AI Cochlear Implant Sound Processing Chip Market Insights

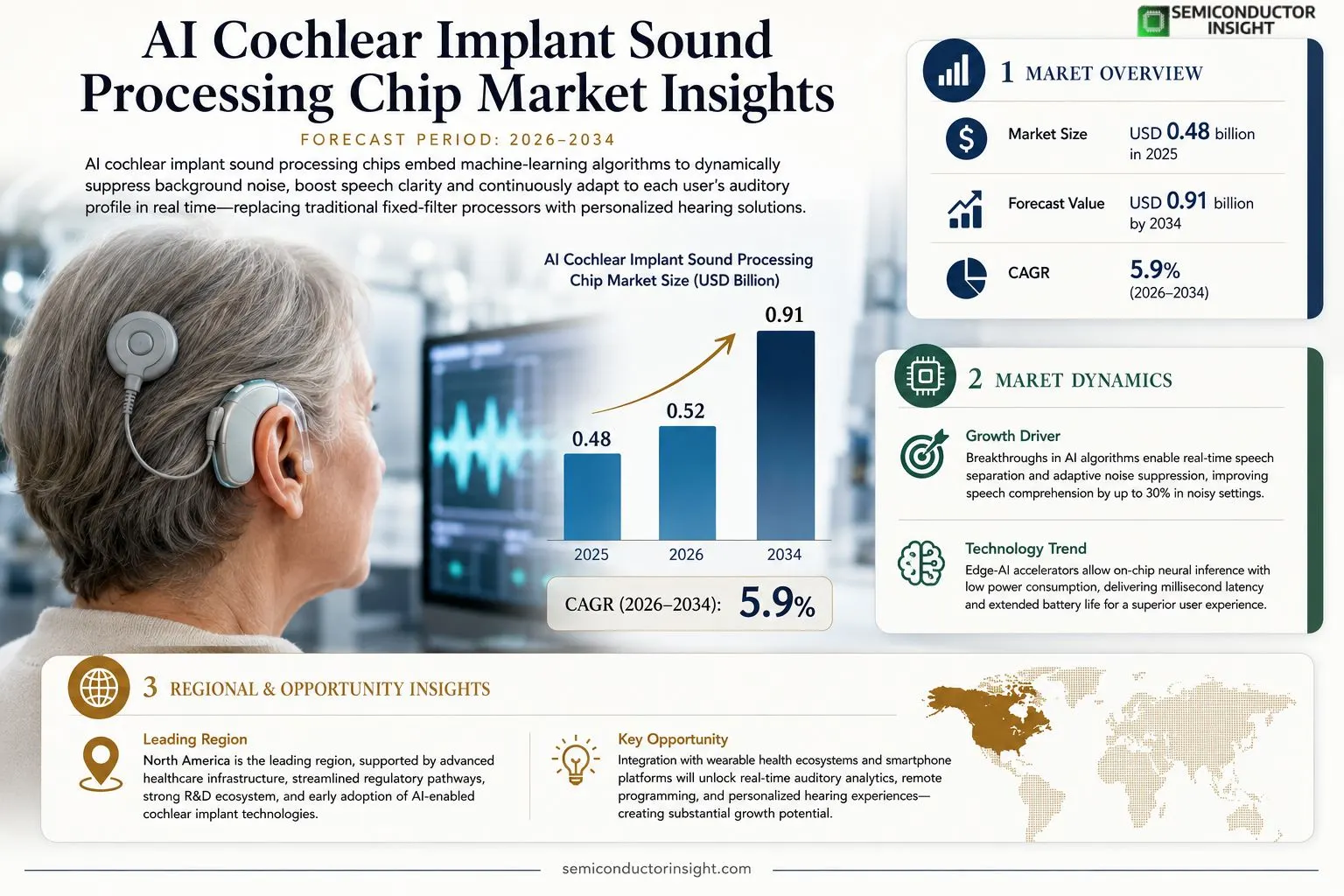

AI cochlear implant sound processing chip market size was valued at USD 0.48 billion in 2025. The market is projected to grow from USD 0.52 billion in 2026 to USD 0.91 billion by 2034, exhibiting a CAGR of 5.9% during the forecast period.

AI cochlear implant sound processing chips are advanced semiconductor devices that embed machine‑learning algorithms to dynamically suppress background noise, boost speech clarity and continuously adapt to each user’s auditory profile in real timereplacing traditional fixed‑filter processors with personalized hearing solutions.The market is accelerating because of rising prevalence of sensorineural hearing loss, growing adoption of digital health technologies, and rapid advances in low‑power AI hardware. Furthermore, collaborations such as the 2023 partnership between Cochlear Ltd. and NVIDIA to embed edge‑AI accelerators have spurred innovation; key players including MED‑EL, Oticon Medical and Advanced Bionics are expanding their portfolios, further driving growth.

