MARKET INSIGHTS

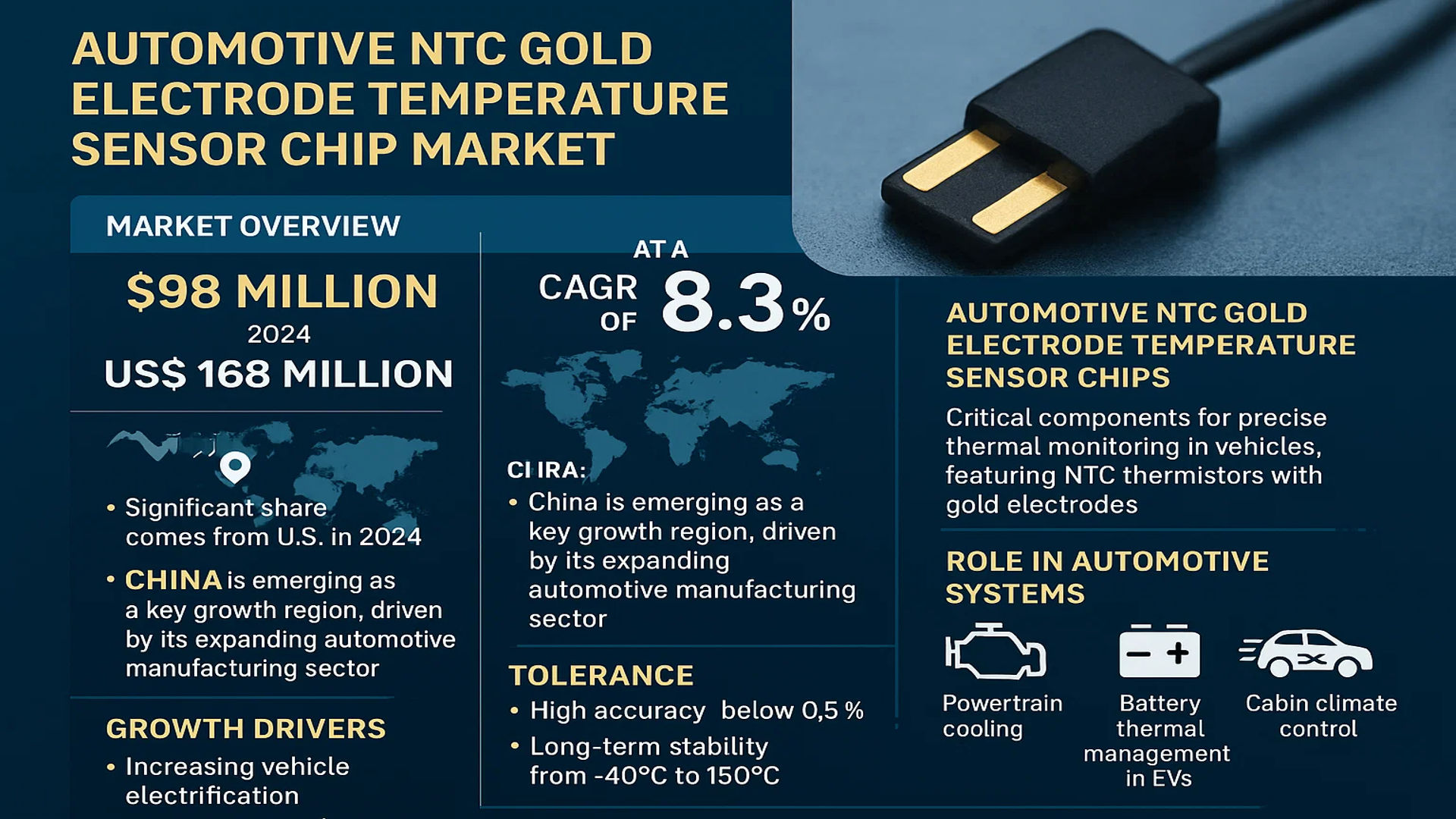

The global Automotive NTC Gold Electrode Temperature Sensor Chip Market was valued at 98 million in 2024 and is projected to reach US$ 168 million by 2032, at a CAGR of 8.3% during the forecast period. While the U.S. market is estimated at a significant share in 2024, China is emerging as a key growth region, driven by its expanding automotive manufacturing sector.

