MARKET INSIGHTS

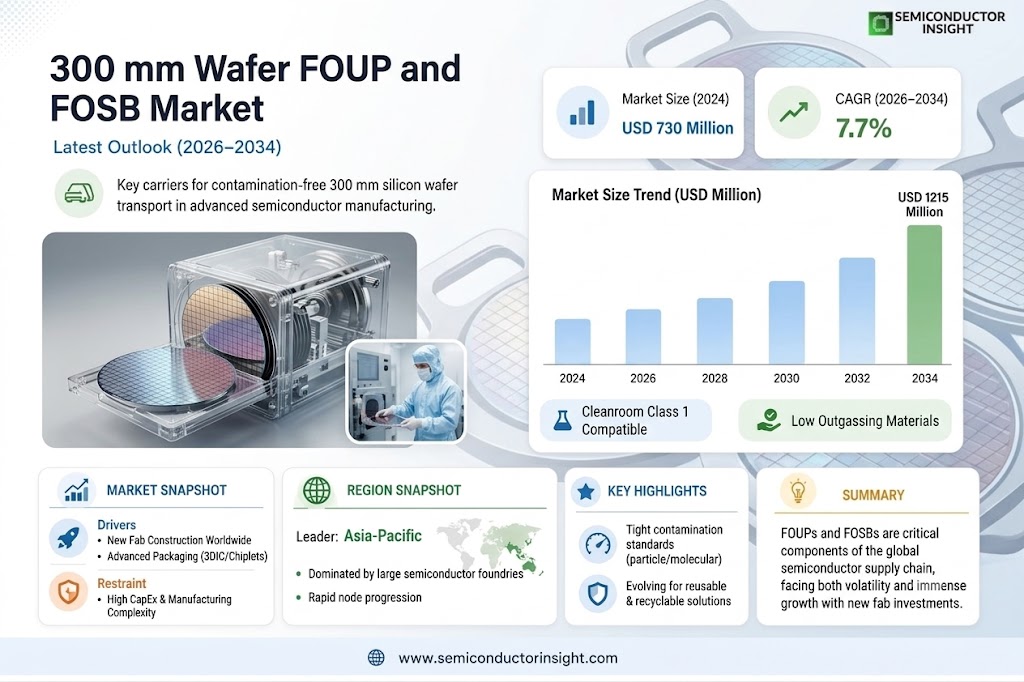

The global 300 mm Wafer FOUP and FOSB Market was valued at 730 million in 2024 and is projected to reach US$ 1215 million by 2032, at a CAGR of 7.7% during the forecast period.

Front Opening Unified Pods (FOUPs) and Front Opening Shipping Boxes (FOSBs) are specialized containers critical for handling 300 mm silicon wafers in semiconductor manufacturing. FOUPs enable robotic wafer handling in cleanroom environments while protecting against contamination, featuring RFID tracking and automated docking systems. FOSBs provide additional shock absorption for inter-facility wafer transportation, utilizing cushioning materials to prevent breakage during transit.

Market growth is driven by expanding semiconductor production capacities, particularly in Taiwan (19.74% market share in 2022) and the US (19.30%). However, high capital requirements create barriers for new entrants, concentrating the market among established players like Entegris and Shin-Etsu Polymer. The increasing shift towards larger 300 mm wafer sizes in foundries and IDMs continues to fuel demand, though pricing pressures and gross margin fluctuations present ongoing challenges for manufacturers.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Semiconductor Manufacturing to Boost Demand for 300 mm Wafer Carriers

The global semiconductor industry is experiencing unprecedented growth, with 300 mm wafers becoming the standard for advanced chip manufacturing. This expansion is directly driving demand for high-performance wafer carriers like FOUPs and FOSBs. As semiconductor fabrication plants (fabs) continue to ramp up production capacities, the need for reliable wafer storage and transportation solutions has become critical. The transition to more advanced process nodes (below 7nm) particularly increases the requirement for contamination-free handling, where FOUPs play a vital role. Recent capacity expansions in major semiconductor hubs like Taiwan, South Korea, and the United States are expected to maintain steady demand growth through at least 2030.

