MARKET INSIGHTS

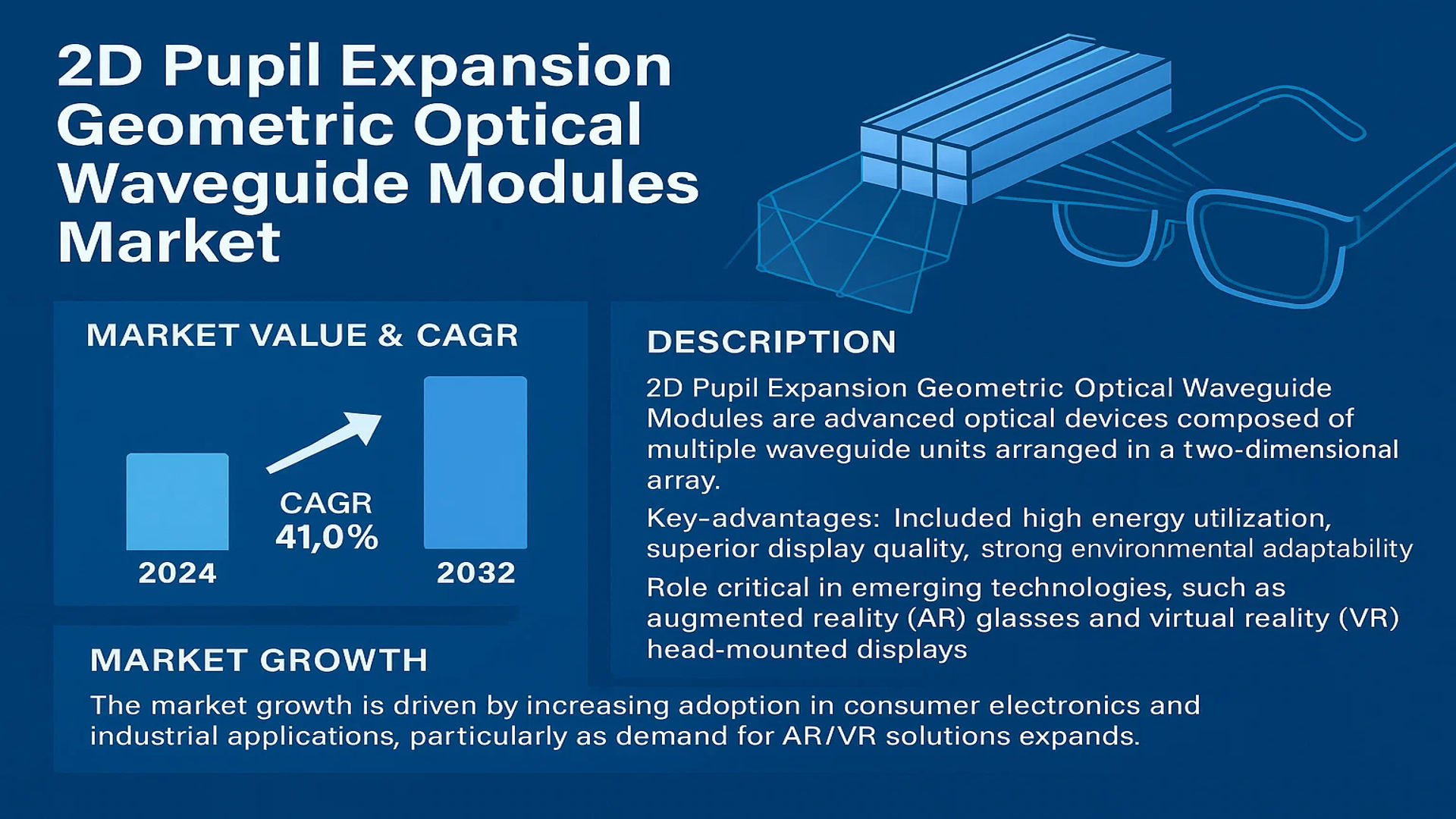

The global 2D Pupil Expansion Geometric Optical Waveguide Modules Market was valued at 38.9 million in 2024 and is projected to reach US$ 393 million by 2032, at a CAGR of 41.0% during the forecast period.

2D Pupil Expansion Geometric Optical Waveguide Modules are advanced optical devices composed of multiple waveguide units arranged in a two-dimensional array. These modules enable efficient pupil expansion of optical signals, offering key advantages such as high energy utilization, superior display quality, and strong environmental adaptability. They play a critical role in emerging technologies like augmented reality (AR) glasses and virtual reality (VR) head-mounted displays.

