AI Accelerator Card Module Market Insights

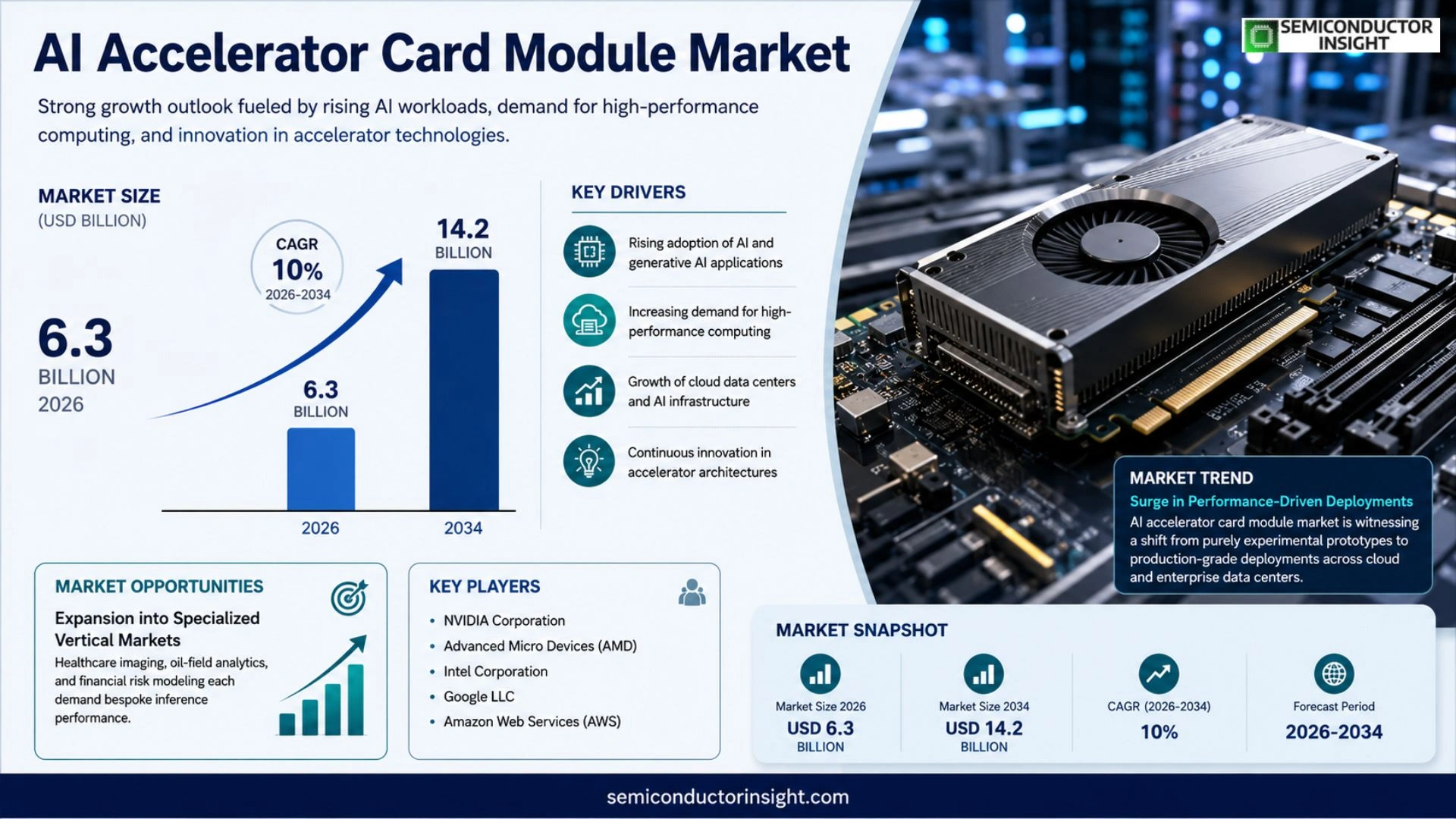

Global AI accelerator card module market size was valued at USD 5.8 billion in 2025. The market is forecasted to increase from USD 6.3 billion in 2026 to USD 14.2 billion by 2034, exhibiting a CAGR of approximately 10 % during the forecast period.

