Brain-computer interface neural recording chip with 1024 channels Market Insights

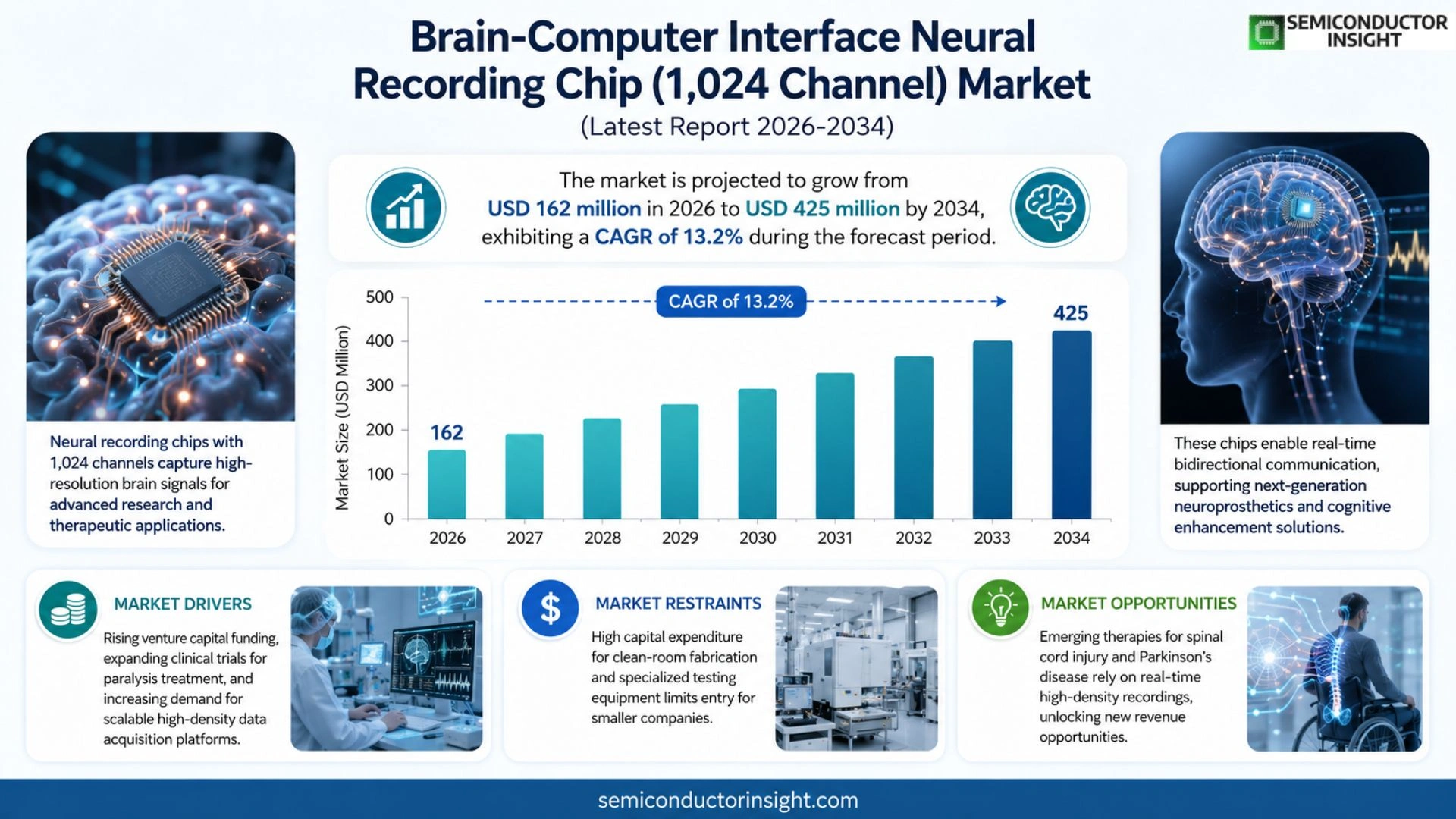

Global Brain-computer interface neural recording chip with 1,024 channel market size was valued at USD 152 million in 2025. The market is projected to grow from USD 162 million in 2026 to USD 425 million by 2034, exhibiting a CAGR of 13.2% during the forecast period.