The market growth is driven by increasing adoption in consumer electronics and industrial applications, particularly as demand for AR/VR solutions expands. However, manufacturing complexities and high production costs pose challenges to widespread adoption. The resin segment is expected to show significant growth potential, while key players including Lumus, Optinvent, and Shanghai Lipai Optical Crystal Technology dominate the competitive landscape with innovative product developments.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Advanced AR/VR Technologies to Accelerate Market Growth

The global surge in augmented reality (AR) and virtual reality (VR) adoption is propelling the 2D Pupil Expansion Geometric Optical Waveguide Modules market forward. These modules enable wider fields of view and reduced bulk in AR glasses, addressing critical consumer demands for lightweight, immersive experiences. With AR/VR headset shipments projected to exceed 50 million units annually by 2027, manufacturers are increasingly integrating waveguide technologies to enhance optical performance while maintaining sleek form factors. Leading technology firms are investing heavily in waveguide solutions, recognizing their potential to revolutionize how users interact with digital content in both consumer and industrial applications.

Advancements in Material Science Enabling Next-Generation Waveguide Development

Material innovation is driving significant improvements in waveguide performance and manufacturability. Recent breakthroughs in nanoimprint lithography and high-index optical resins allow for thinner waveguide structures with superior light transmission characteristics. This enables modules to achieve higher resolution while reducing total internal reflection losses that previously limited optical efficiency. Manufacturers can now produce waveguide arrays with precision down to nanometer scales, resulting in modules that deliver enhanced brightness distribution across the expanded pupil area. The materials segment for these modules is witnessing a compound annual growth rate exceeding 35%, reflecting intense R&D activity across the value chain.

Military and Healthcare Applications Creating New Demand Frontiers

Beyond consumer electronics, defense and medical sectors are emerging as key growth verticals for waveguide modules. Military organizations worldwide are adopting AR headsets with waveguide displays for enhanced situational awareness, with procurement budgets for such systems increasing by 28% annually. In healthcare, surgical visualization systems incorporating these modules allow surgeons to maintain sterility while accessing critical patient data during procedures. The unique combination of high optical clarity and environmental durability makes 2D pupil expansion waveguides ideal for these mission-critical applications where reliability cannot be compromised.

MARKET RESTRAINTS

Complex Manufacturing Processes Limiting Production Scalability

The intricate fabrication requirements for geometric optical waveguides present substantial barriers to mass production. Each module requires precision alignment of multiple optical layers within micrometer tolerances, demanding specialized cleanroom facilities and highly trained technicians. Current yield rates for defect-free waveguide arrays remain below industry targets, causing production costs to stay elevated. This manufacturing complexity not only increases unit prices but also constrains the ability to rapidly scale output to meet growing market demand, particularly for high-volume consumer applications.

Thermal Management Challenges in Compact Module Designs

As waveguide modules shrink to enable slimmer AR/VR form factors, heat dissipation becomes a critical performance limitation. The intense light sources required for bright displays generate significant thermal loads in confined spaces, potentially causing optical distortions and reducing component lifespan. Current thermal management solutions often add unwanted bulk or compromise optical pathways, forcing difficult design trade-offs. Without breakthroughs in thermally conductive optical materials or innovative cooling architectures, this physical constraint may delay the commercialization of next-generation wearable displays planned for market release in the coming years.

MARKET CHALLENGES

High Development Costs Creating Barriers to Market Entry

The substantial capital investment required for waveguide R&D presents a formidable challenge for new market entrants. Developing a commercially viable 2D pupil expansion module typically demands multimillion-dollar investments in optical simulation software, prototype tooling, and testing equipment before reaching production readiness. This financial barrier has concentrated market share among a handful of well-funded players, potentially limiting innovation diversity. While the technology promises attractive margins at scale, the path to profitability remains lengthy and uncertain for all but the most resourced competitors.

Standardization Gaps Hindering Ecosystem Development

The lack of industry-wide specifications for waveguide interfaces and performance metrics creates integration challenges for device manufacturers. Without standardized optical coupling methods or quality assessment protocols, each module implementation requires extensive customization, increasing both development timelines and costs. This fragmentation also complicates component sourcing strategies, as waveguide modules from different suppliers often cannot be used interchangeably within the same product lineup. The absence of clear standards has become particularly problematic as AR platforms expand into regulated industries like automotive and medical devices where certification requirements demand consistent performance benchmarks.

