MARKET INSIGHTS

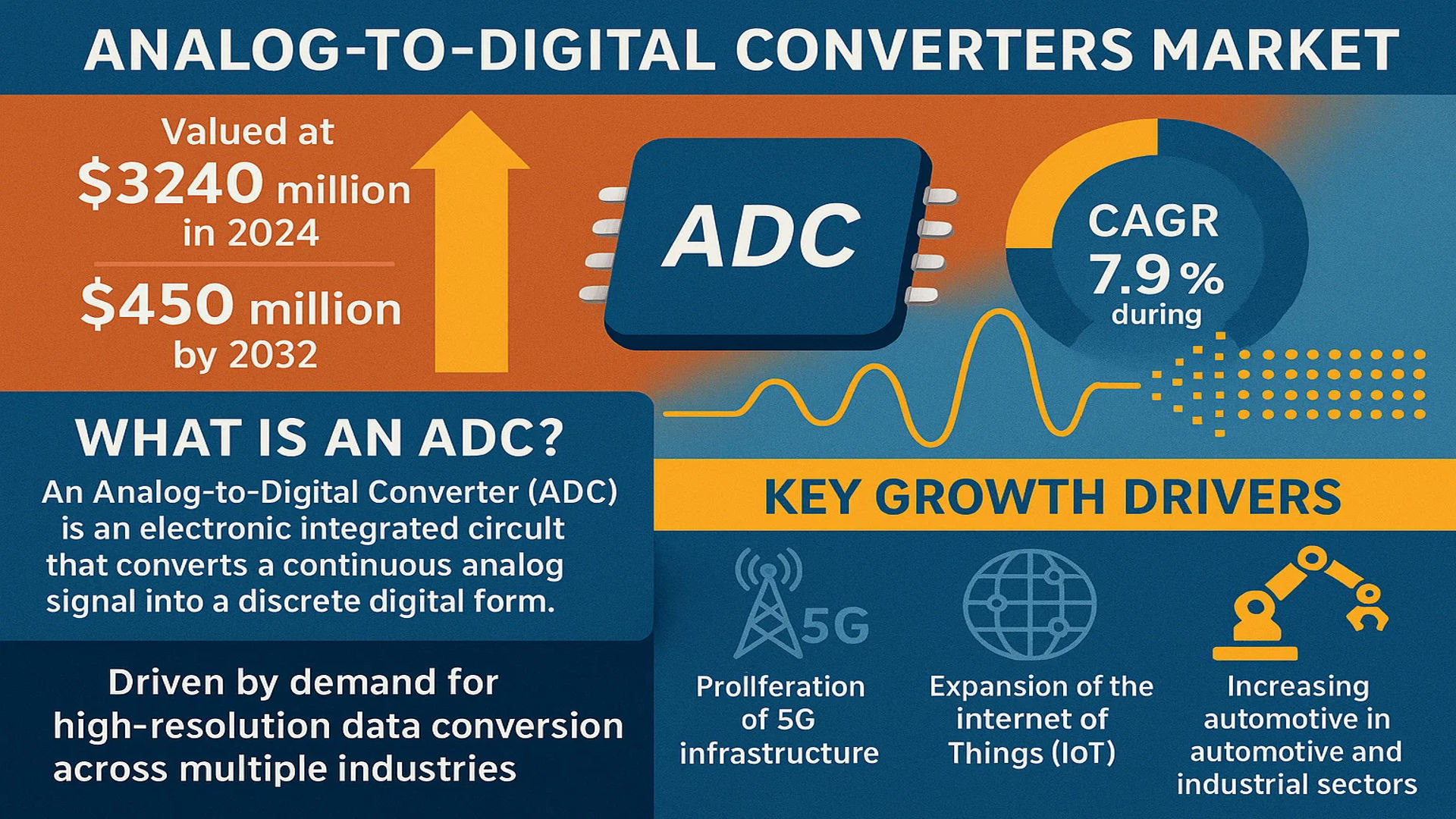

The global Analog-to-Digital Converters Market was valued at 3240 million in 2024 and is projected to reach US$ 5450 million by 2032, at a CAGR of 7.9% during the forecast period.

