MARKET INSIGHTS

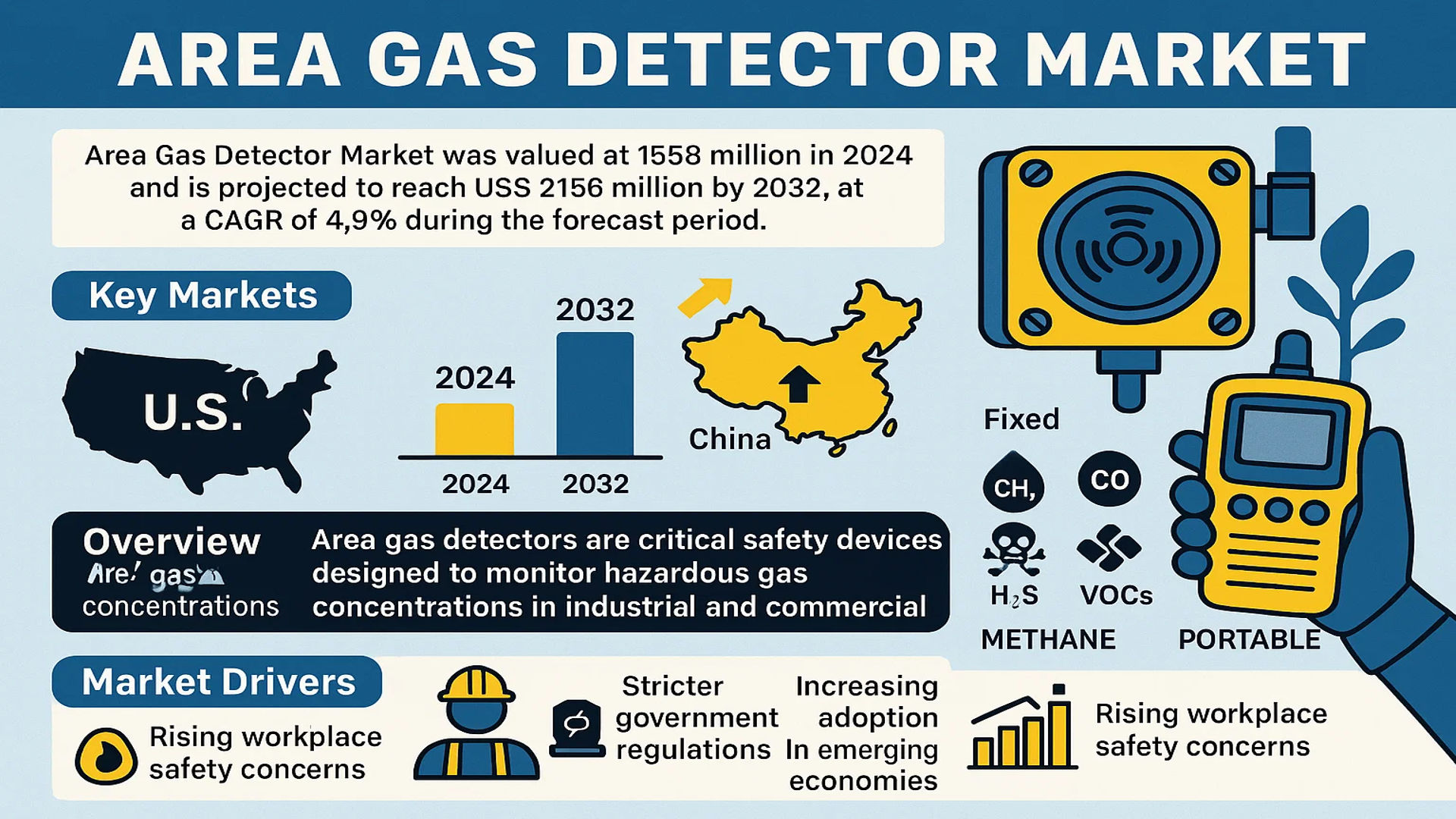

The global Area Gas Detector Market was valued at 1558 million in 2024 and is projected to reach US$ 2156 million by 2032, at a CAGR of 4.9% during the forecast period. The U.S. accounts for a significant share of the market, while China is expected to show robust growth due to increasing industrialization and stringent safety regulations.