AI accelerator card modules are high‑performance add‑on boards that integrate specialized processing units,such as GPUs, TPUs, or dedicated inference chips,into server or workstation architectures to accelerate machine‑learning workloads. These modules typically combine dense memory stacks, high‑bandwidth interconnects, and optimized firmware that enable rapid matrix multiplications and tensor operations essential for deep‑learning models.

The market gains momentum because enterprises are scaling generative‑AI services, while hyperscale cloud providers expand capacity for training large language models. Recent product releases,including Nvidia’s H100 GPU accelerator announced late 2023 and AMD’s MI300X module launched early 2024,have pushed performance per watt higher than ever before, prompting data‑center operators to upgrade existing infrastructure sooner than planned. Meanwhile, collaborations such as Microsoft’s partnership with Nvidia for Azure AI supercomputing clusters illustrate how ecosystem alliances accelerate adoption across industries.

MARKET DRIVERS

Performance Demands from Edge AI Deployments

The surge in real‑time analytics for autonomous vehicles, video surveillance, and industrial robotics forces OEMs to seek compute solutions that can sustain high throughput with minimal latency. AI Accelerator Card Module Market players that deliver low‑power, high‑density designs are witnessing an influx of design wins as system integrators prioritize on‑board inference capability over traditional CPU clusters.

Data Center Refresh Cycles Accelerate

Enterprises are replacing aging GPU farms with purpose‑built accelerator cards that align with emerging transformer models. The shift reduces rack footprint and power draw, directly influencing total cost of ownership calculations. Vendors that bundle optimized software stacks with their hardware are capturing a larger share of the upgrade budget.

➤ Strategic partnerships between silicon fables and AI software firms are reshaping the value chain, creating faster time‑to‑market for next‑generation modules.

Regulatory pressure on energy consumption in large‑scale data facilities is another catalyst. Companies adopting efficient accelerator cards can demonstrate compliance while positioning themselves as environmentally responsible, a factor increasingly considered by investors.

MARKET CHALLENGES

Supply‑Chain Volatility for Advanced Packaging

Modern AI accelerator cards rely on 3D‑IC and silicon‑interposer technologies that are still limited to a handful of specialized fabs. Unexpected capacity constraints translate into longer lead times, forcing OEMs to hold higher inventory buffers and eroding margins.

Other Challenges

Thermal Management Complexity

The integration of densely packed compute cores raises cooling requirements beyond conventional air solutions. Designing liquid‑cool or immersion systems adds to system cost and introduces new reliability considerations that can deter early adoption.

MARKET RESTRAINTS

High Capital Expenditure for Custom ASIC Development

Developing a bespoke accelerator card involves multi‑year R&D cycles, mask set expenses, and extensive validation. Smaller players often lack the financial bandwidth to sustain such programs, limiting the competitive pool to a few well‑capitalized firms.

Fragmented Standards Landscape

The absence of universally accepted programming models and interconnect specifications creates integration friction. System architects must invest additional engineering effort to ensure compatibility across different hardware generations, which can slow deployment timelines.

Finally, geopolitical tensions affecting semiconductor export controls introduce uncertainty for customers operating across borders. Restrictive policies may force redesigns or relocation of production, adding strategic risk to long‑term investment decisions.

MARKET OPPORTUNITIES

Expansion into Specialized Vertical Markets

Healthcare imaging, oil‑field analytics, and financial risk modeling each demand bespoke inference performance. Tailoring accelerator card modules to the computational patterns of these niches opens revenue streams where generic GPUs are less cost‑effective.

Software‑Driven Differentiation

Companies that bundle compiler optimizations, model quantization tools, and managed services with their hardware can command premium pricing. The added value reduces integration effort for end‑users and creates recurring income through support contracts.

Adoption of Open‑Source Hardware Ecosystems

Initiatives that promote reusable IP blocks and open verification environments lower entry barriers for new entrants. Participants that leverage these ecosystems can accelerate product launches, thereby capturing market share before legacy vendors adapt.