An Analog-to-Digital Converter (ADC) is a critical electronic integrated circuit that transforms a continuous analog signal into a discrete digital form. This conversion provides an essential link between the analog world of sensors and transducers and the digital world of signal processing, data handling, and computing. ADCs are ubiquitous in modern electronics, found in applications ranging from digital voltmeters and smartphones to industrial control systems and medical imaging equipment.

The market’s robust growth is driven by the escalating demand for high-resolution data conversion across multiple industries. Key growth drivers include the proliferation of 5G infrastructure, the expansion of the Internet of Things (IoT), and increasing automation in automotive and industrial sectors. The competitive landscape is highly concentrated, with Analog Devices Inc. (ADI) leading the market with a 56% revenue share in 2024, followed by Texas Instruments (22%) and Maxim Integrated (6%). These key players continuously drive innovation, focusing on developing ADCs with higher sampling rates, improved power efficiency, and greater integration to meet the evolving demands of next-generation electronic systems.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of IoT and Connected Devices to Fuel ADC Demand

The exponential growth of the Internet of Things (IoT) ecosystem represents a primary catalyst for the analog-to-digital converters market. IoT devices, which require seamless conversion of real-world analog signals into digital data, are being deployed across consumer, industrial, and commercial applications at an unprecedented rate. With over 15 billion active IoT devices globally and projections indicating this number will surpass 29 billion by 2030, the demand for high-performance ADCs continues to accelerate. These components are fundamental in sensors, smart devices, and edge computing systems that form the backbone of IoT infrastructure. The increasing adoption of Industry 4.0 practices, which rely heavily on sensor data digitization for automation and predictive maintenance, further amplifies this demand. As manufacturing facilities worldwide upgrade to smart factory configurations, the requirement for precision data acquisition systems drives substantial ADC integration across production lines and quality control systems.

Advancements in Automotive Electronics to Accelerate Market Expansion

The automotive industry’s rapid transformation toward electrification and autonomous driving systems has created substantial growth opportunities for analog-to-digital converters. Modern vehicles incorporate hundreds of sensors that monitor everything from battery performance and motor efficiency to environmental conditions and passenger safety systems. The transition to electric vehicles, which is progressing at a compound annual growth rate of approximately 19%, requires sophisticated battery management systems that utilize high-resolution ADCs for precise voltage and current monitoring. Additionally, advanced driver-assistance systems (ADAS) rely on multiple data conversion points for radar, lidar, and camera systems that enable autonomous functionality. With the average premium vehicle now containing over $600 worth of semiconductor content, of which data conversion components represent a significant portion, the automotive sector has become a major revenue driver for ADC manufacturers. The increasing regulatory requirements for vehicle safety and emissions monitoring further necessitate advanced data acquisition capabilities that depend on reliable analog-to-digital conversion.

5G Infrastructure Deployment to Drive High-Speed ADC Requirements

The global rollout of 5G networks represents a significant technological advancement that directly impacts the analog-to-digital converters market. 5G infrastructure requires sophisticated base station equipment capable of handling massive data throughput with minimal latency, creating substantial demand for high-speed ADCs that can operate at microwave and millimeter-wave frequencies. The transition to 5G involves deploying small cells, massive MIMO systems, and beamforming technologies that all rely on advanced data conversion components. With telecommunications operators worldwide investing over $200 billion annually in 5G infrastructure development, the market for high-performance ADCs used in radio frequency front-end modules has experienced remarkable growth. These converters enable the precise signal processing necessary for maintaining signal integrity across complex network architectures. Furthermore, the ongoing development of 6G technologies, which will operate at even higher frequencies, ensures sustained investment in advanced data conversion solutions for telecommunications infrastructure.

