AI Accelerator Advanced Packaging Market Insights

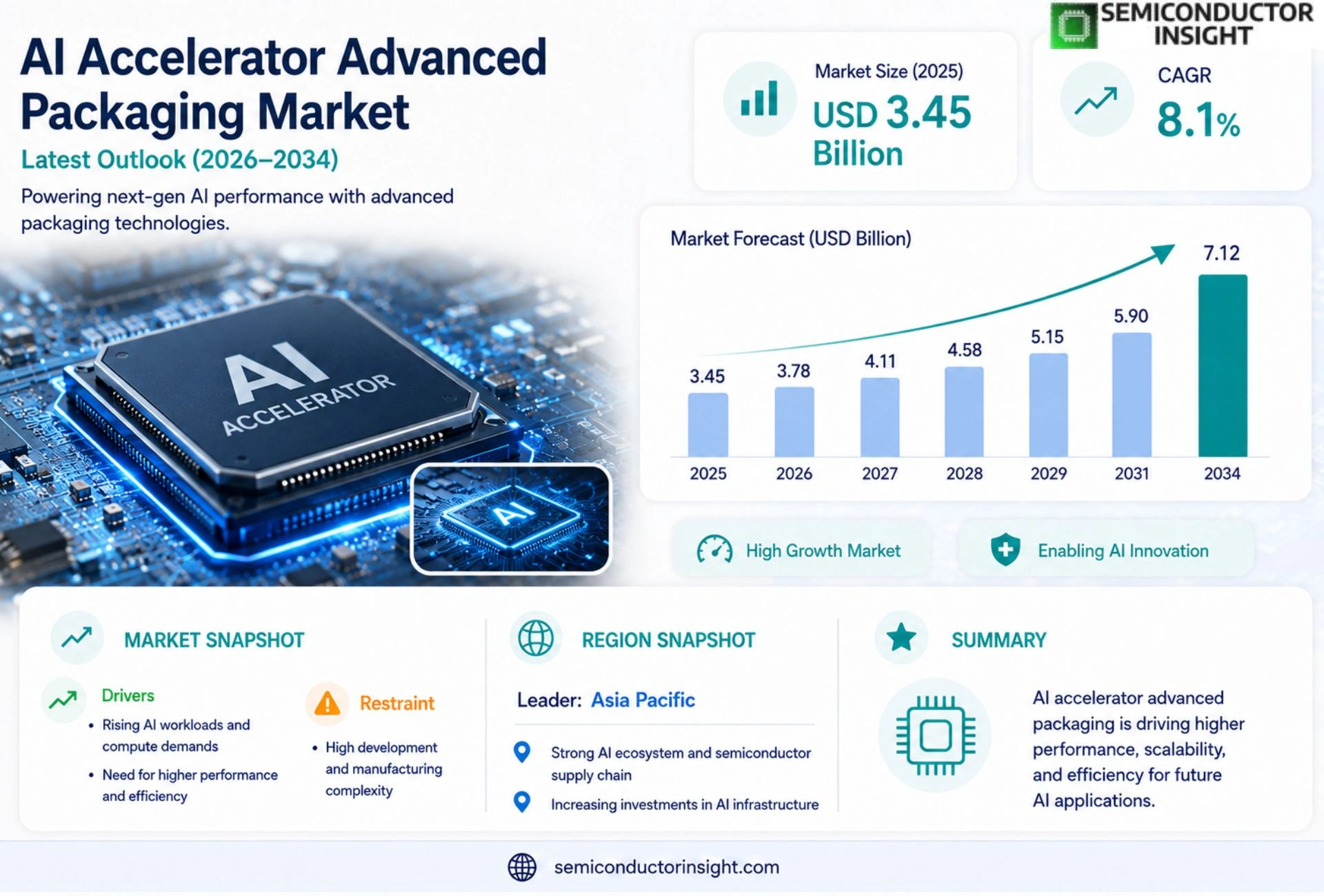

Global AI accelerator advanced packaging market size was valued at USD 3.45 billion in 2025. The market is projected to grow from USD 3.78 billion in 2026 to USD 7.12 billion by 2034, exhibiting a CAGR of 8.1% during the forecast period.

AI accelerator advanced packaging encompasses specialized semiconductor integration techniques,such as fan‑out wafer‑level packaging (FOWLP), chip‑on‑wafer (CoW), and heterogeneous three‑dimensional (3D) stacking,designed to deliver higher bandwidth, lower latency, and superior power efficiency for artificial‑intelligence workloads.

The market is experiencing rapid expansion because AI compute demand across data centers, edge devices, and autonomous systems is soaring. However, supply‑chain constraints and high R&D costs pose challenges. Furthermore, strategic collaborations among leading foundries like TSMC, Samsung Electronics, and Intel Corp., together with emerging packaging innovators, are accelerating adoption of these advanced solutions.

