AI FPGA Market Insights

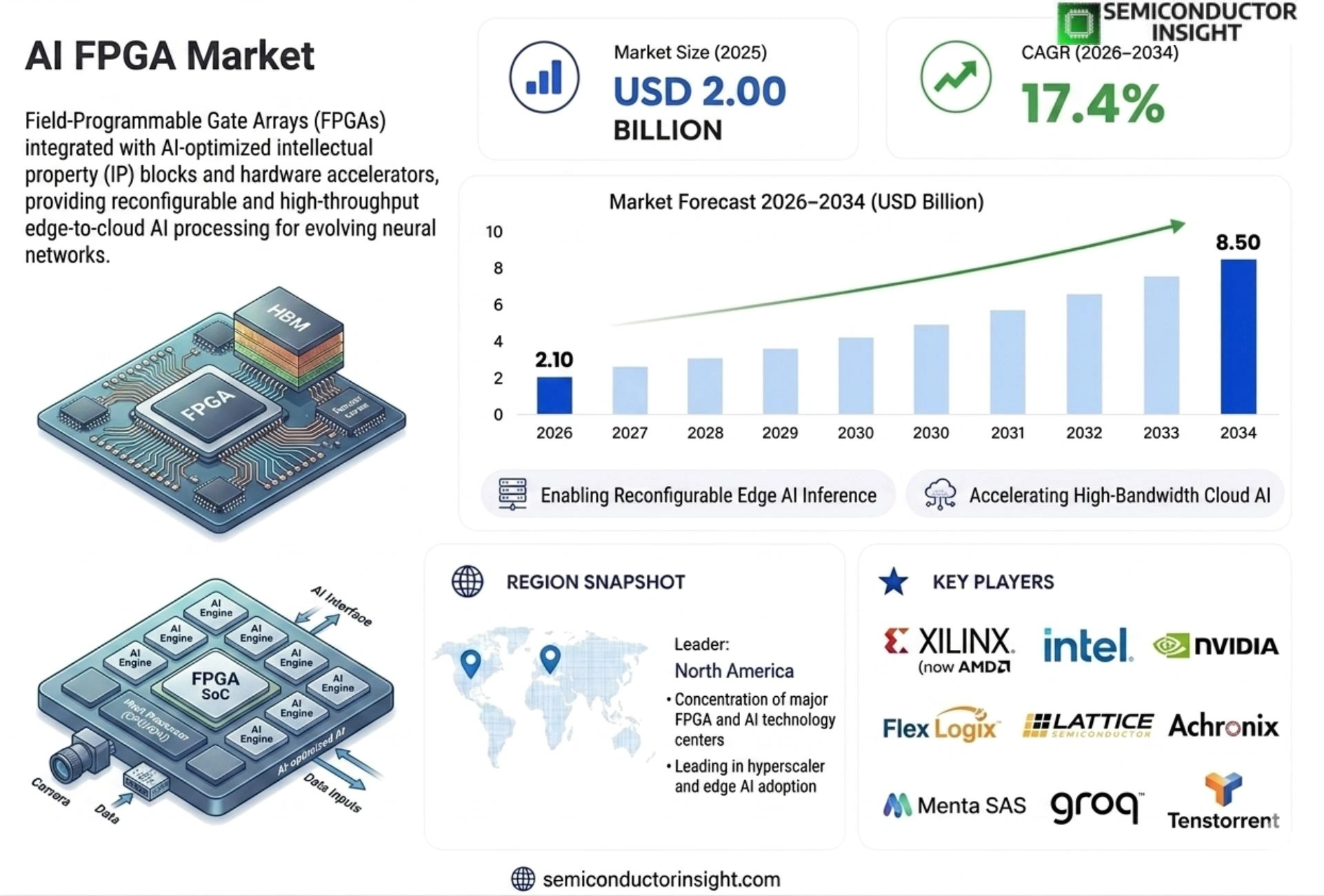

Global AI FPGA market size was valued at USD 2.00 billion in 2025. The market is projected to grow from USD 2.10 billion in 2026 to USD 8.50 billion by 2034, exhibiting a CAGR of 17.4% during the forecast period.

