AI Data Center Power Management IC Market Insights

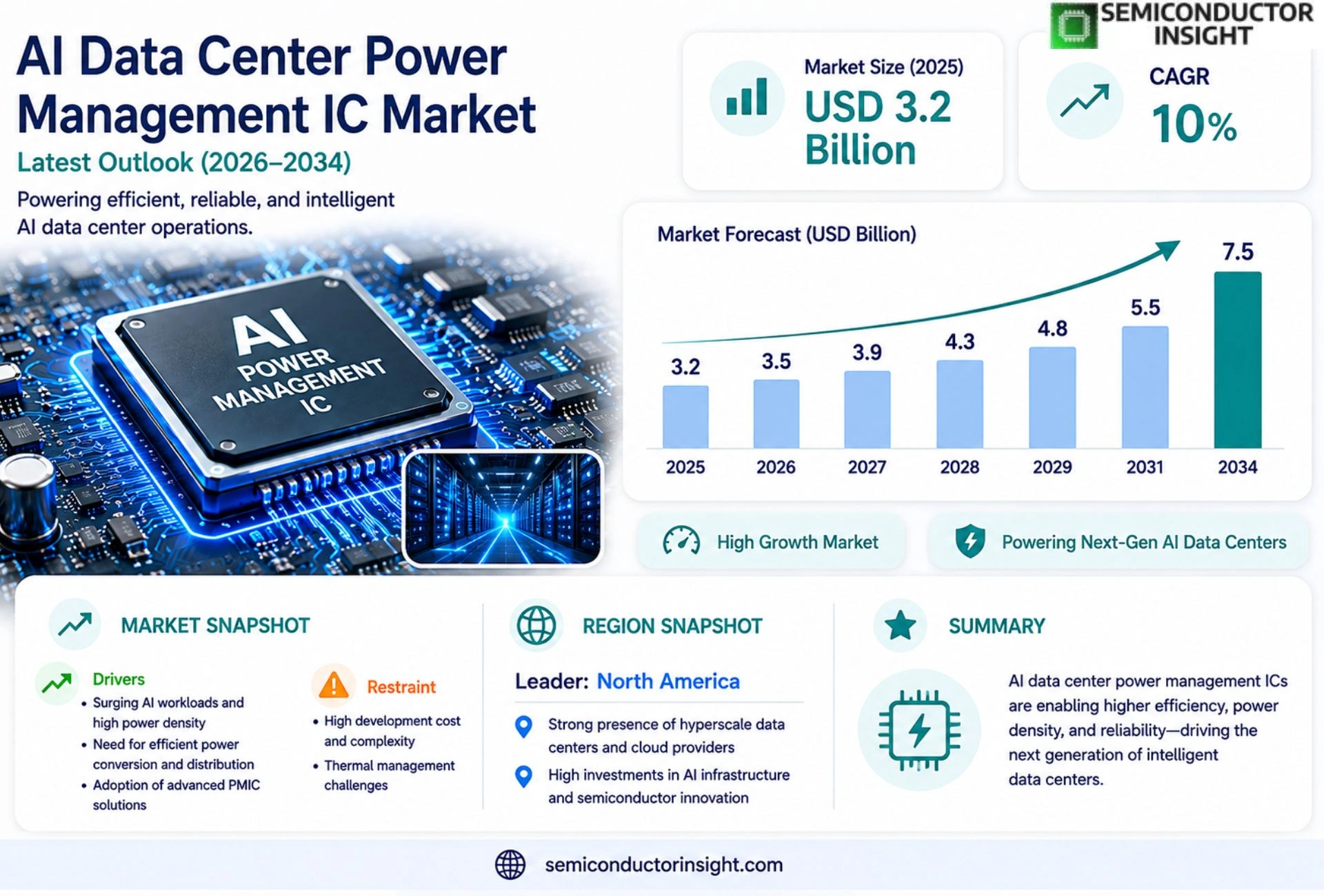

Global AI Data Center Power Management IC market size was valued at USD 3.2 billion in 2025. The market is projected to grow from USD 3.2 billion in 2025 to USD 7.5 billion by 2034, exhibiting a CAGR of 10 % during the forecast period.

AI Data Center Power Management ICs are highly integrated semiconductor solutions that monitor, regulate and optimize electrical power flow within high‑performance computing facilities supporting artificial‑intelligence workloads. These chips incorporate voltage‑conversion modules, digital control loops, telemetry interfaces and safety features designed to improve energy efficiency and reliability of server racks and cooling infrastructure.

