MARKET INSIGHTS

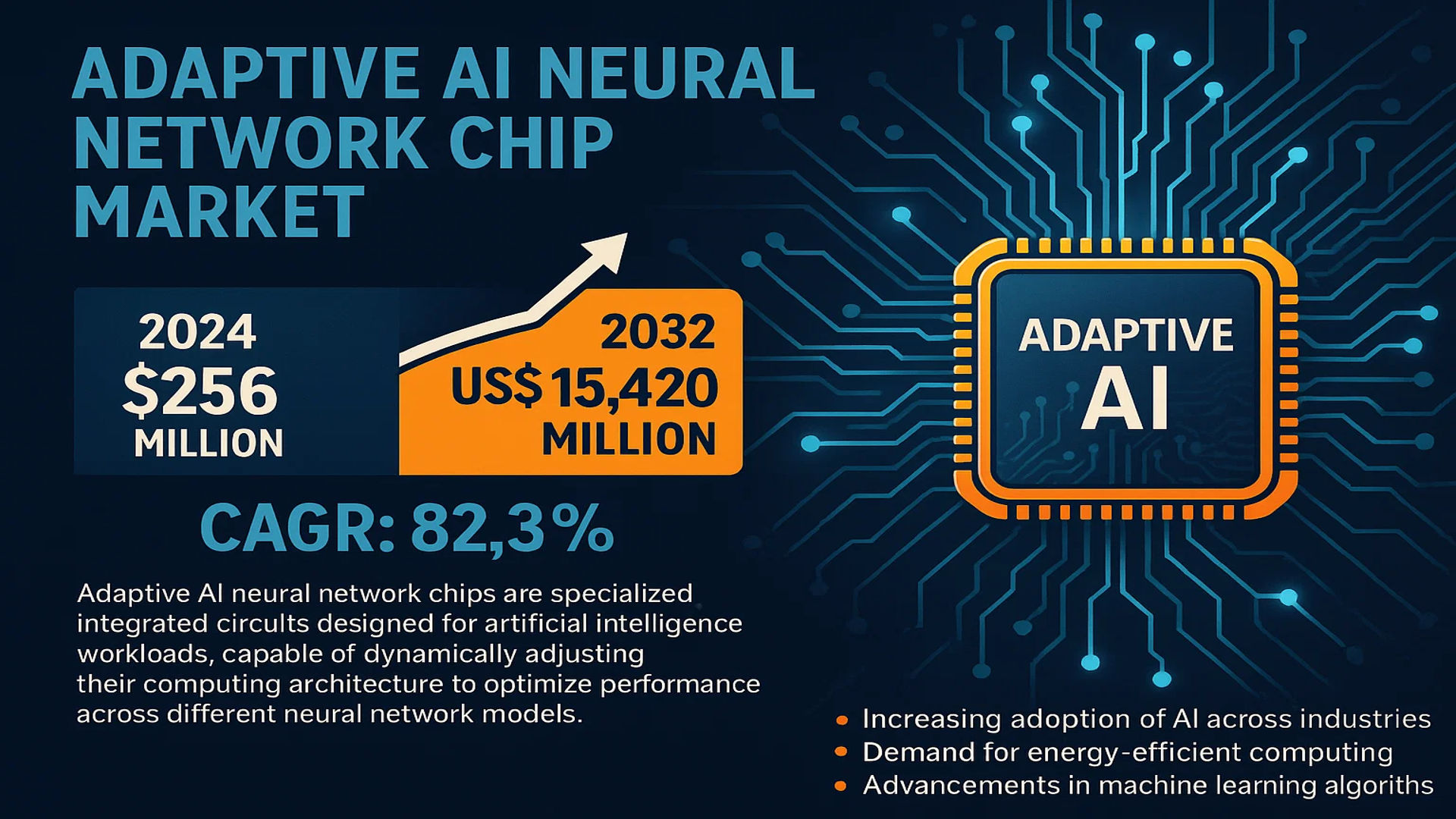

The global Adaptive AI Neural Network Chip Market was valued at 256 million in 2024 and is projected to reach US$ 15420 million by 2032, at a CAGR of 82.3% during the forecast period.

