MARKET INSIGHTS

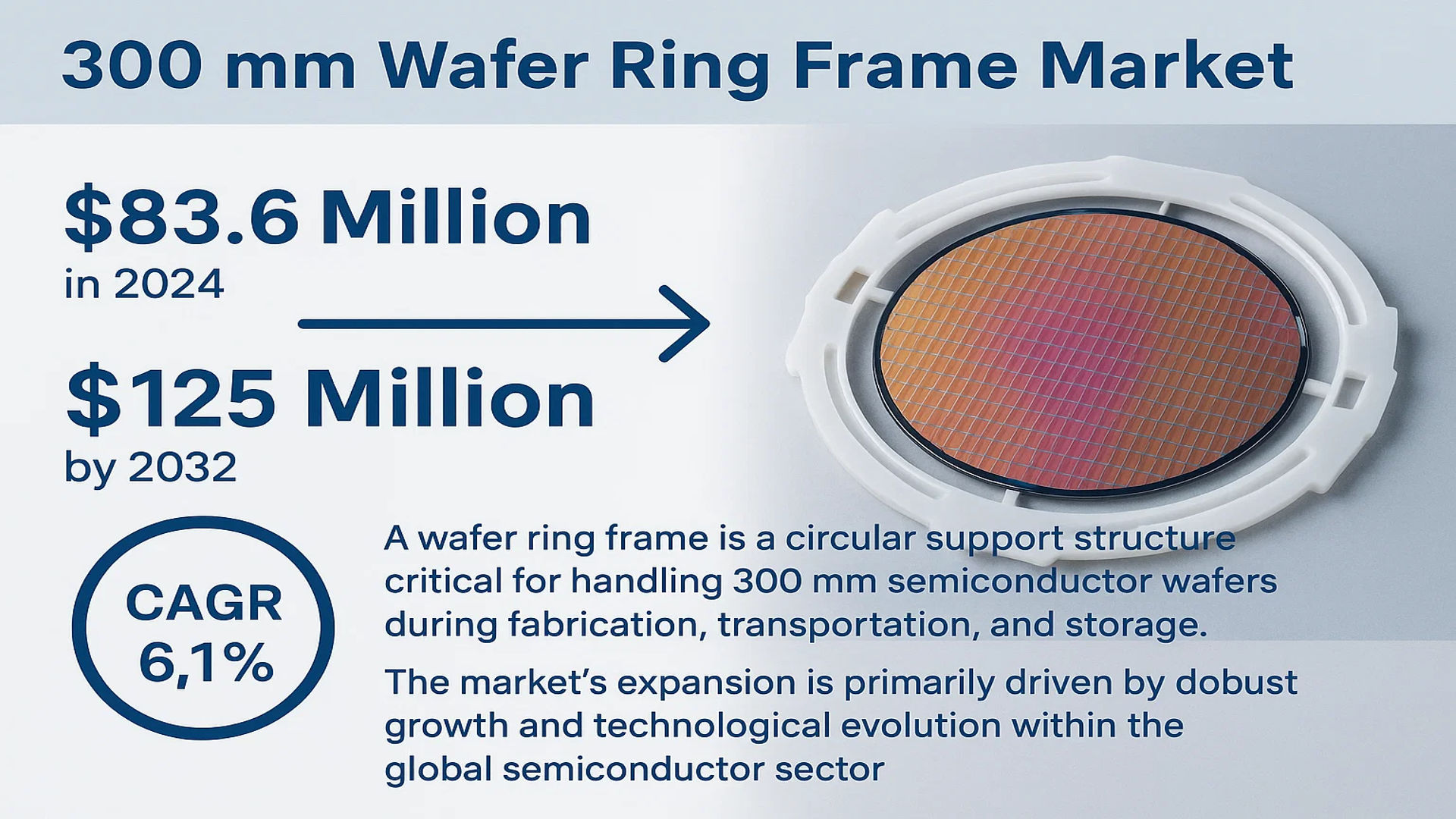

The global 300 mm Wafer Ring Frame Market was valued at 83.6 million in 2024 and is projected to reach US$ 125 million by 2032, at a CAGR of 6.1% during the forecast period.

A wafer ring frame is a circular support structure critical for handling 300 mm semiconductor wafers during fabrication, transportation, and storage. These frames are engineered to securely hold wafers while minimizing risks of contamination, damage, or deformation. They are manufactured from materials compatible with stringent cleanroom environments and are designed with features that facilitate easy loading and unloading of wafers, ensuring process integrity.