Area gas detectors are critical safety devices designed to monitor hazardous gas concentrations in industrial and commercial environments. These systems detect gases such as methane, carbon monoxide, hydrogen sulfide, and volatile organic compounds (VOCs), providing real-time alerts when levels exceed safety thresholds. The detectors are categorized into fixed (wall-mounted) and portable (handheld) variants, with applications spanning oil & gas, mining, manufacturing, and food & beverage industries.

The market growth is driven by rising workplace safety concerns, stricter government regulations, and increasing adoption in emerging economies. Key players like Honeywell, Drager, and MSA dominate the industry, offering advanced detection technologies such as infrared, electrochemical, and catalytic sensors. In 2024, these top five companies collectively held a substantial revenue share, with continuous R&D investments enhancing product accuracy and connectivity features.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Industrial Safety Regulations Fuel Market Expansion

Global industrial safety regulations have intensified in recent years, mandating the deployment of area gas detectors across high-risk facilities. Over 60 countries now enforce strict workplace safety standards requiring continuous gas monitoring in oil refineries, chemical plants, and mining operations. For instance, recent updates to the Occupational Safety and Health Administration (OSHA) standards in the United States have expanded monitoring requirements for hydrogen sulfide and methane detection. These regulatory pressures are compelling industries to upgrade their safety infrastructure, directly accelerating market growth. The petroleum sector alone accounted for nearly 38% of global area gas detector installations in 2023 as companies strive for compliance.

Technological Advancements Enhancing Detection Capabilities

The integration of IoT and AI into gas detection systems represents a paradigm shift in monitoring technology. Modern area detectors now offer predictive analytics capabilities, with some advanced models demonstrating 99.7% detection accuracy for toxic gases. Wireless connectivity has expanded deployment flexibility, reducing installation costs by approximately 25% compared to traditional wired systems. Major manufacturers have introduced detectors with extended sensor lifespans exceeding 5 years, significantly lowering total cost of ownership. These innovations are particularly transformative for the manufacturing sector, where real-time data integration with plant control systems is becoming standard practice.

Growth in Hazardous Industries Driving Equipment Demand

The global expansion of oil & gas exploration activities, particularly in offshore locations, has created substantial demand for robust gas detection solutions. With offshore rig deployments projected to increase by 18% between 2024-2030, the need for explosion-proof area monitors is becoming critical. Similarly, the chemical manufacturing sector’s growth across Asia-Pacific markets is driving double-digit annual demand increases for fixed gas detectors. Food processing facilities are also adopting advanced ammonia detection systems as refrigeration safety standards tighten worldwide. This broad-based industrial expansion across multiple hazardous environments ensures sustained market momentum.

MARKET RESTRAINTS

High Initial Costs Limit Adoption in Emerging Markets

While safety regulations drive adoption in developed nations, price sensitivity significantly impacts market penetration in emerging economies. A complete area monitoring system installation can cost between $5,000-$50,000 depending on configuration, placing it beyond reach for many small and medium enterprises in developing regions. Maintenance expenses further compound this challenge, with annual calibration and sensor replacement costs averaging 15-20% of the initial investment. These financial barriers have resulted in adoption rates below 30% in Southeast Asian industrial facilities, despite growing safety awareness.

Technical Limitations in Extreme Environments

Current gas detection technologies face performance challenges in certain industrial conditions. High humidity environments exceeding 95% RH can reduce sensor accuracy by up to 40% in some detector models. Extremely low temperatures below -40°F (-40°C) similarly impact device reliability, creating coverage gaps in arctic oil fields and cold storage facilities. Even advanced electrochemical sensors experience cross-sensitivity issues between similar gas compounds, potentially generating false alarms. These technical constraints require ongoing research investment to expand operational boundaries while maintaining detection precision.

