MARKET INSIGHTS

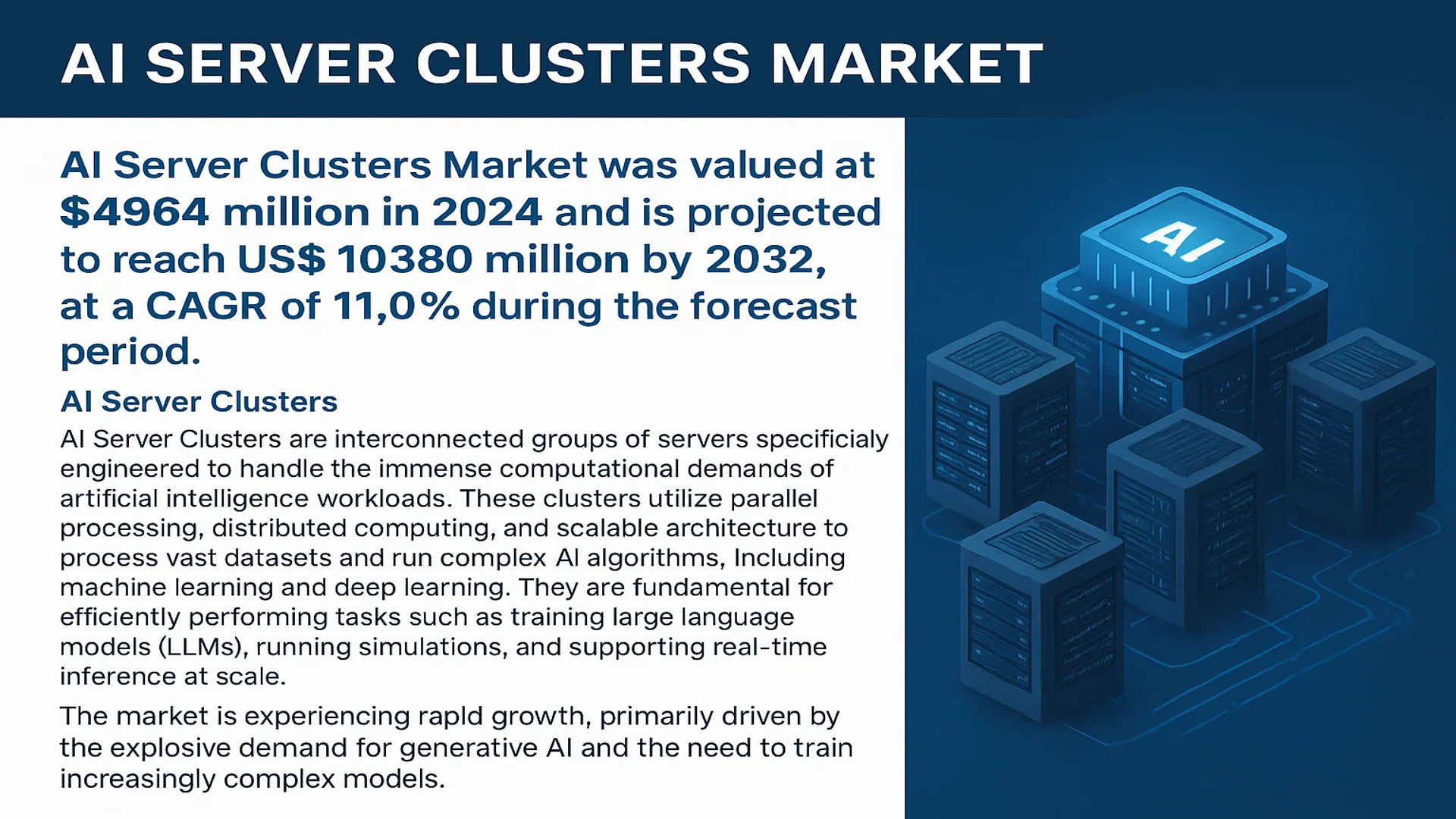

The global AI Server Clusters Market was valued at 4964 million in 2024 and is projected to reach US$ 10380 million by 2032, at a CAGR of 11.0% during the forecast period.

