MARKET INSIGHTS

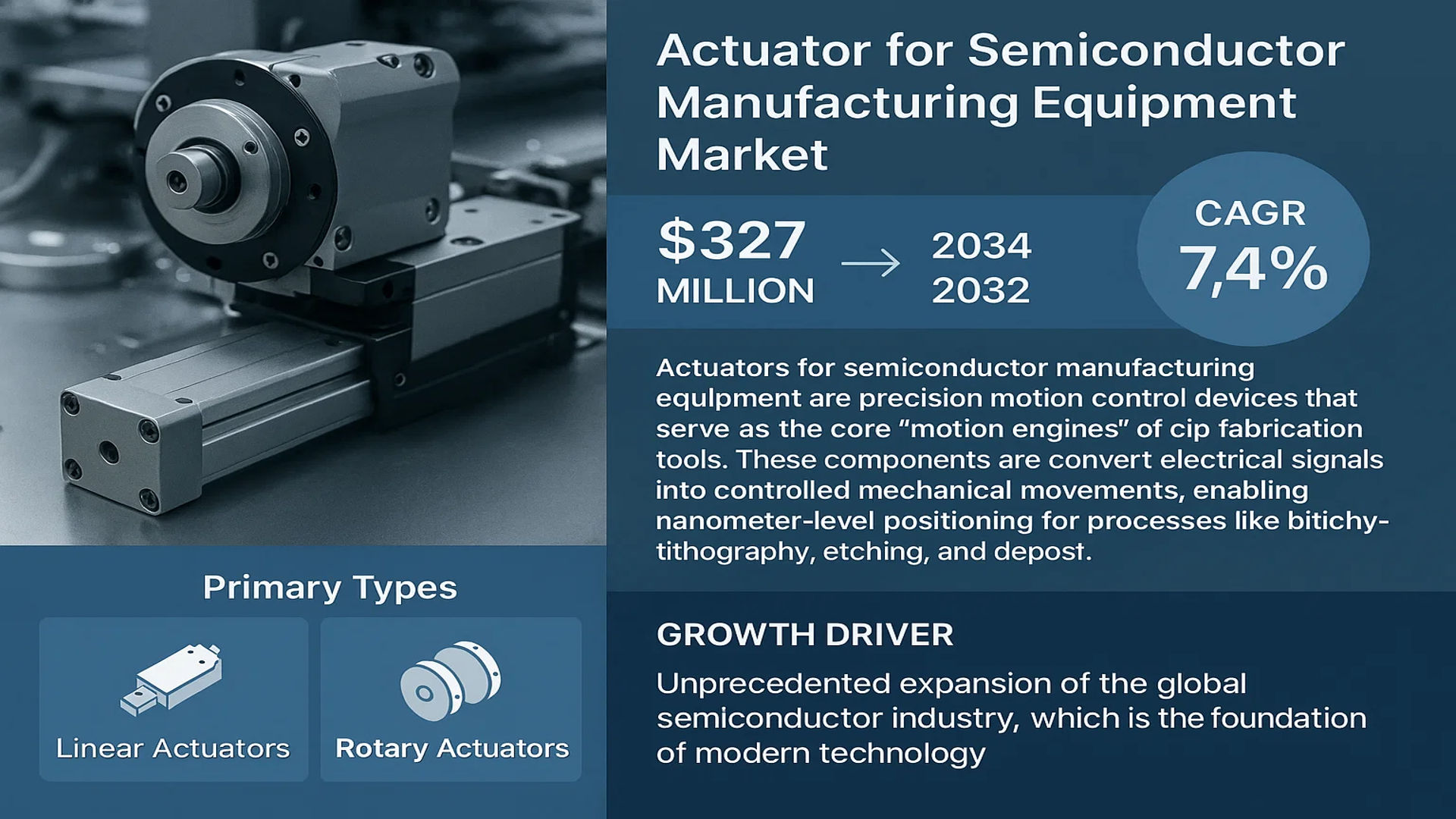

The global Actuator for Semiconductor Manufacturing Equipment Market was valued at 327 million in 2024 and is projected to reach US$ 516 million by 2032, at a CAGR of 7.4% during the forecast period.

