3D Visual Perception Chip Market Insights

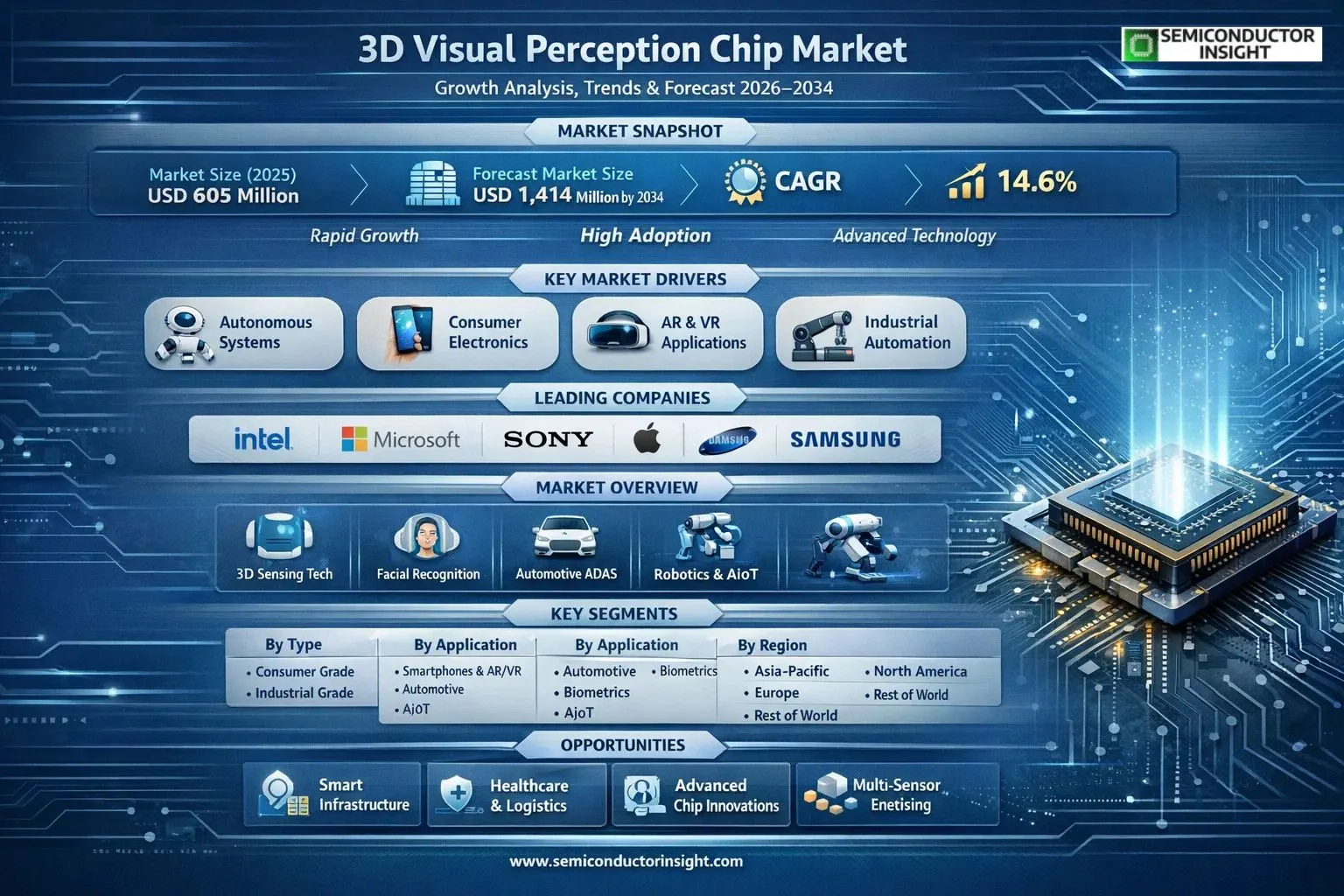

Global 3D visual perception chip market size was valued at USD 605 million in 2025. The market is projected to grow from USD 692 million in 2026 to USD 1,414 million by 2034, exhibiting a CAGR of 14.6% during the forecast period.

