MARKET INSIGHTS

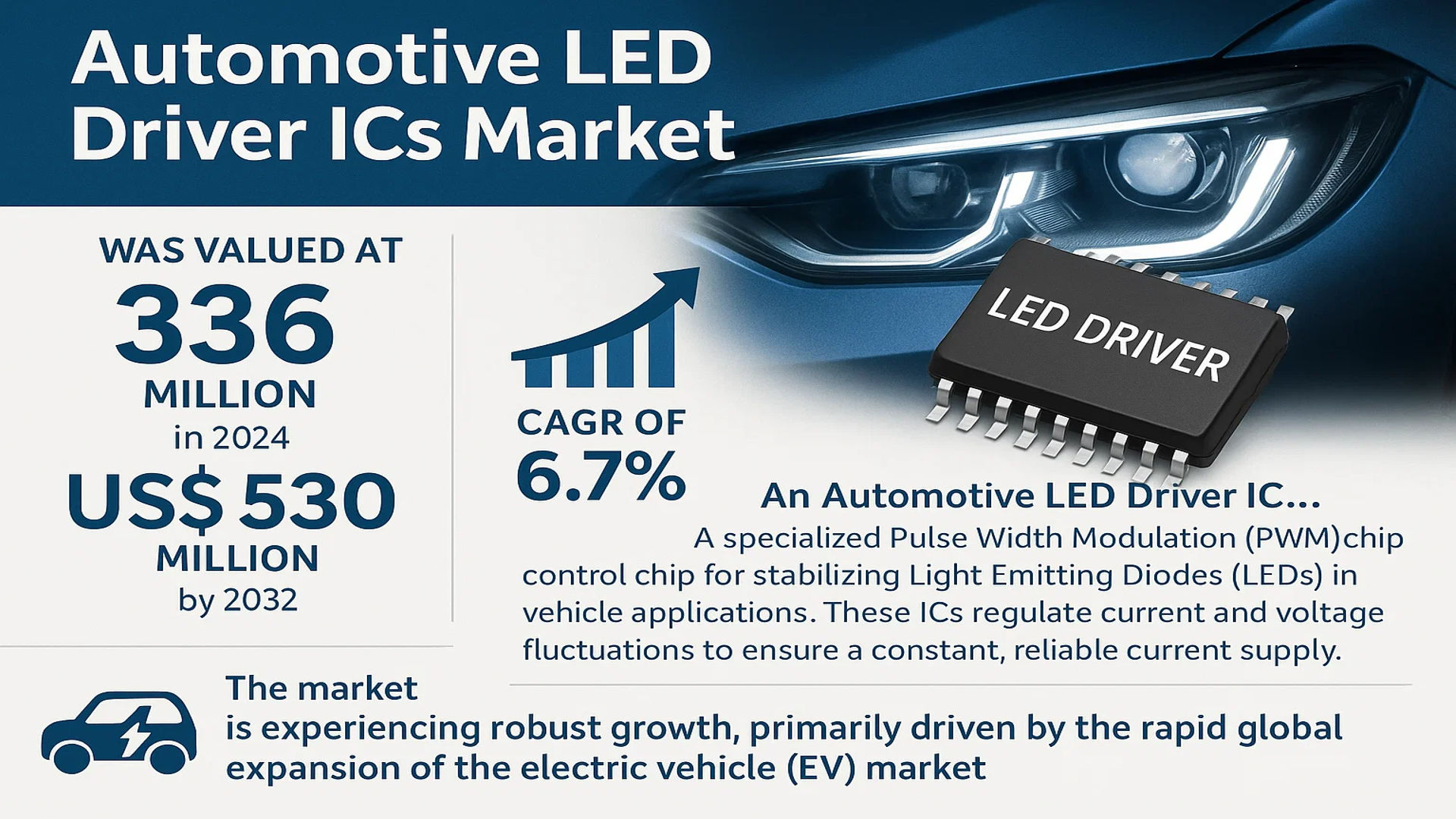

The global Automotive LED Driver ICs Market was valued at 336 million in 2024 and is projected to reach US$ 530 million by 2032, at a CAGR of 6.7% during the forecast period.