Adaptive AI neural network chips are specialized integrated circuits designed for artificial intelligence workloads, capable of dynamically adjusting their computing architecture to optimize performance across different neural network models. Unlike traditional fixed-architecture chips like GPUs or ASICs, these innovative processors automatically reconfigure computing paths based on task requirements, delivering superior efficiency and power optimization for AI applications.

The market’s explosive growth is driven by increasing adoption of AI across industries, demand for energy-efficient computing, and advancements in machine learning algorithms. Key players including NVIDIA, Google, Intel, and AMD are aggressively developing next-generation adaptive chips, with the Field Programmable Gate Array (FPGA) AI Chip segment showing particularly strong growth potential. While North America currently leads in adoption, Asia-Pacific is emerging as the fastest-growing region due to government investments in AI infrastructure.

MARKET DYNAMICS

MARKET DRIVERS

Expanding AI Workloads Across Industries Fueling Demand for Adaptive Chips

The exponential growth of artificial intelligence applications across sectors is creating unprecedented demand for specialized hardware. Adaptive AI neural network chips are becoming essential for running complex AI models efficiently, particularly as traditional architectures struggle with evolving computational demands. Industries such as autonomous vehicles, healthcare diagnostics, and financial forecasting require chips that can dynamically adjust to varying neural network structures in real-time. With autonomous vehicle AI models projected to reach over 500 million parameters by 2026, the need for adaptive processing power has never been greater. Major automotive players are increasingly embedding these chips to handle the sophisticated decision-making required for self-driving capabilities.

Energy Efficiency Advantages Driving Adoption in Edge Computing

Adaptive chips are revolutionizing edge computing by offering superior energy efficiency compared to traditional AI accelerators. Recent advancements have demonstrated up to 60% reduction in power consumption while maintaining comparable performance, making them ideal for battery-powered devices. This advantage is particularly crucial for IoT implementations and mobile applications where power constraints limit conventional AI chip deployment. Smart city infrastructure, for instance, benefits tremendously from these low-power solutions, enabling AI processing at network edges without the need for continuous cloud connectivity. Energy optimization features also make these chips attractive for data centers aiming to reduce their carbon footprint while handling increasingly complex AI workloads.

Military and Defense Applications Accelerating Market Growth

Global defense sectors are rapidly adopting adaptive AI chips for mission-critical applications, driving significant market expansion. These specialized processors enable real-time battlefield analysis, autonomous drone operations, and advanced surveillance systems with unparalleled responsiveness. Unlike fixed-architecture chips, adaptive solutions can be reconfigured in-field to accommodate changing mission parameters and threat landscapes. Recent military contracts have shown increasing allocations for adaptable AI hardware, reflecting their strategic importance in modern warfare systems. The ability to process encrypted communications while adapting to electronic warfare conditions makes these chips indispensable for next-generation defense platforms.

MARKET CHALLENGES

Design Complexity and Thermal Management Pose Significant Hurdles

While offering superior flexibility, adaptive AI chips present substantial design challenges that impact time-to-market and reliability. The complexity of creating reconfigurable architectures that maintain stability across operating conditions requires extensive engineering expertise. Thermal dissipation becomes particularly problematic when chips dynamically alter their processing pathways, creating hotspots that can affect performance and longevity. Recent industry tests have shown adaptive chips can experience temperature fluctuations up to 30% higher than static architectures during reconfiguration phases. These technical barriers require substantial R&D investments, often putting smaller manufacturers at a competitive disadvantage in the rapidly evolving market.

Other Challenges

Supply Chain Vulnerabilities

Semiconductor manufacturing disruptions continue to impact production timelines for specialized AI chips. The sophisticated materials and fabrication processes required for adaptive designs make them particularly susceptible to component shortages. Recent geopolitical tensions have further exacerbated these supply chain pressures, with lead times for certain substrates extending beyond 12 months in some cases.

Standardization Issues

The lack of universal design frameworks for adaptive architectures creates interoperability concerns across platforms. Without established industry standards, developers face challenges in ensuring software compatibility across different chip implementations, potentially limiting adoption in standardized enterprise environments.