A 3D visual perception chip is a specialized semiconductor device that enables machines to perceive and interpret depth and spatial information from their environment. This technology is more stable than traditional imaging because it is not easily affected by complex lighting or external conditions, making it crucial for obtaining accurate depth data. As the key underlying core technology in modern 3D sensors, these chips operate on several technical principles, including binocular vision, structured light, lidar (Light Detection and Ranging), and time-of-flight (ToF) technology.

The market’s rapid expansion is driven by surging demand across multiple high-growth sectors. The proliferation of consumer electronics, such as smartphones with advanced facial recognition and augmented reality features, represents a major driver. Furthermore, the push towards automation in industrial settings and the automotive industry’s relentless advancement in Advanced Driver-Assistance Systems (ADAS) and autonomous vehicles are creating substantial demand for reliable depth-sensing solutions. Key industry players like Intel (with its RealSense technology), Microsoft, Sony, Apple, and Samsung are heavily invested in this space, continuously launching new products and forming strategic partnerships to capture market share. For instance, companies like Newsight Imaging are developing enhanced ToF sensors for automotive lidar, while others like Orbbec provide comprehensive 3D vision solutions for robotics and AIoT applications.

MARKET DRIVERS

Expansion of Autonomous Systems and Robotics

The primary engine for 3D Visual Perception Chip Market is the surging deployment of autonomous technologies. Advanced driver-assistance systems (ADAS) and autonomous mobile robots rely on real-time, accurate environmental mapping that only dedicated 3D vision processors can provide. These chips are critical for interpreting LiDAR, stereo vision, and time-of-flight sensor data, enabling safe navigation and object avoidance. The demand is further amplified by industrial automation, where robots require precise 3D perception for complex tasks like bin picking and assembly.

Rising Integration in Consumer Electronics and AR/VR

Beyond industrial and automotive applications, consumer electronics present a significant growth vector. The integration of 3D sensing for facial recognition, augmented reality (AR) effects, and gesture control in smartphones and headsets drives volume production. This consumer-scale adoption puts downward pressure on costs while spurring innovation in chip miniaturization and power efficiency, creating a positive feedback loop for the broader 3D Visual Perception Chip Market.

➤ Industry analysis indicates that the need for chips capable of processing high-resolution 3D point clouds in real-time, with low latency and power consumption, is non-negotiable for next-generation smart devices and machines.

Finally, advancements in artificial intelligence, particularly in edge AI, are a core driver. Modern 3D visual perception chips integrate specialized neural processing units (NPUs) to run complex computer vision algorithms directly on-device. This shift from cloud to edge processing is essential for applications requiring immediate response, data privacy, and operational reliability, thereby accelerating market adoption.

MARKET CHALLENGES

High Design Complexity and Integration Hurdles

A significant challenge in 3D Visual Perception Chip Market is the immense technical complexity of designing and manufacturing these semiconductors. They must efficiently fuse data from disparate 3D sensor modalities while performing sophisticated algorithm computations. Integrating various processing cores (CPU, GPU, NPU, DSP) into a single, low-power system-on-chip (SoC) requires substantial R&D investment and deep expertise, creating a high barrier to entry.

Other Challenges

Sensor Standardization and Data Processing

The lack of universal standards across different 3D sensing technologies (e.g., structured light vs. LiDAR) forces chip designers to create versatile, but often more complex and expensive, solutions. Furthermore, developing and optimizing the software stack and algorithms to extract meaningful information from raw 3D data adds considerable time and cost to system development.

Cost-Sensitivity in High-Volume Sectors

While performance is critical, achieving a competitive cost-per-chip is paramount for penetration into mass-market applications like consumer electronics and entry-level automotive. Balancing advanced performance with stringent cost targets under intense market competition remains a persistent challenge for vendors.

MARKET RESTRAINTS

Supply Chain Vulnerabilities and Geopolitical Factors

Global semiconductor supply chain’s fragility presents a major restraint. 3D Visual Perception Chip Market relies on advanced fabrication nodes and specialized packaging, which are concentrated in a few geographic regions. Trade tensions, export controls, and material shortages can disrupt production timelines and increase costs, delaying product launches and hindering market growth for even the most innovative chip designs.

Extended Development and Validation Cycles

The lengthy design, testing, and certification cycles, especially for safety-critical applications like autonomous vehicles, act as a brake on market velocity. A chip intended for automotive use requires years of rigorous validation to meet functional safety standards (e.g., ISO 26262). This protracted timeline delays revenue realization and increases the financial risk for companies investing in 3D Visual Perception Chip Market.