An Automotive LED Driver IC is a specialized Pulse Width Modulation (PWM) control chip essential for stabilizing and protecting Light Emitting Diodes (LEDs) in vehicle applications. Because LEDs are semiconductor devices with sensitive and negative temperature characteristics, these driver ICs regulate current and voltage fluctuations to ensure a constant, reliable current supply. This precise control is fundamental for maintaining optimal performance and longevity of automotive lighting and display systems.

The market is experiencing robust growth, primarily driven by the rapid global expansion of the electric vehicle (EV) market. For instance, global sales of new energy vehicles surpassed 10 million units in 2022, representing a significant 61% year-on-year increase. China, a dominant force, recorded production and sales of 7.058 million and 6.887 million new energy vehicles respectively in 2022. This electrification trend demands more sophisticated LED driver ICs that offer higher efficiency, superior electromagnetic interference (EMI) immunity, and enhanced integration to support advanced lighting and infotainment features in modern vehicles.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Electrification of Global Vehicle Fleet to Accelerate Market Expansion

The global shift toward vehicle electrification represents a primary catalyst for the automotive LED driver ICs market. Electric vehicles (EVs) and hybrid vehicles require sophisticated lighting systems that demand precise current regulation and energy efficiency, which LED driver ICs provide. The worldwide sales of new energy vehicles surpassed 10 million units in 2022, marking a 61% year-on-year increase, with China and Europe leading this expansion. China alone recorded production and sales of 7.058 million and 6.887 million new energy vehicles respectively in 2022, maintaining its position as the global leader for eight consecutive years. This electrification trend necessitates advanced LED driver solutions that optimize power consumption and enhance vehicle range, directly driving market growth.

Increasing Adoption of Advanced Automotive Lighting Systems to Fuel Demand

Modern vehicles increasingly incorporate sophisticated lighting applications that extend beyond basic illumination to include adaptive driving beams, dynamic turn signals, and ambient interior lighting. These systems require precise current control and dimming capabilities that only specialized LED driver ICs can provide. The automotive lighting market has evolved from simple functionality to becoming a key differentiator in vehicle design and safety. High-end vehicles now incorporate over 300 LEDs for various functions, each requiring individual driver control. This proliferation of LED applications across headlights, taillights, and interior lighting creates substantial demand for driver ICs that can manage complex lighting scenarios while meeting stringent automotive reliability standards.

Stringent Regulatory Standards for Vehicle Safety and Efficiency to Propel Market Growth

Government regulations worldwide are mandating improved vehicle safety and energy efficiency, directly influencing the adoption of advanced LED lighting systems and their driver ICs. Regulatory bodies across major automotive markets have implemented standards requiring brighter, more efficient, and more reliable lighting systems. These regulations often specify minimum illumination levels, beam patterns, and energy consumption limits that conventional lighting cannot meet. LED systems with advanced driver ICs provide the necessary performance while reducing power consumption by up to 60% compared to traditional lighting solutions. The alignment of regulatory requirements with LED technology capabilities creates a compelling case for increased adoption across all vehicle segments.

MARKET RESTRAINTS

Complex Automotive Certification Processes to Hinder Market Penetration

The automotive industry imposes rigorous certification requirements that significantly challenge LED driver IC manufacturers. Components must meet numerous international standards covering temperature tolerance, electromagnetic compatibility, and operational lifespan under extreme conditions. The certification process for a single automotive-grade LED driver IC typically requires 18-24 months of testing and validation, creating substantial barriers to market entry. These prolonged development cycles and compliance costs particularly affect smaller manufacturers who lack the resources to navigate the complex automotive qualification landscape. The stringent requirements also increase research and development expenses, which ultimately translate to higher component costs that may limit adoption in price-sensitive vehicle segments.