Automotive NTC gold electrode temperature sensor chips are critical components used for precise thermal monitoring in vehicles. These sensors leverage negative temperature coefficient (NTC) thermistors with gold electrodes to deliver high accuracy (often below 0.5% tolerance) and long-term stability across temperature ranges from -40°C to 150°C. They play a vital role in multiple automotive systems including powertrain cooling, battery thermal management in EVs, and cabin climate control.

Market growth is propelled by increasing vehicle electrification, stringent emission regulations requiring optimized thermal management, and rising demand for advanced driver-assistance systems (ADAS). The precision segment (less than 0.5% tolerance) is expected to witness accelerated adoption, particularly in luxury and electric vehicles where temperature sensitivity is crucial. Leading manufacturers like Murata, TDK, and TE Connectivity are investing in miniaturized sensor designs with improved response times below 3 seconds to meet evolving OEM requirements.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Electric Vehicles Accelerating Adoption of Advanced Temperature Sensors

The global shift toward electric vehicles (EVs) is a primary driver for NTC gold electrode temperature sensor chips, as these components play a critical role in battery thermal management systems. With EVs projected to account for over 30% of new car sales by 2030, the need for precise temperature monitoring in high-voltage battery packs and charging systems is creating substantial market growth. These sensors ensure optimal performance while preventing thermal runaway events, which can lead to safety hazards. The precision of less than 0.5% offered by gold electrode variants makes them particularly valuable in these sensitive applications where marginal temperature fluctuations can impact battery lifespan and vehicle efficiency.

Stringent Automotive Safety Regulations Fueling Market Expansion

Government mandates regarding vehicle safety systems are compelling automakers to integrate more sophisticated temperature monitoring solutions. Regulatory bodies worldwide are implementing stricter standards for thermal management in both conventional and electric vehicles, particularly concerning battery systems and powertrain components. This regulatory push is driving automotive manufacturers to adopt high-reliability NTC sensors with gold electrodes, which offer superior stability and longevity compared to conventional options. Automakers are also prioritizing these sensors because they maintain calibration over extended periods, reducing warranty claims and improving brand reliability.

➤ For instance, recent updates to UNECE vehicle safety regulations now require more comprehensive temperature monitoring in EV battery systems, directly benefiting the sensor market.

Advancements in Sensor Miniaturization Creating New Application Areas

Technological progress in microfabrication is enabling the production of increasingly compact NTC sensors without compromising performance. This miniaturization trend is allowing sensor installation in previously inaccessible vehicle locations, such as within individual battery cells or compact electric motor housings. The automotive industry’s growing emphasis on predictive maintenance systems is further accelerating demand, as these miniature sensors can be distributed throughout vehicle systems to provide comprehensive thermal profiling. Manufacturers are responding by developing chip-scale packaging solutions that maintain the gold electrode’s superior conductivity while meeting space constraints in modern vehicle designs.

MARKET RESTRAINTS

Volatile Gold Prices Creating Cost Pressure on Sensor Manufacturing

The gold electrode component represents a significant portion of these sensors’ production cost, making the market sensitive to fluctuations in precious metal commodities. During periods of economic uncertainty, gold prices can experience substantial volatility, complicating long-term pricing strategies for sensor manufacturers. While the automotive industry generally prioritizes performance over cost in safety-critical components, recent supply chain disruptions have made OEMs more price-conscious, sometimes leading to compromises on sensor specifications. Some manufacturers are exploring alternative electrode materials, though none have yet matched gold’s combination of conductivity and long-term stability in harsh automotive environments.

Complex Certification Processes Slowing Time-to-Market

Automotive-grade components face rigorous qualification procedures that can delay product launches. NTC gold electrode sensors must undergo extensive testing for thermal cycling endurance, vibration resistance, and long-term drift characteristics before receiving automotive approval. The certification process for a single sensor variant can span 12-18 months, creating bottlenecks in product development cycles. Furthermore, regional differences in automotive standards require separate validation processes for major markets, adding complexity for global suppliers. These challenges are particularly acute for new market entrants lacking established relationships with certification bodies and automotive OEMs.