MARKET CHALLENGES

Design Complexity and Power Consumption Constraints to Challenge ADC Implementation

The analog-to-digital converters market faces significant technical challenges related to increasing design complexity and power efficiency requirements. As applications demand higher resolution and sampling rates, ADC designs must overcome inherent trade-offs between speed, accuracy, and power consumption. The development of nanometer-scale semiconductor technologies introduces additional complications, including increased noise susceptibility and reduced voltage headroom, which adversely affect converter performance. Designing ADCs for battery-powered IoT devices requires achieving sampling rates above 100 MSPS while maintaining power consumption below 100 milliwatts, creating substantial engineering challenges. Additionally, the integration of mixed-signal components in system-on-chip designs introduces substrate noise and cross-talk issues that can degrade ADC performance. These technical hurdles necessitate extensive research and development investments, with leading manufacturers allocating approximately 15-20% of their revenue to advanced development programs aimed at overcoming these limitations.

Other Challenges

Supply Chain Vulnerabilities

The global semiconductor supply chain disruptions that began in 2020 continue to present significant challenges for ADC manufacturers and consumers. Geopolitical tensions, trade restrictions, and manufacturing capacity constraints have created volatility in component availability and pricing. The specialized nature of analog and mixed-signal semiconductor manufacturing, which requires mature process technologies often produced in older fabrication facilities, has been particularly affected by these disruptions. Many ADC products rely on semiconductor processes between 180nm and 65nm nodes, production capacity for which has been redirected to more advanced nodes in recent years. This has created supply constraints that are projected to persist through 2025, affecting delivery timelines and production costs for end products incorporating analog-to-digital converters.

Technical Standardization Issues

The absence of universal technical standards across different application segments creates interoperability challenges that hinder market growth. Various industries implement proprietary data acquisition protocols and interface standards, requiring ADC manufacturers to develop application-specific solutions rather than standardized products. This fragmentation increases development costs and limits economies of scale, particularly for high-performance converters used in specialized industrial and medical applications. The lack of standardization also complicates system integration, as engineers must address compatibility issues between ADCs and downstream digital processing components, potentially delaying product development cycles and increasing implementation costs.

MARKET RESTRAINTS

High Development Costs and Extended Design Cycles to Limit Market Accessibility

The analog-to-digital converters market experiences significant restraints due to the substantial financial and temporal investments required for product development. Designing high-performance ADCs involves complex analog circuitry that doesn’t benefit from digital scaling laws, requiring specialized expertise and extensive validation processes. The development cycle for a new ADC architecture typically spans 18-36 months, with engineering costs frequently exceeding $5 million for advanced designs. This high barrier to entry limits market participation to established semiconductor companies with sufficient financial resources and technical capabilities. Additionally, the testing and characterization of analog components require sophisticated equipment and controlled environments, further increasing development expenses. These factors collectively restrain market growth by limiting innovation from smaller players and extending the time-to-market for new products, particularly in rapidly evolving application segments where technological requirements change frequently.

MARKET OPPORTUNITIES

Emerging Medical Diagnostic Applications to Create New Growth Frontiers

The healthcare sector presents substantial growth opportunities for analog-to-digital converters, particularly in medical imaging and diagnostic equipment. Advanced medical devices such as digital X-ray systems, MRI machines, and portable ultrasound equipment require high-resolution ADCs with sampling rates exceeding 100 MSPS and resolution greater than 16 bits. The global medical imaging market, valued at approximately $35 billion and growing at 5% annually, drives continuous demand for improved data acquisition components. Additionally, the proliferation of wearable health monitors and point-of-care diagnostic devices creates opportunities for low-power, high-integration ADCs that can operate in battery-constrained environments. The increasing adoption of telemedicine and remote patient monitoring systems further expands the addressable market for data conversion components, as these systems rely on accurate signal acquisition from various biomedical sensors. This convergence of medical technology and digital health solutions represents a significant growth vector for ADC manufacturers capable of meeting the stringent reliability and performance requirements of healthcare applications.