MARKET CHALLENGES

Cybersecurity Risks in Connected Detection Systems

The transition to networked gas monitoring solutions introduces critical cybersecurity vulnerabilities that manufacturers must address. Industrial facilities have reported a 220% increase in cyberattack attempts on safety systems since 2020. Compromised area detectors could either fail to alert during gas leaks or trigger false shutdowns, both carrying severe safety and financial consequences. Developing secure communication protocols without sacrificing real-time responsiveness remains a significant engineering challenge. The industry faces mounting pressure to implement robust encryption while maintaining system simplicity for operators.

Workforce Skill Gap in System Maintenance

The technical sophistication of modern area gas detectors has outpaced the availability of qualified maintenance personnel. Industry surveys indicate only 45% of facility technicians possess adequate training to properly calibrate and troubleshoot advanced monitoring systems. This skills shortage leads to improper maintenance practices that degrade system reliability over time. Manufacturers are responding with augmented reality-assisted maintenance guides and certified training programs, but the workforce development challenge persists across global markets.

MARKET OPPORTUNITIES

Smart City Infrastructure Creating New Application Horizons

Urban area gas monitoring represents an emerging frontier for detection technology. Underground parking garages, wastewater treatment plants, and public utility tunnels increasingly incorporate fixed gas detectors as part of smart city initiatives. This municipal application sector grew 27% annually from 2020-2023 and shows continued strong potential. Some forward-thinking cities have begun integrating gas detection data with emergency response systems, enabling faster incident resolution. The global smart cities market is projected to invest over $20 billion in environmental monitoring solutions by 2028, presenting substantial growth opportunities for area detector manufacturers.

Miniaturization Enabling New Product Categories

Advancements in microsensor technology are enabling the development of compact, cost-effective area monitors suitable for small commercial spaces. New MEMS-based detectors weighing less than 500 grams now offer detection capabilities approaching larger industrial units. This miniaturization is opening previously inaccessible market segments including restaurants, laboratories, and small manufacturing workshops. Portable area monitors with extended battery life are also gaining traction for temporary work sites, with the construction sector accounting for 18% of portable detector sales growth in 2023.

Green Energy Transition Driving Innovation

The shift toward hydrogen economy and renewable energy infrastructure creates demand for specialized gas detection solutions. Hydrogen fuel facilities require detectors capable of identifying leaks at concentrations as low as 1% of the lower explosive limit (LEL). Similarly, biogas plants necessitate robust monitoring for methane and hydrogen sulfide mixtures. These emerging applications are spurring development of novel sensor technologies, with the hydrogen detection segment projected to grow at 32% CAGR through 2030. Manufacturers investing in these niche applications stand to gain first-mover advantages in rapidly evolving energy markets.

AREA GAS DETECTOR MARKET TRENDS

Technological Advancements in IoT and Wireless Connectivity Drive Market Growth

The global Area Gas Detector market is witnessing significant growth, driven by advancements in Internet of Things (IoT) and wireless connectivity. Modern gas detectors now feature real-time remote monitoring, data logging, and cloud-based analytics, enabling predictive maintenance and enhanced workplace safety. For instance, smart gas detectors with integrated AI algorithms can detect anomalies in gas concentrations and send automated alerts, reducing response times by up to 60%. The increasing adoption of Industry 4.0 in sectors like oil & gas and manufacturing further accelerates demand for connected gas detection systems.

Other Trends

Stringent Government Safety Regulations

Stricter workplace safety regulations, particularly in North America and Europe, are compelling industries to upgrade gas detection systems. Regulatory bodies such as OSHA and the EU’s ATEX directives mandate the use of fixed and portable gas detectors in hazardous environments. Compliance with these standards has contributed to a 15% annual increase in installations across key industrial sectors. Companies are increasingly investing in multi-gas detectors and explosion-proof models to meet these requirements.