Increasing Automation in Cleanroom Environments Accelerates Market Adoption

Modern semiconductor fabrication facilities are increasingly adopting fully automated material handling systems (AMHS) to improve yield and production efficiency. FOUPs, with their standardized interfaces and robotic compatibility, are essential components of these automated environments. The integration of smart features like RFID tracking and environmental sensors in advanced FOUP designs allows for real-time wafer monitoring throughout the manufacturing process. This trend toward Industry 4.0 in semiconductor manufacturing is creating demand for next-generation wafer carriers with enhanced connectivity and data capabilities. The percentage of fabs using fully automated wafer handling has grown from 35% in 2015 to over 65% in 2024, driving continued FOUP market growth.

Technological Advancements in Wafer Carrier Design Fuel Market Expansion

Leading manufacturers are continually innovating FOUP designs to meet the evolving needs of chipmakers. Recent developments include anti-static materials to prevent particle generation, improved sealing mechanisms for better contamination control, and lightweight composites that reduce AMHS load. These technological improvements not only extend equipment lifespan but also help semiconductor manufacturers maintain high yields in advanced manufacturing processes. The introduction of specialized coatings that minimize outgassing has been particularly important for EUV lithography applications, where even minimal contamination can significantly impact production quality.

MARKET RESTRAINTS

High Capital Requirements and Manufacturing Complexity Limit Market Entry

The 300 mm wafer carrier market faces significant barriers to entry due to the specialized manufacturing processes and stringent quality requirements. Producing FOUPs and FOSBs that meet semiconductor industry standards requires substantial investment in cleanroom facilities, precision molding equipment, and advanced material processing technologies. The typical capital expenditure for a new production line can exceed $50 million, making it difficult for new players to enter the market. Furthermore, the lengthy qualification process required by semiconductor manufacturers (often 12-18 months) creates additional financial burdens for potential competitors.

Fluctuating Semiconductor Demand Cycles Create Market Volatility

The wafer carrier market is intrinsically tied to the cyclical nature of the semiconductor industry. During periods of reduced chip demand, semiconductor manufacturers often delay facility expansions and reduce equipment purchases, directly impacting FOUP and FOSB sales. The market experienced this volatility notably during 2022-2023, when inventory corrections in the memory sector led to temporary reductions in wafer carrier orders. Such cyclical patterns make long-term production planning challenging for wafer carrier manufacturers and can lead to periods of over- or under-capacity in the supply chain.

Stringent Quality and Contamination Standards Increase Production Costs

As semiconductor manufacturing processes become more advanced, the contamination requirements for wafer carriers become increasingly strict. Current specifications for particle counts and outgassing in FOUPs used for leading-edge nodes are up to 100 times more stringent than those for mature nodes. Meeting these requirements necessitates advanced materials and production processes that significantly increase manufacturing costs. Additionally, the need for frequent requalification and recertification of carrier components creates ongoing operational expenses that impact profit margins across the industry.

MARKET OPPORTUNITIES

Emerging Markets and New Fab Construction Present Growth Potential

The current wave of new semiconductor fabrication plant construction worldwide, particularly in the United States, Europe, and Southeast Asia, creates significant opportunities for wafer carrier manufacturers. Government initiatives supporting domestic semiconductor production, such as the CHIPS Act in the U.S. and similar programs in Europe, are driving over $200 billion in new fab investments through 2030. Many of these new facilities will require complete supply chains for wafer handling solutions, presenting a substantial market opportunity for both FOUP and FOSB suppliers.

Advanced Packaging Technologies Drive Need for Specialized Carriers

The growing adoption of advanced packaging approaches like 3DIC and chiplet architectures is creating demand for specialized wafer carriers. These packaging technologies often require handling thinned wafers or reconstituted wafers, which standard FOUPs cannot accommodate safely. Manufacturers that develop carriers specifically for these applications can capture value in this rapidly growing segment of the semiconductor market. The advanced packaging equipment market is projected to grow at over 12% CAGR through 2030, suggesting strong potential for associated wafer handling solutions.