The market is experiencing rapid growth because AI‑driven cloud services are expanding exponentially, driving data‑center operators to seek more efficient power architectures. Furthermore, stricter sustainability regulations and rising electricity costs push vendors toward advanced power‑management solutions. Key players such as Texas Instruments, Analog Devices, Infineon Technologies and Maxim Integrated are accelerating product roadmaps and forming strategic alliances,e.g., a June 2024 partnership between Infineon and NVIDIA on next‑generation power modules,to capture emerging demand.

MARKET DRIVERS

Rising AI Workload Demands

The exponential growth of AI inference and training workloads is pressuring data centers to adopt highly efficient power management solutions. AI Data Center Power Management IC Market revenues are expected to surpass $5 billion by 2030, driven by a 15% annual increase in AI‑driven compute capacity.

Energy‑Efficiency Regulations

Stringent governmental energy‑efficiency standards worldwide are compelling operators to replace legacy power converters with advanced integrated circuits. Companies that integrate dynamic voltage scaling and real‑time load monitoring are gaining market share.

➤ “Adoption of smart power ICs can reduce overall data‑center PUE by up to 7%.”

These drivers translate into a robust pipeline of design wins for silicon vendors, with projected annual shipments of AI‑optimized power management ICs increasing from 120 million units in 2024 to over 350 million units by 2030.

MARKET CHALLENGES

Complex Integration Requirements

Designing power management ICs that can operate across heterogeneous AI accelerator architectures adds significant engineering complexity. The need for multi‑phase converters and advanced thermal management raises development costs for OEMs.

Other Challenges

Supply‑Chain Volatility

Global semiconductor shortages and fluctuating component lead times constrain the ability of manufacturers to meet rapid demand spikes, potentially delaying product launches.

MARKET RESTRAINTS

High Capital Expenditure

Upgrading existing data‑center infrastructure to accommodate next‑generation power management ICs requires substantial capital outlays. Many operators prioritize cost‑effective retrofits over wholesale replacements, slowing market penetration.

Additionally, legacy power architectures often lack the firmware interfaces needed for seamless integration of AI‑specific power monitoring, creating a technical lock‑in that restrains adoption.

These financial and technical restraints keep the overall adoption curve flatter than projected, especially in regions with tighter budget constraints.

MARKET OPPORTUNITIES

Edge AI Deployments

The rapid expansion of edge AI workloads,ranging from autonomous vehicles to smart factories,opens a new frontier for power management ICs that deliver high efficiency in compact form factors. Edge installations are projected to account for 22% of total AI Data Center Power Management IC Market revenue by 2028.

Furthermore, the emergence of heterogeneous compute stacks combining GPUs, TPUs, and specialized ASICs creates opportunities for modular IC platforms that can be re‑programmed to support multiple accelerator types, unlocking recurring revenue streams for chip makers.

Investors are also eyeing collaborations between silicon vendors and renewable‑energy providers to integrate on‑board energy‑harvesting capabilities, a niche that could differentiate early entrants in the market.

AI Data Center Power Management IC Market Trends

Integrated Power Control for AI Workloads

AI Data Center Power Management IC Market is being reshaped by highly integrated semiconductor solutions that combine voltage‑conversion modules, digital control loops, telemetry interfaces, and advanced safety features within a single package. These chips continuously monitor power quality, regulate voltage rails, and dynamically adjust conversion efficiency to match fluctuating AI‑driven compute loads. By embedding telemetry, operators gain real‑time visibility into rack‑level consumption, enabling predictive maintenance and tighter thermal management. The result is a measurable uplift in overall energy efficiency and a reduction in downtime for high‑performance servers that support intensive machine‑learning tasks. This integration trend reduces board‑level component count, simplifies system design, and directly addresses the power‑quality challenges of next‑generation AI data centers.

Other Trends

Sustainability‑Driven Design

Stricter sustainability regulations and rising electricity costs are prompting data‑center owners to prioritize power‑management architectures that minimize waste. Within AI Data Center Power Management IC Market, manufacturers are embedding low‑dropout regulators and synchronous buck converters that operate efficiently across a broad load spectrum, thereby lowering standby power draw. Designers are also adopting adaptive control algorithms that shift load between power rails based on real‑time workload forecasts, which helps meet carbon‑reduction targets without compromising performance. The focus on green design not only aligns with corporate ESG goals but also translates into lower operational expenses for large‑scale facilities.