The market’s expansion is primarily driven by the robust growth and technological evolution within the global semiconductor sector. Surging demand for semiconductor devices, fueled by advancements in 5G communication, IoT, AI, and electric vehicles, has increased the need for high-performance, reliable wafers. This, in turn, necessitates continuous upgrades in wafer manufacturing processes and places higher demands on support tools like ring frames. For instance, advanced process nodes such as 7nm and 5nm require more precise and stable frames to ensure accuracy in critical processes like lithography and etching. Furthermore, stringent environmental regulations are pushing manufacturers towards developing greener, recyclable materials, reducing the carbon footprint of production. Key players operating in this market include DISCO, Shin-Etsu Polymer, Entegris, Dou Yee, and ePAK, who provide a wide range of specialized solutions.

MARKET DYNAMICS

MARKET DRIVERS

Semiconductor Industry Expansion and Advanced Node Manufacturing to Drive Market Growth

The global semiconductor industry’s robust expansion serves as the primary catalyst for the 300 mm wafer ring frame market. With semiconductor demand projected to grow at approximately 6-8% annually through 2030, manufacturers are scaling production capacity significantly. This growth is particularly driven by emerging technologies including 5G infrastructure, artificial intelligence systems, and electric vehicles, all requiring advanced semiconductor components. The transition to smaller process nodes below 7nm necessitates exceptionally stable wafer handling solutions, creating substantial demand for precision ring frames that can maintain wafer integrity during complex fabrication processes. Additionally, the increasing adoption of 300 mm wafers in new fabrication facilities worldwide further accelerates market growth, as these larger wafers provide better economies of scale for high-volume semiconductor production.

Automation and Smart Manufacturing Trends to Boost Market Adoption

The semiconductor industry’s rapid shift toward fully automated manufacturing environments is driving significant demand for compatible wafer handling solutions. Modern fabrication facilities require ring frames that integrate seamlessly with automated material handling systems, robotic arms, and intelligent transport mechanisms. This trend toward Industry 4.0 implementation in semiconductor manufacturing has created a pressing need for ring frames with standardized interfaces, improved durability, and enhanced compatibility with sensor-based monitoring systems. The growing emphasis on yield optimization and defect reduction further reinforces the importance of reliable wafer support systems that minimize particle generation and ensure consistent performance across thousands of production cycles.

Furthermore, increasing investments in semiconductor manufacturing capacity across key regions are expected to fuel market growth. Major semiconductor-producing countries have announced substantial expansion plans, with projected capital expenditures exceeding $500 billion globally over the next five years. These investments specifically target 300 mm wafer production capabilities, creating parallel demand for auxiliary equipment including high-performance ring frames.

➤ For instance, recent industry data indicates that over 70% of new semiconductor fabrication facilities under construction worldwide are designed for 300 mm wafer processing, creating sustained demand for compatible ring frame solutions.

Moreover, the continuous development of new semiconductor applications in areas such as quantum computing, advanced sensors, and heterogeneous integration is anticipated to drive additional growth in the wafer ring frame market throughout the forecast period.

MARKET CHALLENGES

High Precision Manufacturing Requirements and Quality Control Challenges to Constrain Market Growth

The manufacturing of 300 mm wafer ring frames faces significant technical challenges due to extremely stringent precision requirements. These components must maintain dimensional stability within micron-level tolerances while withstanding repeated thermal cycles and mechanical stresses during semiconductor processing. The specialized materials and advanced manufacturing techniques required to achieve these specifications result in substantial production complexities and higher manufacturing costs. Additionally, maintaining consistent quality across large production volumes presents ongoing challenges, as even minor variations can lead to wafer damage or processing defects that impact overall yield rates in semiconductor fabrication.

Other Challenges

Material Compatibility and Contamination Risks

Ensuring material compatibility with cleanroom environments remains a persistent challenge for ring frame manufacturers. The materials used must exhibit minimal outgassing, resist chemical exposure from processing chemicals, and maintain dimensional stability across varying temperature conditions. Any material degradation or particle generation can compromise wafer quality and lead to substantial production losses, making material selection and validation processes critically important yet challenging aspects of ring frame manufacturing.