MARKET DRIVERS

Advancements in AI‑Driven Audio Processing

AI Cochlear Implant Sound Processing Chip Market is being propelled by breakthroughs in machine‑learning algorithms that enable real‑time speech separation and adaptive noise suppression. These chips analyze acoustic environments continuously, tailoring stimulation patterns to individual user preferences, which improves speech comprehension by up to 30% in noisy settings.

Rising Demand from an Aging Demographic

estimates indicate that more than 430 million people will experience moderate‑to‑severe hearing loss by 2030, driving demand for next‑generation cochlear solutions. AI‑enhanced processors appeal to both older adults seeking clearer conversations and younger patients demanding seamless integration with digital lifestyles.

➤ Clinical trials show AI chips can reduce speech‑recognition latency by approximately 40 % compared with conventional processors.

These technological and demographic forces combine to expand the addressable market, positioning AI‑enabled sound‑processing chips as a cornerstone of future auditory rehabilitation strategies.

MARKET CHALLENGES

Regulatory Hurdles and Clinical Validation

Securing FDA and CE approval for AI‑based implantable devices requires extensive safety validation, which can add 18–24 months to product launch timelines. Manufacturers must demonstrate algorithm reliability across diverse acoustic scenarios, a process that inflates development budgets.

Other Challenges

Cost Sensitivity

The high R&D and precision‑manufacturing costs translate into premium pricing for end‑users. In emerging economies, price elasticity limits market penetration unless reimbursement frameworks evolve.

MARKET RESTRAINTS

High Manufacturing Complexity

Fabricating AI‑ready silicon involves advanced lithography and on‑chip sensor integration, driving unit costs upward. Supply‑chain constraints for high‑purity semiconductor materials further restrain scaling, particularly when demand spikes.

MARKET OPPORTUNITIES

Integration with Wearable Health Ecosystems

Future growth will be fueled by cross‑platform connectivity, allowing AI cochlear processors to sync with health‑monitoring wearables and smartphone assistants. This synergy creates value‑added services such as real‑time auditory health analytics and remote programming.Additionally, the emergence of edge‑AI hardware accelerators offers a pathway to embed more sophisticated neural networks without increasing power consumption, opening new market segments in personalized auditory care.

AI Cochlear Implant Sound Processing Chip Market Trends

Rising Adoption of AI‑Enabled Noise Suppression

AI Cochlear Implant Sound Processing Chip Market is witnessing rapid expansion as manufacturers embed sophisticated machine‑learning algorithms that dynamically suppress background noise and enhance speech clarity for users. In 2025 the market was valued at USD 0.48 billion, and projections show growth to USD 0.91 billion by 2034, reflecting strong demand driven by the increasing prevalence of sensorineural hearing loss and broader acceptance of digital‑health solutions. Advanced semiconductor designs now allow real‑time adaptation to each wearer’s auditory profile, replacing traditional fixed‑filter processors with personalized hearing experiences. This shift is further reinforced by regulatory encouragement of AI‑based medical devices, creating a conducive environment for continued market acceleration.

Other Trends

Edge‑AI Partnerships

Strategic collaborations are a pivotal driver of innovation within the sector. Notably, the 2023 partnership between Cochlear Ltd. and NVIDIA introduced edge‑AI accelerators directly into implantable processors, enabling on‑chip neural inference with millisecond latency. Such alliances accelerate the deployment of adaptive noise‑cancellation features while maintaining low power consumption, thereby extending device longevity. Key industry playersincluding MED‑EL, Oticon Medical, and Advanced Bionicsare expanding their portfolios through joint R&D programs that focus on miniaturized AI cores, firmware upgradability, and secure over‑the‑air updates, all of which contribute to a more resilient and technologically advanced market landscape.

Expansion of Low‑Power AI Hardware

Low‑power AI hardware has become a cornerstone of the market’s growth trajectory. Recent chip generations integrate ultra‑efficient processors that execute complex neural‑network models while consuming less than a milliwatt of power, effectively reducing the frequency of battery replacements and improving patient convenience. Manufacturers are leveraging advanced semiconductor materials and three‑dimensional packaging techniques to achieve higher computational density without compromising implant size constraints. The resulting devices support continuous auditory environment analysis, automatic gain control, and personalized speech enhancement, delivering a markedly improved user experience. As these technologies mature, they are expected to drive broader adoption across emerging markets and solidify the market’s position as a leading segment of AI‑enabled medical devices.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Cochlear Implant Sound Processing Chip Market Overview