MARKET OPPORTUNITIES

Emergence of Smart Infrastructure and Spatial Computing

A frontier of opportunity lies in smart cities and infrastructure. 3D visual perception chips are key for intelligent traffic management, crowd monitoring, and security systems that understand the environment in three dimensions. Concurrently, the evolution towards immersive spatial computing,blending AR, VR, and the physical world,creates demand for powerful, efficient chips that can map and interact with 3D spaces in real time, opening new consumer and enterprise applications.

Healthcare, Logistics, and Niche Industrial Automation

Beyond mainstream applications, high-growth niche sectors offer substantial potential. In healthcare, these chips enable advanced surgical robotics and patient monitoring systems. In logistics, they facilitate automated dimensioning, sorting, and warehouse inventory drones. The ongoing push for Industry 4.0 will drive adoption in quality inspection and predictive maintenance on factory floors, providing diverse revenue streams for 3D Visual Perception Chip Market.

Advancements in Chiplet Architecture and Heterogeneous Integration

Technological innovation in semiconductor packaging itself presents a strategic opportunity. The adoption of chiplet-based designs and advanced heterogeneous integration allows for the modular combination of best-in-class processing cores (e.g., a leading-edge NPU with a mature I/O chiplet). This approach can reduce development cost and time, improve yield, and allow for more customizable solutions tailored to specific 3D perception tasks within the market.

Insights on 3D Visual Perception Chip Market Trends

Convergence of Technologies Drives Market Evolution

3D Visual Perception Chip market is experiencing significant transformation, driven by the deepening convergence of its core technical principles. The integration of technologies like Structured Light, Time of Flight (ToF), and LiDAR onto single-chip platforms is a dominant trend. This convergence, particularly in consumer electronics and automotive applications, enhances performance while optimizing size and power consumption. Chips are increasingly designed to support multiple sensing modalities, allowing devices to intelligently switch between or fuse data from different techniques to improve accuracy and reliability in varying environmental conditions. This multifunctional approach is expanding the utility and adoption of 3D Visual Perception Chip solutions beyond traditional use cases, creating versatile platforms for spatial computing.

Other Trends

Expansion into Next-Generation Applications

Beyond established areas like smartphone facial recognition and industrial automation, 3D Visual Perception Chip market is seeing strong growth in the AIoT and advanced automotive sectors. The rise of smart homes, robotics, and augmented reality devices within the AIoT ecosystem demands robust, low-power chips for environmental mapping and object interaction. In the automotive space, chips are fundamental to in-cabin monitoring for driver alertness and gesture control, as well as to exterior perception systems that complement traditional cameras and radar for enhanced autonomy and safety features.

Consolidation and Specialist Innovation

The competitive landscape features established technology and semiconductor giants alongside specialized innovators. While major players like Apple, Samsung, Sony, and Intel leverage vast resources for integration into their consumer ecosystems, companies such as Orbbec, Newsight Imaging, and Inuchip are driving innovation in specific technical niches and emerging application areas. This dynamic creates a market where broad-scale manufacturing capability coexists with targeted R&D, particularly in cost-optimized and application-specific 3D Visual Perception Chip designs for industrial and biometric uses.

Regional Demand Dynamics and Supply Chain Focus

Geographically, the market for 3D Visual Perception Chips is underpinned by strong R&D investment in North America and massive manufacturing and application demand from the Asia-Pacific region, particularly China and South Korea. This has led to heightened focus on supply chain resilience and regional capacity development. Strategic partnerships between chip designers, sensor module makers, and end-device manufacturers are becoming more common to secure supply and co-develop optimized solutions. The push for technological sovereignty is also influencing investment flows, fostering local innovation hubs dedicated to 3D perception technologies alongside the established global supply network.

COMPETITIVE LANDSCAPE

Key Industry Players

A Market Driven by Semiconductor Giants and Specialized Innovators

Global 3D Visual Perception Chip market is characterized by a dynamic mix of established semiconductor behemoths and agile, specialized technology firms. The competitive landscape is moderately concentrated, with the top five players accounting for a significant revenue share as of recent analyses. Dominance is held by a handful of vertically integrated consumer electronics titans like Apple and Samsung, which leverage these chips for in-house applications in smartphones, tablets, and wearable devices, and technology giants such as Intel and Microsoft, which provide core sensing platforms like RealSense and Azure Kinect for broader developer and industrial adoption. This segment exerts considerable pricing and technological influence, with heavy investment in R&D for Time of Flight (ToF), structured light, and advanced binocular vision technologies.