Supply Chain Complexity and Geopolitical Factors

The global nature of semiconductor manufacturing creates supply chain vulnerabilities that impact ring frame availability and pricing. Recent geopolitical tensions and trade restrictions have introduced additional complexities in sourcing specialized materials and components required for high-quality ring frame production. These factors can lead to supply disruptions, extended lead times, and increased costs that ultimately affect the entire semiconductor manufacturing ecosystem.

MARKET RESTRAINTS

Cost Sensitivity and Price Pressure from Semiconductor Manufacturers to Limit Market Expansion

The 300 mm wafer ring frame market faces significant restraint from ongoing cost pressure within the semiconductor industry. As semiconductor manufacturers continuously seek to reduce production costs, auxiliary equipment suppliers including ring frame manufacturers experience persistent pressure to lower prices while maintaining or improving product quality. This cost sensitivity is particularly pronounced in highly competitive semiconductor segments where profit margins are increasingly constrained. The requirement for frequent ring frame replacement due to wear and tear further amplifies cost concerns among semiconductor manufacturers, leading to extended evaluation periods and rigorous cost-benefit analyses before adopting new ring frame solutions.

Additionally, the capital-intensive nature of ring frame manufacturing creates barriers to market entry and expansion. Establishing production facilities capable of meeting the stringent quality requirements necessitates substantial investment in specialized equipment, cleanroom infrastructure, and quality control systems. These high capital requirements limit the ability of smaller manufacturers to compete effectively, thereby restraining overall market growth and innovation.

Furthermore, the cyclical nature of the semiconductor industry introduces demand volatility that complicates production planning and inventory management for ring frame manufacturers. During industry downturns, semiconductor manufacturers typically extend equipment usage periods and delay replacement purchases, creating unpredictable demand patterns that challenge ring frame suppliers’ operational stability and growth prospects.

MARKET OPPORTUNITIES

Emerging Material Technologies and Sustainability Initiatives to Create New Growth Avenues

The development of advanced composite materials and sustainable manufacturing practices presents significant growth opportunities for the 300 mm wafer ring frame market. Recent advancements in material science have enabled the creation of new polymer composites and metal alloys that offer improved durability, reduced particle generation, and enhanced thermal stability. These material innovations allow ring frame manufacturers to develop products with extended service life and improved performance characteristics, creating opportunities for premium product segments and replacement market growth.

Additionally, the increasing focus on sustainability within the semiconductor industry is driving demand for recyclable and environmentally friendly ring frame solutions. Manufacturers that develop closed-loop recycling programs and implement sustainable production processes are positioned to capture market share as semiconductor companies increasingly prioritize environmental responsibility in their supply chain decisions. This trend toward green manufacturing creates opportunities for innovative ring frame designs that reduce material usage while maintaining performance standards.

Moreover, the integration of smart technologies and IoT capabilities into ring frames offers substantial growth potential. The development of ring frames with embedded sensors for real-time monitoring of wear, contamination levels, and structural integrity enables predictive maintenance strategies that can reduce unplanned downtime in semiconductor fabrication facilities. These smart ring frame solutions represent an emerging product category with significant revenue potential as semiconductor manufacturers seek to optimize operational efficiency through advanced equipment monitoring capabilities.

300 MM WAFER RING FRAME MARKET TRENDS

Advanced Semiconductor Process Nodes Driving Demand for High-Precision Ring Frames

The relentless progression towards more advanced semiconductor process nodes, particularly those at 5nm and below, is a primary catalyst for innovation and demand in the 300 mm wafer ring frame market. These sophisticated manufacturing processes require exceptional stability and precision during lithography, etching, and deposition steps, where even nanometer-scale vibrations or thermal distortions can compromise yield. Consequently, ring frame manufacturers are engineering solutions with enhanced mechanical rigidity and superior thermal management properties. The market is responding to the need for frames that can maintain dimensional integrity under extreme process conditions, with an estimated over 40% of new frame designs now specifically tailored for sub-7nm fabrication facilities. This trend is inextricably linked to the broader expansion of the semiconductor industry, which is projected to require a significant increase in wafer starts per month to meet global chip demand.