Actuators for semiconductor manufacturing equipment are precision motion control devices that serve as the core “motion engines” of chip fabrication tools. These components are critical for converting electrical signals into highly controlled mechanical movements, enabling nanometer-level positioning essential for processes like photolithography, etching, and deposition. The primary types include linear actuators and rotary actuators, each designed to meet the extreme precision, reliability, and cleanliness standards required in semiconductor fabs.

The market is experiencing robust growth driven by the unprecedented expansion of the global semiconductor industry, which is the foundation of modern technology. This growth is fueled by rising demand for electronic products, the proliferation of 5G, IoT, and artificial intelligence (AI) applications, and the rapid advancement of the automotive and industrial electronics sectors. Furthermore, global government initiatives encouraging semiconductor investment, particularly in strategic regions like Taiwan, South Korea, China, the United States, and Japan, are significantly boosting equipment demand and, consequently, the actuators within them.

MARKET DYNAMICS

MARKET DRIVERS

Unprecedented Semiconductor Industry Growth Driving Actuator Demand

The semiconductor industry is experiencing unprecedented growth as semiconductors become the foundational technology for modern digital transformation. This expansion is driving demand for higher performance, efficiency, and reliability in semiconductor manufacturing equipment actuators. The global semiconductor market is projected to reach approximately $650 billion by 2025, creating substantial demand for manufacturing equipment and their critical components. Actuators serve as the core motion engines in semiconductor manufacturing equipment, with their performance directly determining equipment throughput and chip yield. In photolithography machines, for example, linear actuators control nanometer-level precise positioning of wafer stages and mask stages, requiring positioning accuracy within 2-3 nanometers for advanced nodes. The continuous advancement toward smaller process nodes below 3nm necessitates increasingly sophisticated actuator technologies capable of maintaining precision at atomic scales.

Emerging Applications and Technology Advancements Fueling Market Expansion

The semiconductor manufacturing industry’s expansion into new materials and applications is creating additional demand for specialized actuators. While silicon remains dominant, the growing adoption of compound semiconductors including silicon carbide (SiC), gallium nitride (GaN), and gallium arsenide (GaAs) requires specialized manufacturing processes and equipment. Each 300mm silicon wafer contains thousands of integrated chips, and the increasing manufacturing volumes demand more sophisticated equipment with enhanced actuator capabilities. The rapid growth of automotive electronics, particularly in electric and autonomous vehicles, requires actuators that can ensure higher reliability and precision. Automotive applications demand semiconductor devices capable of operating in extreme conditions, necessitating actuators that maintain performance across temperature variations from -40°C to 150°C while providing consistent positioning accuracy.

Global Semiconductor Capacity Expansion and Government Initiatives Accelerating Growth

The semiconductor market is experiencing a robust recovery and capacity expansion in 2024, with wafer foundry and packaging/testing facilities expanding globally to meet strong demand. Governments worldwide are implementing substantial initiatives to encourage semiconductor investment, particularly in strategic regions including Taiwan, South Korea, China, the United States, and Japan. These regions have identified semiconductors as critical strategic industries, leading to significant investments in domestic manufacturing capabilities. Major semiconductor manufacturing equipment projects require thousands of precision actuators per facility, with a single advanced fabrication plant potentially utilizing over 50,000 precision actuators across various equipment types. The ongoing capacity expansion, coupled with technological migration to more advanced nodes, ensures sustained demand for high-precision actuators in semiconductor manufacturing equipment.

MARKET CHALLENGES

Extreme Precision Requirements and Technical Complexities Pose Significant Challenges

The semiconductor actuator market faces substantial technical challenges due to the extreme precision requirements of modern semiconductor manufacturing. As process nodes shrink below 5nm, actuators must achieve positioning accuracy within atomic-scale tolerances, often requiring sub-nanometer precision. This level of precision demands extraordinary technical sophistication in actuator design, manufacturing, and calibration. The development of actuators capable of maintaining such precision over millions of cycles presents significant engineering challenges, particularly when considering environmental factors including temperature fluctuations, vibration, and electromagnetic interference. These technical requirements drive extensive research and development investments, with leading manufacturers spending approximately 8-12% of their annual revenue on R&D to maintain technological competitiveness.