Artificial Intelligence Integration to Open New Application Horizons

The integration of artificial intelligence and machine learning capabilities across various industries creates compelling opportunities for advanced analog-to-digital converters. AI systems require massive datasets for training and inference, much of which originates from analog sensors monitoring physical environments. High-performance ADCs enable the precise data acquisition necessary for effective machine learning algorithms, particularly in applications such as computer vision, natural language processing, and predictive analytics. The edge AI segment, which involves deploying intelligence directly in devices rather than cloud platforms, particularly benefits from optimized data conversion solutions that can preprocess analog signals before digital analysis. With edge AI hardware investments projected to grow at approximately 20% annually through 2030, the demand for ADCs tailored for neural network applications represents a significant opportunity. These converters must provide the necessary bandwidth and resolution while maintaining power efficiency suitable for deployment in energy-constrained edge computing environments.

Renewable Energy Systems to Drive Precision Measurement Requirements

The global transition toward renewable energy sources creates substantial opportunities for analog-to-digital converters in power management and monitoring applications. Solar inverters, wind turbine control systems, and battery storage installations require precise measurement of voltage, current, and power quality parameters, all of which depend on high-accuracy ADCs. The renewable energy sector, which is experiencing annual growth rates exceeding 8%, utilizes sophisticated power electronics that incorporate multiple data conversion points for maximum power point tracking, grid synchronization, and fault detection. These systems demand ADCs with resolution up to 24 bits and sampling rates sufficient to capture harmonic distortions and transient events in power systems. Additionally, smart grid implementations and electric vehicle charging infrastructure rely on advanced metering systems that incorporate multiple high-performance data conversion channels. This convergence of energy transformation and digitalization drives continuous innovation in ADC technologies tailored for power electronics applications, representing a significant growth opportunity for manufacturers serving this sector.

ANALOG-TO-DIGITAL CONVERTERS MARKET TRENDS

Proliferation of High-Resolution Data Acquisition Systems to Emerge as a Trend in the Market

The relentless demand for higher precision and faster data conversion is fundamentally reshaping the ADC landscape. This trend is primarily fueled by the exponential growth in applications requiring ultra-high-resolution signal processing, such as scientific instrumentation, medical imaging, and next-generation communication systems like 5G infrastructure. The market is witnessing a significant shift towards ADCs with resolutions exceeding 24 bits and sampling rates soaring into the gigahertz range. For instance, the adoption of high-speed ADCs in 5G massive MIMO base stations is critical for processing wide bandwidth signals, with the global rollout of 5G networks acting as a colossal catalyst. Furthermore, advancements in semiconductor process technologies, such as finer lithography nodes, are enabling the development of these highly integrated, power-efficient converters that meet the stringent performance requirements of modern electronic systems.

Other Trends

Automotive Electrification and Automation

The automotive sector represents a powerhouse of growth for ADC components, driven squarely by the twin engines of electrification and the progression towards autonomous driving. Modern vehicles are essentially data centers on wheels, equipped with a vast array of sensors—LiDAR, radar, ultrasonic sensors, and battery management systems—that all rely on high-performance ADCs to translate analog real-world data into actionable digital information. The number of ADCs per vehicle is increasing dramatically; a single electric vehicle’s battery management system alone may utilize dozens of channels for precise voltage and current monitoring. This surge is directly correlated with the projected expansion of the advanced driver-assistance systems (ADAS) market, which necessitates unparalleled data accuracy for functions like object detection and collision avoidance.

