MARKET INSIGHTS

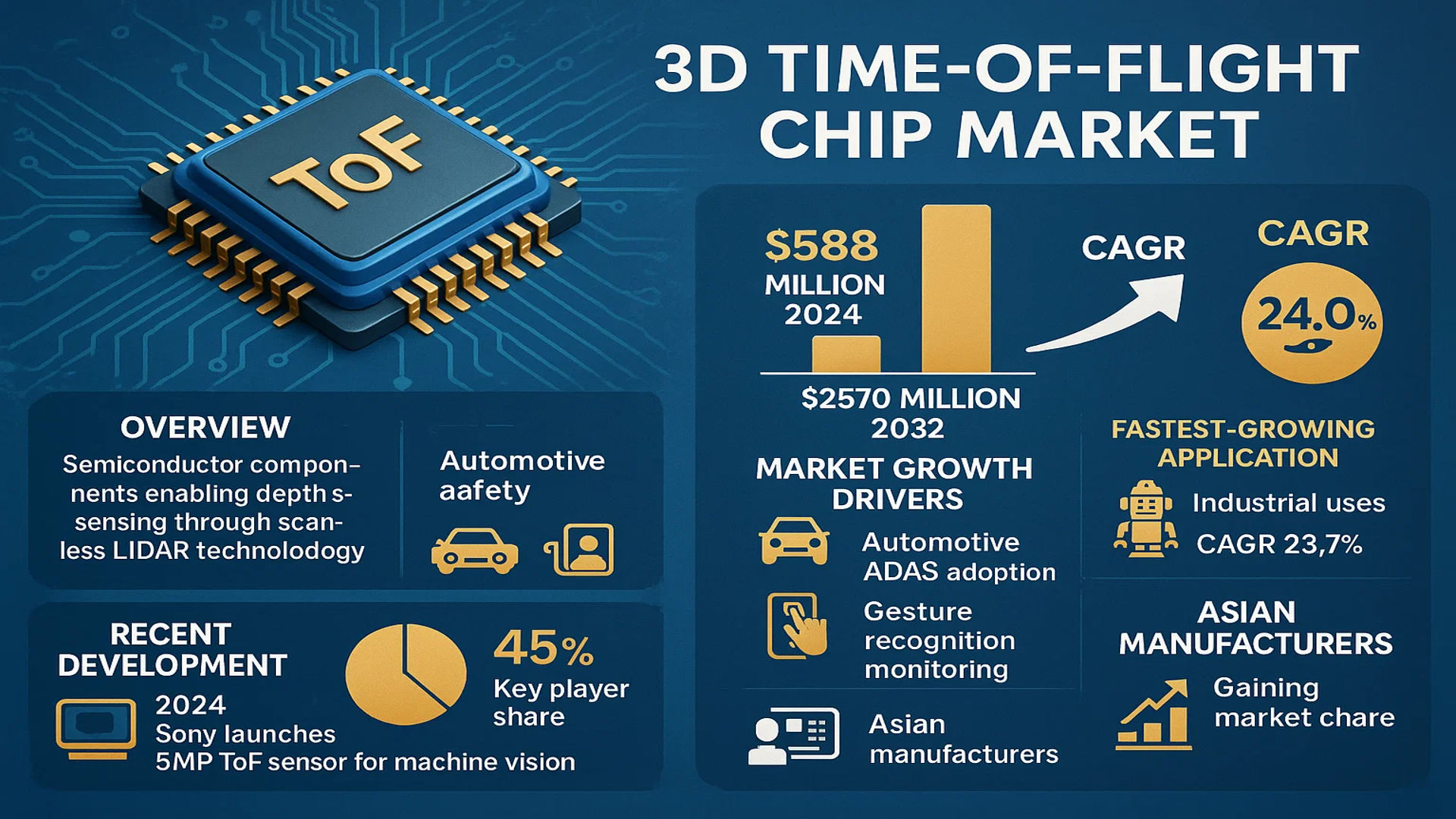

The global 3D Time-of-flight Chip Market was valued at 588 million in 2024 and is projected to reach US$ 2570 million by 2032, at a CAGR of 24.0% during the forecast period.