Other Challenges

Supply Chain Constraints and Component Availability

The global semiconductor equipment supply chain faces ongoing challenges related to component availability and lead times. Precision actuators require specialized materials, advanced sensors, and high-performance electronic components that often have extended procurement cycles. The increasing complexity of actuator systems necessitates components with exceptionally tight tolerances and specialized certifications, creating potential bottlenecks in manufacturing. These supply chain constraints can impact equipment delivery schedules and potentially delay semiconductor fabrication facility expansions, particularly when actuator lead times extend beyond 26 weeks for custom high-precision models.

Technical Expertise Shortage and Knowledge Transfer

The industry faces a significant shortage of qualified technical professionals capable of designing, manufacturing, and maintaining advanced semiconductor actuators. The specialized knowledge required for developing nanometer-precision motion systems is scarce, and the retirement of experienced engineers exacerbates this challenge. Knowledge transfer becomes increasingly difficult as actuator technology advances, requiring continuous training and development programs. This expertise shortage affects not only actuator manufacturers but also semiconductor equipment companies that integrate these components into their systems.

MARKET RESTRAINTS

High Development Costs and Economic Sensitivity Limiting Market Penetration

The development and manufacturing of precision actuators for semiconductor equipment involve substantial financial investments that restrain market growth. Advanced actuator systems require extensive research and development expenditures, specialized manufacturing facilities, and highly skilled personnel. The cost of developing a new high-precision actuator platform can exceed $50 million, considering the necessary investments in precision machining equipment, cleanroom facilities, and testing infrastructure. This financial barrier makes it challenging for new entrants to compete effectively, limiting innovation and market competition. Additionally, the semiconductor industry’s cyclical nature creates economic sensitivity, where equipment purchasing decisions are often deferred during industry downturns, directly impacting actuator demand.

Technical Integration Complexities and Compatibility Issues

Integrating advanced actuators into semiconductor manufacturing equipment presents significant technical challenges that restrain market growth. Each semiconductor equipment platform has unique interface requirements, control systems, and performance specifications, making actuator integration a complex engineering task. Compatibility issues between actuator systems and existing equipment control architectures can require extensive customization and validation processes. The need for seamless integration with equipment software systems, safety protocols, and maintenance frameworks adds layers of complexity to actuator implementation. These integration challenges often require specialized engineering teams and extended validation periods, potentially delaying equipment deployment and increasing total cost of ownership for semiconductor manufacturers.

Regulatory Compliance and Certification Requirements

Stringent regulatory requirements and certification processes present significant restraints for actuator manufacturers serving the semiconductor industry. Actuators must comply with international standards for electrical safety, electromagnetic compatibility, and environmental performance. The certification process for semiconductor-grade actuators often requires extensive testing and documentation, including validation of performance under continuous operation conditions. Compliance with regional regulations, particularly in markets with rigorous environmental and safety standards, adds complexity to global product distribution. These regulatory requirements necessitate substantial investments in testing facilities and quality assurance systems, increasing development timelines and costs while potentially limiting market access for smaller manufacturers.

MARKET OPPORTUNITIES

Advanced Technology Nodes and Next-Generation Manufacturing Creating New Opportunities

The ongoing transition to more advanced semiconductor technology nodes below 3nm presents significant opportunities for actuator manufacturers. These advanced nodes require entirely new levels of precision, stability, and reliability in manufacturing equipment. The development of extreme ultraviolet (EUV) lithography systems, advanced etching technologies, and atomic-layer deposition equipment creates demand for actuators with unprecedented performance characteristics. Each technology advancement requires corresponding improvements in motion control systems, with opportunities emerging in multi-axis precision positioning, vibration isolation, and thermal stability technologies. The migration to advanced packaging technologies, including 2.5D and 3D integration, further expands opportunities for specialized actuators capable of handling heterogeneous integration processes.

Strategic Collaborations and Technology Partnerships Driving Innovation

Increasing strategic collaborations between actuator manufacturers, semiconductor equipment companies, and research institutions present substantial growth opportunities. These partnerships facilitate technology development, knowledge sharing, and accelerated innovation in precision motion systems. Joint development agreements enable actuator manufacturers to align their product development roadmaps with equipment makers’ future requirements, ensuring technology readiness for next-generation manufacturing processes. Collaborative research initiatives focusing on emerging technologies including artificial intelligence-based motion control, advanced materials for actuator components, and innovative drive technologies create opportunities for market differentiation and technological leadership. These partnerships often lead to exclusive supply agreements and long-term relationships that provide stable revenue streams and market position strengthening.