MARKET DRIVERS

Increasing Demand for High‑Performance AI Compute

Enterprises are expanding AI workloads that require sub‑nanometer performance, prompting semiconductor manufacturers to adopt advanced packaging solutions. The need for higher bandwidth and lower latency directly drives the adoption of AI accelerator advanced packaging.

Shift Toward Heterogeneous Integration

Combining logic, memory, and specialized AI cores in a single package improves energy efficiency and reduces form factor. This trend supports the scalable deployment of AI accelerators across data centers and edge devices.

➤ Advanced interposers and wafer‑level packaging enable multi‑chip modules that meet the compute density demanded by modern AI models.

Regulatory incentives for AI‑driven innovation in cloud infrastructure further accelerate investment in sophisticated packaging technologies.

MARKET CHALLENGES

Escalating Cost Structures

The capital intensity of developing and qualifying advanced packaging processes can limit participation to well‑funded players, creating a barrier for smaller innovators.

Other Challenges

Supply Chain Complexity

Coordinating multiple foundry steps, material suppliers, and testing facilities adds logistical risk, potentially delaying product launches.

Design verification cycles are lengthening as engineers strive to ensure reliability under high‑power AI workloads, further increasing time‑to‑market.

MARKET RESTRAINTS

Limited Availability of Specialized Materials

Advanced substrates and high‑k dielectrics required for AI accelerators are produced in limited volumes, constraining large‑scale rollout.

Thermal management solutions that can dissipate the heat generated by densely packed AI cores remain a technical bottleneck, restraining broader adoption.

Regulatory scrutiny over power consumption in data centers may impose stricter efficiency standards, affecting design choices for packaging.

MARKET OPPORTUNITIES

Emerging Edge AI Applications

Growth in autonomous vehicles, smart sensors, and AR/VR creates a demand for compact, low‑latency AI accelerator packages that can operate in constrained environments.

Collaborative ecosystems between fabless designers and advanced packaging providers enable co‑innovation, accelerating time‑to‑market for next‑generation AI solutions.

Investment in silicon photonics and 3D‑stacked memory offers a pathway to overcome current bandwidth limitations, opening new market segments for AI accelerator advanced packaging.

AI Accelerator Advanced Packaging Market Trends

Rising Demand for AI Compute Power

AI Accelerator Advanced Packaging Market is witnessing a pronounced acceleration as AI workloads intensify across data centers, edge devices, and autonomous platforms. Specialized integration methods such as fan‑out wafer‑level packaging (FOWLP), chip‑on‑wafer (CoW), and heterogeneous three‑dimensional (3D) stacking are increasingly adopted to satisfy the need for higher bandwidth, lower latency, and superior power efficiency. These techniques enable tighter interconnects and reduced signal loss, directly translating into faster inference processing for machine‑learning models. As enterprise AI deployments scale, designers are turning to these packaging solutions to balance performance targets with thermal management constraints, thereby creating a robust pipeline of new products that reinforce market momentum. Manufacturers are also integrating wide‑bandgap semiconductor materials and leveraging system‑in‑package (SiP) architectures to further boost compute density. Energy‑efficiency regulations encourage low‑power packaging, driving innovation in thermal interface materials and reinforcing the long‑term growth outlook.

Other Trends

Supply‑Chain Constraints

Supply‑chain constraints are emerging as a pivotal challenge for AI Accelerator Advanced Packaging Market. Tight component availability, especially for high‑purity silicon wafers and advanced interposer materials, limits production scaling. Additionally, the capital‑intensive nature of novel packaging equipment raises entry barriers, prompting manufacturers to prioritize incremental capacity upgrades over expansive roll‑outs. These pressures contribute to longer lead times and elevate unit costs, compelling OEMs to scrutinize cost‑benefit trade‑offs when selecting packaging options. Nonetheless, firms are mitigating risk through diversified sourcing strategies and strategic inventory buffers, which help sustain momentum despite the logistical bottlenecks. To further address these issues, several players are investing in localized production hubs and adopting digital‑twin simulations for process optimization, reducing material waste and improving yield.