These chips integrate ultra‑high‑density microelectrode arrays capable of simultaneously capturing electrical activity from up to 1,024 neuronal sites. Built on CMOS technology, they provide sub‑microsecond latency and enable bidirectional communication for both recording and stimulation, supporting advanced research in neuroscience and emerging therapeutic applications such as motor prostheses and cognitive augmentation.

Growth is driven by rising venture capital funding in neurotechnology, expanding clinical trials for paralysis treatment, and increasing demand for scalable data acquisition platforms in academic labs.

MARKET DRIVERS

Increasing Demand for High‑Resolution Neural Interfaces

Brain‑computer interface neural recording chip with 1024 channels Market is being propelled by neuroscientists seeking single‑neuron resolution across large cortical areas. Clinical trials in motor‑restoration and epilepsy monitoring are adopting 1024‑channel arrays to capture richer spatiotemporal data, which shortens development cycles for next‑generation implants.

Advancements in Miniaturization and Power Efficiency

Recent CMOS processes have reduced the footprint of 1024‑channel chips to under 5 mm² while maintaining sub‑microwatt power consumption. This enables fully implantable systems with longer battery life, a key factor for patient adoption and reimbursement approvals.

➤ “The ability to record from a thousand channels simultaneously without heat buildup is a game‑changer for chronic neural interfacing.”

Investment activity reflects confidence: venture capital funding for high‑density neural ASICs grew by 38 % year‑over‑year, supporting expanded R&D pipelines and accelerating time‑to‑market for innovative therapeutic solutions.

MARKET CHALLENGES

Regulatory Hurdles and Clinical Validation

Regulators require extensive safety data for devices that interface with thousands of neural sites, extending trial durations and increasing costs. Demonstrating long‑term biocompatibility of dense electrode arrays remains a bottleneck for widespread approval.

Other Challenges

Manufacturing Scale‑Up

Yield optimization for 1024‑channel wafers is complex; defect rates above 5 % can render a production run uneconomical, limiting the ability of manufacturers to meet rising demand without significant capital investment.

MARKET RESTRAINTS

High Capital Expenditure

Building clean‑room facilities capable of fabricating high‑density neural chips requires multi‑million‑dollar investments, which constrains entry to well‑funded incumbents and slows competitive pricing pressures.

In addition, the need for specialized test equipment to verify 1024‑channel functionality adds operational overhead, further restraining smaller firms from scaling their offerings.

MARKET OPPORTUNITIES

Emerging Therapeutic Applications

Therapies for spinal cord injury and Parkinson’s disease are exploring closed‑loop control that relies on real‑time high‑density recordings. The 1024‑channel architecture can provide the necessary feedback bandwidth to fine‑tune stimulation parameters, opening sizable revenue streams.

Integration with artificial intelligence platforms enables on‑chip preprocessing of massive data streams, reducing latency for neuroprosthetic control and creating value‑added services for clinicians and patients.

Beyond clinical use, consumer neurotechnology firms are investigating immersive brain‑gaming and wellness monitoring, where the richness of 1024‑channel data can differentiate premium products in a nascent market.

Brain-computer interface neural recording chip with 1024 channels Market Trends

Rising Venture Capital Investment Accelerates Development

The neurotechnology sector has witnessed a pronounced surge in venture capital allocations aimed at high‑density brain‑computer interface recording platforms. Investors are attracted by the prospect of ultra‑high‑density microelectrode arrays that enable simultaneous monitoring of up to 1,024 neuronal sites, a capability that expands experimental bandwidth for both academic and therapeutic research. Funding rounds in the past twelve months have supported scale‑up of CMOS‑based fabrication, integration of sub‑microsecond latency electronics, and the creation of modular data acquisition pipelines. This capital inflow shortens product development cycles, drives competitive pricing, and reinforces the market’s shift from prototype prototypes to more regulated, commercial‑grade solutions.