Supply Chain Vulnerabilities and Component Shortages to Constrain Market Growth

The automotive LED driver IC market faces significant constraints from ongoing supply chain disruptions and semiconductor shortages. The concentration of semiconductor manufacturing in specific geographic regions creates vulnerability to geopolitical tensions, natural disasters, and production capacity limitations. Recent global chip shortages have demonstrated how quickly supply constraints can impact automotive production, with some manufacturers reporting production delays of 6-12 months due to component unavailability. The specialized nature of automotive-grade semiconductors further complicates supply chain management, as these components cannot be easily substituted with commercial-grade alternatives. These supply challenges force automotive manufacturers to maintain higher inventory levels, increasing costs and potentially delaying new vehicle launches that incorporate advanced LED lighting systems.

Technical Complexity in Electromagnetic Compatibility to Limit Design Flexibility

Modern vehicles contain numerous electronic systems that must operate without mutual interference, creating significant electromagnetic compatibility (EMC) challenges for LED driver ICs. The switching frequencies used in LED drivers can generate electromagnetic emissions that interfere with other vehicle systems, particularly radio receivers, sensors, and control units. Achieving EMC compliance requires sophisticated filtering, shielding, and circuit layout techniques that increase design complexity and component costs. The problem intensifies in electric vehicles where high-power traction systems create additional electromagnetic noise. These technical challenges often force design compromises that limit lighting performance or require additional components, reducing the cost-effectiveness of advanced LED lighting solutions.

MARKET CHALLENGES

Thermal Management Constraints in Compact Automotive Environments to Challenge Reliability

Automotive LED driver ICs face significant thermal management challenges due to the confined spaces and high ambient temperatures in vehicle applications. Unlike consumer electronics, automotive components must operate reliably in environments where temperatures can exceed 105°C, while simultaneously managing the heat generated by their own operation. The power density of modern LED driver ICs continues to increase as manufacturers pack more functionality into smaller packages, exacerbating thermal challenges. Effective heat dissipation requires careful thermal design and often additional heatsinking, which conflicts with the automotive industry’s relentless pursuit of miniaturization and weight reduction. These thermal constraints can limit performance, reduce lifespan, and increase failure rates in demanding automotive applications.

Other Challenges

Cost Pressure from Automotive Manufacturers

Automotive original equipment manufacturers maintain intense cost pressure on component suppliers, particularly for high-volume vehicle models. This cost focus often conflicts with the sophisticated features and high reliability required for automotive LED driver ICs. Manufacturers must balance performance requirements against aggressive cost targets that typically demand annual price reductions of 3-5% while simultaneously adding new features and capabilities.

Rapid Technological Obsolescence

The fast pace of technological advancement in both LED technology and driver IC design creates challenges for long vehicle development cycles. Automotive programs typically span 3-5 years from concept to production, during which time LED and driver technologies may undergo multiple generations of improvement. This mismatch between technology cycles and vehicle development timelines can result in vehicles launching with already-obsolete lighting technology.

MARKET OPPORTUNITIES

Integration of Smart Lighting and Vehicle Communication Systems to Create New Revenue Streams

The convergence of lighting technology with vehicle communication and automation systems presents substantial growth opportunities for LED driver IC manufacturers. Modern vehicles increasingly incorporate lighting systems that communicate with other vehicle systems and external infrastructure. Adaptive front lighting systems that adjust beam patterns based on driving conditions, vehicle-to-vehicle communication through light patterns, and integration with advanced driver assistance systems all require sophisticated driver ICs with enhanced processing capabilities. These smart lighting applications typically command premium prices and higher profit margins compared to basic lighting systems. The integration of lighting with vehicle networks also creates opportunities for value-added features such as predictive maintenance, real-time performance monitoring, and over-the-air updates.

Expansion in Emerging Markets and Entry-Level Vehicle Segments to Broaden Addressable Market

While advanced LED lighting has primarily featured in premium vehicles, significant opportunities exist for expansion into emerging markets and entry-level vehicle segments. As manufacturing costs decrease and production volumes increase, LED lighting technology becomes economically viable for mass-market vehicles. Emerging automotive markets in Asia, Latin America, and Africa are experiencing rapid vehicle adoption, with consumers increasingly demanding features previously available only in developed markets. This democratization of technology creates opportunities for cost-optimized LED driver ICs that provide essential functionality at competitive price points. Manufacturers that successfully develop solutions for these price-sensitive segments can access substantially larger market volumes than the premium segment alone.