Rising Demand from Oil & Gas and Mining Sectors

The oil & gas industry remains the largest end-user of area gas detectors, accounting for over 35% of global market revenue. The expansion of shale gas exploration in the U.S. and LNG projects in the Middle East is fueling demand for advanced detection systems. Similarly, the mining sector requires robust gas monitoring to prevent methane-related hazards, with underground mines increasingly deploying fixed gas detection networks. Emerging economies in Asia-Pacific and Latin America are also witnessing higher adoption due to industrial safety awareness programs.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Leaders and Innovators Drive Market Expansion Through Strategic Investments

The global area gas detector market features a dynamic and moderately consolidated competitive environment, with established multinational corporations competing alongside regional specialists. Honeywell International Inc. emerges as the dominant player, leveraging its century-old expertise in industrial safety solutions. The company’s extensive portfolio of fixed and portable gas detection systems accounts for approximately 18% of global market revenue as of 2024, with particularly strong positions in North American oil & gas and chemical sectors.

Dragerwerk AG & Co. KGaA follows closely, dominating European markets with its technologically advanced infrared and electrochemical detection systems. The German manufacturer has strengthened its market position through strategic acquisitions, including the 2023 purchase of a Brazilian safety equipment firm to expand its Latin American footprint. Similarly, MSA Safety Incorporated maintains robust market share through its innovative connected safety platform, which integrates area monitoring with cloud-based data analytics.

Japanese firm Riken Keiki Co., Ltd. leads innovation in compact detection technologies, holding numerous patents for miniaturized sensors that maintain high accuracy. Their recent partnerships with Southeast Asian industrial plants have driven significant growth in emerging markets. Meanwhile, Industrial Scientific Corporation (now part of Fortive) continues to pioneer wireless area monitoring networks, with its iNet platform becoming an industry standard for large-scale facility monitoring.

The competitive intensity is further heightened by Chinese manufacturers like Shenzhen ExSAF Electronics and Chengdu Action Electronics, who are gaining traction through cost-effective solutions tailored for domestic manufacturing and energy sectors. These regional players collectively account for over 30% of Asia-Pacific market volume, challenging established Western brands in price-sensitive segments.

List of Key Area Gas Detector Companies Profiled

- Honeywell International Inc. (U.S.)

- Dragerwerk AG & Co. KGaA (Germany)

- MSA Safety Incorporated (U.S.)

- Riken Keiki Co., Ltd. (Japan)

- Industrial Scientific Corporation (U.S.)

- 3M Company (U.S.)

- New Cosmos Electric Co., Ltd. (Japan)

- Shenzhen ExSAF Electronics Co., Ltd. (China)

- Johnson Controls International plc (Ireland)

- Emerson Electric Co. (U.S.)

Segment Analysis:

By Type

Wall-Mounted Segment Leads Due to Industrial Safety Compliance Requirements

The market is segmented based on type into:

- Wall Mounted

- Hand Held

- Portable

- Fixed

- Others

By Application

Oil and Gas Sector Dominates with High Demand for Leak Detection

The market is segmented based on application into:

- Oil and Gas

- Mining

- Manufacturing Industry

- Food and Beverage

- Others

By Technology

Electrochemical Sensors Gain Preference for Multi-Gas Detection Capabilities

The market is segmented based on technology into:

- Electrochemical

- Infrared

- Catalytic

- Semiconductor

- Others

By Gas Type

Combustible Gas Detection Remains Critical Across Industries

The market is segmented based on gas type detected into:

- Combustible Gases

- Toxic Gases

- Oxygen

- Carbon Monoxide

- Others

Regional Analysis: Area Gas Detector Market

Asia-Pacific

The Asia-Pacific region dominates the global area gas detector market, accounting for the highest revenue share due to rapid industrialization and stringent workplace safety regulations in countries like China, India, and Japan. China leads the market with over 35% of regional demand, driven by its vast manufacturing sector and expanding oil & gas infrastructure. India’s market is growing at over 6% CAGR, fueled by government initiatives like the ‘Make in India’ campaign and increasing foreign investments in chemical and petrochemical plants. Japan and South Korea remain key markets for advanced detection technologies, with a strong emphasis on IoT-enabled and wireless gas detectors in smart factories.