Other Trends

Material Innovation and Sustainability

While performance is paramount, increasingly stringent environmental regulations are pushing the industry towards greener material solutions. There is a growing shift away from traditional plastics and metals towards the development and adoption of high-performance composite materials and recyclable polymers. These advanced materials not only reduce the carbon footprint associated with production but also offer superior chemical resistance needed to withstand harsh cleaning processes involving solvents and acids. This dual focus on sustainability and performance is creating new market segments, with an observable increase in R&D investment aimed at creating frames that meet both technical specifications and environmental, social, and governance (ESG) criteria set by major semiconductor foundries.

Integration with Industry 4.0 and Automated Material Handling Systems

The transition towards fully automated 300mm fabs is compelling a redesign of wafer ring frames for better integration with automated material handling systems (AMHS) and robotics. Modern frames are being equipped with features such as standardized notches, RFID tags, and enhanced gripping surfaces to ensure seamless and reliable robotic handling, which minimizes human intervention and the associated risk of contamination. This drive for automation compatibility is crucial for improving overall equipment effectiveness (OEE) and reducing cycle times. Furthermore, the integration of IoT sensors into frame designs is an emerging trend, enabling real-time monitoring of parameters like frame stress and temperature during transport and processing, which facilitates predictive maintenance and enhances yield management protocols.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Material Innovation and Precision Engineering to Maintain Competitive Edge

The global 300 mm wafer ring frame market exhibits a semi-consolidated structure, featuring a mix of established multinational corporations and specialized regional manufacturers. DISCO Corporation emerges as a dominant player, leveraging its extensive expertise in precision cutting and grinding equipment to develop highly reliable wafer ring frames. Their strong foothold in key semiconductor manufacturing regions like Japan, Taiwan, and South Korea provides them with significant market advantage.

Shin-Etsu Polymer and Entegris also command substantial market shares, primarily due to their advanced material science capabilities and contamination-control technologies. Shin-Etsu’s development of high-purity plastic compounds and Entegris’ focus on critical handling solutions align perfectly with the industry’s need for ultra-clean manufacturing environments. These companies have demonstrated consistent growth through strategic partnerships with major semiconductor fabrication plants.

Market participants are actively pursuing geographic expansion and product diversification strategies. Several leading companies have recently established production facilities in Southeast Asia to better serve the growing semiconductor manufacturing cluster in that region. Furthermore, continuous investment in R&D has led to the introduction of frames with enhanced thermal stability and improved compatibility with automated handling systems.

Meanwhile, specialized manufacturers like Dou Yee Enterprises and YJ Stainless are strengthening their positions through focused technological innovations and cost-effective manufacturing processes. These companies have developed frames with superior mechanical strength and corrosion resistance, addressing the specific requirements of advanced semiconductor manufacturing nodes.

List of Key 300 mm Wafer Ring Frame Companies Profiled

- DISCO Corporation (Japan)

- Shin-Etsu Polymer Co., Ltd. (Japan)

- Entegris, Inc. (U.S.)

- Dou Yee Enterprises (Singapore)

- YJ Stainless Co., Ltd. (Taiwan)

- Long-Tech Precision Machinery Co., Ltd. (Taiwan)

- Chung King Enterprise Co., Ltd. (Taiwan)

- Shenzhen Dong Hong Xin Industrial Co., Ltd. (China)

- ePAK International Ltd. (China)

- Silicon Connection Corporation (U.S.)

- Wonkang Technics Co., Ltd. (South Korea)

- Grand Tech Innovation Corporation (Taiwan)

Segment Analysis:

By Material Type

Metal Material Segment Dominates the Market Due to Superior Mechanical Strength and Thermal Stability

The market is segmented based on material type into:

- Metal Material

- Subtypes: Stainless Steel, Aluminum Alloy, and others

- Plastic Material

- Subtypes: High-performance engineering plastics, PEEK, and others

By Application

Wafer Suppliers Segment Leads Due to Critical Role in High-Volume Semiconductor Manufacturing

The market is segmented based on application into:

- Equipment Suppliers

- Wafer Suppliers

By End-User Industry

Consumer Electronics Segment Leads Driven by High Demand for Advanced Semiconductor Components

The market is segmented based on end-user industry into:

- Consumer Electronics

- Automotive

- Industrial Manufacturing

- Telecommunications

- Others

By Technology Node

Advanced Nodes Segment (7nm and Below) Demonstrates Strong Growth Due to Increasing Complexity in Semiconductor Fabrication

The market is segmented based on technology node into:

- Mature Nodes (>28nm)

- Intermediate Nodes (28nm-10nm)