Other Trends

Expansion of Clinical Trials for Motor Prostheses

Clinical investigation activity has broadened considerably, with multiple multi‑center trials evaluating the therapeutic impact of 1,024‑channel neural recording chips in restoring motor function for patients with spinal cord injuries. These studies emphasize bidirectional communication,recording neural intent while delivering precise stimulation,to achieve functional hand grasp and finger articulation. Trial outcomes are generating real‑world performance datasets that validate device safety, reliability, and long‑term biocompatibility, thereby expediting regulatory pathways and encouraging broader clinical adoption of the technology.

Strategic Partnerships Drive Commercialization

Collaboration between leading hardware manufacturers and academic institutions has become a defining characteristic of the market’s evolution. Notable examples include joint development agreements that combine deep‑learning‑enabled signal processing with next‑generation probe design, resulting in plug‑and‑play modules for laboratory use. These alliances streamline engineering resources, accelerate technology transfer, and create standardized interfaces that lower entry barriers for emerging startups. As the ecosystem matures, end‑users benefit from interoperable platforms that support scalable data acquisition, fostering a virtuous cycle of innovation and market growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Emerging high‑density neural recording chips reshape BCI market

Brain‑Computer Interface (BCI) neural recording chip segment with 1,024 channels is dominated by a handful of technologically advanced firms that have successfully integrated CMOS‑based micro‑electrode arrays with sub‑microsecond latency. Neuralink Corp. leads the space with its ultra‑dense “N1” probe, leveraging substantial venture capital backing and a vertically integrated manufacturing pipeline. Blackrock Microsystems follows closely, capitalising on its long‑standing reputation for clinical‑grade probes and a strategic partnership with UCSF that accelerates next‑generation high‑channel designs. Paradromics Inc. and Synchron Inc. complement these leaders by offering modular architectures that cater to both research laboratories and emerging therapeutic applications, such as motor‑prosthesis trials, thereby shaping the market’s competitive dynamics and influencing pricing structures.

Beyond the primary incumbents, a diverse set of niche innovators contributes depth to the ecosystem. Cerebras Systems brings its expertise in large‑scale AI hardware to produce high‑throughput data acquisition platforms, while companies like NeuroPace, g.tec medical engineering, BrainCo, NextMind, and NeuroElectrics focus on specialized use cases ranging from epilepsy monitoring to consumer‑grade neuro‑feedback. Academic spin‑outs such as Utah Neurotechnology and emerging European startups further expand the competitive landscape, driving collaborative research and creating pressure on incumbents to continuously improve channel density, power efficiency, and biocompatibility.

List of Key Brain‑computer Interface Companies Profiled

- Neuralink Corp., Blackrock Microsystems, Paradromics Inc., Synchron Inc., Cerebras Systems, NeuroPace, g.tec medical engineering, BrainCo, NextMind, NeuroElectrics, Utah Neurotechnology

- Neuralink Corp., Blackrock Microsystems, Paradromics Inc., Synchron Inc.

- Cerebras Systems, NeuroPace, g.tec medical engineering, BrainCo, NextMind, NeuroElectrics, Utah Neurotechnology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Ultrahigh‑density CMOS probes dominate the market because they enable simultaneous recording from a thousand neuronal sites with sub‑microsecond latency. • They provide seamless integration with existing data‑acquisition ecosystems. • Their scalability supports emerging bidirectional stimulation therapies. • Robust fabrication yields consistent performance across research and clinical settings. |

| By Application |

|

Neuroscience research remains the primary driver, as investigators seek richer spatiotemporal data to decode brain activity. • Academic labs value the open‑source software ecosystem that accompanies many chips. • The ability to capture high‑resolution neural dynamics fuels advances in learning algorithms. • Collaborative projects with clinical partners accelerate translation to therapeutic prototypes. |

| By End User |

|

Academic institutions are the leading end‑user segment, drawn by the flexibility of custom probe designs and the depth of data they can generate. • Universities prioritize open collaboration, driving rapid iteration of chip architectures. • Funding from venture capital and government programs fuels large‑scale recording studies. • The educational component creates a pipeline of skilled researchers who adopt the technology early. |

| By Technology Integration |

|

On‑chip signal processing is emerging as a key differentiator, allowing real‑time artifact removal and feature extraction. • It reduces data bandwidth requirements for downstream systems. • Enhances reliability of long‑duration recordings in ambulatory settings. • Encourages integration with AI‑driven interpretation pipelines. |

| By Deployment Setting |

|

Implantable clinical systems are gaining prominence as therapeutic trials move toward chronic use. • Designers focus on biocompatibility and long‑term stability. • Seamless integration with patient‑specific stimulation algorithms is a priority. • Partnerships between chip makers and biomedical device firms accelerate regulatory pathways. |