3D Time-of-flight (ToF) chips are specialized semiconductor components that enable depth sensing through scanner-less LIDAR technology. These chips measure the time taken for infrared light pulses to reflect off objects, generating precise 3D spatial data over short distances. The technology finds applications across industrial automation, automotive safety systems, consumer electronics (particularly in smartphones and AR/VR devices), and robotics.

The market growth is driven by increasing adoption in automotive ADAS (Advanced Driver Assistance Systems), where ToF sensors enable features like gesture recognition and occupant monitoring. While consumer electronics currently dominate applications, industrial uses are growing fastest with a projected 28.7% CAGR through 2030. Recent developments include Sony’s 2024 launch of a 5MP resolution ToF sensor for industrial machine vision, reflecting the technology’s expanding capabilities. Key players like STMicroelectronics and Infineon Technologies collectively hold over 45% market share, with Asian manufacturers rapidly gaining ground through cost-competitive solutions.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of 3D Sensing Applications Accelerates Market Expansion

The surging adoption of 3D time-of-flight (ToF) technology across diverse applications is propelling market growth at an unprecedented rate. Smartphone manufacturers are increasingly integrating ToF sensors for facial recognition, augmented reality (AR) features, and advanced photography applications. Automotive applications, including advanced driver-assistance systems (ADAS) and in-cabin monitoring, are creating substantial demand. The industrial sector’s growing reliance on automation, robotics, and quality control systems is further driving the need for high-precision depth sensing solutions. With the global smartphone market projected to reach 1.5 billion units annually and automotive ADAS adoption crossing 50% in premium vehicles, the addressable market for ToF chips continues to expand significantly.

Advancements in ToF Technology Enhance Market Potential

Technological breakthroughs in ToF chip design and manufacturing are creating new opportunities across industries. Recent developments include improved resolution sensors capable of up to 640×480 pixels, enhanced power efficiency reducing consumption by up to 40%, and better ambient light immunity. These improvements enable more accurate object detection at longer ranges (up to 10 meters) while maintaining compact form factors. Major semiconductor companies are investing heavily in R&D, with some dedicating over 15% of their annual revenue to develop next-generation ToF solutions. The integration of AI-powered depth processing algorithms directly into ToF chips represents another significant advancement, reducing latency and improving real-time performance for critical applications.

MARKET RESTRAINTS

Design Complexity and Integration Challenges Limit Adoption Rate

While ToF technology offers significant advantages, its implementation presents substantial technical hurdles. The precision required for reliable depth measurement demands complex optical systems, specialized packaging, and sophisticated calibration processes. Many OEMs struggle with integrating ToF sensors into existing product architectures due to thermal management requirements and alignment tolerances that can be as precise as 10 micrometers. These technical challenges often lead to extended development cycles, with some automotive applications requiring 3-5 years of validation before commercial deployment. Additionally, the need for specialized manufacturing equipment and clean room facilities creates barriers to entry for new market participants.

Intense Competition from Alternative Technologies Presents Market Challenges

The 3D sensing competitive landscape includes several viable alternatives to ToF technology that restrain market growth. Structured light solutions, stereo vision systems, and ultrasound sensors continue to capture significant market share in certain applications. Structured light technology, while generally more expensive, offers superior accuracy for short-range applications like facial recognition. Similarly, the maturing LiDAR sector presents growing competition for automotive and industrial applications, with some projections suggesting the automotive LiDAR market could reach $7 billion by 2030. This intense competition forces ToF chip manufacturers to continuously innovate while managing cost pressures in an increasingly price-sensitive market.