Integration of Artificial Intelligence at the Edge

A pivotal trend accelerating ADC innovation is the integration of artificial intelligence directly into edge devices, creating a substantial demand for low-power, high-efficiency data conversion solutions. Because AI and machine learning algorithms process vast streams of sensor data in real-time, the ADC serves as the critical first link in the signal chain. This has led to the development of smarter, more integrated ADCs that feature on-chip digital signal processing (DSP) and built-in functions for filtering and data preprocessing, thereby reducing the computational load on the main processor and minimizing system latency and power consumption. This is particularly crucial for battery-powered Internet of Things (IoT) devices, industrial IoT sensors, and wearable health monitors, where efficient data acquisition directly impacts device longevity and functionality. The push towards more intelligent edge processing is ensuring that the ADC is no longer just a simple converter but an increasingly sophisticated component within a smarter system architecture.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Positioning Drive Market Leadership

The global Analog-to-Digital Converters (ADC) market exhibits a consolidated competitive structure, dominated by a few major semiconductor giants while also featuring several specialized and emerging players. Analog Devices, Inc. (ADI) firmly leads the market, commanding a remarkable 56% revenue share in 2024. This dominance is largely attributed to their extensive and technologically advanced product portfolio, which spans high-speed, high-resolution, and precision ADCs catering to demanding applications in automotive, industrial, and communications sectors. Their strong global distribution network and longstanding relationships with key OEMs further cement their top position.

Texas Instruments (TI), holding a significant 22% market share, follows as a formidable competitor. Their strength lies in a broad portfolio that balances performance with cost-effectiveness, making their solutions highly attractive for high-volume consumer electronics and automotive applications. Meanwhile, Maxim Integrated, which was acquired by Analog Devices in 2021, contributed approximately 6% to the market revenue, bolstering ADI’s overall portfolio, particularly in the automotive and industrial spaces.

Beyond the top three, the competitive landscape includes other established players who are actively investing in research and development to capture niche segments. Companies like STMicroelectronics (STM) and ON Semiconductor are strengthening their positions through strategic product launches focused on energy efficiency and integration, targeting the growing Internet of Things (IoT) and industrial automation markets. Their growth is fueled by expansion into emerging economies and partnerships with regional manufacturers.

Furthermore, Microchip Technology and NXP Semiconductors are enhancing their market presence through significant investments in developing ADCs for automotive and secure connectivity applications. These companies are focusing on innovation in low-power and mixed-signal solutions, ensuring they remain competitive as the demand for smarter and more connected devices continues to rise globally.

List of Key Analog-to-Digital Converter Companies Profiled

- Analog Devices, Inc. (ADI) (U.S.)

- Texas Instruments Inc. (TI) (U.S.)

- Maxim Integrated (Part of Analog Devices) (U.S.)

- Renesas Electronics Corporation (Japan) – (Note: Acquired Intersil in 2017)

- STMicroelectronics (STM) (Switzerland)

- ON Semiconductor (U.S.)

- Microchip Technology Inc. (U.S.)

- NXP Semiconductors N.V. (Netherlands)

- Cirrus Logic, Inc. (U.S.)

- Xilinx, Inc. (Part of AMD) (U.S.)

Segment Analysis:

By Type

SAR ADC Segment Commands Significant Market Share Due to Optimal Balance of Speed, Power, and Resolution

The market is segmented based on type into:

- Pipeline ADC

- SAR ADC

- Subtypes: Successive Approximation Register ADCs, often featuring 8-bit to 18-bit resolution

- SigmaDelta ADC

- Subtypes: High-resolution, oversampling converters primarily used for audio and precision measurement

- Flash ADC

- Subtypes: Ultra-high-speed converters used in applications like radar and high-frequency signal processing

- Others Type ADC

By Application

Consumer Electronics Segment Leads Due to Pervasive Use in Smartphones, Tablets, and Wearable Devices

The market is segmented based on application into:

- Consumer Electronics

- Communications

- Automotive

- Industrials

By Resolution

High-Resolution ADCs (16-bit and Above) are Gaining Traction for Precision Measurement and Industrial Automation

The market is segmented based on resolution into:

- 8-bit to 12-bit ADCs

- 14-bit to 16-bit ADCs

- 18-bit and Above ADCs

By Sampling Rate

High-Speed ADCs (Above 1 MSPS) are Critical for 5G Infrastructure and Advanced Communication Systems

The market is segmented based on sampling rate into:

- Low-Speed ADCs (Up to 1 MSPS)

- Medium-Speed ADCs (1 MSPS to 100 MSPS)