AI Accelerator Card Module Market Trends

Surge in Performance‑Driven Deployments

AI accelerator card module Market is witnessing a shift from purely experimental prototypes to production‑grade deployments across cloud and enterprise data centers. Vendors have delivered boards that couple next‑generation GPUs or tensor‑processing chips with stacked high‑bandwidth memory, allowing matrix multiplications to complete in a fraction of the time required by traditional servers. This efficiency gain aligns with the rapid rollout of generative‑AI services, where model training cycles must be compressed to meet service‑level expectations. Hyperscale operators, in particular, are replacing legacy accelerators with new modules that promise double the throughput per watt, prompting a hardware refresh schedule that is ahead of the original capital‑expenditure plan. The resulting demand surge has lifted revenue from $5.8 billion in 2025 to an estimated $6.3 billion in 2026, with a trajectory that foresees $14.2 billion by 2034.

Other Trends

Supply‑Chain Realignment

Supply‑chain realignment has become a decisive factor for manufacturers seeking to sustain the accelerated rollout. The integration of dense memory stacks and silicon interposers has raised the bill of materials, while global semiconductor allocations remain tight. To mitigate bottlenecks, leading module makers have entered long‑term agreements with memory suppliers and diversified their packaging partners across Asia and Europe. These measures have shortened lead times from three months to roughly six weeks for high‑density configurations, enabling data‑center operators to meet quarterly upgrade targets without incurring excess inventory costs. The strategic focus on component resilience also reduces the risk of price volatility that could otherwise erode the cost advantage of newer modules.

Ecosystem Partnerships Accelerate Adoption

Strategic ecosystem partnerships are reshaping how AI accelerator card module Market scales across industry verticals. Microsoft’s collaboration with Nvidia to embed H100‑based cards into Azure AI supercomputing clusters illustrates a model where software stacks, licensing, and hardware are co‑engineered to deliver turnkey solutions. AMD’s early‑2024 launch of the MI300X module, coupled with joint go‑to‑market programs with hyperscale providers, creates a competitive counterbalance that pressures pricing while spurring innovation. For end users, these alliances translate into faster access to optimized libraries and firmware updates, shortening the time from purchase to production. Consequently, operators can extract higher utilization rates, improve return on infrastructure spend, and justify further investment in AI‑centric workloads such as real‑time video analytics and autonomous decision engines.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive forces shaping AI accelerator card module ecosystem

NVIDIA continues to dominate the high‑performance card segment, leveraging the H100 GPU accelerator to set a new benchmark for throughput and energy efficiency. The company’s extensive software stack, including CUDA and cuDNN, creates a lock‑in effect for enterprises that have standardized on its development tools. This advantage translates into a de‑facto tier‑one position where data‑center operators prioritize NVIDIA‑based modules when expanding capacity for large‑language‑model training. Intel’s acquisition of Habana Labs has broadened its portfolio, offering Gaudi inference cards that compete on cost per operation while integrating tightly with the company’s broader Xeon ecosystem. AMD’s MI300X module, launched in early 2024, pushes the performance envelope in hybrid CPU‑GPU configurations, appealing to hyperscalers seeking flexible scaling. The concentration of R&D in a handful of firms forces smaller vendors to differentiate through niche architectures or specialized software, fostering a fragmented but innovative second tier.

Beyond the dominant trio, a constellation of challengers is reshaping specific market niches. Graphcore’s IPU cards excel in fine‑grained parallelism, attracting research labs focused on graph‑based neural networks. Tenstorrent and Groq deliver low‑latency inference solutions that resonate with edge‑computing deployments and real‑time analytics. Cerebras’s massive wafer‑scale engine provides an alternative for ultra‑large models, while Lambda Labs offers turnkey server bundles that lower entry barriers for AI startups. Asian manufacturers such as Cambricon and Samsung are expanding their presence through collaborations with OEMs, emphasizing integration with custom silicon in consumer devices. These players collectively increase competitive pressure, prompting incumbents to accelerate roadmap timelines and broaden ecosystem support to retain market share.

List of Key AI Accelerator Card Module Companies Profiled

- NVIDIA Corporation

- Advanced Micro Devices (AMD)

- Intel Corporation

- Graphcore Ltd.

- Qualcomm Incorporated

- Tenstorrent Inc.

- Groq Inc.

- Cerebras Systems

- Lambda Labs

- Cambricon Technologies

- Samsung Electronics

- Habana Labs (Intel)

- Mythic AI

- Xilinx Inc.