AI Server Clusters are interconnected groups of servers specifically engineered to handle the immense computational demands of artificial intelligence workloads. These clusters utilize parallel processing, distributed computing, and scalable architecture to process vast datasets and run complex AI algorithms, including machine learning and deep learning. They are fundamental for efficiently performing tasks such as training large language models (LLMs), running simulations, and supporting real-time inference at scale.

The market is experiencing rapid growth, primarily driven by the explosive demand for generative AI and the need to train increasingly complex models. This growth is further fueled by substantial investments from major cloud providers and technology firms expanding their AI infrastructure. For instance, in 2024, companies like Microsoft and Google announced multi-billion dollar investments to scale their AI data center capabilities. NVIDIA, a dominant force with its GPU-based systems, continues to lead the market, while other key players include AWS, Meta, and a growing ecosystem of specialized providers like Cerebras and CoreWeave.

MARKET DYNAMICS

MARKET DRIVERS

Exponential Growth in AI Workloads and Data Processing Demands

The global AI Server Clusters market is experiencing robust growth primarily driven by the exponential increase in AI workloads across industries. The computational requirements for training large language models have grown by a factor of 10 every year since 2010, creating unprecedented demand for high-performance computing infrastructure. AI server clusters, particularly those utilizing GPU-based architectures, have become essential for handling the massive parallel processing needs of deep learning algorithms. The training of advanced AI models now requires clusters with thousands of interconnected processors working simultaneously, driving substantial investments in data center infrastructure. This surge is further accelerated by the widespread adoption of cloud-based AI services and the increasing complexity of neural networks, which demand specialized computing resources that only server clusters can provide efficiently.

Rising Enterprise Adoption of AI Across Multiple Industries

Enterprise adoption of artificial intelligence has become a critical driver for the AI Server Clusters market, with organizations across sectors investing heavily in AI infrastructure. The financial services industry alone is projected to increase its AI infrastructure spending by over 40% annually, driven by algorithmic trading, fraud detection, and personalized banking services. Similarly, the healthcare sector is implementing AI clusters for medical imaging analysis, drug discovery, and genomic sequencing, where processing millions of medical images or genetic sequences requires massive computational power. The automotive industry’s shift toward autonomous vehicles has created demand for AI clusters that can process sensor data and run complex simulation environments. This cross-industry adoption is creating a sustainable growth pattern for the market, with enterprises recognizing that dedicated AI infrastructure is essential for maintaining competitive advantage and innovation capabilities.

Advancements in Hardware Technology and Cluster Architecture

Technological advancements in processing units and cluster architecture design are significantly accelerating market growth. The development of specialized AI chips, including GPUs, TPUs, and neural processing units, has dramatically improved the efficiency and performance of AI server clusters. Recent architectural innovations have enabled clusters to achieve near-linear scaling performance, allowing organizations to expand their computing power proportionally with their AI ambitions. The integration of high-speed interconnects such as NVLink and InfiniBand has reduced communication latency between nodes, enabling more efficient distributed training of large models. These technological improvements have made AI clusters more accessible and cost-effective, lowering the barrier to entry for organizations seeking to deploy sophisticated AI solutions without building massive internal expertise in distributed computing systems.

MARKET CHALLENGES

Significant Capital Investment and Operational Costs

The AI Server Clusters market faces substantial challenges related to the high capital expenditure and operational costs associated with deploying and maintaining these systems. A single high-performance AI server can cost upwards of $200,000, while complete clusters often require investments ranging from millions to tens of millions of dollars depending on scale and performance requirements. Beyond the initial hardware investment, organizations face significant ongoing expenses for power consumption, cooling systems, and specialized facility requirements. The energy consumption of large AI clusters can reach several megawatts, creating both financial and environmental sustainability concerns. These cost barriers particularly affect small and medium-sized enterprises and research institutions, limiting broader market adoption and creating a concentration of AI computing power among well-funded technology giants and cloud service providers.