Geographic Expansion and Localization Initiatives Creating New Markets

Global initiatives for semiconductor manufacturing localization create substantial opportunities for actuator manufacturers to expand their geographic presence. Various countries are implementing policies to develop domestic semiconductor capabilities, leading to new fabrication facilities and equipment requirements. These geographic expansion initiatives require local supply chains and support networks, creating opportunities for actuator manufacturers to establish regional manufacturing, service, and support operations. The trend toward supply chain resilience and regional self-sufficiency in critical technologies drives demand for local actuator manufacturing and technical support capabilities. This geographic diversification reduces dependence on single regions and provides access to emerging semiconductor manufacturing hubs, potentially increasing market share and revenue stability.

ACTUATOR FOR SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET TRENDS

Advancements in Semiconductor Process Nodes to Drive Demand for High-Precision Actuators

The relentless drive towards smaller semiconductor process nodes, particularly below 5nm, is fundamentally reshaping actuator requirements. As feature sizes shrink to atomic scales, the demand for sub-nanometer positioning accuracy in equipment like EUV lithography scanners and atomic layer deposition systems has become non-negotiable. This technological arms race has accelerated the adoption of piezoelectric and voice coil actuators, which offer the exceptional resolution and stability needed for these advanced processes. Furthermore, the transition to larger 450mm wafer prototypes in R&D facilities is creating parallel demand for actuators with greater load capacity and travel range without compromising precision. This trend is not merely about incremental improvement but represents a fundamental shift in motion control philosophy, where vibration damping, thermal stability, and minimal particulate generation have become as critical as positional accuracy itself.

Other Trends

Integration of Industry 4.0 and Predictive Maintenance

The semiconductor industry’s embrace of Industry 4.0 principles is transforming actuators from simple motion components into intelligent, data-generating subsystems. Modern actuators are increasingly equipped with integrated sensors for real-time monitoring of parameters like temperature, vibration, and force feedback. This data enables predictive maintenance models, allowing equipment manufacturers and foundries to anticipate failures before they cause costly unplanned downtime. In a high-volume manufacturing environment where equipment availability directly impacts revenue, the ability to predict and schedule maintenance can improve overall equipment effectiveness (OEE) by a significant margin. This shift is also facilitating remote diagnostics and support, a crucial advantage for global semiconductor equipment suppliers servicing fabs worldwide.

Geopolitical Factors and Supply Chain Resilience Reshaping Sourcing Strategies

Recent global chip shortages and heightened geopolitical tensions have underscored the strategic importance of a resilient semiconductor supply chain, impacting the actuator market profoundly. Major economies are implementing policies to onshore or friend-shore critical semiconductor manufacturing capabilities, leading to a surge in fab construction. This wave of investment directly fuels demand for manufacturing equipment and their core components, including actuators. Consequently, equipment manufacturers are diversifying their supplier base to mitigate risks, creating opportunities for actuator suppliers who can guarantee supply chain security and geopolitical neutrality. This trend prioritizes not just technical specifications but also reliability of supply, local support capabilities, and adherence to international trade regulations, making the actuator sourcing decision more strategic than ever before.

COMPETITIVE LANDSCAPE

Key Industry Players

Precision and Reliability Drive Strategic Positioning in a High-Stakes Market

The competitive landscape of the global actuator for semiconductor manufacturing equipment market is characterized by a mix of established multinational corporations and specialized niche players, all vying for dominance in a sector where nanometer-level precision is non-negotiable. The market is semi-consolidated, with innovation and technical expertise serving as the primary differentiators. While the demand for more advanced nodes and complex chip architectures drives growth, it simultaneously raises the performance bar, compelling manufacturers to continuously invest in research and development.