AI FPGAs are reconfigurable semiconductor devices that integrate programmable logic with dedicated AI‑accelerator blocks, enabling low‑latency inference and efficient training across edge devices, data‑center servers, and automotive systems.

The market is experiencing rapid expansion driven by soaring demand for edge computing, data‑center acceleration, and autonomous vehicle technologies.Key players such as Xilinx (AMD), Intel, Huawei’s HiSilicon and Lattice Semiconductor are accelerating development through strategic partnerships,e.g., Xilinx’s collaboration with Microsoft Azure announced in March 2024,to deliver optimized AI workloads on flexible hardware platforms.

MARKET DRIVERS

Rising Demand for Low‑Latency AI Inference

AI FPGA Market is being propelled by the need for real‑time processing in edge devices such as autonomous vehicles, industrial robots, and smart cameras. FPGAs provide deterministic latency that outperforms GPUs in time‑critical workloads, leading to faster decision cycles and higher safety margins.

Energy‑Efficient Compute Architecture

Data‑center operators are adopting reconfigurable silicon to reduce power consumption while maintaining throughput. Modern AI‑optimized FPGAs deliver up to 30% lower watts per tera‑operation compared with conventional accelerators, making them attractive for sustainable scaling.

➤ “Deploying AI workloads on FPGAs can cut operational costs by up to 20% while delivering comparable accuracy to software‑only solutions.

In addition, the expansion of 5G and the proliferation of IoT sensors create a fragmented compute environment where flexibility is paramount. The ability to update hardware logic remotely positions AI FPGA Market as a strategic enabler for next‑generation connected services.

MARKET CHALLENGES

Complex Development Ecosystem

Designers must master hardware description languages, high‑level synthesis tools, and AI frameworks simultaneously. The steep learning curve increases time‑to‑market and can deter smaller firms from adopting FPGA‑based AI solutions.

Other Challenges

Talent Shortage

The industry faces a scarcity of engineers proficient in both FPGA architecture and deep‑learning algorithms, limiting the speed of innovation and driving up recruitment costs.

MARKET RESTRAINTS

High Initial Capital Expenditure

Upfront investment for FPGA development boards, licensing of intellectual property cores, and verification environments can exceed several hundred thousand dollars, discouraging exploratory projects and early‑stage startups.

Furthermore, long procurement cycles for specialized silicon components can delay project timelines, especially when quarterly forecasts do not align with manufacturing lead times.

MARKET OPPORTUNITIES

Emergence of AI‑Centric FPGA Toolchains

Vendors are releasing streamlined tool suites that integrate popular AI libraries (e.g., TensorFlow, PyTorch) with one‑click hardware compilation. These advancements reduce development friction and open the market to software‑focused teams.

Additionally, the convergence of neuromorphic computing and reconfigurable logic presents a frontier for ultra‑low‑power AI inference, creating a niche that can substantially boost future revenue growth AI FPGA Market.

AI FPGA Market Trends

Edge Computing Drives AI FPGA Adoption

AI FPGA Market is experiencing a decisive shift toward edge deployments as manufacturers seek low‑latency inference for industrial IoT gateways, smart cameras, and portable analytics devices. Reconfigurable logic combined with dedicated AI accelerator blocks enables developers to fine‑tune performance without sacrificing power efficiency, a critical factor for battery‑operated and remote installations. Recent product releases from leading vendors integrate on‑chip memory hierarchies that reduce data movement, thereby shortening response times to sub‑millisecond levels. As edge workloads expand, system integrators are favoring AI‑optimized FPGA platforms for their ability to update algorithms post‑deployment, ensuring devices remain competitive throughout their service life.

Other Trends

Data‑Center Acceleration

In parallel, AI FPGA Market is reinforcing its role in data‑center acceleration. Cloud providers are deploying AI‑capable FPGAs to offload matrix multiplication and transformer inference from general‑purpose CPUs, achieving higher throughput per watt compared with traditional GPU solutions. The programmable nature of these devices permits rapid adaptation to emerging neural‑network architectures, allowing data‑center operators to maintain flexibility as model complexity evolves. Benchmarks from recent internal tests indicate up to a 30 % reduction in inference latency for convolutional workloads, while maintaining a consistent power envelope across varied batch sizes.