Strategic Partnerships Accelerate Adoption

Strategic partnerships are accelerating adoption across the ecosystem, reinforcing AI Accelerator Advanced Packaging Market trajectory. Leading foundries such as TSMC, Samsung Electronics, and Intel Corp. have entered joint development programs with packaging specialists to co‑design next‑generation solutions that align with emerging AI compute standards. These collaborations streamline technology transfer, reduce time‑to‑market, and distribute R&D risk across multiple stakeholders. Moreover, alliances with equipment manufacturers are enabling higher throughput and yield improvements in advanced stacking processes. The combined effect of shared expertise and pooled investment is fostering a more resilient supply chain and catalyzing broader deployment of high‑performance AI accelerators in both cloud and edge environments. In addition, joint standardization efforts through industry consortia are shaping common design rules, ensuring interoperability across heterogeneous components and driving economies of scale that lower total cost of ownership for AI accelerator deployments.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Accelerator Advanced Packaging: Competitive Dynamics and Market Leaders

AI Accelerator Advanced Packaging Market is dominated by a few large foundries and packaging specialists that control the majority of capacity and technology roadmaps. TSMC leverages its leading fan‑out wafer‑level packaging (FOWLP) platform to serve high‑volume AI compute chips, while Samsung Electronics combines 3D‑IC stacking with its advanced logic nodes to offer integrated solutions for data‑center accelerators. Intel Corp. has accelerated its package‑on‑package (PoP) and heterogeneous integration capabilities through strategic investments in silicon photonics and interposer technologies, positioning itself as a key enabler for edge AI devices. Together, these leaders shape the market’s supply chain, dictate pricing trends, and set technical standards that smaller players must follow.

Beyond the tier‑one founders, a cohort of specialized packaging firms and fabless chip designers contributes significant niche value. ASE Technology Holding and Amkor Technology provide mature 2.5‑D and 3‑D stacking services for AI‑focused startups, while JCET Group (including the former STATS ChipPAC) targets cost‑effective heterogeneous solutions for automotive and IoT segments. GlobalFoundries and United Microelectronics Corp (UMC) support custom advanced packaging for mid‑range AI accelerators, and fabless leaders such as Nvidia, Qualcomm, Marvell Technology, and Broadcom integrate these packaging options into their product portfolios to differentiate performance and power efficiency. This diversified ecosystem fosters rapid innovation while maintaining competitive pressure across the value chain.

List of Key AI Accelerator Advanced Packaging Companies Profiled

- TSMC

- Samsung Electronics

- Intel Corp.

- ASE Technology Holding

- Amkor Technology

- JCET Group

- GlobalFoundries

- United Microelectronics Corp (UMC)

- Nvidia

- Qualcomm

- Marvell Technology

- Broadcom Inc

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Fan‑out Wafer‑Level Packaging (FOWLP) is emerging as the most attractive type because it delivers a fine balance between high density interconnects and thermal management. • Provides excellent signal integrity for AI inference engines. • Enables thinner form‑factors suited for edge accelerators. • Simplifies supply‑chain integration with existing wafer‑fab lines, fostering quicker time‑to‑market for new AI chips. The other types such as CoW and heterogeneous 3D stacking are valued for their ability to co‑locate memory and logic, but they require more complex alignment processes and are favored in high‑performance data‑center solutions. |

| By Application |

|

Data‑Center AI Accelerators dominate the application landscape due to relentless demand for massive compute throughput. • Advanced packaging enables dense interconnects that reduce latency between compute cores and high‑bandwidth memory. • Provides power‑efficiency gains that align with sustainability goals of hyperscale operators. Edge devices benefit from compact FOWLP solutions that fit within constrained footprints, while autonomous systems rely on heterogeneous 3D stacking to integrate sensor processing and inference in a single package, ensuring real‑time decision making. |

| By End User |

|

Technology Vendors are leading the push for sophisticated packaging because they own the intellectual property that unlocks AI workload efficiency. • They collaborate closely with foundries to co‑develop process nodes that complement advanced packaging layers. • Their roadmaps prioritize integration of AI‑specific memory stacks, which shapes the ecosystem for system integrators and OEMs. System integrators leverage these packages to differentiate product portfolios, while automotive OEMs value the reliability and thermal performance offered by heterogeneous 3D solutions for autonomous driving platforms. |

| By Integration Technology |

|

Chip‑Scale Interposer is gaining prominence because it bridges the gap between dense die‑to‑die connectivity and manageable thermal profiles. • Enables designers to embed high‑speed signaling without resorting to full 3D stacking, simplifying test and validation. • Provides a flexible substrate for mixing logic, memory, and analog components in AI accelerators. SOI platforms are valued for their electrical isolation, while embedded passive components reduce board‑level complexity, both supporting the overall trend toward compact, high‑performance AI modules. |

| By Market Driver |

|

Performance‑Driven AI Workloads push vendors to adopt packaging that maximizes bandwidth and minimizes latency. • The need for real‑time inference in autonomous vehicles and edge devices fuels demand for tightly integrated memory and compute. • Thermal challenges encourage the use of packaging architectures that spread heat efficiently, such as fan‑out and 3D stacking. Collaborative agreements between leading foundries and packaging innovators accelerate technology transfer, while a vibrant R&D ecosystem ensures continuous improvement of materials and processes. |

Regional Analysis: North America

North America

North America remains at the forefront of technological breakthroughs in advanced packaging for AI accelerators, with continuous research into 3D stacking, chiplets, and heterogeneous integration.