Other Challenges

Technical Complexity and Integration Hurdles

The implementation of AI server clusters involves substantial technical complexity that presents significant challenges for many organizations. Designing optimal cluster architectures requires deep expertise in parallel computing, network topology, and distributed systems. The integration of diverse hardware components, software frameworks, and storage systems creates compatibility issues and performance optimization challenges. Many organizations struggle with the sophisticated orchestration and management software needed to efficiently utilize cluster resources across multiple AI workloads. This technical complexity often leads to underutilization of expensive hardware resources and extended implementation timelines, reducing the return on investment and delaying AI project deployment.

Rapid Technological Obsolescence and Upgrade Cycles

The accelerated pace of hardware innovation creates challenges related to technological obsolescence and frequent upgrade requirements. New generations of AI processors typically offer 2-3 times the performance of previous versions, making existing clusters comparatively inefficient within short timeframes. This rapid advancement forces organizations to make difficult decisions about upgrading existing infrastructure versus deploying new systems, often while previous investments have not yet been fully depreciated. The constant need for upgrades creates financial planning challenges and operational disruptions, as cluster upgrades often require significant downtime and retraining of technical staff on new architectures and software ecosystems.

MARKET RESTRAINTS

Supply Chain Constraints and Component Availability Issues

The AI Server Clusters market faces significant restraints due to ongoing supply chain challenges and component availability issues. The specialized nature of AI processors, particularly high-end GPUs and TPUs, creates manufacturing bottlenecks and extended lead times. The concentration of advanced semiconductor production capabilities in limited geographic regions creates vulnerability to geopolitical tensions and trade restrictions. These supply constraints are exacerbated by the simultaneous demand from multiple sectors including consumer electronics, automotive, and other industrial applications competing for the same manufacturing capacity. The resulting component shortages delay cluster deployments, increase costs, and create uncertainty in project planning, particularly affecting organizations without established relationships with major hardware vendors or cloud providers.

Shortage of Skilled Professionals and Expertise Gap

A critical restraint affecting market growth is the severe shortage of professionals with expertise in AI infrastructure design and cluster management. The specialized knowledge required to design, implement, and optimize AI server clusters encompasses multiple disciplines including hardware architecture, networking, distributed systems, and AI framework optimization. The global shortage of professionals with these combined skills limits the ability of organizations to effectively deploy and utilize AI clusters. Educational institutions struggle to keep pace with the rapidly evolving technology landscape, creating an expertise gap that cannot be quickly filled through traditional training programs. This skills shortage forces organizations to compete aggressively for limited talent, driving up labor costs and delaying project implementations while potentially compromising cluster performance and efficiency due to insufficient operational expertise.

Regulatory and Compliance Considerations in Global Markets

Regulatory frameworks and compliance requirements present additional restraints to the global expansion of AI Server Clusters. Data sovereignty regulations in various jurisdictions require that AI processing and data storage occur within specific geographic boundaries, complicating cluster deployment strategies for multinational organizations. Export controls on high-performance computing technology restrict the transfer of advanced AI clusters across borders, particularly affecting countries subject to technology embargoes. Environmental regulations regarding energy consumption and carbon emissions impact cluster design and location decisions, as large computing facilities face increasing scrutiny regarding their sustainability practices. These regulatory considerations add complexity to cluster deployment planning, increase compliance costs, and may limit the optimal geographical distribution of AI computing resources based on performance considerations alone.

MARKET OPPORTUNITIES

Emerging Edge Computing and Distributed AI Applications

The evolution toward edge computing presents substantial opportunities for the AI Server Clusters market, particularly through the development of smaller, specialized clusters deployed closer to data sources. The integration of 5G networks with edge computing capabilities enables real-time AI processing for applications requiring low latency, such as autonomous vehicles, industrial IoT, and augmented reality systems. This distributed architecture approach creates demand for heterogeneous cluster designs that combine central large-scale clusters with numerous edge deployment units. The edge AI market is projected to grow at approximately 20% annually, driven by applications in manufacturing, retail, and smart cities. This expansion creates opportunities for cluster vendors to develop specialized solutions optimized for edge environments, including ruggedized hardware, energy-efficient designs, and simplified management interfaces for distributed deployment scenarios.