MARKET RESTRAINTS

High Development Costs Limiting Market Penetration

The substantial R&D investments required for adaptive AI chip development create significant barriers to market entry. Unlike conventional AI accelerators, adaptive designs require specialized toolchains and verification processes that can increase development costs by 40-60%. These elevated expenses ultimately translate to higher consumer prices, making adoption challenging in price-sensitive sectors. While high-performance computing markets can absorb these costs, widespread implementation in consumer electronics and industrial IoT remains constrained by budget limitations. The specialized skill set required for adaptive chip programming further adds to implementation costs, requiring extensive developer training.

Regulatory Uncertainties Impacting Deployment Timelines

Evolving regulations surrounding AI hardware present another critical restraint for market growth. Governments worldwide are implementing stricter controls over AI processor exports, particularly those with military applications. These regulatory hurdles can delay product launches by 12-18 months while compliance is verified. Additionally, intellectual property protection remains a significant concern, with patent disputes increasing as companies race to establish dominance in this emerging field. The uncertain regulatory landscape makes long-term product planning challenging, potentially discouraging investments in next-generation adaptive architectures.

MARKET OPPORTUNITIES

Healthcare AI Revolution Creating New Growth Avenues

The healthcare sector represents a massive untapped opportunity for adaptive AI chip manufacturers. Medical AI applications require processors that can adapt to diverse data types—from imaging to genomic analysis—while maintaining stringent accuracy requirements. Adaptive chips capable of dynamic precision scaling are particularly well-suited for diagnostic equipment that processes both high-resolution medical scans and streaming patient vitals. Recent trials have shown 35% faster processing times for adaptive chips in complex diagnostic workflows compared to conventional AI accelerators. As hospitals worldwide digitize their operations, the demand for these specialized processors in medical devices and diagnostic systems is poised for exponential growth.

5G Edge Networks Driving Next Wave of Adoption

The global rollout of 5G networks is creating compelling opportunities for adaptive AI chips in telecommunications infrastructure. Network operators require intelligent edge devices that can process data locally while adapting to fluctuating network conditions and traffic patterns. Adaptive processors enable base stations to dynamically optimize signal processing algorithms based on real-time demand, significantly improving network efficiency. Major telecom equipment providers are increasingly integrating these chips into their next-generation infrastructure, with deployment expected to accelerate as 5G adoption reaches critical mass. The ability to handle diverse workloads—from beamforming to network slicing—positions adaptive chips as foundational components in the evolving telecommunications landscape.

Strategic Partnerships Accelerating Commercialization Pathways

Collaborations between chip manufacturers and AI software developers are unlocking new commercialization opportunities. These partnerships enable hardware-software co-design that maximizes the performance benefits of adaptive architectures. Recent alliances have focused on optimizing popular AI frameworks for adaptive chip implementations, reducing the programming complexity that previously hindered adoption. Joint ventures between semiconductor firms and cloud providers are also driving innovation, creating vertically integrated solutions that combine adaptive processing with scalable infrastructure. As these ecosystems mature, they will lower barriers to entry for enterprises looking to leverage adaptive AI capabilities across their operations.

ADAPTIVE AI NEURAL NETWORK CHIP MARKET TRENDS

Advancements in Neural Network Architecture to Drive Market Growth

The adaptive AI neural network chip market is witnessing unprecedented growth due to significant advancements in neural network architecture. Unlike traditional fixed-architecture chips such as GPUs or FPGAs, adaptive AI chips dynamically reconfigure their processing pathways to optimize performance for varying workloads. This flexibility enables higher computational efficiency and reduced energy consumption—key factors driving adoption across industries. The market, valued at $256 million in 2024, is projected to reach $15,420 million by 2032, growing at a staggering CAGR of 82.3%.

Other Trends

Edge Computing Integration

The shift toward edge computing is fueling demand for adaptive AI chips as they enable real-time data processing with low latency. Industries such as autonomous vehicles and industrial IoT require localized AI decision-making, reducing dependence on cloud infrastructure. This trend is reflected in the automotive sector’s rapid adoption, where adaptive neural chips enhance safety through real-time object recognition and predictive analytics, even in resource-constrained environments.

Rising Demand in Healthcare Applications

The medical industry is leveraging adaptive AI chips for applications ranging from diagnostic imaging to drug discovery. Their ability to process complex genomic datasets and medical imaging with adaptive precision supports advancements in personalized medicine. Key applications include real-time MRI analysis, where adaptive chips reduce processing times by 40% compared to conventional systems, while maintaining diagnostic accuracy. The segment is expected to grow at a 78% CAGR through 2032.

