MARKET INSIGHTS

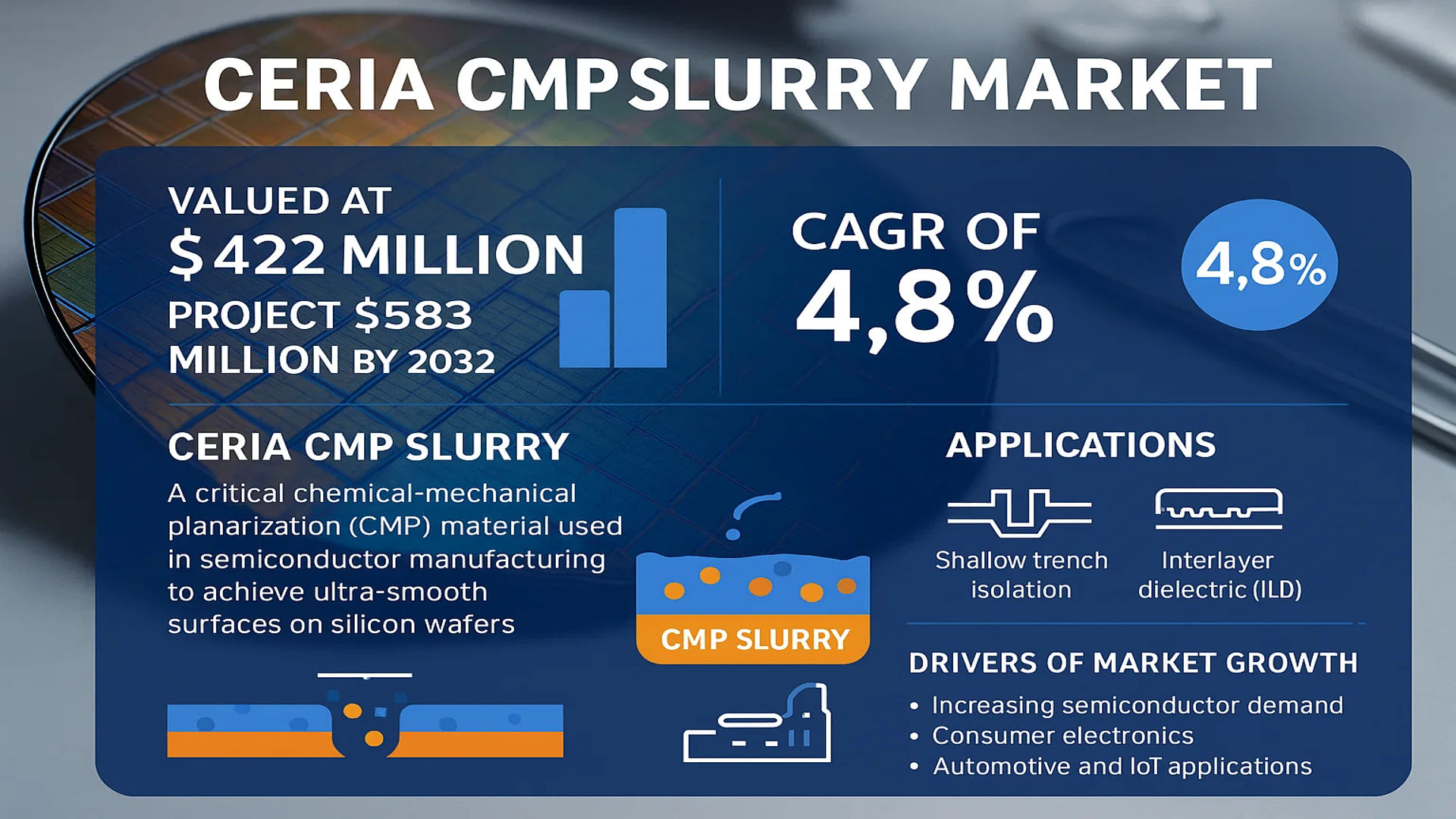

The global Ceria CMP Slurry Market was valued at 422 million in 2024 and is projected to reach US$ 583 million by 2032, at a CAGR of 4.8% during the forecast period.

Ceria CMP Slurry is a critical chemical-mechanical planarization (CMP) material used in semiconductor manufacturing to achieve ultra-smooth surfaces on silicon wafers. These slurries utilize cerium oxide (ceria) particles suspended in a chemical solution to remove material through both abrasive and chemical action during IC fabrication. The technology is particularly dominant in shallow trench isolation (STI) and interlayer dielectric (ILD) applications, where precise planarization is essential for multi-layer chip architectures.