Advancements in Sustainable and Energy-Efficient Computing

Growing emphasis on sustainable computing practices creates significant opportunities for innovation in energy-efficient AI cluster designs. The development of advanced cooling technologies, including liquid immersion cooling and direct-to-chip cooling systems, can reduce cluster energy consumption by 30-40% compared to traditional air cooling methods. Opportunities exist for integrating renewable energy sources directly with computing facilities and developing power management systems that optimize energy usage based on computational demand patterns. The emergence of specialized low-power AI processors designed specifically for efficient inference workloads enables the creation of clusters that deliver high performance with reduced environmental impact. These sustainability-focused innovations address both environmental concerns and operational cost pressures, creating competitive advantages for vendors that can deliver high-performance computing with improved energy efficiency metrics.

Expansion into Emerging Markets and Vertical-Specific Solutions

Significant growth opportunities exist through expansion into emerging geographic markets and the development of vertical-specific AI cluster solutions. Countries across Asia, Latin America, and the Middle East are increasing investments in AI infrastructure as part of national digital transformation initiatives, creating new market segments beyond traditional North American and European strongholds. The development of pre-configured cluster solutions tailored to specific industry requirements—such as healthcare imaging clusters, financial trading clusters, or automotive simulation clusters—enables faster deployment and reduces implementation complexity for vertical markets. These specialized solutions incorporate industry-specific software frameworks, compliance features, and performance optimizations that address particular use cases more effectively than general-purpose clusters. The vertical-specific approach allows vendors to differentiate their offerings and capture premium pricing while providing customers with solutions that deliver immediate value without extensive customization efforts.

AI SERVER CLUSTERS MARKET TRENDS

Accelerated Adoption of GPU-Based Clusters for Complex AI Workloads

The market is witnessing a pronounced shift towards GPU-based AI server clusters, driven by their unparalleled parallel processing capabilities essential for training large language models and deep learning algorithms. This trend is underscored by the fact that the GPU-Based AI Clusters segment is projected to grow at a significant rate, with its market value expected to reach into the multi-billion-dollar range by 2032. The computational intensity of modern AI models, some requiring weeks of training on thousands of interconnected GPUs, makes this architecture indispensable. While initial deployments were dominated by tech giants, the democratization of AI is now pushing this technology into a broader range of enterprises seeking competitive advantages through proprietary AI.

Other Trends

Rise of Hyperscale Cloud Providers as AI Infrastructure Hubs

The growing reliance on cloud-based AI solutions is a primary market driver, with hyperscale providers like AWS, Microsoft Azure, and Google Cloud Platform becoming central hubs for AI compute. These providers offer scalable, on-demand access to massive AI server clusters, eliminating the prohibitive capital expenditure required for private deployments. This has particularly accelerated adoption among small and medium-sized enterprises and startups, enabling them to innovate without upfront infrastructure investment. The cloud segment’s growth is further fueled by the integration of these clusters with managed AI services, providing a complete ecosystem for development and deployment.

Strategic Industry-Specific Customization and Deployment

Beyond generic computing power, a key trend is the strategic, industry-specific customization of AI server clusters. In the automotive sector, for instance, clusters are being optimized for the immense data processing requirements of autonomous vehicle simulation and real-time decision-making. The financial services industry leverages similar clusters for high-frequency trading algorithms and real-time fraud detection systems, where latency is measured in microseconds. This trend towards specialized deployments indicates a maturation of the market, moving from general-purpose computing to tailored solutions that address the unique data, latency, and regulatory challenges of each vertical, thereby unlocking new, high-value applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The competitive landscape of the global AI Server Clusters market is dynamic and semi-consolidated, characterized by a mix of established technology giants, specialized hardware manufacturers, and emerging innovators. NVIDIA Corporation stands as a dominant force, primarily due to its industry-leading GPU technology which serves as the computational backbone for the majority of AI training workloads worldwide. The company’s data center revenue, a key indicator of its AI cluster business, reached a record $18.4 billion in Q1 fiscal 2025, underscoring its significant market influence.