Beyond these leaders, a vibrant ecosystem of niche players drives innovation in specific applications and technologies. Companies like Newsight Imaging specialize in enhanced CMOS image sensors for LiDAR and machine vision, while Infineon provides essential components like ToF sensor chips. Pure-play 3D sensing firms, such as Orbbec and Aivatech, focus on complete 3D camera modules and perception solutions for robotics, biometrics, and AIoT. Emerging fabless semiconductor companies, including Inuchip, are also gaining traction by developing dedicated, low-power perception processors for edge AI applications in automotive and industrial automation, creating a fragmented yet highly innovative competitive layer beneath the market leaders.

List of Key 3D Visual Perception Chip Companies Profiled

- Intel Corporation

- Microsoft Corporation

- Sony Group Corporation

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Newsight Imaging Ltd.

- Infineon Technologies AG

- Orbbec

- Inuchip

- Aivatech

- STMicroelectronics N.V.

- Texas Instruments Incorporated

- OmniVision Technologies, Inc.

- AMS OSRAM AG

- Himax Technologies, Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Consumer Grade chips are the leading segment, driven by massive integration into high-volume consumer electronics which places a premium on cost-effectiveness and mass manufacturability. Their design prioritizes stability in diverse lighting conditions and compact form factors to fit within smartphones, tablets, and AR/VR headsets. Advanced consumer applications like facial recognition for biometric security and immersive gaming experiences are primary growth catalysts, encouraging continuous innovation from major technology firms. |

| By Application |

|

Consumer Electronic applications dominate, as this segment is the primary conduit for bringing 3D sensing capabilities to a global mass market. The integration of these chips enables sophisticated features including enhanced photography with portrait modes, secure facial recognition for device unlocking and payments, and gesture control for interactive gaming. The relentless push for more intuitive and immersive user interfaces in smartphones, laptops, and wearable devices ensures sustained R&D investment and chip iteration, keeping this application area at the forefront of market demand and technological advancement. |

| By End User |

|

Consumer Electronics OEMs represent the most influential end-user group, characterized by their high-volume procurement and intense focus on miniaturization and power efficiency. Companies like Apple, Samsung, and Sony drive specifications and are deeply involved in co-development with chip suppliers to create proprietary, differentiated sensing solutions. Their demand shapes supply chains and accelerates the commercialization of new perception technologies, such as enhanced time-of-flight (ToF) and structured light systems, creating a highly competitive and innovation-led landscape for chip manufacturers. |

| By Technology |

|

Time of Flight (ToF) technology is emerging as a leading segment due to its balance of performance, scalability, and cost for mid-to-long range applications. ToF chips are gaining significant traction in mobile devices for augmented reality and in automotive applications for driver monitoring and interior sensing because they offer fast data capture and are less susceptible to ambient light interference. The ongoing refinement of ToF sensor resolution and power consumption is expanding its use cases beyond consumer electronics into areas like logistics, robotics, and smart home devices within the AIoT ecosystem. |

| By Integration |

|

System-on-Chip (SoC) Integration is the strategic direction for high-growth applications, particularly in space (PCB area)-constrained devices like smartphones and wearables. Integrating the perception processing core with other system functions (e.g., application processor, neural processing unit) reduces overall device footprint, lowers power consumption, and improves data processing latency. This trend is pushing chip designers and foundries to develop more advanced heterogenous integration techniques and is creating a significant competitive advantage for firms that can offer compact, highly integrated vision processing solutions to OEMs. |

Regional Analysis: Global 3D Visual Perception Chip Market

Asia-Pacific (Leading Region)

Asia-Pacific’s leadership is anchored by its control over semiconductor fabrication and advanced packaging, essential for producing high-performance, cost-effective 3D Visual Perception Chips. The concentration of electronics assembly creates an unparalleled demand-pull for integrated depth-sensing solutions.

The region’s smartphone OEMs are primary adopters, embedding 3D perception chips for facial authentication and augmented reality features. This high-volume application drives continuous chip miniaturization and power optimization, setting global standards for mobile-centric design.

There is a strong strategic push from automotive manufacturers and robotics companies to integrate sophisticated 3D visual perception for autonomous navigation and quality inspection. Regional chip suppliers are developing robust solutions tailored to these challenging operational environments.