MARKET OPPORTUNITIES

Emerging Applications in Healthcare and Robotics Offer Untapped Potential

The healthcare sector presents substantial growth opportunities for ToF technology, particularly in patient monitoring, surgical robotics, and medical imaging applications. The global medical robotics market, projected to exceed $20 billion by 2025, increasingly relies on precise depth sensing for minimally invasive procedures. ToF sensors enable touchless interfaces in medical environments, reducing infection risks while improving workflow efficiency. In industrial automation, the expansion of collaborative robots (cobots) and automated guided vehicles (AGVs) creates additional demand for reliable 3D sensing solutions. These emerging applications benefit from ToF’s balance of performance and cost-effectiveness compared to alternative technologies.

Advancements in Computational Imaging Expand Addressable Market

Recent progress in computational photography and computer vision is creating new use cases for ToF technology. The integration of ToF data with neural networks enables advanced scene understanding capabilities for smart cities, retail analytics, and security applications. Some advanced systems now combine multiple ToF sensors with RGB cameras and AI processing to create comprehensive 3D environment models in real-time. These hybrid systems demonstrate accuracy improvements of up to 30% compared to standalone solutions, opening doors for deployment in mission-critical applications. The growing demand for such intelligent sensing solutions across multiple industries suggests continued market expansion for advanced ToF implementations.

MARKET CHALLENGES

Supply Chain Disruptions and Component Shortages Impact Production

The semiconductor industry’s ongoing supply chain challenges significantly affect ToF chip production and availability. Specialized components like VCSEL arrays and high-speed image sensors frequently experience allocation constraints, with lead times extending beyond 52 weeks in some cases. These disruptions stem from both material shortages and capacity limitations at fabrication facilities. The automotive sector, which requires automotive-grade components with stringent reliability standards, faces particular challenges in securing adequate ToF chip supplies. These constraints have led some manufacturers to redesign products or seek alternative suppliers, potentially delaying time-to-market for new applications.

Performance Limitations in Challenging Environments Create Adoption Barriers

ToF technology faces inherent performance limitations that restrict adoption in certain environments. Outdoor applications must contend with varying lighting conditions that can reduce measurement accuracy by up to 25% in bright sunlight. Multiphase interference from multiple ToF systems operating in proximity presents another significant challenge, particularly in industrial settings. Reflective surfaces and transparent materials often cause measurement artifacts that require complex software compensation. These technical challenges necessitate ongoing investment in algorithm development and sensor improvements to expand the viable application space for ToF solutions.

3D TIME-OF-FLIGHT CHIP MARKET TRENDS

Expanding Applications in Consumer Electronics Driving Market Growth

The 3D Time-of-Flight (ToF) chip market is experiencing significant traction due to its expanding applications in consumer electronics, particularly smartphones, AR/VR devices, and gaming consoles. With smartphone manufacturers integrating advanced depth-sensing capabilities for facial recognition and enhanced photography, the demand for high-precision ToF sensors has surged by over 35% year-over-year since 2020. Major technology players are increasingly adopting ToF chips to enable gesture recognition, 3D mapping, and augmented reality experiences, creating a sustained growth path for the industry.

Automotive Sector Emerges as a High-Growth Vertical

While consumer electronics dominate current adoption, the automotive sector is emerging as the next major growth driver for 3D ToF technology. Advanced driver-assistance systems (ADAS) and autonomous vehicles require highly accurate depth perception for collision avoidance, parking assistance, and cabin monitoring. The global automotive LiDAR market, where ToF plays a crucial role, is projected to exceed $8 billion by 2030, with passenger vehicles accounting for nearly 60% of this demand. This shift toward smart mobility solutions is accelerating R&D investments in more robust and compact ToF sensor designs.

Other Notable Trends

Industrial Automation Adoption

The increasing automation across manufacturing and logistics sectors is fueling demand for ToF-based machine vision systems. These chips enable precise object detection, quality control, and robotic navigation in industrial environments. Warehouse automation alone accounts for nearly 25% of industrial ToF sensor deployments, with growing applications in inventory management and autonomous material handling. As factories embrace Industry 4.0 principles, the need for real-time 3D spatial awareness will continue driving technological advancements in this space.