Google and Microsoft also command substantial market share, leveraging their vast cloud infrastructure ecosystems—Google Cloud Platform (GCP) and Microsoft Azure, respectively. Their growth is propelled by integrated offerings that combine proprietary hardware, like Google’s Tensor Processing Units (TPUs) and Microsoft’s Azure Maia AI Accelerator, with comprehensive cloud services, making AI cluster deployment more accessible to enterprises. Furthermore, Amazon Web Services (AWS) remains a critical player, with its custom Inferentia and Trainium chips designed to offer cost-effective AI compute options.

Additionally, these leading companies are aggressively pursuing growth through strategic partnerships, geographical expansion of data center regions, and continuous R&D investments. For instance, NVIDIA’s collaborations with major cloud service providers to host its DGX Cloud platform exemplify efforts to capture a broader customer base by offering AI-as-a-Service.

Meanwhile, specialized firms like Cerebras Systems and Lambda are strengthening their positions by focusing on ultra-high-performance computing solutions tailored for large language model training and scientific research. Their innovative architectures challenge traditional designs, offering unique value propositions in a crowded market. Established hardware vendors such as Hewlett Packard Enterprise (HPE), Dell Technologies, and Lenovo are also expanding their AI-optimized server portfolios through partnerships with chipmakers and software integrations, ensuring they remain relevant to enterprises building on-premises clusters.

List of Key AI Server Clusters Companies Profiled

- NVIDIA Corporation (U.S.)

- Google LLC (Alphabet Inc.) (U.S.)

- Microsoft Corporation (U.S.)

- Amazon Web Services, Inc. (AWS) (U.S.)

- Meta Platforms, Inc. (U.S.)

- OpenAI (U.S.)

- Tesla, Inc. (U.S.)

- Cerebras Systems (U.S.)

- Lambda (U.S.)

- CoreWeave (U.S.)

- Run:ai (Israel)

- Hewlett Packard Enterprise (HPE) (U.S.)

- Supermicro (U.S.)

- Dell Technologies Inc. (U.S.)

- Oracle Corporation (U.S.)

- GigaIO (U.S.)

- Lenovo Group Limited (China)

- Inspur (China)

- Huawei Technologies Co., Ltd. (China)

- Baidu, Inc. (China)

Segment Analysis:

By Type

GPU-Based AI Clusters Segment Dominates the Market Due to Superior Parallel Processing Capabilities for Deep Learning

The market is segmented based on type into:

- GPU-Based AI Clusters

- CPU-Based AI Clusters

- TPU-Based AI Clusters

- Virtual AI Clusters

By Application

IT & Telecom Segment Leads Due to Massive Data Processing Needs for Network Optimization and AI Services

The market is segmented based on application into:

- Automotive

- Industrial Manufacturing

- Financial Services

- IT & Telecom

- Retail & eCommerce

- Entertainment & Media

- Others

Regional Analysis: AI Server Clusters Market

North America

North America, particularly the United States, is the undisputed global leader in the AI Server Clusters market, driven by a powerful confluence of technological innovation, significant venture capital investment, and a mature ecosystem of hyperscalers and AI-native companies. The region is home to industry titans like NVIDIA, Google, Microsoft, AWS, and Meta, whose massive capital expenditure on AI infrastructure, estimated to be in the tens of billions of dollars annually, fuels demand for cutting-edge GPU-based clusters. This leadership is further cemented by a robust startup culture, with firms like OpenAI, Cerebras, and CoreWeave pushing the boundaries of computational scale. The market is characterized by a strong preference for high-performance, energy-efficient clusters to support complex applications in financial services, autonomous vehicle development, and advanced cloud computing services. However, the region also faces challenges, including intense competition for a limited supply of advanced GPUs and increasing scrutiny regarding the immense power consumption and environmental footprint of large-scale data centers.

