Market Insights

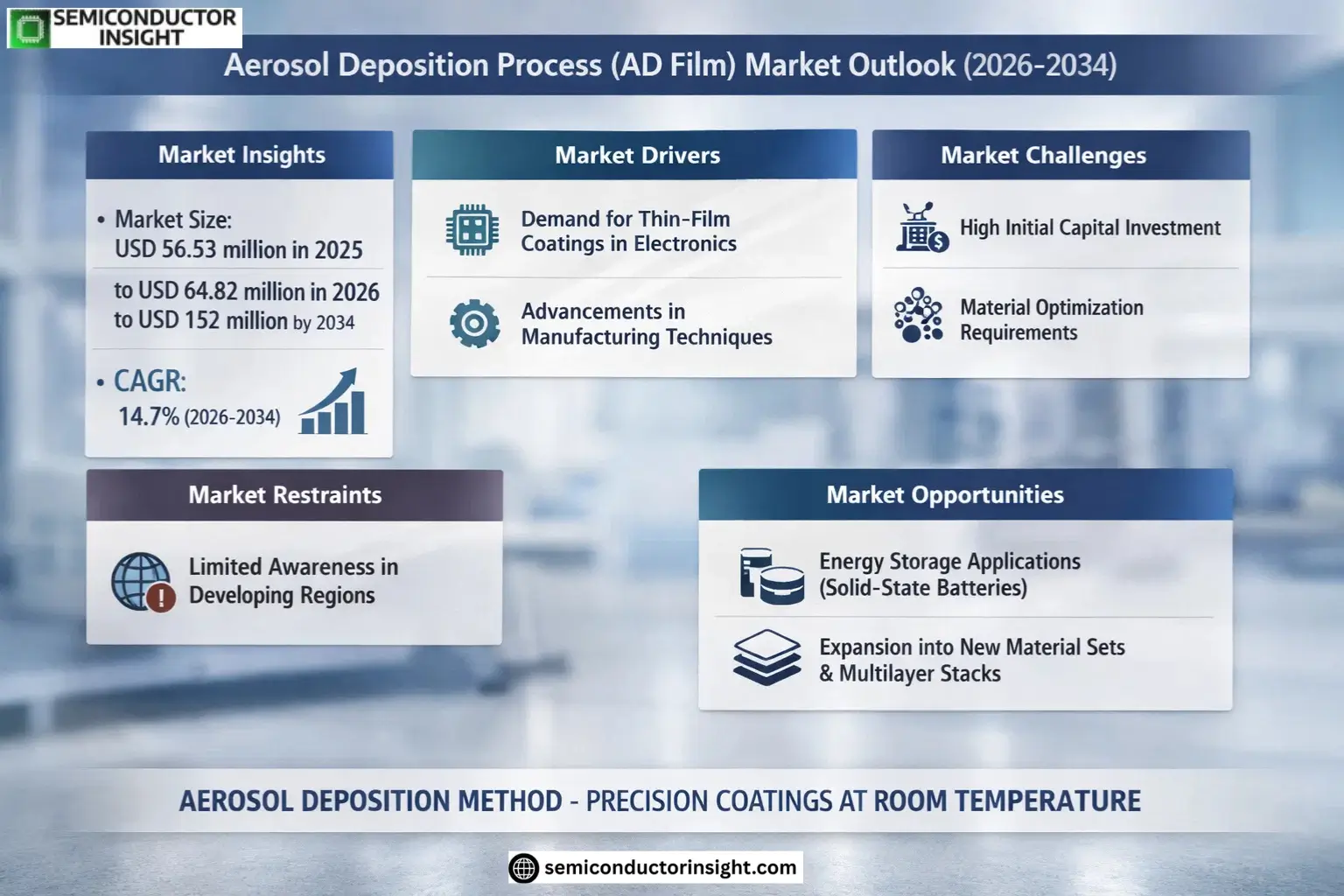

Global Aerosol Deposition Process (AD Film) Market size was valued at USD 56.53 million in 2025. The market is projected to grow from USD 64.82 million in 2026 to USD 152 million by 2034, exhibiting a CAGR of 14.7% during the forecast period.

Aerosol Deposition (AD), also known as Aerosol Deposition Method (ADM) or Powder Aerosol Deposition (PAD), is a room-temperature coating process that forms dense ceramic films through high-velocity particle impact consolidation. This technique enables deposition without high-temperature sintering, making it ideal for temperature-sensitive substrates and applications requiring precise material properties.

The technology’s adoption is accelerating due to its superior performance in semiconductor manufacturing, particularly for plasma-resistant coatings in etch chambers where particle contamination control directly impacts production yields. While yttrium oxide remains the dominant material, industry players are expanding into new compositions and multilayer structures to address evolving semiconductor process requirements and emerging applications in energy storage and electronic components.