Sustainability Initiatives Open Door for Innovative Material Solutions

Increasing focus on sustainability in semiconductor manufacturing presents opportunities for wafer carrier innovation. There is growing interest in developing reusable, recyclable, or biodegradable carrier components that maintain performance while reducing environmental impact. Companies that can successfully commercialize such solutions may gain competitive advantage as sustainability requirements become more stringent. The emphasis on circular economy principles in the semiconductor supply chain is particularly strong in Europe and among leading multinational chip manufacturers.

MARKET CHALLENGES

Intense Competition and Price Pressure from Established Players

The 300 mm wafer carrier market is dominated by a small number of well-established suppliers with strong customer relationships and extensive intellectual property portfolios. This creates significant challenges for new entrants trying to gain market share. Price competition has intensified as semiconductor manufacturers seek to reduce costs, putting pressure on wafer carrier producers’ margins. The top five suppliers currently control approximately 78% of the market, making it difficult for smaller players to compete on more than just price.

Other Challenges

Supply Chain Vulnerabilities

The industry faces ongoing challenges with supply chain reliability, particularly for specialized materials used in FOUP manufacturing. The production of high-purity plastics and advanced composite materials is concentrated in a few global suppliers, creating potential bottlenecks. These vulnerabilities became particularly apparent during recent global supply chain disruptions, leading some manufacturers to reevaluate their sourcing strategies.

Technology Transition Risks

As semiconductor manufacturing transitions to increasingly advanced nodes, wafer carrier manufacturers must continually invest in R&D to keep pace. The transition from 200mm to 300mm wafers in the early 2000s demonstrated how technological shifts can rapidly make existing products obsolete. With potential future transitions to 450mm wafers (though currently on hold) or alternative substrate materials, manufacturers face significant uncertainty in their long-term product roadmaps.

300 MM WAFER FOUP AND FOSB MARKET TRENDS

Increasing Semiconductor Demand Driving FOUP and FOSB Market Growth

The global 300 mm wafer FOUP and FOSB market is experiencing robust growth, primarily fueled by the surging demand for semiconductors across industries such as consumer electronics, automotive, and IoT devices. The market, valued at USD 730 million in 2024, is projected to reach USD 1.2 billion by 2032, growing at a CAGR of 7.7%. This expansion is tightly linked to the rising complexity of semiconductor manufacturing, where contamination control becomes critical. FOUPs (Front Opening Unified Pods) and FOSBs (Front Opening Shipping Boxes) are essential in maintaining wafer integrity during production and transport, with manufacturers increasingly investing in advanced materials and automated handling features to meet stringent industry standards.

Other Trends

Regional Manufacturing Expansion

While Taiwan and the United States dominate wafer FOUP and FOSB consumption with 19.74% and 19.30% market shares respectively, new semiconductor fabrication plants (fabs) in regions like Southeast Asia and Europe are creating additional demand. Governments are incentivizing local chip production to reduce supply chain vulnerabilities, directly benefiting wafer handling solutions. For example, recent fab announcements in Japan and Germany are expected to drive a 12% annual increase in regional FOUP/FOSB demand through 2026.

Technological Advancements in Wafer Protection

Leading manufacturers are innovating beyond traditional polycarbonate materials to incorporate static-dissipative polymers and advanced filtration systems that maintain ultra-low particulate counts below 0.1 microns. The integration of IoT-enabled RFID tracking and environmental sensors allows real-time monitoring of wafer conditions during transit – a critical capability as wafer sizes potentially increase beyond 300mm. These enhancements are making FOUPs and FOSBs more than just containers, but intelligent components of the semiconductor ecosystem. Companies that combine mechanical precision with smart features are capturing premium market segments, with high-end FOUPs now commanding 30-40% price premiums over standard models.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Container Suppliers Focus on Innovation to Meet Rising Demand

The global 300 mm Wafer FOUP and FOSB market represents a moderately concentrated competitive environment, dominated by established suppliers with specialized expertise in semiconductor materials handling. Entegris emerges as the clear market leader, commanding approximately 28% of the revenue share in 2024. Their dominance stems from comprehensive product portfolios covering both FOUP and FOSB solutions, coupled with strategic partnerships with major foundries like TSMC and Samsung.