National policies promoting AI, Industry 4.0, and semiconductor independence are funneling significant capital into perception chip development. This fosters deep collaboration between academia, research institutes, and commercial entities, accelerating innovation from lab to market.

North America

North America remains a critical innovation hub for 3D Visual Perception Chip market, characterized by its strength in foundational research, advanced algorithm development, and high-value applications. The region is home to leading technology firms and chip designers who pioneer architectures for complex computational photography, LiDAR-based depth mapping, and AI-accelerated scene understanding. Demand is significantly driven by the aerospace, defense, and premium automotive sectors, which require perception chips with exceptional reliability and performance under diverse conditions. The market dynamics here focus on cutting-edge features, low-latency processing for real-time applications, and securing intellectual property, rather than competing solely on cost. Collaborative ecosystems between Silicon Valley tech giants, automotive OEMs, and specialized startups fuel a continuous pipeline of advanced prototypes and niche, high-margin solutions for Global 3D Visual Perception Chip Market.

Europe

The European 3D Visual Perception Chip market is distinguished by its strong emphasis on precision engineering, stringent regulatory standards, and applications within high-end industrial and automotive fields. Automotive OEMs and Tier-1 suppliers, particularly in Germany and France, are integrating sophisticated perception chips to meet rigorous safety requirements for next-generation ADAS and autonomous driving functions. The industrial sector leverages these chips for quality control and robotic guidance in manufacturing, demanding high accuracy and robustness. A notable market dynamic is the collaborative research funded through EU initiatives, pushing innovation in areas like neuromorphic computing for vision and privacy-preserving edge processing. While the volume may trail Asia-Pacific, Europe competes effectively by specializing in premium, safety-critical 3D Visual Perception Chip solutions that command higher value, focusing on data integrity and system-level integration.

South America

3D Visual Perception Chip market in South America is in a developmental phase, with growth primarily driven by targeted industrial modernization and the gradual adoption of automation technologies. Key applications are emerging in agricultural technology, mining automation, and security systems, where 3D sensing can enhance operational efficiency and safety. The market is largely served by international suppliers, with local integration and customization beginning to take root. Challenges include navigating economic volatility and building the necessary technical infrastructure and expertise. However, the region presents a future growth avenue as industries seek to improve productivity through smart technologies, gradually increasing the demand for reliable and cost-optimized visual perception solutions tailored to local industrial needs.

Middle East & Africa

3D Visual Perception Chip market in the Middle East & Africa region is nascent but shows focused potential within specific verticals. In the Middle East, development is spurred by smart city initiatives, security and surveillance infrastructure projects, and investments in logistics automation, particularly around major trade hubs. African markets are seeing early adoption in security applications and pilot projects for agricultural monitoring and mineral exploration. The regional dynamic is defined by a technology import model, with partnerships forming between global chip suppliers and local system integrators. Growth is expected to follow infrastructure development and digital transformation agendas, with 3D Visual Perception Chip Market finding its initial foothold in government-led and large-scale commercial projects that prioritize long-term operational upgrades.

Report Scope

This market research report provides a comprehensive analysis of 3D Visual Perception Chip Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining the current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 3D Visual Perception Chip Market?

-> 3D Visual Perception Chip Market was valued at USD 605 million in 2025 and is projected to reach USD 1414 million by 2034, at a CAGR of 14.6% during the forecast period.

Which key companies operate in 3D Visual Perception Chip Market?

-> Key players include Intel, Microsoft, Sony, Apple, Samsung, Newsight Imaging, Infineon, Orbbec, Inuchip, and Aivatech, among others. In 2025, Global top five players held a significant revenue share.

What are the key growth drivers?

-> Key growth drivers include the increasing demand for depth-sensing capabilities across applications such as biometrics, AIoT, automotive, and consumer electronics, alongside the technological stability and robustness of 3D perception systems in complex environments.

Which region dominates the market?

-> Both North America (with the U.S. as a key market) and Asia (with China as a major growing market) are significant regions, with detailed market estimations provided for each country in the report.

What are the emerging trends?

-> Emerging trends include the integration of various 3D sensing technologies like binocular vision, structured light, LiDAR, and ToF, and the expansion of 3D chips into industrial automation, smart vehicles, and advanced consumer electronics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...