The North American market is populated by prominent semiconductor companies like Intel, AMD, NVIDIA, and Texas Instruments, along with innovative packaging solutions providers.

Government initiatives and funding programs are actively supporting the development and adoption of advanced packaging technologies for AI, fostering a favorable market environment.

A well-established and resilient supply chain network in North America ensures efficient manufacturing and distribution of AI accelerator packages.

North America

The North American AI Accelerator Advanced Packaging Market is characterized by high-performance demands across diverse sectors. The burgeoning cloud computing industry necessitates increasingly powerful AI accelerators, creating significant demand for advanced packaging solutions. Furthermore, the expansion of edge AI deployments in areas like industrial automation and smart cities is directly contributing to market growth. The adoption of chiplet designs and 3D integration is gaining traction, allowing for higher performance and energy efficiency in AI systems. Research and development efforts are heavily focused on improving thermal management and reducing power consumption in these complex packages. The region’s strong intellectual property ecosystem and skilled workforce provide a competitive advantage in this rapidly evolving landscape. The focus on specialized packaging tailored to specific AI workloads is also a key trend shaping the market in North America.

Europe

Europe presents a significant, yet evolving, market for AI Accelerator Advanced Packaging. Driven by initiatives like the European Chips Act, there’s a strong push to bolster domestic semiconductor capabilities and reduce reliance on external suppliers. The automotive sector, particularly in Germany and the UK, is a key driver, with increasing adoption of AI for autonomous driving and in-car infotainment systems. Research institutions across Europe are actively engaged in developing novel packaging technologies. While the market currently lags behind North America in terms of overall volume, the strategic investments and supportive policies position Europe for substantial growth in the coming years. Collaboration between industry, academia, and government is crucial to fostering innovation and commercialization in advanced packaging for AI.

Asia-Pacific

Asia-Pacific, spearheaded by China, Japan, and South Korea, is emerging as the largest and fastest-growing market for AI Accelerator Advanced Packaging. China’s significant investments in AI infrastructure and its rapidly expanding domestic semiconductor industry are the primary drivers of this growth. The demand for AI accelerators is surging across various applications, including smart manufacturing, retail, and healthcare. Japan and South Korea maintain a strong presence in high-end AI accelerator packaging, with significant R&D investments in advanced technologies. Despite geopolitical complexities, the Asia-Pacific region represents a critical growth engine for the global market. The focus is on cost-effective solutions to meet rapidly increasing demand.

South America

South America represents a nascent market for AI Accelerator Advanced Packaging, with potential for future growth. The increasing adoption of AI in sectors like financial services and agriculture is driving initial demand. However, limited domestic manufacturing capabilities and a reliance on imports currently characterize the region. Government initiatives focused on fostering technological development and attracting foreign investment could unlock significant opportunities in the long term. The cost of advanced packaging solutions remains a barrier to entry, but as the market matures, localized production and innovation could address these challenges.

Middle East & Africa

The Middle East and Africa are relatively small but rapidly growing markets for AI Accelerator Advanced Packaging. The increasing adoption of AI in sectors like oil and gas, healthcare, and smart cities is fueling demand. Government investments in technology and infrastructure are creating a favorable environment for market expansion. The region’s focus on digital transformation and its growing pool of skilled talent present significant opportunities for growth. While the market is still in its early stages, the potential for future growth is substantial, particularly with increased investment in AI-driven solutions.

Report Scope

This market research report provides a comprehensive analysis of the AI Accelerator Advanced Packaging Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Accelerator Advanced Packaging Market?

-> AI accelerator advanced packaging market size was valued at USD 3.45 billion in 2025. The market is projected to grow from USD 3.78 billion in 2026 to USD 7.12 billion by 2034.

Which key companies operate in AI Accelerator Advanced Packaging Market?

-> Key players include TSMC, Samsung Electronics, Intel Corp. These foundries drive advanced‑packaging adoption through large‑scale investments and strategic collaborations.

What are the key growth drivers?

-> Key growth drivers include rising AI compute demand across data centers, edge devices, and autonomous systems, which require higher bandwidth, lower latency, and improved power efficiency.

Which region dominates the market?

-> Asia‑Pacific leads due to the concentration of major semiconductor fabs and strong governmental support for AI and advanced packaging technologies.

What are the emerging trends?

-> Emerging trends include heterogeneous 3D stacking, fan‑out wafer‑level packaging (FOWLP), and chip‑on‑wafer (CoW) integration, which enable higher performance and lower power consumption for AI workloads.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...