Development of Specialized Solutions for Electric and Autonomous Vehicles to Enable Premium Applications

The specific requirements of electric and autonomous vehicles create specialized opportunities for LED driver IC manufacturers. Electric vehicles prioritize energy efficiency to maximize driving range, creating demand for ultra-efficient driver ICs with minimal power loss. Autonomous vehicles require lighting systems that communicate vehicle intent to pedestrians and other road users, necessitating dynamic lighting capabilities and sophisticated control interfaces. These specialized applications often justify higher component costs and provide opportunities for technology differentiation. Manufacturers that develop solutions specifically optimized for these emerging vehicle categories can establish strong market positions before technology standards become firmly established.

AUTOMOTIVE LED DRIVER ICS MARKET TRENDS

Electrification and Advanced Lighting Systems Drive Market Expansion

The global automotive industry’s rapid shift toward electrification has become the primary catalyst for the Automotive LED Driver ICs market. With electric vehicle sales surpassing 10 million units globally in 2022, representing a 61% year-over-year growth, the demand for sophisticated electronic components has surged dramatically. LED driver ICs are essential for managing the precise current requirements of modern automotive lighting systems, particularly in electric vehicles where energy efficiency directly impacts driving range. These components ensure stable operation of LED arrays despite voltage fluctuations and temperature variations, which is critical in the demanding automotive environment. Furthermore, the increasing adoption of advanced driver assistance systems (ADAS) and autonomous driving features has created additional demand for reliable illumination systems that require sophisticated driver ICs to maintain consistent performance under varying conditions.

Other Trends

Integration of Smart Lighting Solutions

The automotive lighting landscape is evolving beyond basic illumination to incorporate intelligent, adaptive lighting systems that enhance safety and user experience. Modern vehicles increasingly feature matrix LED headlights that can dynamically adjust beam patterns to avoid dazzling other drivers while maintaining optimal road illumination. These systems require advanced driver ICs capable of precise current control and rapid response times. The trend toward customizable interior lighting, with some premium vehicles offering over 16 million color options for ambient lighting, further drives demand for sophisticated driver ICs that can manage complex RGB LED configurations. This evolution toward smart lighting represents a significant value-added opportunity for semiconductor manufacturers, as these systems typically require more advanced and higher-margin driver IC solutions compared to traditional lighting applications.

Miniaturization and Increased Functional Integration

Automotive manufacturers face constant pressure to reduce system size and weight while increasing functionality, particularly in electric vehicles where every gram affects efficiency and range. This has driven LED driver IC manufacturers to develop highly integrated solutions that combine multiple functions into single packages. Modern driver ICs now often incorporate protection features, diagnostics, and communication interfaces alongside their primary current regulation functions. The industry has seen a notable shift toward higher integration levels, with some latest-generation devices reducing component count by up to 40% compared to previous solutions. This trend toward miniaturization is particularly important as vehicle designs become more streamlined and packaging space becomes increasingly constrained, especially with the proliferation of additional electronic systems in modern vehicles. The development of these compact, multi-functional driver ICs represents a significant engineering achievement that addresses both performance requirements and spatial constraints in contemporary automotive design.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Positioning Drive Market Leadership

The global automotive LED driver ICs market exhibits a semi-consolidated structure, characterized by intense competition between established semiconductor giants and agile, specialized firms. This dynamic is fueled by the rapid electrification of vehicles and the increasing complexity of automotive lighting and display systems. Leading players leverage their extensive R&D capabilities, robust supply chains, and deep relationships with Tier-1 automotive suppliers to maintain a competitive edge. The market’s evolution is further shaped by stringent automotive safety and reliability standards, which act as significant barriers to entry and favor companies with proven quality management systems like AEC-Q100 certification.