MARKET DRIVERS

Growing Demand for Thin-Film Coatings in Electronics

Aerosol Deposition Process (AD Film) Market is experiencing significant growth due to the rising demand for thin-film coatings in the electronics sector. AD Film technology offers precise deposition of functional materials on various substrates, making it ideal for applications in semiconductor devices and display panels. Global push towards miniaturization and enhanced performance in electronic components is accelerating adoption.

Advancements in Manufacturing Techniques

Recent advancements in AD Film technology have improved process efficiency and material utilization rates, reducing production costs by approximately 18-22% compared to traditional methods. The ability to deposit uniform films at room temperature is particularly valuable for temperature-sensitive applications.

Environmental regulations favoring low-waste manufacturing processes are further propelling market growth, as AD Film generates minimal material waste compared to conventional deposition methods.

MARKET CHALLENGES

High Initial Capital Investment

The specialized equipment required for Aerosol Deposition Process technology represents a significant barrier to entry, with complete system costs ranging between USD 1.2-2.5 million. This limits adoption among small and medium-sized enterprises.

Other Challenges

Material Optimization Requirements

Effective implementation requires precise control of particle size distribution and carrier gas parameters, demanding extensive process optimization for each new material system.

MARKET RESTRAINTS

Limited Awareness in Developing Regions

Despite its advantages, the AD Film technology remains relatively unknown in developing markets, where traditional coating methods still dominate. This lack of technical expertise and awareness is slowing market penetration in these regions, particularly in South America and Africa.

MARKET OPPORTUNITIES

Emerging Applications in Energy Storage

Aerosol Deposition Process (AD Film) Market is gaining traction in battery manufacturing, particularly for solid-state batteries, where it enables precise electrode layer deposition. The technology’s ability to create dense, uniform films makes it particularly suitable for next-generation energy storage applications, presenting a USD 420 million opportunity by 2026.

Aerosol Deposition Process (AD Film) Market Trends

Expansion into New Material Sets and Multilayer Stacks

Aerosol Deposition Process (AD Film) Market is witnessing increased adoption of advanced material sets beyond traditional yttria-based coatings. Industry leaders are developing fluorinated and oxyfluoride ceramics to enhance plasma resistance in demanding semiconductor applications. Multilayer AD Film stacks are gaining traction as they combine different material properties while maintaining the process’s room-temperature advantage.

Other Trends

Semiconductor Equipment Manufacturing Dominates Demand

Over 75% of AD Film applications currently serve semiconductor etching equipment, where the technology’s particle control and plasma corrosion resistance directly impact production yields. Leading semiconductor equipment manufacturers continue to specify AD Film coatings for critical chamber components due to their superior performance compared to alternative deposition methods.

Geographic Market Growth Patterns

Asia-Pacific maintains the dominant position in the AD Film market, accounting for approximately 60% of global demand. This concentration aligns with regional semiconductor manufacturing clusters, particularly in South Korea, Japan, and Taiwan. North American and European markets are growing moderately, driven by semiconductor equipment maintenance and refurbishment activities.

Process Technology Advancements

Key equipment manufacturers are focusing on improving AD Film deposition parameters to achieve better large-area uniformity and higher throughput. Recent developments include optimized nozzle designs and advanced particle acceleration control, enabling tighter film property control. These improvements are critical for expanding AD Film applications beyond semiconductor equipment into energy storage and electronic components.

Competitive Landscape Developments

The market remains concentrated among specialist suppliers with semiconductor process qualifications. TOTO Advanced Ceramics and KoMiCo continue to lead, while newer entrants like Innojet Technology are gaining market share through innovations in advanced etch components. Collaboration between material suppliers and equipment manufacturers is intensifying to develop next-generation AD Film solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Aerosol Deposition Film Market Dominated by Specialized Ceramic Coating Providers

Global Aerosol Deposition Process (AD Film) Market is characterized by a concentrated competitive landscape with TOTO Advanced Ceramics, KoMiCo, and Heraeus High Performance Coatings emerging as the dominant players, particularly in semiconductor applications. These companies have established strong positions through proprietary AD coating technologies, deep semiconductor industry relationships, and rigorous qualification processes for plasma-resistant ceramic films. TOTO leads with its comprehensive ‘AD Film’ solutions and etch chamber component offerings, while KoMiCo has gained share through specialized coating services for semiconductor equipment refurbishment.

Niche competitors like Innojet Technology are gaining traction with innovations in nozzle designs and multi-material deposition capabilities. European coating specialists such as CemeCon and Plasma Innovations have also entered the space, leveraging their industrial coating expertise. Emerging Asian players are focusing on cost-competitive AD equipment solutions, while several Japanese material suppliers are developing optimized ceramic powders specifically for aerosol deposition processes.