- High-Speed ADCs (Above 100 MSPS)

Regional Analysis: Analog-to-Digital Converters Market

Asia-Pacific

The Asia-Pacific region dominates the global ADC market, accounting for approximately 48% of total revenue share in 2024. This leadership position is driven by massive electronics manufacturing hubs in China, Taiwan, and South Korea, coupled with robust consumer electronics demand across India and Southeast Asia. The region benefits from extensive semiconductor fabrication facilities and strong government support for technological advancement, particularly in 5G infrastructure and industrial automation. While cost-competitive SAR and Pipeline ADCs remain prevalent for mass-market applications, there is growing adoption of high-resolution SigmaDelta converters for precision instruments and automotive systems. The Chinese market alone represents over 30% of regional demand, fueled by domestic semiconductor policies and expanding electric vehicle production.

North America

North America represents the second-largest ADC market, characterized by high-value applications in aerospace, defense, and medical equipment. The region’s technological sophistication drives demand for high-speed Flash ADCs and precision SigmaDelta converters, particularly in test and measurement equipment and advanced communication systems. Major players like Analog Devices and Texas Instruments maintain significant manufacturing and R&D presence in the United States, benefiting from strong intellectual property protection and substantial defense contracts. Recent developments include increased ADC integration in automotive LiDAR systems and next-generation wireless infrastructure, supported by both private investment and government initiatives like the CHIPS Act.

Europe

Europe maintains a strong position in the ADC market, particularly in automotive and industrial applications. Germany leads regional demand due to its robust automotive industry and Industry 4.0 initiatives, requiring high-performance ADCs for motor control, sensor interfaces, and automation systems. The region shows growing emphasis on energy-efficient ADC designs compliant with EU environmental standards, with increasing adoption in renewable energy systems and smart grid applications. European semiconductor companies like STMicroelectronics and NXP focus on developing ADCs with enhanced signal integrity and lower power consumption, catering to the region’s stringent technical requirements and quality standards.

South America

The South American ADC market is emerging, with growth primarily driven by industrial automation and consumer electronics adoption. Brazil represents the largest market in the region, though economic volatility sometimes affects investment in advanced semiconductor technologies. Most demand centers on cost-effective SAR and Pipeline ADCs for consumer devices and basic industrial applications, with limited adoption of high-end converters. The market shows potential for expansion as manufacturing capabilities improve and telecommunications infrastructure develops, though it remains constrained by import dependencies and limited local semiconductor production.

Middle East & Africa

This region represents the smallest but growing segment of the global ADC market. Development is primarily driven by telecommunications infrastructure projects and oil & gas industry automation. The United Arab Emirates and Saudi Arabia lead ADC adoption through smart city initiatives and industrial modernization programs. Market growth is tempered by limited local semiconductor manufacturing and reliance on imports, though increasing investments in technological infrastructure suggest long-term potential. Most demand focuses on mid-range ADCs for communication equipment and industrial control systems rather than cutting-edge applications.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Semiconductor and Electronics markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Analog-to-Digital Converters Market?

-> Analog-to-Digital Converters Market was valued at 3240 million in 2024 and is projected to reach US$ 5450 million by 2032, at a CAGR of 7.9% during the forecast period.

Which key companies operate in Global Analog-to-Digital Converters Market?

-> Key players include Analog Devices Inc. (ADI), Texas Instruments (TI), Maxim Integrated (now part of ADI), STMicroelectronics (STM), ON Semiconductor, Microchip Technology, NXP Semiconductors, Cirrus Logic, and Xilinx, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-resolution data conversion in consumer electronics, expansion of 5G infrastructure, automotive electrification, and industrial automation.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing region, driven by electronics manufacturing hubs in China, South Korea, and Taiwan, while North America remains a key market due to advanced technological adoption.

What are the emerging trends?

-> Emerging trends include integration of AI for smart signal processing, development of ultra-low-power ADCs for IoT devices, and advancements in high-speed data conversion for 5G and automotive applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...