North America

North America, particularly the U.S., is a mature yet growing market for area gas detectors, with stringent OSHA and EPA regulations mandating gas safety compliance in industries. The U.S. alone contributes nearly 25% of global sales, driven by the oil & gas sector’s demand for explosion-proof and multi-gas detectors. Canada’s mining industry further boosts adoption, while Mexico sees steady growth from chemical manufacturing plants. Technological advancements, such as AI-driven predictive maintenance features, are gaining traction, with companies like Honeywell and MSA leading innovation.

Europe

Europe’s market is characterized by strict adherence to ATEX and IECEx safety standards, particularly in Germany, the UK, and France. The region prioritizes sustainable and low-maintenance detectors, with a shift toward battery-operated and solar-powered models in offshore oil rigs and renewable energy facilities. Germany remains the largest consumer, while Eastern Europe shows potential with increasing industrial automation. The EU’s Green Deal policies are also accelerating the replacement of outdated systems with eco-friendly alternatives.

Middle East & Africa

The Middle East, led by Saudi Arabia and the UAE, is a high-growth market due to massive oil & gas projects and investments in smart city infrastructure. Portable gas detectors are widely used in refineries, while fixed systems dominate in petrochemical zones. Africa’s market is nascent but emerging, with South Africa and Nigeria adopting detectors in mining and power generation. However, political instability and budget constraints in some countries delay large-scale deployments.

South America

Brazil and Argentina drive demand in South America, where mining and agriculture sectors rely heavily on gas detection for ammonia and methane monitoring. Brazil’s pre-salt oil reserves have attracted investments, boosting detector sales. Economic volatility and fragmented regulations, however, hinder faster adoption. Local players like Tecnova are gaining ground with cost-competitive solutions tailored to regional needs.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Area Gas Detector markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Area Gas Detector market was valued at USD 1,558 million in 2024 and is projected to reach USD 2,156 million by 2032, growing at a CAGR of 4.9%.

- Segmentation Analysis: Detailed breakdown by product type (Wall Mounted, Hand Held, Others), application (Oil & Gas, Mining, Manufacturing, Food & Beverage), and end-user industries to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis of key markets including U.S., China, Germany, Japan, and others.

- Competitive Landscape: Profiles of leading market participants including Honeywell, Drager, MSA, Riken Keiki, and Industrial Scientific, covering their product portfolios, market share (top five players held approximately 45% share in 2024), and strategic developments.

- Technology Trends & Innovation: Assessment of emerging technologies including IoT-enabled detectors, wireless monitoring systems, and AI-based predictive analytics in gas detection solutions.

- Market Drivers & Restraints: Analysis of factors such as stringent safety regulations, increasing industrial automation, and growing awareness of workplace safety, along with challenges like high installation costs.

- Stakeholder Analysis: Strategic insights for gas detector manufacturers, system integrators, industrial end-users, and regulatory bodies regarding market opportunities and technological evolution.

The research methodology combines primary interviews with industry experts and secondary data from verified sources, ensuring the accuracy and reliability of market intelligence.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Area Gas Detector Market?

-> Area Gas Detector Market was valued at 1558 million in 2024 and is projected to reach US$ 2156 million by 2032, at a CAGR of 4.9% during the forecast period.

Which key companies operate in Global Area Gas Detector Market?

-> Key players include Honeywell, Drager, MSA, Riken Keiki, Industrial Scientific, 3M, New Cosmos Electric, and Johnson Controls, among others.

What are the key growth drivers?

-> Key growth drivers include stringent workplace safety regulations, increasing industrialization in emerging economies, and technological advancements in gas detection systems.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is expected to exhibit the highest growth rate during the forecast period.

What are the emerging trends?

-> Emerging trends include integration of IoT and cloud connectivity in gas detectors, development of multi-gas detection systems, and increasing adoption in food processing facilities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...