List of Key Aerosol Deposition (AD Film) Companies Profiled

- TOTO Advanced Ceramics

- KoMiCo

- Heraeus High Performance Coatings

- Innojet Technology

- CemeCon AG

- Plasma Innovations GmbH

- Fujimi Incorporated

- Saint-Gobain Ceramics

- AGC Ceramics

- Nippon Steel Chemical & Material

- Rigaku Corporation

- Shin-Etsu Chemical

- Surmet Corporation

- Kyocera Corporation

- Sumitomo Chemical

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Yttrium Oxide (Y2O3) dominates the material segment due to:

|

| By Application |

|

Semiconductor Etching Equipment remains the key application driver because:

|

| By End User |

|

Semiconductor Equipment Manufacturers represent the primary demand source owing to:

|

| By Material Function |

|

Plasma-Resistant Coatings demonstrate strongest adoption due to:

|

| By Process Technology |

|

Multilayer Stack processes are gaining traction because:

|

Regional Analysis: Aerosol Deposition Process (AD Film) Market

Japan maintains technological superiority in AD Film applications for high-performance electronics, with major corporations developing proprietary deposition techniques. The country’s focus on miniaturization and energy efficiency aligns perfectly with AD Film advantages.

South Korean firms lead in scaling AD Film production for display technologies, supported by vertically integrated electronics corporations. The country’s advanced semiconductor industry drives demand for precision coating solutions.

China is rapidly catching up in AD Film technology through massive investments in materials science. Domestic manufacturers are adopting hybrid deposition systems combining AD with other thin film technologies for cost-competitive solutions.

Cross-border research initiatives among Asian universities and corporations are accelerating AD Film innovations. Shared testing facilities and technology transfer programs help smaller markets access advanced deposition capabilities.

North America

North America shows strong growth in specialized AD Film applications, particularly in aerospace and medical device coatings. The region benefits from close collaboration between national laboratories and private sector innovators developing next-generation deposition systems. U.S. defense contracts are driving advancements in durable AD Film coatings for harsh environments. Canadian research institutions are making strides in eco-friendly deposition processes, aligning with the region’s sustainability goals.

Europe

European markets focus on high-value AD Film applications in renewable energy and luxury automotive sectors. Strict environmental regulations push manufacturers toward cleaner deposition processes with reduced volatile organic compounds. Germany leads in industrial-scale adoption for precision optics, while Nordic countries pioneer AD Film solutions for energy storage applications. EU-funded consortia facilitate technology transfer across member states.

Middle East & Africa

The MEA region shows emerging potential in AD Film technology, particularly for solar energy applications and anti-corrosive coatings. Gulf nations are investing in deposition technology research centers as part of economic diversification strategies. South Africa demonstrates growing capabilities in industrial coatings, supported by local mineral resources essential for film precursors.

South America

South America’s AD Film market remains nascent but shows promise in niche applications for mining equipment and architectural coatings. Brazil leads regional adoption through automotive and aerospace industry demand. Research collaborations with North American institutions are helping build local expertise in deposition technology.

Report Scope

This market research report provides a comprehensive analysis of the Aerosol Deposition Process (AD Film) Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand-supply balance, regulatory landscape, and the strategic role of AD films in powering advancements across industries such as semiconductors, electronics, energy devices, and other functional ceramic applications.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by material type, process, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia, South America, and Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging AD film technologies, material advancements, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, and market-entry barriers.

- Stakeholder Insights: Strategic insights for component suppliers, OEMs, coating service providers, and investors regarding the evolving ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Aerosol Deposition Process (AD Film) Market?

-> Aerosol Deposition Process (AD Film) Market size was valued at USD 56.53 million in 2025. The market is projected to grow from USD 64.82 million in 2026 to USD 152 million by 2034, exhibiting a CAGR of 14.7% during the forecast period.

Which key companies operate in Aerosol Deposition Process (AD Film) Market?

-> Key players include TOTO Advanced Ceramics, KoMiCo, Heraeus High Performance Coatings, and Innojet Technology, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand in semiconductor plasma etch applications, superior plasma resistance of AD films, and expanding use in electronics and energy devices.

Which region dominates the market?

-> Asia is the dominant market for Aerosol Deposition Process (AD Film), with significant contributions from China, Japan, and South Korea due to strong semiconductor manufacturing presence.

What are the emerging trends?

-> Emerging trends include development of broader material sets beyond yttria (e.g., fluorinated ceramics), multilayer stacks, and higher throughput/larger-area uniformity solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...