Miniaturization and Power Efficiency Innovations

Recent breakthroughs in semiconductor fabrication have enabled the development of smaller, more power-efficient ToF chips without compromising performance. Next-generation sensors now achieve sub-millimeter accuracy while consuming up to 40% less power compared to previous iterations. This progress is critical for battery-operated devices and has opened new possibilities in wearable tech and IoT applications. Leading manufacturers are focusing on system-on-chip (SoC) integrations to further reduce form factors and production costs.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Giants and Innovators Drive Market Expansion with Advanced 3D ToF Solutions

The global 3D Time-of-Flight (ToF) chip market exhibits a dynamic competitive environment with established semiconductor leaders and emerging innovators shaping industry growth. With the market projected to grow at a 24.0% CAGR through 2032, companies are aggressively expanding their portfolios to capitalize on surging demand across automotive, industrial, and consumer applications.

STMicroelectronics and Infineon Technologies currently dominate the market, collectively holding over 32% revenue share in 2024. Their leadership stems from vertically integrated manufacturing capabilities and strategic partnerships with major smartphone and automotive OEMs. STMicroelectronics notably secured design wins in Apple’s Face ID system and automotive cabin monitoring solutions.

Meanwhile, Texas Instruments and Sony continue to gain traction through technological differentiation. Texas Instruments’ indirect ToF solutions achieve industry-leading accuracy (<0.1% error margin), while Sony leverages its image sensor expertise for high-resolution depth mapping. Both companies are investing heavily in automotive LiDAR applications, poised to become a $1.7 billion market by 2027.

The competitive landscape also features disruptive innovators like Espros Photonics and AMS, specializing in miniaturized ToF chips for IoT devices. Their ultra-low-power designs (<10mW consumption) are gaining adoption in wearables and smart home products. Recent industry developments include:

- AMS’ acquisition of Princeton Optronics to enhance VCSEL technology

- Renesas’ collaboration with Microsoft for Azure Depth Platform integration

- Panasonic’s 10μm pixel pitch ToF sensor for industrial automation

List of Key 3D Time-of-Flight Chip Companies

- STMicroelectronics (Switzerland)

- Infineon Technologies (Germany)

- Texas Instruments (U.S.)

- Sony Semiconductor (Japan)

- Melexis (Belgium)

- Espros Photonics (Switzerland)

- Renesas Electronics (Japan)

- Panasonic (Japan)

- ams-OSRAM AG (Austria)

Segment Analysis:

By Type

Direct ToF Segment Dominates the Market Due to Higher Accuracy in Depth Sensing Applications

The market is segmented based on type into:

- Direct ToF

- Indirect ToF

By Application

Consumer Electronics Segment Leads Due to Rising Adoption of 3D Sensing in Smartphones and AR/VR Devices

The market is segmented based on application into:

- Industrial

- Automotive

- Consumer Electronics

- Healthcare

- Others

By End-User

Consumer Electronics Manufacturers Dominate Due to Mass Adoption in Mobile Devices

The market is segmented based on end-user into:

- Consumer Electronics Manufacturers

- Automotive OEMs

- Industrial Equipment Manufacturers

- Medical Device Companies

- Others

Regional Analysis: 3D Time-of-Flight Chip Market

Asia-Pacific

With a 38.2% revenue share in 2024, Asia-Pacific dominates the 3D ToF chip market, driven by China’s massive electronics manufacturing sector and Japan’s leadership in semiconductor innovation. The region’s consumer electronics boom, particularly in smartphone 3D sensing applications, accounts for 62% of regional demand. Though facing a 2% semiconductor market decline in 2022, governments are investing heavily in domestic chip production – China allocated $140 billion to semiconductor self-sufficiency programs. Automotive ADAS adoption in South Korea and industrial automation growth in Southeast Asia present significant opportunities. Cost competition remains intense, with local manufacturers like OmniVision gaining ground against global players.