Competitive Landscape and Regional Dynamics

The market is dominated by key players such as NVIDIA, Intel, and Google, which collectively hold over 50% revenue share. Meanwhile, regional dynamics show robust growth in Asia-Pacific, particularly China, where government investments in AI R&D are accelerating chip development. North America remains a technology leader, with the U.S. accounting for nearly 35% of global adaptive AI chip production. Europe follows closely, driven by automotive and industrial automation demand.

COMPETITIVE LANDSCAPE

Key Industry Players

Technology Giants and Specialized Chipmakers Compete for AI Hardware Dominance

The global adaptive AI neural network chip market is highly dynamic, with established semiconductor leaders and agile AI specialists vying for market share. Nvidia currently dominates the sector, leveraging its early-mover advantage in GPU-accelerated AI computing and continuous architectural innovations like the Hopper H100 tensor core GPU. The company captured approximately 44% of the data center AI chip market in 2024, according to industry estimates.

Intel and AMD are aggressively expanding their AI silicon portfolios through strategic acquisitions and architectural breakthroughs. Intel’s acquisition of Habana Labs and AMD’s integration of Xilinx FPGA technology demonstrate how traditional chipmakers are adapting to compete in this high-growth sector. Meanwhile, Google’s Tensor Processing Units (TPUs) have gained significant traction in cloud-based AI services, particularly for transformer-based models.

The market also features several specialized AI chip designers making strategic moves. Graphcore recently unveiled its Bow IPU with 3D wafer-on-wafer technology, while Cerebras continues pushing the boundaries of wafer-scale integration. Chinese players like Huawei and Cambricon are also expanding internationally despite geopolitical challenges, with Huawei’s Ascend chips showing particularly strong adoption in domestic markets.

Startups and established players alike are increasing R&D investment, with industry analysts estimating adaptive AI chip development budgets grew 62% year-over-year in 2024. Recent collaborations between chip designers and major cloud providers signal potential shifts in the competitive balance as vertical integration increases.

List of Key Adaptive AI Neural Network Chip Companies

- Nvidia Corporation (U.S.)

- Intel Corporation (U.S.)

- Advanced Micro Devices (AMD) (U.S.)

- Google AI (U.S.)

- Tesla, Inc. (U.S.)

- Apple Inc. (U.S.)

- Huawei Technologies (China)

- Cambricon Technologies (China)

- Graphcore (UK)

- Cerebras Systems (U.S.)

Segment Analysis:

By Type

Field Programmable Gate Array AI Chip Leads Due to High Flexibility in AI Workload Optimization

The market is segmented based on type into:

- Field Programmable Gate Array (FPGA) AI Chip

- Application-Specific Integrated Circuit (ASIC) AI Chip

- Graphics Processing Unit (GPU) AI Chip

- Tensor Processing Unit (TPU) AI Chip

- Others

By Application

Automotive Industry Dominates Due to Rising Demand for Autonomous Vehicles and AI-powered ADAS

The market is segmented based on application into:

- Automotive Industry

- Medical Industry

- Financial Industry

- Consumer Electronics

- Industrial Automation

By Technology

Deep Learning Accelerators Segment Leads Due to Growth in Complex Neural Network Processing

The market is segmented based on technology into:

- Deep Learning Accelerators

- Edge AI Processors

- Neuromorphic Computing Chips

- Cloud AI Acceleration

By End User

Enterprise Segment Dominates Through AI Adoption Across Business Processes

The market is segmented based on end user into:

- Enterprise

- Government & Defense

- Research Institutions

- Cloud Service Providers

Regional Analysis: Adaptive AI Neural Network Chip Market

North America

North America leads the global Adaptive AI Neural Network Chip market, driven by massive investments in AI research and strong adoption across consumer electronics, automotive, and enterprise applications. The U.S. accounts for over 38% of global market revenue, with tech giants like Nvidia, Intel, and Google driving innovation. Recent developments include Nvidia’s H100 Tensor Core GPU, which delivers adaptive AI acceleration for large language models. Government initiatives like the National AI Initiative Act further support R&D, positioning the region as the primary hub for next-generation chip development. Challenges include export restrictions on advanced chips to certain markets, which could impact long-term growth strategies.