Regional Analysis: North America

The medical sector represents the largest application area for BCI neural recording chips. These chips are crucial in developing advanced prosthetic limbs, communication systems for paralyzed individuals, and therapies for neurological conditions like epilepsy and Parkinson’s disease. The demand for more precise and high-resolution neural data is driving the adoption of 1024-channel systems.

Research institutions and academic laboratories are significant consumers of these advanced chips. They are utilized for fundamental research into brain function, cognitive processes, and the development of new BCI algorithms. The high channel count enables researchers to capture more detailed neural activity patterns, leading to deeper insights into the brain.

While still in its early stages, the application of BCI technology for cognitive enhancement is gaining traction. High-channel-count chips hold the potential to decode complex cognitive states and provide feedback for improved focus, memory, and learning. Ethical considerations and regulatory hurdles remain key challenges in this area.

The defense and security sectors are exploring the potential of BCI technology for applications such as soldier performance enhancement and secure communication. However, these applications are often subject to stringent regulations and ethical reviews.

Europe

Europe exhibits a steady growth trajectory in Brain-computer interface neural recording chip with 1024 channels market. Several countries, including Germany, the UK, and France, have strong research ecosystems and are actively investing in BCI development. The focus in Europe tends to be on medical applications and research collaborations, with a strong emphasis on data privacy and ethical considerations. While the market is fragmented compared to the US, there is significant potential for growth as the technology matures and regulatory frameworks become clearer. The European Union’s support for health technology innovation is fostering further advancements in this field.

Asia-Pacific

Asia-Pacific represents a rapidly expanding market for BCI technology. Countries like China and Japan are witnessing substantial investments in neuroscience and related technologies. The demand is driven by an aging population, increasing prevalence of neurological disorders, and a growing interest in assistive technologies. While the market is still relatively nascent, the rapid adoption of smart healthcare solutions and the government’s focus on technological advancement are expected to fuel significant growth in the coming years. The cost-effectiveness of manufacturing in the region also presents an advantage.

South America

South America is an emerging market with growing interest in BCI technology, primarily driven by the increasing prevalence of neurological conditions and a rising awareness of assistive devices. While the market size is currently smaller compared to North America and Europe, there is potential for expansion as healthcare infrastructure improves and investments in research and development increase. The focus is largely on providing accessible medical solutions to a vast population.

Middle East & Africa

The Middle East and Africa represent a relatively nascent market for brain-computer interface neural recording chip with 1024 channels. However, with increasing investments in healthcare infrastructure and a growing awareness of advanced medical technologies, the market is poised for future growth. The demand is expected to be driven by the rising prevalence of neurological disorders and a growing need for innovative treatment options. The adoption rate is likely to be influenced by economic factors and the availability of skilled healthcare professionals.

Report Scope

This market research report provides a comprehensive analysis of the Brain-computer interface neural recording chip with 1024 channels Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Brain-computer interface neural recording chip with 1024 channels Market?

-> Brain-computer interface neural recording chip with 1,024 channel market is projected to grow from USD 162 million in 2026 to USD 425 million by 2034.

Which key companies operate in Brain-computer interface neural recording chip with 1024 channels Market?

-> Key players include Neuralink Corp., Blackrock Microsystems, Paradromics Inc., and Cerebras Systems.

What are the key growth drivers?

-> Key growth drivers include venture capital funding in neurotechnology, expanding clinical trials for paralysis treatment, and rising demand for scalable data acquisition platforms in academic and research labs.

Which region dominates the market?

-> Regional dominance information is not explicitly disclosed in the source data.

What are the emerging trends?

-> Emerging trends include ultra‑high‑density microelectrode arrays, bidirectional communication capabilities, and therapeutic applications such as motor prostheses and cognitive augmentation.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...