Infineon Technologies (Germany) and STMicroelectronics (Switzerland) are dominant forces, collectively commanding a significant portion of the market share. Their leadership is underpinned by comprehensive product portfolios that cater to the entire spectrum of automotive applications, from basic interior lighting to advanced adaptive headlight systems. A key to their success is the vertical integration of manufacturing and a strong focus on developing highly efficient, robust ICs that meet the exacting demands of the automotive environment, including wide operating temperature ranges and high electromagnetic compatibility (EMC).

Texas Instruments (TI) (U.S.) and ON Semiconductor (onsemi) (U.S.) also hold substantial market positions, recognized for their innovation in analog and power management technologies. Their growth is propelled by strategic investments in developing advanced driver ICs that support complex matrix LED headlights and sophisticated infotainment display backlighting. These companies excel in providing integrated solutions that reduce system complexity and board space, a critical factor for automotive designers striving for miniaturization and cost reduction.

Furthermore, companies are aggressively expanding their market presence through targeted growth initiatives. ROHM Semiconductor (Japan) and NXP Semiconductors (Netherlands) are strengthening their positions through significant R&D investments focused on enhancing product intelligence and functional safety features. Recent developments include the launch of new IC families with integrated diagnostics and communication interfaces, such as I²C or SPI, enabling more precise control and feedback for smart lighting systems. Strategic partnerships with major automotive OEMs and expansions of production capacity, particularly in Asia to cater to the booming electric vehicle market in China, are expected to significantly grow their market share over the forecast period.

Meanwhile, specialized players like Melexis (Belgium) and Monolithic Power Systems (MPS) (U.S.) are carving out strong niches by offering highly differentiated products. Melexis, for instance, is renowned for its expertise in current-sensing and communication technologies vital for modern LED drivers. These companies are intensifying competition through innovative product expansions and a focus on application-specific technical support, ensuring their continued relevance and growth within the competitive landscape.

List of Key Automotive LED Driver IC Companies Profiled

- Infineon Technologies AG (Germany)

- Texas Instruments Incorporated (TI) (U.S.)

- NXP Semiconductors N.V. (Netherlands)

- STMicroelectronics N.V. (Switzerland)

- ON Semiconductor Corporation (onsemi) (U.S.)

- ROHM Semiconductor (Japan)

- Analog Devices, Inc. (U.S.)

- Melexis NV (Belgium)

- Toshiba Electronic Devices & Storage Corporation (Japan)

- Microchip Technology Inc. (U.S.)

- Renesas Electronics Corporation (Japan)

- Diodes Incorporated (U.S.)

- Monolithic Power Systems, Inc. (MPS) (U.S.)

- Nexperia B.V. (Netherlands)

- Macroblock, Inc. (Taiwan)

Segment Analysis:

By Type

Buck LED Driver Segment Leads the Market Due to High Adoption in Interior and Exterior Lighting Applications

The market is segmented based on type into:

- Buck LED Driver

- Boost LED Driver

- Buck-Boost LED Driver

- Linear Current Sources LED Driver

- Others

By Application

Headlights Segment Dominates Owing to Stringent Safety Regulations and High-Brightness Requirements

The market is segmented based on application into:

- Headlights

- Taillights/Interior Lights

- Infotainment Systems

- Others

By Vehicle Type

Electric Vehicles Segment Exhibits Strongest Growth Driven by Higher LED Penetration and Advanced Lighting Systems

The market is segmented based on vehicle type into:

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

By Sales Channel

OEM Segment Commands Largest Share Due to Direct Integration in Vehicle Manufacturing Process

The market is segmented based on sales channel into:

- OEM (Original Equipment Manufacturer)

- Aftermarket

Regional Analysis: Automotive LED Driver ICs Market

Asia-Pacific

The Asia-Pacific region dominates the global Automotive LED Driver ICs market, accounting for over 45% of the total market share by revenue in 2024. This leadership position is primarily driven by China, the world’s largest producer and consumer of new energy vehicles (NEVs). In 2022, China’s NEV sales reached 6.887 million units, a staggering 93.4% year-on-year increase, creating immense demand for advanced automotive electronics. The region’s robust semiconductor manufacturing ecosystem, coupled with aggressive government support for electric vehicle adoption, fuels the production and integration of sophisticated LED driver ICs. Key markets like Japan and South Korea, home to leading automakers and Tier-1 suppliers, further bolster demand for high-reliability components for both domestic production and global exports. The focus is on cost-competitive, highly integrated solutions to support the mass production of vehicles featuring advanced lighting and infotainment systems.