MARKET OPPORTUNITIES

Expansion of Autonomous Vehicle Platforms Opening New Sensor Applications

The development of autonomous driving systems is creating novel thermal management requirements that favor precision NTC sensors. Advanced driver-assistance systems (ADAS) and autonomous vehicle computers generate significant heat loads that require precise monitoring to prevent performance degradation. Unlike conventional automotive applications, these systems demand sensors with enhanced EMI resistance – a characteristic where gold electrode designs excel. As automakers progress toward higher levels of vehicle autonomy, the integration of multiple redundant sensor systems will likely become standard practice, potentially doubling or tripling sensor content per vehicle in critical systems.

Emerging Markets Present Untapped Growth Potential

Developing automotive markets are demonstrating growing demand for advanced thermal management solutions as they transition to more sophisticated vehicle architectures. Countries with nascent EV industries represent particularly promising opportunities, as their vehicle designs often incorporate the latest thermal management technologies from the outset. Localization initiatives in these regions are prompting international sensor manufacturers to establish regional production capabilities, creating strategic partnerships with domestic automakers. This trend is especially notable in Southeast Asia, where government incentives are accelerating EV adoption and creating a favorable environment for component suppliers.

MARKET CHALLENGES

Supply Chain Vulnerabilities Impacting Sensor Availability

The automotive industry’s continued recovery from semiconductor shortages has revealed vulnerabilities in the temperature sensor supply chain. While gold electrode sensors don’t rely on advanced nodes like microcontrollers, their production requires specialized ceramic substrates and precious metal deposition equipment with limited global capacity. Recent geopolitical tensions have further complicated material sourcing, particularly for gold supply chains originating from certain regions. These disruptions are forcing manufacturers to maintain higher inventory levels and diversify their supplier networks, increasing operational costs that may eventually translate to higher prices for automotive customers.

Other Challenges

Intense Competition from Alternative Technologies

While NTC gold electrode sensors dominate many automotive applications, emerging technologies like thin-film RTDs and fiber optic temperature sensors are gaining traction in certain niche applications. These alternatives offer different performance trade-offs that may appeal to specific vehicle architectures, particularly in ultra-high-precision applications where cost is secondary to performance. Sensor manufacturers must continue innovating to maintain their competitive edge, particularly in gold electrode manufacturing processes that can enhance performance while controlling costs.

Technological Obsolescence Risks

The rapid pace of automotive electrification is driving continuous innovation in thermal management strategies, potentially rendering current sensor technologies obsolete more quickly than traditional automotive development cycles. Manufacturers face the challenge of anticipating future system requirements while maintaining production of current-generation products. This dynamic creates significant R&D investment requirements as companies work to develop next-generation sensors capable of meeting emerging demands for higher accuracy, faster response times, and enhanced communication capabilities within vehicle networks.

AUTOMOTIVE NTC GOLD ELECTRODE TEMPERATURE SENSOR CHIP MARKET TRENDS

Electrification and Smart Automotive Systems Drive Demand for High-Precision Sensors

The rapid electrification of vehicles, particularly in New Energy Vehicles (NEVs), is significantly boosting the adoption of NTC gold electrode temperature sensor chips. With over 10 million electric vehicles sold globally in 2024, these sensors have become critical for battery thermal management, ensuring safety and longevity. Automotive manufacturers are increasingly prioritizing precision sensors with tolerances below 0.5% to meet stringent EV performance requirements. Furthermore, the integration of these sensors with vehicle telematics enables real-time thermal monitoring, reducing battery failures by up to 30% compared to conventional systems.

Other Trends

Miniaturization and Integration with IoT Platforms

The push towards compact and lightweight automotive components is accelerating the development of smaller form-factor NTC sensor chips that maintain high accuracy. Major manufacturers are embedding these chips with IoT connectivity to feed temperature data into predictive maintenance systems. This trend aligns with the broader Industry 4.0 transformation in automotive production, where sensor data analytics optimizes everything from assembly line processes to post-sale vehicle performance monitoring. The Asia-Pacific region leads in this adoption, accounting for 48% of global sensor-integrated automotive IoT solutions as of 2024.