Market growth is driven by increasing semiconductor demand across consumer electronics, automotive, and IoT applications, coupled with the transition to smaller node sizes requiring advanced planarization solutions. However, the industry faces challenges from alternative slurry technologies and the need for continuous particle size optimization. The market remains highly concentrated, with the top five players including Resonac, Merck KGaA (Versum Materials), and AGC collectively holding over 85% market share. Geographically, production is dominated by the United States (38% share), followed by Taiwan, Japan, and South Korea.

MARKET DYNAMICS

MARKET DRIVERS

Growing Semiconductor Industry to Propel Demand for Ceria CMP Slurry

The semiconductor industry’s rapid expansion is a primary driver for the ceria CMP slurry market. With the increasing demand for smaller, faster, and more efficient electronic devices, semiconductor manufacturers are investing heavily in advanced fabrication technologies. Ceria-based slurries provide superior planarization performance for critical applications like shallow trench isolation (STI) and inter-layer dielectrics (ILD). The semiconductor market is projected to exceed $800 billion by 2030, with foundries accelerating capacity expansions to meet this demand.

Advancements in IC Manufacturing Technology to Boost Market Growth

Technological advancements in integrated circuit manufacturing are creating significant opportunities for ceria CMP slurry providers. As nodes shrink below 7nm, the need for precision planarization increases dramatically. Ceria slurries offer exceptional selectivity and removal rate control, making them indispensable for advanced node fabrication. Leading players are investing in next-generation slurry formulations to meet the exacting requirements of 3D NAND and FinFET technologies.

Major semiconductor manufacturers are also expanding their production capacities globally. For instance, several multi-billion dollar fab projects are currently underway in Asia and North America, which will significantly increase slurry consumption in the coming years.

MARKET RESTRAINTS

Fluctuating Rare Earth Metal Prices to Challenge Market Stability

The ceria CMP slurry market faces significant challenges due to the volatility of rare earth metal prices. Cerium oxide, the primary raw material, is subject to price fluctuations influenced by geopolitical factors and supply chain disruptions. This unpredictability makes cost management difficult for both suppliers and end-users, potentially slowing market growth.

Additionally, environmental concerns surrounding rare earth mining may lead to stricter regulations, further complicating the supply situation. Some manufacturers are exploring alternative materials, though ceria remains the preferred choice for critical applications due to its superior performance characteristics.

MARKET CHALLENGES

Technical Complexity in Slurry Formulation to Hinder Market Expansion

Developing high-performance ceria CMP slurries involves significant technical challenges. Achieving the optimal balance between removal rate, selectivity, and surface quality requires specialized knowledge and precise control over particle size distribution and chemical composition. The increasing complexity of semiconductor devices demands even more sophisticated slurry formulations, creating barriers for new market entrants.

Other Challenges

Supply Chain Vulnerabilities

The concentrated nature of ceria slurry production, with over 85% market share held by just five companies, creates potential supply chain risks. Any disruption among key suppliers could significantly impact semiconductor production worldwide.

Performance Consistency Requirements

Semiconductor manufacturers demand extremely tight specifications for slurry performance, with minimal batch-to-batch variation. Maintaining this level of consistency at scale represents an ongoing challenge for suppliers.

MARKET OPPORTUNITIES

Emerging Applications in Advanced Packaging to Create New Growth Avenues

The growth of advanced packaging technologies such as 2.5D/3D IC packaging and fan-out wafer-level packaging presents significant opportunities for ceria CMP slurry providers. These packaging approaches require precise planarization of multiple material layers, where ceria slurries can provide distinct advantages. The advanced packaging market is projected to grow at over 8% annually through 2030.

Regional Capacity Expansions to Drive Localized Demand

Government initiatives to strengthen domestic semiconductor manufacturing capabilities in various regions are creating new opportunities. Major chipmakers are establishing production facilities in previously underserved markets, necessitating the development of localized supply chains for critical materials like ceria CMP slurries.

Several countries have announced substantial investments in semiconductor manufacturing as part of national industrial strategies, with some programs committing tens of billions of dollars to build domestic capacity over the next decade.

CERIA CMP SLURRY MARKET TRENDS

Expansion in Semiconductor Industry Fuels Market Demand

The increasing demand for advanced semiconductor devices, particularly in applications such as memory chips, logic devices, and microprocessors, has been the primary driver for the Ceria CMP Slurry market. As semiconductor nodes shrink to 5nm and below, the need for ultra-precise planarization has intensified, positioning ceria-based slurries as a critical material in shallow trench isolation (STI) and interlayer dielectric (ILD) CMP processes. The global semiconductor industry’s revenue exceeded $600 billion in 2024, a clear indicator of the underlying demand for high-performance CMP slurries. Manufacturers are now prioritizing low-defect slurries with tighter particle size distribution to meet the stringent requirements of next-generation chip manufacturing.