- Advanced Nodes (7nm and below)

Regional Analysis: 300 mm Wafer Ring Frame Market

Asia-Pacific

The Asia-Pacific region dominates the global 300 mm Wafer Ring Frame market, accounting for over 65% of global consumption volume. This leadership position is driven by the concentration of semiconductor manufacturing giants and massive fab investments in Taiwan, South Korea, China, and Japan. Major foundries like TSMC, Samsung, and SMIC are continuously expanding their 300 mm wafer production capacities to meet the insatiable demand for advanced chips used in AI, 5G, and automotive applications. This creates a robust and consistent demand for high-precision ring frames. The region is also a hub for key manufacturers like Shin-Etsu Polymer and DISCO, ensuring a strong supply chain. While cost-competitive plastic frames see significant usage, there is a marked shift towards advanced metal and composite frames to support the transition to sub-7nm process nodes, which require exceptional dimensional stability and thermal performance.

North America

North America is a significant market characterized by high-value, technologically advanced demand. The presence of leading semiconductor equipment suppliers and IDMs (Integrated Device Manufacturers) like Intel and GlobalFoundries fuels the need for premium, high-reliability ring frames. The market is heavily influenced by stringent quality control standards and a focus on innovation to support cutting-edge R&D in areas like quantum computing and advanced packaging. Environmental sustainability is becoming a key purchasing criterion, prompting suppliers to develop recyclable and longer-lasting frame solutions. While the volume may be lower than Asia-Pacific, the demand for frames compatible with fully automated fabs and capable of handling ultra-thin wafers for 3D integration makes it a high-margin, innovation-driven region.

Europe

Europe’s market is defined by its strong automotive and industrial semiconductor sectors. The region’s demand for 300 mm wafer ring frames is closely tied to the production of power semiconductors, sensors, and microcontrollers for the automotive industry, which is undergoing a massive transformation towards electrification and autonomy. This necessitates frames that offer high mechanical strength and reliability for thicker wafers often used in these applications. EU regulations promoting a circular economy are pushing manufacturers towards more durable and recyclable frame materials. The presence of specialized semiconductor clusters in Germany, France, and the Benelux countries supports a steady demand, though growth is more measured compared to the explosive expansion seen in Asia.

South America

The market in South America is nascent and volume-limited. The region lacks major semiconductor fabrication facilities, resulting in demand being primarily driven by a small number of assembly and test operations, research institutions, and maintenance needs for imported equipment. The market is highly cost-sensitive, with a strong preference for standard plastic frames over advanced metal variants. Economic volatility and a lack of significant local government investment in semiconductor infrastructure are the primary factors hindering market development. Growth is expected to remain incremental, tied to the broader expansion of the regional electronics manufacturing sector rather than leading-edge semiconductor production.

Middle East & Africa

This region represents an emerging and opportunistic market with currently minimal consumption. Any demand is almost entirely import-dependent and is generated by a handful of technology parks and universities engaging in small-scale research and development activities. Countries like Israel, with its strong tech sector, show the most potential for future growth. However, the absence of a local semiconductor manufacturing base and significant infrastructure investments means the market is not a priority for major global frame suppliers. Demand is sporadic and focused on basic, off-the-shelf products for prototyping and educational purposes, with long-term growth contingent on successful economic diversification strategies into high-tech industries.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Semiconductor and Electronics markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global 300 mm Wafer Ring Frame Market?

-> 300 mm Wafer Ring Frame Market was valued at 83.6 million in 2024 and is projected to reach US$ 125 million by 2032, at a CAGR of 6.1% during the forecast period.

Which key companies operate in Global 300 mm Wafer Ring Frame Market?

-> Key players include Shin-Etsu Polymer, DISCO, Entegris, Dou Yee, YJ Stainless, Long-Tech Precision Machinery, ePAK, and Silicon Connection, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for semiconductor devices in 5G, IoT, AI, and electric vehicles, advancements in process nodes (7nm, 5nm and below), and increasing automation in semiconductor manufacturing.

Which region dominates the market?

-> Asia-Pacific is the dominant and fastest-growing region, driven by major semiconductor manufacturing hubs in Taiwan, South Korea, China, and Japan.

What are the emerging trends?

-> Emerging trends include development of recyclable materials, integration of IoT for predictive maintenance, adoption of high-strength composite materials, and compatibility with ultra-thin wafer processing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...