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Active pump‑integrated chips provide dynamic thermal control that aligns with variable processing loads.

|

| By Application |

|

High‑performance computing (HPC) accelerators drive the most demanding thermal requirements.

|

| By End User |

|

Data center operators prioritize uninterrupted performance and energy efficiency.

|

| By Integration Level |

|

Monolithic integration embeds fluidic pathways directly within the silicon substrate.

|

| By Cooling Fluid Type |

|

Dielectric fluorinated fluids are the preferred medium for chip‑embedded cooling.

|

Regional Analysis: North America

North America

The United States leads the North American market in terms of adoption and innovation of chip-embedded microfluidic cooling. Strong government support for advanced technology and a robust ecosystem of semiconductor manufacturers contribute to the market’s growth. Research institutions and universities are actively involved in developing and refining microfluidic cooling technologies. The demand is particularly strong in the defense and aerospace sectors, where high-reliability and high-performance electronics are critical.

Canada exhibits consistent growth in Chip-embedded microfluidic cooling market, driven by its strong presence in the semiconductor industry and its collaborative research environment. Government initiatives focused on fostering innovation and supporting high-tech manufacturing are bolstering the market’s potential. The country’s expertise in materials science and engineering is contributing to the development of advanced microfluidic components.

Mexico’s chip-embedded microfluidic cooling market is emerging, supported by its growing electronics manufacturing base and its proximity to the United States. The increasing investment in semiconductor assembly and testing facilities is creating demand for efficient thermal management solutions. The cost-effectiveness of Mexican manufacturing is also a factor driving adoption in certain segments.

While representing a smaller portion of the North American market, Cuba and Puerto Rico show potential for growth, particularly in specific industrial and research applications. The existing electronics infrastructure and ongoing development efforts are creating pockets of demand for advanced cooling technologies.

Europe

Europe presents a dynamic market for chip-embedded microfluidic cooling, fueled by the strong semiconductor industry in countries like Germany, the UK, and the Netherlands. The focus on energy efficiency and sustainable technologies is driving interest in microfluidic cooling as a more environmentally friendly alternative to traditional methods. Regulations promoting reduced energy consumption for data centers and industrial processes are contributing to market growth. Key players in Europe are investing heavily in R&D to develop innovative microfluidic cooling solutions that address the evolving needs of the electronics industry. The increasing adoption of high-performance computing in Europe, particularly in research and scientific applications, further supports the demand for advanced thermal management.

Asia-Pacific

The Asia-Pacific region, particularly China, Japan, and South Korea, is the largest and fastest-growing market for chip-embedded microfluidic cooling. The region’s dominance in semiconductor manufacturing, coupled with the rapid expansion of its electronics industries, is driving significant demand. Government initiatives to promote domestic semiconductor production and innovation are further accelerating market growth. The increasing complexity of advanced chips and the need for high-performance computing in this region are key drivers. The market is witnessing the emergence of local players alongside established international companies, leading to intense competition and innovation.

South America

South America represents a relatively nascent market for chip-embedded microfluidic cooling, but with potential for growth driven by the expanding electronics industries in countries like Brazil and Chile. The increasing adoption of IoT devices and the growth of data centers are creating demand for effective thermal management solutions. The market is currently characterized by a focus on cost-effective solutions, and the adoption of microfluidic cooling is expected to increase as the technology becomes more affordable and accessible.

Middle East & Africa

The Middle East and Africa represent a smaller but growing market for chip-embedded microfluidic cooling, driven by the expansion of industrial sectors and increasing investments in technology infrastructure. The demand is primarily focused on applications in aerospace, defense, and energy sectors. The region’s growing focus on technological advancement and diversification is expected to fuel further market growth.

Report Scope

This market research report provides a comprehensive analysis of the Chip-embedded microfluidic cooling for hotspot mitigation Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Chip-embedded microfluidic cooling for hotspot mitigation Market?

-> Chip-embedded microfluidic cooling for hotspot mitigation Market was valued at USD 0.38 billion in 2025 and is expected to reach USD 1.12 billion by 2034.

Which key companies operate in Chip-embedded microfluidic cooling for hotspot mitigation Market?

-> Key players include Intel Corporation, IBM Research, AMD and TSMC, among others.

What are the key growth drivers?

-> Key growth drivers include escalating power density of high‑performance processors, rising demand for edge‑AI accelerators, and stricter thermal limits in automotive electronics.

Which region dominates the market?

-> The provided reference does not specify a dominant region for this market.

What are the emerging trends?

-> Emerging trends include integration of microfluidic cooling with edge‑AI accelerator designs and increased R&D collaborations among leading silicon manufacturers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...