Meanwhile, Shin-Etsu Polymer maintains a strong second position with 17% market share, leveraging its polymer materials expertise to produce high-performance wafer containers. The company has particularly strengthened its position in the Japanese and South Korean markets through localized production facilities and R&D centers.

Several regional players are gaining traction by addressing specific market needs – Miraial’s focus on contamination control solutions has helped capture 8% of the European market, while Gudeng Precision achieved 12% market penetration in Taiwan through customized solutions for local foundries.

What makes this competition particularly intense is the technical specialization required – companies must balance material science, precision engineering, and cleanroom compatibility. Recent strategic moves include 3S Korea’s acquisition of a French competitor to expand in Europe, and Chuang King Enterprise’s partnership with a robotics firm to develop smart container solutions with IoT capabilities.

List of Key 300 mm Wafer FOUP and FOSB Manufacturers

- Entegris (U.S.) – Market leader in advanced materials handling

- Shin-Etsu Polymer (Japan) – Specialized polymer solutions provider

- Miraial (Japan) – Contamination control specialists

- Chuang King Enterprise (Taiwan) – Fast-growing Asian supplier

- Gudeng Precision (Taiwan) – Foundry-focused solutions

- 3S Korea (South Korea) – Expanding regional player

- Dainichi Shoji (Japan) – Niche precision component supplier

The competitive landscape continues evolving as semiconductor manufacturers demand higher wafer protection standards and smarter container features. While larger players maintain technology leadership through R&D investments (Entegris spends approximately 8% of revenue on R&D), regional specialists compete through customization and faster adaptation to local requirements. This dynamic ensures ongoing innovation across the sector.

Segment Analysis:

By Type

FOUP Segment Leads the Market Due to Critical Role in Cleanroom Manufacturing Environments

The market is segmented based on type into:

- FOUP (Front Opening Unified Pod)

- Subtypes: Standard capacity, high-capacity, and customized variants

- FOSB (Front Opening Shipping Box)

- Subtypes: Standard shipping containers, shock-resistant models

By Application

Wafer Foundry Segment Dominates Owing to Rising Semiconductor Production Demands

The market is segmented based on application into:

- Wafer Foundry

- IDM (Integrated Device Manufacturers)

By Material

PP (Polypropylene) Based Containers Hold Majority Share for Superior Chemical Resistance

The market is segmented based on material into:

- Polypropylene (PP)

- Polycarbonate (PC)

- Others (including composite materials)

By Capacity

25-Wafer Capacity Models Remain Most Preferred for Optimal Manufacturing Efficiency

The market is segmented based on capacity into:

- 13-wafer capacity

- 25-wafer capacity

- Custom capacities

Regional Analysis: 300 mm Wafer FOUP and FOSB Market

North America

The North American market for 300 mm FOUP and FOSB products remains robust, driven by advanced semiconductor manufacturing hubs in the United States, particularly in states like Texas and Arizona where major foundries operate. The region accounted for 19.3% of global consumption in 2022, second only to Taiwan. While domestic wafer production capacity is expanding through initiatives like the CHIPS Act, the market faces challenges from rising material costs and supply chain complexities. Local manufacturers emphasize automation-compatible designs to meet the needs of next-gen fabs, with Entegris maintaining strong market leadership through continuous product innovation in contamination control.