- Alibaba Cloud (ET) AI Chip

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

GPU‑Based Cards

|

| By Application |

|

Model Training

|

| By End User |

|

Cloud Service Providers

|

| By Architecture |

|

GPU‑Centric Architecture

|

| By Deployment Model |

|

Hybrid Edge Installations

|

Regional Analysis: AI Accelerator Card Module Market

North America

Recent legislative measures incentivize on‑shoring of semiconductor assets, granting tax credits to facilities that produce AI‑optimized modules. This policy thrust lowers the effective cost of scaling production lines, encouraging manufacturers to expand capacity without exposing supply chains to geopolitical friction.

Universities in the region churn out graduates versed in high‑performance computing and machine‑learning hardware, feeding a talent pipeline that fuels both design innovation and rapid prototyping. Collaborative research programs between academia and industry accelerate the translation of theoretical advances into market‑ready modules.

The concentration of advanced packaging facilities inland mitigates risks associated with overseas logistics. Firms leverage these domestic capabilities to shorten lead times for module assembly, delivering more predictable timelines to customers.

Cloud service providers and hyperscale data centers prioritize low‑power, high‑throughput modules to sustain AI model training at scale. Their procurement cycles now favor vendors that can guarantee a steady stream of performance‑tuned cards, prompting suppliers to tighten integration with software stacks.

Europe

European markets are distinguished by an early focus on regulatory compliance and sustainability. Manufacturers embed energy‑efficiency metrics into module specifications to satisfy stringent EU directives, creating a niche for low‑power designs that still deliver high compute density. Collaborative consortia linking hardware firms with AI research institutes accelerate standardization of interface protocols, which eases integration for enterprise buyers across sectors such as automotive and fintech. While capital deployment lags behind North America, steady public funding for green semiconductor initiatives sustains a pipeline of environmentally conscious products that appeal to ESG‑aware customers.

Asia‑Pacific

Asia‑Pacific exhibits a dynamic blend of large‑scale manufacturing capability and rapidly evolving AI application demand. Nations with mature foundry ecosystems leverage cost‑advantageous wafer production to supply volume‑oriented modules for consumer electronics and smart‑city deployments. Concurrently, rapid digital transformation in emerging economies fuels demand for edge‑focused accelerator cards that can process data locally, reducing bandwidth strain. The region’s competitive pricing pressure encourages vendors to optimize design‑for‑manufacturability, resulting in modules that balance performance with affordability.

South America

In South America, market momentum is driven by growing investments in cloud infrastructure and a surge in AI‑related startups. Regional data‑center operators seek modular solutions that can be retrofitted into existing racks, allowing incremental capacity upgrades without extensive capital outlay. Governments are beginning to outline strategic roadmaps that highlight AI hardware as a catalyst for economic diversification, prompting local firms to explore partnerships with global module suppliers to accelerate technology transfer.

Middle East & Africa

The Middle East & Africa region is at a nascent stage, yet strategic initiatives are shaping its trajectory. Sovereign wealth funds allocate capital toward technology parks that host AI accelerator research hubs, aiming to attract foreign expertise. Telecommunications providers, in particular, experiment with edge‑deployed modules to support low‑latency services in remote locales. Although overall market size remains modest, the combination of visionary fiscal policies and a willingness to adopt pioneering hardware suggests a fertile ground for early entrants seeking market share.

Report Scope

This market research report provides a comprehensive analysis of the AI Accelerator Card Module Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Accelerator Card Module Market?

-> AI accelerator card module market is forecasted to increase from USD 6.3 billion in 2026 to USD 14.2 billion by 2034, exhibiting a CAGR of approximately 10 %

Which key companies operate in AI Accelerator Card Module Market?

-> Key players include NVIDIA Corp., AMD Inc., Intel Corp., Xilinx Inc., Qualcomm Technologies, and Graphcore Ltd.

What are the key growth drivers?

-> Key growth drivers include rapid adoption of generative AI services, expanding data‑center capacity for large‑scale model training, and increasing demand for high‑performance inference at the edge.

Which region dominates the market?

-> North America remains the dominant market, while Asia‑Pacific is the fastest‑growing region.

What are the emerging trends?

-> Emerging trends include chiplet‑based accelerator architectures, PCIe 5.0/CCIX interconnect adoption, integration of AI accelerators in edge devices, and the rise of AI‑optimized software stacks.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...