Other Trends

Preference for Colloidal Ceria Slurries

Colloidal ceria slurries are gaining prominence due to their superior polishing uniformity and reduced defectivity compared to calcined variants. These slurries exhibit better dispersion stability and controlled chemical reactivity, making them ideal for advanced semiconductor applications. The colloidal ceria segment accounted for over 60% of the market share in 2024, driven by their adoption in both legacy and cutting-edge fabrication processes. Ongoing improvements in nanoparticle synthesis techniques are further enhancing the performance characteristics of these slurries.

Regional Market Dynamics and Growth Opportunities

Asia-Pacific remains the dominant region in the Ceria CMP Slurry market, primarily due to the high concentration of semiconductor fabs in South Korea, Taiwan, and China. Taiwan alone contributed nearly 30% of the global production capacity in 2024, supported by leading foundries like TSMC. Meanwhile, North America remains a key player in slurry development, with companies such as Versum Materials and Ferro driving innovations. Europe, though smaller in market share, is witnessing steady growth, propelled by investments in electric vehicle semiconductors and IoT devices that require precision CMP solutions.

Sustainability and Material Efficiency in CMP Processes

Sustainability concerns are reshaping CMP slurry formulations, with manufacturers focusing on reducing waste and improving recyclability. Advanced filtration techniques and closed-loop slurry recycling systems are being tested to minimize environmental impact. Additionally, there is a growing emphasis on developing low-consumption slurries that maintain performance while reducing chemical usage by 15-20%. The industry is also exploring bio-based dispersion agents to enhance green chemistry compliance without compromising planarization efficiency.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Focus on Technological Innovation and Regional Expansion

The global Ceria CMP Slurry market exhibits a highly concentrated competitive structure, with the top five companies collectively holding over 85% market share in 2024. This dominance stems from the specialized nature of CMP slurry manufacturing and the significant technological barriers to entry in this space. Resonac, the market leader, has cemented its position through superior product formulations and strategic partnerships with semiconductor manufacturers across Asia and North America.

Merck KGaA (Versum Materials) follows closely, leveraging its expertise in advanced materials science to develop high-performance slurry formulations. The company’s recent investments in colloidal ceria slurry technology have significantly improved planarization efficiency for sub-7nm chip manufacturing processes. Meanwhile, AGC has capitalized on its strong foothold in the Japanese and South Korean markets, where it supplies over 60% of local semiconductor manufacturers.

Market dynamics show increasing competition from emerging Asian players, particularly KC Tech and Dongjin Semichem, who are gaining traction through cost-competitive offerings. These companies are investing heavily in R&D to challenge the technological dominance of established players, with several patent filings in nanoparticle dispersion technology reported in 2023-2024.

The competitive intensity is further amplified by recent vertical integration strategies, where major slurry manufacturers are acquiring upstream rare earth processing capabilities to secure raw material supply. Saint-Gobain’s 2023 acquisition of a ceria powder production facility in Vietnam exemplifies this trend, enabling better control over supply chain costs and quality.

List of Key Ceria CMP Slurry Manufacturers

- Resonac (Japan)

- Merck KGaA (Versum Materials) (Germany)

- AGC (Japan)

- KC Tech (South Korea)

- Anjimirco Shanghai (China)

- Soulbrain (South Korea)

- Dongjin Semichem (South Korea)

- SKC (South Korea)

- Saint-Gobain (France)

- Ferro (UWiZ Technology) (USA)

Segment Analysis

By Product Type

Colloidal Ceria Slurry Holds Major Market Share Due to Superior Planarization Performance in IC Manufacturing

The market is segmented based on product type into:

- Calcined Ceria Slurry

- Colloidal Ceria Slurry

By Application

STI/ILD CMP Application Dominates the Market Owing to Widespread Use in Semiconductor Fabrication

The market is segmented based on application into:

- STI/ILD CMP

- Others (Filter)

By Particle Size

Fine Particle Ceria Slurries Gain Traction for High-Precision Polishing Applications

The market is segmented based on particle size into:

- Fine particle slurries (<100nm)

- Medium particle slurries (100-500nm)

- Coarse particle slurries (>500nm)