THK Co., Ltd. and Bosch Rexroth AG are recognized as dominant forces, collectively holding a significant portion of the market share. Their leadership is largely attributed to extensive product portfolios that cater to the entire semiconductor fabrication process—from lithography and etching to deposition and metrology. Both companies boast a strong global footprint, with substantial manufacturing and support facilities in key semiconductor hubs like Asia, North America, and Europe, allowing them to serve major equipment OEMs directly and respond swiftly to regional demand fluctuations.

Meanwhile, companies like Parker Hannifin Corporation and Sinfonia Technology Co., Ltd. have carved out strong positions by focusing on high-reliability motion solutions for critical applications. Parker Hannifin’s recent developments in ultra-clean, vacuum-compatible linear actuators are specifically engineered for deposition and etching tools, a segment experiencing growth due to the proliferation of 3D NAND and advanced logic chips. Their strategy involves deep collaboration with equipment manufacturers to co-develop customized solutions, thereby embedding themselves firmly in the supply chain.

Specialized players, including TAKANO Co., Ltd. and Citizen Chiba Precision Co., Ltd., compete effectively by focusing on specific actuator types or applications. TAKANO, for instance, is renowned for its high-precision rotary actuators used extensively in wafer handling and packaging equipment. Their growth is fueled by the ongoing expansion in backend packaging and testing capacity, particularly across Asia. These companies strengthen their market presence not through sheer scale, but through technological specialization, often achieving leading positions in their chosen niches.

The competitive dynamics are further intensified by strategic movements such as mergers, acquisitions, and partnerships aimed at technology integration and market expansion. For example, Ewellix, a former SKF Group company, was acquired by Schaeffler Group to enhance its linear motion capabilities for industrial automation, including semiconductors. This consolidation trend is expected to continue as companies seek to offer more comprehensive motion solution packages and secure their supply chains against global disruptions.

List of Key Actuator for Semiconductor Manufacturing Equipment Companies Profiled

- THK Co., Ltd. (Japan)

- Bosch Rexroth AG (Germany)

- Parker Hannifin Corporation (U.S.)

- Allient Inc. (U.S.)

- Sinfonia Technology Co., Ltd. (Japan)

- TAKANO Co., Ltd. (Japan)

- Ewellix (Switzerland)

- Tolomatic Inc. (U.S.)

- Citizen Chiba Precision Co., Ltd. (Japan)

- Cosmic Industry Co., Ltd. (South Korea)

Segment Analysis:

By Type

Linear Actuators Segment Dominates the Market Due to Critical Role in Precision Positioning Applications

The market is segmented based on type into:

- Linear Actuators

- Subtypes: Piezoelectric, Ball Screw, Lead Screw, and others

- Rotary Actuators

- Subtypes: Electric Rotary, Pneumatic Rotary, and others

By Application

Lithography Segment Leads Due to Extreme Precision Requirements for Advanced Node Chip Manufacturing

The market is segmented based on application into:

- Lithography

- Etching

- Deposition

- Inspection and Metrology

- Cleaning

- Packaging and Testing

- Others

By Actuation Technology

Electric Actuators Hold Largest Share Owing to Superior Control and Precision Capabilities

The market is segmented based on actuation technology into:

- Electric Actuators

- Subtypes: Servo Motors, Stepper Motors, and others

- Pneumatic Actuators

- Hydraulic Actuators

- Piezoelectric Actuators

By Motion Control

Precision Positioning Segment Leads Driven by Nanometer-Level Accuracy Requirements in Semiconductor Fabrication

The market is segmented based on motion control into:

- Precision Positioning

- High-Speed Movement

- Vibration Control

- Force Control

Regional Analysis: Actuator for Semiconductor Manufacturing Equipment Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global actuator market for semiconductor manufacturing equipment, driven by its position as the world’s semiconductor manufacturing hub. This dominance is fueled by massive government-backed investment initiatives, such as China’s “Big Fund” and South Korea’s K-Semiconductor Strategy, which collectively represent hundreds of billions of dollars in capital expenditure aimed at achieving self-sufficiency and technological leadership. The region’s high concentration of leading-edge foundries, including TSMC in Taiwan and Samsung in South Korea, creates an insatiable demand for the most precise and reliable actuators, particularly for lithography and advanced packaging applications. While cost competitiveness remains a key factor, the primary market driver is the relentless pursuit of technological advancement to support the production of sub-5nm node chips, necessitating actuators capable of sub-nanometer precision and exceptional reliability to maximize yield.