Strategic Alliances and Roadmap Acceleration

Key industry players are accelerating product roadmaps through strategic partnerships that enhance the capabilities of AI Data Center Power Management IC solutions. Notably, a June 2024 collaboration between Infineon Technologies and NVIDIA introduced next‑generation power modules optimized for GPU‑intensive AI inference, showcasing tighter integration between semiconductor performance and AI workload requirements. Parallel efforts by Texas Instruments, Analog Devices, and Maxim Integrated focus on expanding temperature ranges and adding advanced diagnostic interfaces to meet the reliability standards of hyperscale operators. These alliances expedite the delivery of specialized ICs that address emerging power‑density challenges, reinforcing the market’s momentum toward more resilient and efficient AI data‑center infrastructures.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Data Center Power Management IC Market Overview

AI Data Center Power Management IC market is dominated by a handful of large semiconductor firms that offer highly integrated voltage‑conversion and digital‑control platforms specifically engineered for high‑performance computing racks. Texas Instruments, Analog Devices, Infineon Technologies, and NXP Semiconductors each command significant design‑win shares by delivering power‑module families that combine wide input ranges, precise telemetry, and built‑in safety functions required for AI‑intensive workloads. These leaders leverage deep R&D pipelines and strategic alliances,such as Infineon’s 2024 partnership with NVIDIA,to accelerate next‑generation‑module rollouts that improve overall data‑center energy efficiency. Maxim Integrated (now operating under Analog Devices) also contributes differentiated low‑noise regulators that are increasingly adopted in rack‑level power distribution units. Collectively, these companies shape the market structure, set benchmark specifications, and influence pricing dynamics across the 2025‑2034 forecast horizon.

Beyond the primary quadrants, several niche but technically strong players are expanding their footprints in specialized segments of the AI data‑center ecosystem. STMicroelectronics and ON Semiconductor focus on rugged, automotive‑grade power ICs that are being repurposed for edge‑server environments, while Renesas Electronics provides micro‑controller‑centric power‑management solutions that integrate AI inference acceleration. Microchip Technology and Power Integrations target cost‑sensitive mid‑range servers with compact, high‑efficiency converters. Mitsubishi Electric supplies high‑voltage modules for large‑scale cooling systems, and Skyworks offers RF‑optimized power‑management chips for AI‑driven networking fabrics. Broadcom and Samsung Electronics round out the competitive set with system‑level power‑delivery architectures that address emerging heterogeneous compute nodes.

List of Key AI Data Center Power Management IC Companies Profiled

- Texas Instruments

- Analog Devices

- Infineon Technologies

- NXP Semiconductors

- Maxim Integrated

- STMicroelectronics

- ON Semiconductor

- Renesas Electronics

- Microchip Technology

- Power Integrations

- Mitsubishi Electric

- Skyworks Solutions

- Broadcom Inc.

- Samsung Electronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Switching converters drive the market by offering high efficiency and flexible voltage conversion.

|

| By Application |

|

Server power distribution remains the core application, shaping design philosophies across data centers.

|

| By End User |

|

Cloud service providers lead adoption due to relentless demand for AI compute.

|

| By Power Architecture |

|

Integrated power‑and‑telemetry modules are gaining momentum for their holistic approach.

|

| By Sustainability Focus |

|

Energy‑saving designs resonate strongly with operators seeking greener footprints.

|

Regional Analysis: North America

The rapid expansion of cloud computing in North America directly correlates with the need for efficient and reliable power management in data centers. This section explores the specific power requirements of hyperscale cloud deployments and the innovations driving solutions in this area.

North American data centers are increasingly focused on reducing their energy consumption and carbon footprint. This analysis delves into the key energy efficiency initiatives and the role of power management ICs in achieving these goals.

This section examines the latest technological advancements in power management ICs for AI data centers, including advancements in DC-DC converters, power factor correction, and thermal management solutions. The focus is on how these innovations are addressing the challenges posed by next-generation AI workloads.

A review of the current and emerging regulatory landscape impacting power consumption and efficiency in North American data centers, and its implications for AI Data Center Power Management IC Market.