Supply Chain Diversification Redefines Manufacturing Landscapes

Geopolitical tensions and pandemic-driven disruptions have forced automakers to reconsider single-region supplier dependencies, particularly for critical components like temperature sensors. This has spurred investments in localized production facilities across North America and Europe, with an estimated 35% increase in regional sensor chip manufacturing capacity since 2022. Meanwhile, China continues to dominate the global supply, producing approximately 60% of automotive NTC sensor components, though export restrictions on rare-earth materials used in gold electrodes are prompting alternative material research and development.

COMPETITIVE LANDSCAPE

Key Industry Players

Manufacturers Expand Capabilities to Address Rising EV Demand and Temperature Control Needs

The global Automotive NTC Gold Electrode Temperature Sensor Chip market features a moderately fragmented competitive environment, with leading electronic component suppliers competing alongside specialized sensor manufacturers. This technology segment is gaining strategic importance as automakers prioritize thermal management solutions for electric vehicles and advanced powertrains. While Asian manufacturers dominate production volume, Western firms maintain strong positions in high-precision applications through technological differentiation.

Murata Manufacturing and TDK Corporation emerge as technology leaders, leveraging their comprehensive electronics portfolios to offer integrated sensor solutions. Murata’s 2023 acquisition of a temperature sensor specialist strengthened its capability to serve automotive OEMs with high-reliability chips rated for extreme environments. Meanwhile, Panasonic continues to expand its sensor production capacity in China to meet growing regional demand, particularly for new energy vehicles.

The market sees increasing specialization, with firms like Semitec focusing exclusively on temperature-sensitive components, achieving precision levels below 0.5% for critical automotive applications. Chinese manufacturers including Shenzhen Kemin Sensor and Huagong Tech are gaining market share through competitive pricing and rapid design iteration capabilities tailored to domestic automakers’ needs.

Recent industry developments highlight a strategic push toward miniaturization and enhanced durability. TE Connectivity‘s 2024 product launch featured gold-electrode sensors with 30% faster response times, while Vishay introduced a new anti-corrosion coating technology extending sensor lifespans in harsh automotive environments. Such innovations are reshaping competitive dynamics as suppliers vie for position in this $98 million market poised for 8.3% annual growth through 2032.

List of Key Automotive NTC Sensor Chip Manufacturers

- Murata Manufacturing (Japan)

- Panasonic Corporation (Japan)

- TDK Corporation (Japan)

- Semitec Corporation (Japan)

- TE Connectivity (Switzerland)

- Vishay Intertechnology (U.S.)

- Shenzhen Kemin Sensor Technology (China)

- Huagong Tech Company (China)

- Shenzhen KEPENGDA Electronics (China)

- TOPOS Technology (China)

- Sinochip Electronics (China)

Segment Analysis:

By Type

Precision: Less Than 0.5% Segment Dominates Due to the Increasing Need for High-Accuracy Temperature Monitoring in Electric Vehicles

The market is segmented based on type into:

- Precision: Less than 0.5%

- Preferred for applications requiring ultra-high accuracy in temperature sensing

- Precision: 0.5%-1%

- Precision: 1-2%

- Precision: More than 2%

- Typically used in less critical automotive applications with relaxed accuracy requirements

By Application

New Energy Heat Management Systems Lead the Market Due to Rapid EV Adoption and Thermal Management Needs

The market is segmented based on application into:

- Automotive Transmission

- New Energy Heat Management Systems

- Battery Pack Water Cooling Systems

- On-board Charging Temperature Control Systems

- Others

Regional Analysis: Automotive NTC Gold Electrode Temperature Sensor Chip Market

Asia-Pacific

The Asia-Pacific region dominates the global Automotive NTC Gold Electrode Temperature Sensor Chip market, accounting for over 45% of the total market share. China, Japan, and South Korea lead the regional demand due to their established automotive manufacturing ecosystems. The rapid adoption of electric vehicles (EVs) and hybrid vehicles in China (which alone contributes to nearly 60% of the region’s market) is accelerating the need for precise temperature monitoring solutions. Japanese automotive giants like Toyota and Honda heavily integrate these sensors in their EV battery management systems, while South Korea benefits from strong electronics manufacturing capabilities through companies like LG and Samsung. The region’s competitive advantage lies in its vertically integrated supply chains and government subsidies promoting local semiconductor production.