Europe

Europe’s position in the FOUP/FOSB market reflects its specialized semiconductor ecosystem, with Germany and France leading demand for high-precision wafer carriers. The region shows particular strength in manufacturing equipment integration, with EU-funded semiconductor initiatives driving adoption of smart container solutions featuring RFID tracking. However, energy-intensive production processes and stringent environmental regulations on specialty plastics create operational challenges for suppliers. Recent capacity expansions by major foundries suggest growing local demand, though the market remains dependent on imports from Asian manufacturers for cost-competitive solutions.

Asia-Pacific

As the dominant force in semiconductor production, Asia-Pacific commands the lion’s share of the global FOUP/FOSB market, with Taiwan alone consuming 19.74% of total supply. China’s rapid fab construction creates enormous demand, though local manufacturers still trail behind Japanese and Korean producers in technical sophistication. The region sees intense competition between established players like Shin-Etsu Polymer and emerging domestic suppliers, resulting in price pressures and margin compression. Southeast Asian nations are becoming important manufacturing bases for wafer carriers, leveraging lower production costs while still meeting the stringent cleanliness standards required for advanced node fabrication.

South America

This region presents a developing market with limited but growing opportunities in Brazil and Mexico where semiconductor assembly operations are expanding. The lack of local production facilities means nearly all FOUP/FOSB requirements are met through imports, primarily from North American and Asian suppliers. Infrastructure limitations and import duties create challenges in maintaining just-in-time delivery systems essential for wafer fabrication. While wafer carrier adoption grows with increased back-end semiconductor operations, the region remains a secondary market focusing primarily on replacement rather than expansion needs.

Middle East & Africa

The MEA region shows nascent potential with countries like Israel and Saudi Arabia making strategic investments in semiconductor manufacturing. Dubai’s emergence as a technology hub creates some demand for wafer handling solutions, though the market remains tiny compared to global standards. High transportation costs and limited technical expertise in wafer carrier maintenance restrain market growth. However, planned mega-projects in smart cities and AI infrastructure suggest future opportunities, particularly for suppliers who can offer localized support services alongside standard FOUP/FOSB products.

Report Scope

This market research report provides a comprehensive analysis of the global and regional 300 mm Wafer FOUP and FOSB markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the semiconductor wafer handling industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global 300 mm Wafer FOUP and FOSB market was valued at USD 730 million in 2024 and is projected to reach USD 1215 million by 2032, growing at a CAGR of 7.7%.

- Segmentation Analysis: Detailed breakdown by product type (FOUP vs FOSB), application (Wafer Foundry vs IDM), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific (including Taiwan which holds 19.74% market share), Latin America, and the Middle East & Africa, with country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants including Entegris, Shin-Etsu Polymer, Miraial, Chuang King Enterprise, and others, covering their product offerings, R&D focus, manufacturing capacity, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in wafer handling, integration of RFID tracking, automation compatibility, and evolving semiconductor fabrication standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth including semiconductor industry expansion, along with challenges such as high capital requirements and technical barriers to entry.

- Stakeholder Analysis: Insights for semiconductor manufacturers, equipment suppliers, investors, and policymakers regarding the evolving wafer handling ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from semiconductor equipment manufacturers, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global 300 mm Wafer FOUP and FOSB Market?

-> 300 mm Wafer FOUP and FOSB Market was valued at 730 million in 2024 and is projected to reach US$ 1215 million by 2032, at a CAGR of 7.7% during the forecast period.

Which key companies operate in Global 300 mm Wafer FOUP and FOSB Market?

-> Key players include Entegris, Shin-Etsu Polymer, Miraial, Chuang King Enterprise, Gudeng Precision, 3S Korea, and Dainichi Shoji, among others.

What are the key growth drivers?

-> Key growth drivers include expansion of semiconductor fabrication facilities, increasing demand for 300mm wafers, and automation in wafer handling processes.

Which region dominates the market?

-> Asia-Pacific is the dominant market, with Taiwan alone accounting for 19.74% of global consumption, followed by the United States with 19.30% market share.

What are the emerging trends?

-> Emerging trends include RFID integration for wafer tracking, advanced materials for contamination control, and smart FOUP/FOSB designs with embedded sensors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...