Asia-Pacific

The Asia-Pacific region is experiencing the fastest growth (projected CAGR of 86.2%), led by China’s aggressive semiconductor self-sufficiency push and South Korea’s AI chip manufacturing advancements. China accounts for 32% of global demand, with Huawei’s Ascend AI processors and Cambricon’s MLU chips gaining traction despite U.S. sanctions. Japan and Taiwan are key players in advanced packaging technologies essential for adaptive chips. However, geopolitical tensions and uneven intellectual property protections create volatility in supply chains, though the region remains critical for cost-effective mass production.

Europe

Europe maintains a strong position in specialized industrial applications of adaptive AI chips, particularly in automotive (for autonomous driving) and medical diagnostics. The EU’s Chips Act allocates €43 billion to boost semiconductor sovereignty, with companies like Graphcore (UK) and ASML (Netherlands) playing pivotal roles in chip design and manufacturing equipment. Strict GDPR compliance requirements shape product development priorities toward edge computing solutions with built-in privacy features. The market shows steady rather than explosive growth, constrained by fewer homegrown hyperscale tech firms compared to the U.S. and China.

Middle East & Africa

This emerging market is witnessing strategic investments in AI infrastructure, particularly in UAE and Saudi Arabia’s smart city projects. The UAE’s G42 group has partnered with Cerebras to deploy adaptive AI systems, while Israel’s AI chip startups focus on military and cybersecurity applications. Growth is tempered by limited local fab capacity—most chips are imported—but government-backed initiatives aim to develop regional AI capabilities. The market shows promise in financial services applications, though adoption lags other regions in consumer segments.

South America

South America represents the smallest but gradually expanding market, with Brazil leading in fintech and agricultural tech applications. The lack of domestic semiconductor manufacturing means complete reliance on imports, primarily from the U.S. and China. Economic instability and currency fluctuations present challenges for long-term investments, though increasing AI adoption in banking and healthcare drives steady demand. Local startups increasingly incorporate off-the-shelf adaptive chips into customized solutions rather than developing native architectures.

Report Scope

This market research report provides a comprehensive analysis of the Global Adaptive AI Neural Network Chip Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Adaptive AI Neural Network Chip market was valued at USD 256 million in 2024 and is projected to reach USD 15,420 million by 2032, growing at a CAGR of 82.3%.

- Segmentation Analysis: Detailed breakdown by product type (Field Programmable Gate Array AI Chip, ASIC AI Chip, Graphics Processing Unit AI Chip, Tensor Processing Unit AI Chip), application (Automotive, Medical, Financial Industries), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America (U.S., Canada, Mexico), Europe (Germany, France, U.K., Italy), Asia-Pacific (China, Japan, South Korea), and other key regions with country-level analysis.

- Competitive Landscape: Profiles of leading market participants including Nvidia, Google, Intel, AMD, Tesla, Apple, Huawei, Cambricon, Graphcore, and Cerebras, covering their product offerings, R&D focus, manufacturing capacity, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging AI chip architectures, adaptive computing technologies, semiconductor fabrication advancements, and integration with next-generation AI applications.

- Market Drivers & Restraints: Evaluation of factors driving market growth (AI adoption, edge computing demand) along with challenges (supply chain constraints, high R&D costs).

- Stakeholder Analysis: Strategic insights for chip manufacturers, system integrators, investors, and policymakers regarding market opportunities and competitive positioning.

The research methodology combines primary interviews with industry experts and secondary data from verified sources to ensure accuracy and reliability of market insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Adaptive AI Neural Network Chip Market?

-> Adaptive AI Neural Network Chip Market was valued at 256 million in 2024 and is projected to reach US$ 15420 million by 2032, at a CAGR of 82.3% during the forecast period.

Which key companies operate in this market?

-> Key players include Nvidia, Google, Intel, AMD, Tesla, Apple, Huawei, Cambricon, Graphcore, and Cerebras.

What are the key growth drivers?

-> Key growth drivers include rising AI adoption across industries, demand for energy-efficient computing, and advancements in neural network architectures.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is expected to witness the fastest growth during the forecast period.

What are the emerging trends?

-> Emerging trends include edge AI chip deployment, neuromorphic computing, and integration with 5G networks.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...