North America

North America represents the second-largest market for Automotive NTC Gold Electrode Temperature Sensor Chips, driven by stringent automotive safety regulations and the U.S. automotive industry’s technological advancements. With major automakers investing heavily in autonomous vehicles and EV infrastructure, the demand for high-precision temperature sensing chips (particularly those with less than 0.5% tolerance) is growing exponentially. Canada’s focus on cold-climate EV testing and Mexico’s expanding automotive component manufacturing further complement regional growth. However, reliance on imports for semiconductor components remains a key challenge, prompting initiatives like the CHIPS Act to boost local production capabilities.

Europe

Europe’s market is characterized by strong regulatory frameworks (EU’s Battery Directive and Euro 7 emissions standards) that mandate advanced thermal management systems in vehicles. Germany leads regional demand through automotive OEMs like Volkswagen and BMW, who prioritize sensor integration for battery thermal management in their EV platforms. The region shows growing preference for gold electrode sensors due to their corrosion resistance and long-term reliability in extreme conditions. While Western Europe maintains technological leadership, Eastern European countries are emerging as cost-effective manufacturing hubs. The region’s focus on circular economy principles also drives innovation in sensor recyclability and material efficiency.

South America

The South American market is in a growth phase, with Brazil and Argentina showing increasing adoption of temperature sensor chips in their growing automotive sectors. While the region still relies heavily on imported sensors, local assembly of vehicles (especially in Brazil’s Manaus industrial zone) creates opportunities for sensor suppliers. The market faces challenges including economic volatility and inconsistent regulatory standards, which slow adoption of advanced sensor technologies. However, the gradual shift towards flex-fuel vehicles and growing awareness of thermal management benefits present long-term growth potential.

Middle East & Africa

This region represents an emerging market with focused growth in Gulf Cooperation Council (GCC) countries, where extreme temperatures necessitate robust automotive thermal management solutions. The UAE and Saudi Arabia are leading in luxury vehicle adoption, driving demand for high-end sensor technologies. Africa’s market remains largely untapped due to limited local automotive production, though South Africa’s established vehicle manufacturing industry shows promising adoption rates. Infrastructure limitations and scarce technical expertise in sensor integration remain primary barriers to widespread market penetration across the region.

Report Scope

This market research report provides a comprehensive analysis of the Global Automotive NTC Gold Electrode Temperature Sensor Chip Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 98 million in 2024 and is projected to reach USD 168 million by 2032, growing at a CAGR of 8.3%.

- Segmentation Analysis: Detailed breakdown by product type (precision levels), application (automotive transmission, battery cooling systems, etc.), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with the U.S. and China as key growth markets.

- Competitive Landscape: Profiles of leading manufacturers including Murata, Panasonic, TDK, TE Connectivity, and Vishay, analyzing market share, product portfolios, and strategic developments.

- Technology Trends & Innovation: Assessment of miniaturization trends, integration with vehicle electronics, and advanced temperature sensing technologies.

- Market Drivers & Restraints: Evaluation of factors like EV adoption, thermal management needs, along with challenges in material costs and supply chain complexities.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, automotive OEMs, and component suppliers in the evolving automotive electronics ecosystem.

The analysis employs both primary research (industry interviews) and secondary research (verified market data) to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive NTC Gold Electrode Temperature Sensor Chip Market?

-> Automotive NTC Gold Electrode Temperature Sensor Chip Market was valued at 98 million in 2024 and is projected to reach US$ 168 million by 2032, at a CAGR of 8.3% during the forecast period.

Which key companies operate in this market?

-> Major players include Murata, Panasonic, TDK, TE Connectivity, Vishay, and Shenzhen Kemin Sensor, with the top five companies holding significant market share.

What are the key growth drivers?

-> Growth is driven by rising EV production, stringent thermal management requirements, and automotive electronics integration.

Which region dominates the market?

-> Asia-Pacific leads in both production and consumption, while North America shows strong growth in precision sensor adoption.

What are the emerging trends?

-> Key trends include miniaturization of sensors, integration with battery management systems, and development of high-precision (under 0.5%) variants.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...