North America

The U.S. accounts for 72% of North America’s 3D ToF market, fueled by defense applications and Silicon Valley’s tech ecosystem. With 17% YoY semiconductor sales growth in 2022, the region leads in R&D for advanced driver assistance systems (ADAS) and industrial robotics. The CHIPS Act’s $52 billion funding is accelerating domestic production capabilities. Key challenges include strict ITAR regulations limiting technology exports and high manufacturing costs. Major players like Texas Instruments and ON Semiconductor are focusing on high-margin industrial and medical applications to differentiate from Asian mass-market suppliers.

Europe

Europe’s 12.6% semiconductor market growth in 2022 reflects strong demand for automotive-grade 3D ToF solutions, particularly from German automakers implementing EU-mandated safety systems. The region specializes in high-precision industrial applications, holding 28% of the global market for manufacturing automation ToF sensors. Strict GDPR regulations influence data processing architectures in consumer devices. STMicroelectronics leads with differentiated indirect ToF solutions, while smaller firms like Melexis dominate niche automotive markets. The EU Chips Act aims to double Europe’s semiconductor market share to 20% by 2030 through €43 billion in investments.

Middle East & Africa

This emerging market shows 19% CAGR potential through 2030, driven by smart city initiatives in UAE and Saudi Arabia. The $500 billion NEOM project incorporates ToF sensors across infrastructure. Challenges include limited local technical expertise and reliance on imports. Israel’s startup ecosystem is developing specialized security and agricultural ToF applications. While currently representing just 4% of global demand, the region’s willingness to adopt cutting-edge technologies positions it for long-term growth as infrastructure matures.

South America

Brazil accounts for 61% of regional 3D ToF demand, primarily for industrial automation in mining and agriculture. Economic volatility has constrained growth, with the semiconductor market growing just 3.8% in 2022. Local assembly of consumer electronics in Mexico is creating downstream demand. The lack of local semiconductor fabrication limits technological sophistication, but also creates opportunities for cost-optimized solutions. Automotive adoption lags other regions due to weaker safety regulations, though Mercosur trade agreements are gradually raising standards.

Report Scope

This market research report provides a comprehensive analysis of the global and regional 3D Time-of-flight Chip markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global 3D Time-of-flight Chip market was valued at USD 588 million in 2024 and is projected to reach USD 2570 million by 2032, growing at a CAGR of 24.0% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (Direct ToF, Indirect ToF), application (Industrial, Automotive, Consumer, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific dominates the market with over 40% revenue share in 2024.

- Competitive Landscape: Profiles of leading market participants including Melexis, STMicroelectronics, Infineon Technologies, Sony, and Texas Instruments, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT in 3D sensing applications, semiconductor design trends, fabrication techniques, and evolving industry standards in ToF technology.

- Market Drivers & Restraints: Evaluation of factors driving market growth (increasing demand for 3D sensing in smartphones, AR/VR applications, automotive ADAS) along with challenges (high development costs, supply chain constraints, and technical limitations in outdoor environments).

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in the 3D sensing market.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global 3D Time-of-flight Chip Market?

-> 3D Time-of-flight Chip Market was valued at 588 million in 2024 and is projected to reach US$ 2570 million by 2032, at a CAGR of 24.0% during the forecast period.

Which key companies operate in Global 3D Time-of-flight Chip Market?

-> Key players include Melexis, STMicroelectronics, Infineon Technologies, Sony, Texas Instruments, Renesas, and Panasonic, among others.

What are the key growth drivers?

-> Key growth drivers include increasing adoption in smartphones, demand for AR/VR applications, automotive ADAS systems, and industrial automation solutions.

Which region dominates the market?

-> Asia-Pacific is the dominant market with over 40% revenue share in 2024, driven by strong electronics manufacturing in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include miniaturization of ToF sensors, integration with AI for enhanced depth perception, and development of low-power consumption chips for IoT applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...