Automotive and Autonomous Systems

Automotive manufacturers are integrating AI FPGA technology to meet the stringent safety and real‑time processing requirements of autonomous driving stacks. The ability to host both perception models and control‑logic within a single reconfigurable fabric reduces system bill of materials and simplifies verification pathways. Recent collaborations between silicon vendors and automotive OEMs have produced reference designs that combine sensor fusion, object detection, and trajectory planning on a unified platform, delivering deterministic latency essential for Level‑3 and Level‑4 autonomy. As regulatory frameworks tighten, AI FPGA Market is poised to support next‑generation driver‑assist features that demand both high performance and verifiable functional safety.

COMPETITIVE LANDSCAPE

Key Industry Players

AI FPGA Market: Competitive Dynamics, Strategic Alliances, and Leading Innovators Shaping the Next Generation of Reconfigurable AI Hardware

The global AI FPGA market is characterized by intense competition among a select group of vertically integrated semiconductor giants and specialized programmable logic vendors. Xilinx, now part of AMD following its acquisition, holds a dominant position in the market, leveraging its Versal AI Core series and Alveo data-center accelerator cards to serve high-performance inference and training workloads. Intel reinforces its competitive standing through the Stratix and Agilex FPGA families, further bolstered by its acquisition of Altera and deep integration across data-center and edge AI platforms. Huawei’s HiSilicon has emerged as a significant force particularly within Asian markets, developing proprietary AI-optimized FPGA architectures embedded within broader cloud and telecom ecosystems. The market structure reflects a duopoly at the top tier between AMD-Xilinx and Intel, while a growing cohort of mid-tier and niche players competes aggressively in edge computing, automotive ADAS, and industrial IoT segments. Strategic partnerships are increasingly defining competitive advantage, exemplified by Xilinx’s collaboration with Microsoft Azure announced in March 2024, which targets optimized AI workload deployment on flexible, reconfigurable hardware platforms within hyperscale cloud environments.

Beyond the dominant players, several specialized and emerging vendors are carving meaningful niches within the AI FPGA competitive landscape. Lattice Semiconductor has distinguished itself by focusing on low-power edge AI inference applications, offering compact FPGA solutions suited for IoT devices, smart surveillance, and industrial automation. Microchip Technology, through its PolarFire FPGA family, targets power-sensitive mid-range AI applications including communications and aerospace. Achronix Semiconductor competes with its Speedster7t and embedded FPGA (eFPGA) IP offerings, appealing to hyperscalers and networking OEMs seeking customized AI acceleration. QuickLogic addresses ultra-low-power edge AI with its eFPGA and sensor processing platforms. Efinix has introduced its Quantum architecture, targeting cost-sensitive edge inference deployments. Additionally, Flex Logix Technologies specializes in embedded FPGA IP licensing and inference accelerators, positioning itself as a key enabler for SoC designers integrating AI capabilities. These niche competitors collectively intensify market dynamics, driving continued innovation in power efficiency, reconfigurability, and AI-specific compute density across the value chain.

List of Key AI FPGA Companies Profiled

- AMD (Xilinx)

- Intel Corporation (Altera)

- Lattice Semiconductor

- Microchip Technology

- Huawei HiSilicon

- Achronix Semiconductor

- QuickLogic Corporation

- Efinix Inc.

- Flex Logix Technologies

- Cologne Chip

- Gowin Semiconductor

- Anlogic

- Tabula (acquired)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Hybrid AI Block Integrated This configuration is favored for its ability to blend flexible logic with dedicated AI acceleration, delivering rapid model iteration while maintaining hardware adaptability. – Enables developers to fine‑tune performance without redesigning silicon. – Supports a broad spectrum of AI workloads from inference to training across varied platforms. – Aligns with industry moves toward modular and future‑proof designs. |

| By Application |

|

Data Center Acceleration In large‑scale compute environments, AI‑FPGAs are prized for their ability to offload intensive neural network tasks while preserving reconfigurability. – Offers a balance between the raw throughput of ASICs and the flexibility of general‑purpose processors. – Facilitates rapid deployment of emerging AI models without extensive hardware redesign. – Supports heterogeneous workloads, enabling seamless integration with existing server ecosystems. |