By End-Use Industry

Semiconductor Industry Accounts for Largest Demand Due to Expanding Wafer Fabrication Facilities

The market is segmented based on end-use industry into:

- Semiconductors

- Optoelectronics

- Memory Devices

- Others

Regional Analysis: Ceria CMP Slurry Market

Asia-Pacific

The Asia-Pacific region dominates the global Ceria CMP Slurry market, accounting for over 60% of total production and consumption. This leadership position stems from the concentration of semiconductor manufacturing hubs in countries like Taiwan, South Korea, Japan, and China. Taiwan alone contributes approximately 28% of global production, home to key players like AGC and KC Tech. The region’s growth is propelled by massive investments in semiconductor fabrication plants (fabs) and the presence of leading foundries such as TSMC and Samsung. However, geopolitical tensions and trade restrictions present challenges for supply chain stability. Recent capacity expansions by semiconductor manufacturers are driving demand for high-purity colloidal ceria slurries for advanced node IC manufacturing.

North America

North America represents a technologically advanced market, with the United States contributing about 38% of global production. The region benefits from strong R&D capabilities in slurry formulation and the presence of major manufacturers including Merck KGaA (Versum Materials) and Ferro. The CHIPS and Science Act’s $52 billion investment in domestic semiconductor production is expected to boost demand for localized CMP slurry supply. While calcined ceria slurries remain prevalent for legacy nodes, manufacturers are transitioning toward colloidal slurries to meet the requirements of sub-7nm processes. Intellectual property protection and stringent quality standards create both opportunities and barriers for market entrants in this region.

Europe

Europe maintains a specialized position in the Ceria CMP Slurry market, focusing on high-value applications and sustainable production methods. EU environmental regulations under REACH influence slurry formulations, driving innovation in eco-friendly chemistries. While production capacity is limited compared to Asia and North America, companies like Merck KGaA and Saint-Gobain maintain advanced R&D facilities developing next-generation slurries. The region shows growing demand from automotive semiconductor manufacturers, particularly for power devices requiring specialized CMP solutions. However, the lack of major foundry operations limits volume growth potential compared to other regions.

Middle East & Africa

This emerging region shows nascent potential for Ceria CMP Slurry adoption, particularly in Israel and the UAE where semiconductor-related investments are increasing. The market remains dependent on imports from established production hubs, with limited local manufacturing capabilities. Efforts to diversify economies beyond oil are creating opportunities for technology sector growth, though high infrastructure costs and lack of technical expertise remain barriers. Some investments in semiconductor test and packaging facilities could generate demand for basic CMP slurry products in the medium term.

South America

South America represents the smallest market for Ceria CMP Slurries, characterized by minimal semiconductor manufacturing presence. Brazil shows some activity in electronics assembly, creating limited demand for basic CMP formulations. The region is likely to remain dependent on imports from North America and Asia for the foreseeable future. Economic volatility and lack of technology investment incentives hinder market development, though some local research institutions are exploring specialty material applications for niche markets.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Ceria CMP Slurry markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Ceria CMP Slurry market was valued at USD 422 million in 2024 and is projected to reach USD 583 million by 2032, at a CAGR of 4.8%.

- Segmentation Analysis: Detailed breakdown by product type (calcined ceria slurry, colloidal ceria slurry), application (STI/ILD CMP, others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The United States accounts for 38% of global production.

- Competitive Landscape: Profiles of leading market participants including Resonac, Merck KGaA (Versum Materials), and AGC, which collectively hold over 85% market share, along with their product offerings and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in chemical mechanical planarization processes and evolving industry standards for semiconductor manufacturing.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges in supply chain, raw material availability, and technical specifications for advanced node semiconductor fabrication.

- Stakeholder Analysis: Insights for semiconductor manufacturers, material suppliers, foundries, and investors regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Ceria CMP Slurry Market?

-> CMP Slurry Market was valued at 422 million in 2024 and is projected to reach US$ 583 million by 2032, at a CAGR of 4.8% during the forecast period.

Which key companies operate in Global Ceria CMP Slurry Market?

-> Key players include Resonac, Merck KGaA (Versum Materials), AGC, KC Tech, and Anjimirco Shanghai, among others.

What are the key growth drivers?

-> Key growth drivers include increasing semiconductor manufacturing, demand for advanced nodes, and expansion of wafer fabrication facilities.

Which region dominates the market?

-> Asia-Pacific is the largest consumer, while North America remains the dominant production region with 38% market share.

What are the emerging trends?

-> Emerging trends include development of next-generation slurries for advanced nodes, eco-friendly formulations, and precision particle size control technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...