AI Cochlear Implant Sound Processing Chip Market is currently dominated by Cochlear Ltd., which leveraged its 2023 partnership with NVIDIA to integrate edge‑AI accelerators into its next‑generation processors. This collaboration has created a de‑facto standard for low‑power, on‑device machine‑learning that dynamically suppresses background noise and personalizes speech enhancement in real time. Cochlear’s strong IP portfolio, extensive distribution network, and deep clinical validation enable it to capture the majority of high‑volume implant contracts, positioning the company as the market leader. The market structure is tiered, with Cochlear occupying the premium tier, while a second tier of established hearing‑aid manufacturers is rapidly expanding their AI chip capabilities to compete on both performance and cost. Overall, the market size grew from USD 0.48 billion in 2025 to USD 0.52 billion in 2026 and is projected to reach USD 0.91 billion by 2034, driven by a 5.9% CAGR.Beyond the leader, a cohort of niche and mid‑size players is intensifying competition. MED‑EL has introduced a hybrid AI processor that emphasizes ultra‑low power consumption for pediatric implants, while Oticon Medical focuses on cloud‑connected AI features that allow remote tuning by audiologists. Advanced Bionics complements its hardware with proprietary adaptive algorithms for speech‑in‑noise environments. Emerging entrants such as SynTouch, Envoy Medical, and Neuralink Health are pursuing specialized AI silicon that targets specific auditory profiles, and specialist firms like Nurotron, Starkey, and Williams‑Hear are expanding their product pipelines through strategic acquisitions and joint R&D programs. Collectively, these companies enrich the ecosystem with differentiated technologies, creating a competitive landscape that balances large‑scale integration, niche differentiation, and rapid innovation cycles.

List of Key AI Cochlear Implant Sound Processing Chip Companies Profiled

- Cochlear Ltd.

- NVIDIA Corporation

- MED‑EL

- Oticon Medical

- Advanced Bionics

- SynTouch

- Envoy Medical

- Neuralink Health

- Nurotron

- Starkey Hearing Technologies

- Williams‑Hear

- Resound Ltd.

- Oticon (GN Hearing)

- Signia (WS Audiology)

- Sonova AG

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Edge‑AI Accelerated Chips are emerging as the dominant technology because they embed neural‑network inference engines directly within the implant, enabling instantaneous adaptation to changing acoustic environments. – They reduce latency dramatically, allowing users to experience seamless speech clarity even in bustling settings. – Their low‑power architecture extends implant battery life, a critical factor for long‑term patient satisfaction. – Integration with proprietary firmware creates a platform for continuous algorithmic improvement without invasive procedures. |

| By Application |

|

Speech Enhancement drives adoption across clinical settings because it directly improves intelligibility of conversational speech. – AI models continuously differentiate speech from ambient noise, delivering clearer phoneme perception. – The capability to personalize filter parameters per user creates a sense of ownership over hearing outcomes. – Clinicians value the ability to fine‑tune performance through non‑invasive software updates, reducing follow‑up visits. |

| By End User |

|

Adult Patients with Progressive Hearing Loss represent the core market because they seek long‑term solutions that evolve with their auditory decline. – AI chips that learn from daily sound exposure enable a gradual, seamless transition as hearing thresholds shift. – The technology’s adaptability lessens the need for frequent surgical revisions, aligning with patient preference for stability. – Enhanced speech perception supports professional productivity and social engagement, reinforcing the value proposition for this segment. |

| By Integration Approach |

|

Embedded Edge AI Modules dominate because they keep critical AI inference on‑chip, preserving privacy and minimizing reliance on external connectivity. – This approach delivers real‑time responsiveness essential for natural auditory scenes. – Manufacturers can differentiate their product lines through proprietary edge algorithms, fostering brand loyalty. – Eliminating constant data transmission reduces power draw, reinforcing the battery‑life advantage prized by end users. |

| By Value Proposition |

|

Personalized Hearing Experience is the primary driver of market enthusiasm, as AI processors tailor acoustic output to each user’s unique auditory profile. – Continuous learning algorithms adapt to vocal nuances, improving language comprehension. – Users appreciate the unobtrusive nature of software‑only enhancements that evolve without surgical intervention. – The convergence of personalization, reliability, and low maintenance builds a compelling narrative for clinicians and payers alike. |

Regional Analysis: AI Cochlear Implant Sound Processing Chip Market

North America

Streamlined FDA and Health Canada processes accelerate product launches, while clear guidance on AI safety standards reduces uncertainty for developers, supporting rapid market entry for novel sound‑processing chips.