Asia-Pacific

The Asia-Pacific region represents the fastest-growing and most dynamic market for AI Server Clusters, with China as its primary engine. The Chinese market is propelled by substantial government support as part of national strategic initiatives in AI, leading to the rapid expansion of domestic tech giants like Alibaba, Tencent, Baidu, and Huawei. These companies are deploying vast server clusters to power everything from e-commerce and fintech to smart city and surveillance applications. While cost sensitivity leads to a diverse mix of GPU and custom ASIC/TPU-based solutions, the drive for technological sovereignty is accelerating local innovation. Japan and South Korea are also significant contributors, with their strong automotive and electronics manufacturing sectors investing heavily in AI for industrial automation and R&D. A key regional challenge involves navigating complex international trade policies that can impact the supply chain for critical hardware components.

Europe

The European market for AI Server Clusters is growing steadily, underpinned by a strong industrial base and increasing digitalization across the automotive, manufacturing, and pharmaceutical sectors. Germany, France, and the U.K. are the key markets, with major enterprises investing in clusters to enhance operational efficiency and drive innovation in areas like industrial IoT and personalized medicine. The region’s growth is supported by EU-wide digital strategies and funding programs aimed at boosting AI capabilities and reducing technological dependency. European adoption is notably influenced by stringent data sovereignty regulations, such as GDPR, which drives demand for on-premise and localized cloud clusters. While the market is active, it generally trails behind North America and Asia-Pacific in terms of the sheer scale of deployment, partly due to a more fragmented landscape and less concentrated capital investment from hyperscale providers.

South America

The AI Server Clusters market in South America is in a nascent but promising stage of development. Growth is primarily concentrated in Brazil and Argentina, where the financial services and agricultural technology sectors are beginning to leverage AI for data analytics, risk modeling, and supply chain optimization. The adoption is largely driven by multinational corporations and larger domestic enterprises starting their digital transformation journeys. However, the market’s expansion faces significant headwinds from economic volatility, which constrains large capital expenditures on IT infrastructure, and limited local AI expertise. The reliance on imported technology and cloud services from North American providers is high, presenting both an opportunity for international vendors and a challenge for developing a resilient local ecosystem.

Middle East & Africa

The market in the Middle East & Africa is emerging, with growth hotspots primarily in the Gulf Cooperation Council (GCC) nations, notably the UAE, Saudi Arabia, and Israel. These countries are leveraging sovereign wealth funds to make ambitious investments in AI as a cornerstone of their economic diversification plans away from oil. Initiatives like Saudi Arabia’s NEOM smart city project and the UAE’s national AI strategy are creating demand for high-performance computing infrastructure. Israel’s vibrant tech startup scene, focused on cybersecurity and AI, also contributes to cluster demand. Outside these hubs, adoption is minimal due to infrastructural limitations, funding constraints, and a smaller industrial base. The region’s long-term potential is significant, but progress is incremental and focused on specific, well-funded national projects.

Report Scope

This market research report provides a comprehensive analysis of the global AI Server Clusters market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global AI Server Clusters Market?

-> AI Server Clusters Market was valued at 4964 million in 2024 and is projected to reach US$ 10380 million by 2032, at a CAGR of 11.0% during the forecast period.

Which key companies operate in Global AI Server Clusters Market?

-> Key players include NVIDIA, Google, Microsoft, AWS, Meta, OpenAI, Tesla, Cerebras, Lambda, CoreWeave, HPE, Dell, Oracle, Lenovo, Inspur, Huawei, and Baidu, among others.

What are the key growth drivers?

-> Key growth drivers include increasing adoption of AI and machine learning across industries, rising demand for high-performance computing, expansion of cloud computing services, and significant investments in AI infrastructure by major technology firms.

Which region dominates the market?

-> North America currently holds the largest market share, driven by the United States, while Asia-Pacific is expected to be the fastest-growing region, led by China and its substantial investments in AI technology.

What are the emerging trends?

-> Emerging trends include the development of more energy-efficient AI clusters, integration of advanced cooling technologies, adoption of specialized AI chips (GPUs, TPUs), and the rise of AI-as-a-Service models.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...