North America

North America’s market is characterized by a strong focus on research, development, and innovation, particularly within the United States. The passage of the CHIPS and Science Act, which allocates over $52 billion in funding for domestic semiconductor research and manufacturing, is a monumental driver for the entire supply chain, including precision actuator suppliers. This legislative push aims to onshore critical manufacturing capabilities and reduce geopolitical supply chain risks. Consequently, demand is surging for actuators that support the production of legacy and leading-edge logic chips, as well as those essential for compound semiconductors like GaN and SiC, which are critical for electric vehicles and power electronics. The market is less volume-driven than Asia-Pacific but demands the highest levels of performance, innovation, and supply chain security from actuator manufacturers.

Europe

The European market is propelled by strategic ambitions to bolster its semiconductor sovereignty and strengthen its position in specific technology niches. The European Chips Act, with a mobilized budget exceeding €43 billion, is designed to double the EU’s global market share in semiconductors by 2030 and mitigate dependency on external sources. This initiative is creating significant opportunities for actuator suppliers, especially those serving equipment for automotive-grade semiconductors, power devices, and micro-electromechanical systems (MEMS), sectors where European companies hold a strong position. The demand is for highly reliable and durable actuators that can meet the stringent quality and safety standards required by the region’s dominant automotive industry, with a growing emphasis on partnering with local suppliers to ensure supply chain resilience.

South America

The semiconductor actuator market in South America is nascent and faces significant developmental challenges. The region lacks a substantial domestic semiconductor fabrication presence, resulting in a market that is primarily driven by the maintenance, servicing, and occasional upgrading of existing manufacturing equipment within packaging and testing facilities. Economic volatility and limited government investment in high-tech industrial policy constrain the growth of a local advanced manufacturing ecosystem. Consequently, demand for new, high-precision actuators is limited and often tied to multinational corporations upgrading specific production lines. The market is characterized by a strong focus on cost-effectiveness and the availability of reliable after-sales support for existing equipment, rather than the adoption of cutting-edge technology.

Middle East & Africa

The market in the Middle East and Africa is in its very early stages of development. While certain nations, particularly in the Gulf Cooperation Council (GCC) region, have expressed ambitious economic diversification plans that include technology and manufacturing, these have yet to materialize into a significant semiconductor fabrication footprint. Current demand for actuators is almost exclusively linked to the operation and maintenance of equipment used in research institutions, universities, and small-scale electronics assembly plants. The absence of a cohesive regional strategy for semiconductor manufacturing, coupled with infrastructure gaps, means that the market for new manufacturing equipment actuators is negligible. Long-term growth is a possibility, but it is entirely dependent on successful execution of large-scale national visions that currently remain largely aspirational in the semiconductor domain.

Report Scope

This market research report provides a comprehensive analysis of the global Actuator for Semiconductor Manufacturing Equipment market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Actuator for Semiconductor Manufacturing Equipment Market?

->Actuator for Semiconductor Manufacturing Equipment Market was valued at 327 million in 2024 and is projected to reach US$ 516 million by 2032, at a CAGR of 7.4% during the forecast period.

Which key companies operate in Global Actuator for Semiconductor Manufacturing Equipment Market?

-> Key players include Allient, Parker Hannifin, THK, Bosch Rexroth, TAKANO Co.,Ltd, Ewellix, Sinfonia Technology, Cosmic Industry Co., Ltd, Tolomatic USA, and Citizen Chiba Precision, among others.

What are the key growth drivers?

-> Key growth drivers include unprecedented semiconductor industry growth, demand for higher precision and reliability, expansion into compound semiconductors (SiC, GaN, GaAs), and strong government investment incentives in strategic markets including the United States, Taiwan, South Korea, China, and Japan.

Which region dominates the market?

-> Asia-Pacific is the dominant and fastest-growing region, driven by major semiconductor manufacturing hubs in Taiwan, South Korea, China, and Japan.

What are the emerging trends?

-> Emerging trends include integration of AI for predictive maintenance and motion control, development of actuators for extreme precision in advanced lithography (EUV), and increased demand for reliability in automotive and industrial electronics applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...