Europe

Europe represents a highly advanced and innovation-driven market for Automotive LED Driver ICs, characterized by stringent automotive safety and electromagnetic compatibility (EMC) standards. The region’s strong push towards electrification is a key growth driver; for instance, pure electric vehicle sales in Europe grew 29% year-on-year to 1.58 million units in 2022. This rapid adoption of electric vehicles necessitates LED driver ICs with exceptional efficiency to maximize driving range and superior performance to meet the high bar set by premium European automotive brands. The presence of major semiconductor companies like Infineon Technologies, STMicroelectronics, and NXP Semiconductors within the region fosters a strong environment for research and development, leading to the creation of intelligent, AEC-Q100 qualified components that support complex adaptive lighting systems and enhanced user interfaces.

North America

The North American market is characterized by a strong demand for high-performance and feature-rich vehicles, particularly in the United States. While the overall automotive semiconductor market is significant, the adoption rate of electric vehicles, though growing, has been more measured compared to China and Europe. However, this is changing rapidly with increased investments from domestic automakers. The market demand is heavily skewed towards LED driver ICs that support advanced applications such as autonomous driving sensor systems, high-resolution display panels, and premium adaptive headlights. The stringent vehicle safety regulations enforced by bodies like the NHTSA (National Highway Traffic Safety Administration) compel manufacturers to integrate highly reliable and fault-tolerant components, making quality and long-term durability paramount purchasing factors for OEMs in this region.

South America

The Automotive LED Driver ICs market in South America is emerging and is currently characterized by a higher proportion of cost-sensitive, traditional internal combustion engine vehicles. The adoption of advanced automotive electronics is gradual, often limited to premium vehicle segments. Economic volatility in key markets like Brazil and Argentina can impact automotive production volumes and, consequently, the demand for semiconductor components. However, a slow but steady increase in the penetration of basic LED lighting and infotainment systems in mid-range vehicles presents a growing opportunity for suppliers of entry-level to mid-range LED driver ICs. The market’s growth is tethered to broader economic stability and increasing consumer purchasing power, which would enable a faster transition towards vehicles with more electronic content.

Middle East & Africa

This region presents a nascent but potential long-term market for Automotive LED Driver ICs. Current demand is primarily driven by the premium and luxury vehicle segments, which are equipped with advanced lighting and display technologies. The harsh environmental conditions, including extreme heat and dust, necessitate components with high durability and wide operating temperature ranges. While large-scale automotive production is limited, the region is a significant importer of vehicles. As urbanization progresses and infrastructure develops, the gradual modernization of vehicle fleets is expected to slowly increase the demand for more sophisticated automotive electronics. The market’s evolution will be closely linked to economic diversification efforts and the development of local automotive assembly and regulations.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Automotive LED Driver ICs markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive LED Driver ICs Market?

-> Automotive LED Driver ICs Market was valued at 336 million in 2024 and is projected to reach US$ 530 million by 2032, at a CAGR of 6.7% during the forecast period.

Which key companies operate in Global Automotive LED Driver ICs Market?

-> Key players include Infineon Technologies, Texas Instruments, NXP Semiconductors, STMicroelectronics, and Toshiba, among others.

What are the key growth drivers?

-> Key growth drivers include global electric vehicle adoption, automotive lighting advancements, and increasing demand for energy-efficient infotainment systems.

Which region dominates the market?

-> Asia-Pacific is the dominant market, with China leading both production and consumption due to its position as the world’s largest electric vehicle market.

What are the emerging trends?

-> Emerging trends include integration of smart lighting systems, development of high-efficiency driver ICs for extended EV range, and advanced thermal management solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...