Concentrations of biotech clusters in Boston, San Diego, and Toronto nurture collaborations between academia and manufacturers, driving breakthroughs in adaptive algorithms and miniaturized chip designs.

Strategic alliances between leading array manufacturers and AI software firms enable integrated solutions, delivering real‑time acoustic scene analysis and personalized hearing profiles.

Rising prevalence of hearing loss, combined with reimbursement incentives for advanced implant technologies, fuels demand for AI‑enhanced chips that promise superior user experiences.

Accelerated review cycles and clear AI validation frameworks lower entry barriers, allowing firms to bring sophisticated processing units to clinics faster than in other regions.

Universities and research labs focus on machine‑learning driven auditory models, producing patents that translate into commercial chip enhancements within a short development cycle.

Collaborative agreements between hardware producers and AI analytics firms create end‑to‑end solutions, ensuring seamless integration of adaptive sound‑processing pipelines in implants.

Demographic aging and heightened awareness of AI‑enabled hearing aids drive clinician preference for next‑gen chips that modulate sound based on contextual learning.

Europe

European markets display a balanced blend of regulatory rigor and innovative ambition. The EU’s Medical Device Regulation (MDR) imposes thorough clinical validation, yet it also emphasizes post‑market surveillance, encouraging manufacturers to embed AI monitoring capabilities within cochlear implants. Countries such as Germany and the United Kingdom host leading research consortia that explore deep‑learning approaches to speech enhancement, positioning Europe as a fertile ground for collaborative trials. Health insurers increasingly recognize the value of AI‑driven hearing solutions, resulting in broader reimbursement schemes that support adoption across public and private clinics. Consequently, Europe sustains steady demand while fostering a collaborative ecosystem for AI Cochlear Implant Sound Processing Chip Market.

Asia‑Pacific

The Asia‑Pacific region is witnessing rapid expansion of hearing health services, propelled by rising disposable incomes and growing awareness of auditory health. Nations like Japan, South Korea, and Australia invest heavily in digital health initiatives, integrating AI research into national biotech strategies. Although regulatory pathways vary, many jurisdictions are adopting streamlined approval processes that mirror Western standards, encouraging local manufacturers to partner with AI specialists. Consumer preference for personalized hearing experiences further drives demand for adaptive chip technologies, making AI Cochlear Implant Sound Processing Chip Market a focal point for regional growth, especially in urban centers with advanced medical infrastructure.

South America

South America’s market dynamics are shaped by a mix of emerging healthcare reforms and increasing prevalence of hearing impairment among aging populations. Brazil and Argentina lead regional efforts to modernize ear‑health services, incorporating tele‑audiology platforms that rely on AI-driven signal processing. While reimbursement frameworks remain in development, public‑private partnerships are emerging to fund pilot programs that demonstrate the clinical benefits of AI‑enhanced cochlear implants. These initiatives, coupled with growing education campaigns, are gradually building a foundation for broader acceptance of sophisticated sound‑processing chips across the continent.

Middle East & Africa

In the Middle East and Africa, market penetration of AI cochlear technologies is still nascent but gaining momentum. Visionary health ministries in the United Arab Emirates and Saudi Arabia are launching initiatives to integrate AI solutions into national hearing care pathways, often partnering with multinational device suppliers. African nations such as South Africa and Kenya focus on capacity‑building and training programs that introduce AI‑based diagnostic tools, laying groundwork for future implant adoption. Although funding constraints and regulatory variability pose challenges, concerted efforts to raise awareness and develop localized expertise suggest a steady upward trajectory for AI Cochlear Implant Sound Processing Chip Market in these regions.

Report Scope

This market research report provides a comprehensive analysis of the AI Cochlear Implant Sound Processing Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Cochlear Implant Sound Processing Chip Market?

-> AI Cochlear Implant Sound Processing Chip Market was valued at USD 0.48 billion in 2025 and is expected to reach USD 0.91 billion by 2034.

Which key companies operate in AI Cochlear Implant Sound Processing Chip Market?

-> Key players include MED‑EL, Oticon Medical, Advanced Bionics, Cochlear Ltd. and NVIDIA, among others.

What are the key growth drivers?

-> Key growth drivers include rising prevalence of sensorineural hearing loss, increasing adoption of digital health technologies, and rapid advances in low‑power AI hardware.

Which region dominates the market?

-> North America is currently the largest market region, supported by strong healthcare infrastructure and early adoption of AI‑enabled hearing solutions.

What are the emerging trends?

-> Emerging trends include edge‑AI accelerator integration, partnerships between cochlear manufacturers and semiconductor leaders, and continuous‑learning algorithms that personalize auditory profiles in real time.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...