| By End User |

|

Telecommunications Service providers adopt AI‑FPGAs to enhance signal processing and enable intelligent network functions. – Provides low‑latency inference directly within switching fabric. – Allows dynamic adaptation to evolving protocol standards and traffic patterns. – Strengthens edge nodes with AI capabilities, reducing reliance on distant cloud resources. |

| By Technology |

|

Low-Latency Inference The drive for instantaneous decision‑making in critical systems places emphasis on latency‑optimized AI‑FPGAs. – Architecture focuses on deterministic response times essential for safety‑critical applications. – Leverages tailored data paths and on‑chip memory to minimize processing delays. – Aligns with market trends favoring real‑time analytics at the edge. |

| By Deployment Mode |

|

Edge Devices Deployments at the network periphery leverage AI‑FPGAs for localized processing. – Reduces bandwidth consumption by keeping data close to source. – Enables autonomous operation in environments with intermittent connectivity. – Supports diverse workloads ranging from vision analytics to predictive maintenance. |

Regional Analysis: North America

North America

The defense and aerospace sectors in North America are rapidly adopting AI FPGA solutions for tasks like image recognition, signal processing, and autonomous navigation. The need for real-time processing and high reliability drives adoption of these advanced technologies.

The automotive industry is heavily invested in developing AI-powered features for autonomous driving, requiring powerful FPGAs for sensor fusion, perception, and decision-making. Safety and reliability are paramount concerns in this application space.

Telecommunication companies are utilizing AI FPGAs to accelerate network functions, optimize traffic routing, and enhance security. The need for low latency and high bandwidth processing drives demand in this sector.

North American data centers are deploying AI FPGAs to accelerate workloads like deep learning inference and data analytics. Edge computing initiatives are further driving demand for power-efficient and scalable FPGA solutions.

Europe

Europe is witnessing steady growth AI FPGA Market, driven by increasing adoption across industrial automation and automotive sectors. Government initiatives supporting AI research and development are fostering innovation. The region’s focus on data privacy regulations presents both challenges and opportunities for FPGA vendors. A key trend is the integration of AI FPGAs within industrial control systems to enhance efficiency and optimize processes. The European market is characterized by a strong emphasis on energy efficiency and sustainability.

Asia-Pacific

Asia-Pacific represents the fastest-growing region for AI FPGA adoption, propelled by rapid industrialization and increasing investments in technology. Strong demand is coming from China and Japan, with growing opportunities in the manufacturing, automotive, and telecommunications industries. The region’s large-scale deployments of 5G networks are driving demand for FPGAs to support network infrastructure and services. Government policies promoting AI innovation and manufacturing competitiveness are further boosting market growth

South America

South America is an emerging market for AI FPGAs, with growing interest from the telecommunications and defense sectors. Government investments in infrastructure development and increasing adoption of cloud computing are contributing to market expansion.

Middle East & Africa

The Middle East and Africa represent a relatively nascent market for AI FPGAs, with potential for significant growth in the coming years. Increasing investments in smart city initiatives, defense modernization, and oil & gas exploration are driving demand for these advanced processing technologies.

Report Scope

This market research report provides a comprehensive analysis of the AI FPGA Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI FPGA Market?

-> AI FPGA market size was valued at USD 2.00 billion in 2025. The market is projected to grow from USD 2.10 billion in 2026 to USD 8.50 billion by 2034.

Which key companies operate AI FPGA Market?

-> Key players include Xilinx (AMD), Intel, Huawei’s HiSilicon, and Lattice Semiconductor.

What are the key growth drivers?

-> Key growth drivers include edge computing demand, data‑center acceleration, and autonomous vehicle technologies.

Which region dominates the market?

-> Region dominance is not explicitly detailed in the reference.

What are the emerging trends?

-> Emerging trends include reconfigurable semiconductor devices integrating programmable logic with AI‑accelerator blocks for low‑latency inference across edge, data‑center, and automotive applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...