North America

The North American market is characterized by a strong emphasis on high-performance computing and data analytics, creating a fertile ground for the adoption of advanced AI Data Center Power Management ICs. The region’s leading technology companies are actively investing in infrastructure to support AI development and deployment, driving demand for sophisticated power solutions. Furthermore, government initiatives promoting green technology and energy efficiency are further boosting the market. The concentration of major cloud providers and the presence of a robust ecosystem of semiconductor vendors contribute to the region’s dominance. This market anticipates continued strong growth in the coming years, fueled by the expanding AI landscape and the increasing need for efficient power delivery in data centers. Innovations in power electronics and thermal management are key to addressing the challenges posed by increasingly powerful AI processors. The emphasis on reliability and scalability also plays a significant role in shaping market trends within this region.

Europe

Europe represents a significant and growing market for AI Data Center Power Management ICs, although it lags slightly behind North America in terms of overall market size. Key drivers include increasing cloud adoption across European countries, particularly in the UK, Germany, and France, and a growing focus on sustainability and energy efficiency, mandated by stringent European Union regulations like the European Green Deal. The European market is witnessing a shift towards more energy-efficient data center designs and a growing demand for power management solutions that can optimize the performance of AI accelerators. Many European companies are actively investing in research and development to create innovative power management technologies that meet the evolving needs of AI workloads. The focus on data sovereignty is also influencing the location of data centers within Europe, creating localized demand for power management solutions.

Asia-Pacific

Asia-Pacific is poised to become the largest and fastest-growing market for AI Data Center Power Management ICs in the coming years. This growth is primarily driven by the rapid expansion of data centers in China, India, and Southeast Asia, fueled by burgeoning AI adoption across various industries, including e-commerce, finance, and healthcare. Government initiatives supporting digital transformation and the increasing availability of cloud services are key factors contributing to the region’s market growth. The Asia-Pacific market presents both opportunities and challenges, including intense competition from local manufacturers and the need to address concerns related to power infrastructure and environmental sustainability. The demand for power management ICs tailored to the specific power requirements of AI accelerators used in the region is accelerating rapidly. The sheer scale of data center construction in Asia-Pacific guarantees significant long-term growth for AI Data Center Power Management IC Market.

South America

South America is an emerging market for AI Data Center Power Management ICs, with potential for significant growth in the coming years. The increasing adoption of cloud services and the growing demand for data analytics are driving the need for more efficient and reliable power management solutions in the region. The development of data centers in countries like Brazil and Argentina is creating new opportunities for power management IC suppliers. However, the market faces challenges related to infrastructure development, regulatory uncertainty, and economic instability. The focus on cost-effectiveness and energy efficiency is particularly important in the South American market, where operating costs can be a significant concern. Opportunities exist for companies offering energy-efficient power management ICs that can help data centers reduce their operational expenses.

Middle East & Africa

The Middle East & Africa region represents a relatively nascent market for AI Data Center Power Management ICs, but it is expected to experience substantial growth in the near future. The increasing investments in digital infrastructure, particularly in countries like Saudi Arabia, the UAE, and South Africa, are driving the demand for data centers and, consequently, for advanced power management solutions. The region’s focus on smart city initiatives and the adoption of AI-powered services are further fueling market growth. However, challenges related to power availability, climate conditions, and regulatory frameworks need to be addressed to facilitate market development. Opportunities exist for companies offering solutions that can enhance energy efficiency and reliability in the region’s data centers. The long-term outlook for AI Data Center Power Management IC Market in the Middle East & Africa is promising, driven by government initiatives and growing digital adoption.

Report Scope

This market research report provides a comprehensive analysis of the AI Data Center Power Management IC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Data Center Power Management IC Market?

-> AI Data Center Power Management IC market size was valued at USD 3.2 billion in 2025. The market is projected to grow from USD 3.2 billion in 2025 to USD 7.5 billion by 2034.

Which key companies operate in AI Data Center Power Management IC Market?

-> Key players include Texas Instruments, Analog Devices, Infineon Technologies, and Maxim Integrated, among others.

What are the key growth drivers?

-> Key growth drivers include rapid expansion of AI‑driven cloud services, stricter sustainability regulations, and rising electricity costs.

Which region dominates the market?

-> The market is globally distributed with strong adoption across North America, Europe, and Asia‑Pacific, reflecting the worldwide demand for efficient data‑center power solutions.

What are the emerging trends?

-> Emerging trends include integration of advanced voltage‑conversion modules, digital control loops, telemetry interfaces, and enhanced safety features to boost energy efficiency and reliability.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...