MARKET OPPORTUNITIES

Emerging Automotive HUD Applications Opening New Revenue Streams

Automotive head-up display systems represent a high-growth opportunity for advanced waveguide technologies. As vehicle manufacturers transition from combiner-based HUDs to windshield-projected systems, the demand for wider fields of view and richer content display creates ideal conditions for 2D pupil expansion modules. Premium automakers are already prototyping waveguide-based augmented reality HUDs that project navigation cues and safety alerts across the entire windshield, with production implementations expected to begin within two years. This automotive segment could account for over 20% of total waveguide module revenues by the end of the forecast period.

Advancements in Mass Production Techniques Enabling Cost Reductions

Innovations in replication and assembly processes promise to significantly lower waveguide manufacturing costs. Emerging nanoimprint technologies can produce master waveguide templates with sub-wavelength features, enabling high-volume stamping of optical structures with nanometer precision. When combined with automated alignment systems now entering pilot production, these techniques may reduce module production costs by up to 40% within three years. Such cost improvements would make waveguide solutions economically viable for mid-range consumer electronics, potentially multiplying the addressable market size severalfold.

Integration with Metaverse Platforms Creating Long-Term Growth Potential

The metaverse ecosystem development presents a transformative opportunity for waveguide display technologies. As virtual world platforms evolve toward persistent 3D environments requiring comfortable extended use, lightweight AR glasses with expansive visual fields will become essential interfaces. Major technology firms are already positioning waveguide solutions as the display foundation for next-generation metaverse hardware, with development partnerships increasing by 58% year-over-year. This strategic alignment with the metaverse roadmap ensures waveguide modules remain at the forefront of spatial computing innovation for the foreseeable future.

2D PUPIL EXPANSION GEOMETRIC OPTICAL WAVEGUIDE MODULES MARKET TRENDS

Augmented Reality (AR) and Virtual Reality (VR) Adoption Accelerates Market Growth

The global 2D Pupil Expansion Geometric Optical Waveguide Modules market is witnessing rapid expansion, driven by the increasing adoption of AR and VR technologies across multiple industries. With an estimated valuation of $38.9 million in 2024, the market is projected to surge to $393 million by 2032, growing at a CAGR of 41.0%. This exponential growth is fueled by the demand for lightweight, high-resolution displays in applications such as smart glasses, military headsets, and training simulations. Technological advancements like ultra-thin waveguide designs and high refractive index materials are enhancing optical efficiency, making these modules indispensable in next-gen display solutions.

Other Trends

Consumer Electronics Boom

The consumer electronics sector is a primary driver for 2D Pupil Expansion Geometric Optical Waveguide Modules, particularly in AR-enabled smart glasses and VR headsets. Leading tech companies are investing heavily in integrating waveguide-based displays to improve user experiences with wider fields of view and better brightness efficiency. Resin-based waveguide modules, projected to grow substantially, are gaining traction due to their cost-effectiveness and flexibility in mass production. Meanwhile, applications in gaming, navigation, and remote collaboration are further boosting market penetration.

Technological Innovations Enhance Competitive Landscape

Key market players like Lumus, Optinvent, and Shanghai Lipai Optical Crystal Technology are spearheading innovations in waveguide technology to maintain a competitive edge. Developments such as multi-layer optical coatings and advanced pupil replication techniques are enhancing light transmission efficiency, a critical factor for AR/VR adoption. Regional dynamics show that North America, led by the U.S., holds the largest market share due to strong R&D investments, while China is emerging as a fast-growing hub with increasing manufacturing capabilities and government support for AR/VR development.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Alliances Drive Market Leadership in Optical Waveguide Technology

The global 2D Pupil Expansion Geometric Optical Waveguide Modules market exhibits a dynamic competitive environment, characterized by a blend of established technology leaders and emerging innovators. Lumus has established itself as a pioneer in the sector, leveraging its extensive expertise in AR/VR optics to capture a significant market share. The company’s focus on high-performance waveguide displays has positioned it as a preferred supplier for consumer electronics manufacturers seeking cutting-edge optical solutions.

Optinvent and Shanghai Lipai Optical Crystal Technology have emerged as formidable competitors, particularly in the Asian markets. These companies have differentiated themselves through proprietary manufacturing techniques that enable cost-effective production without compromising optical clarity or energy efficiency. Their growing partnerships with regional device manufacturers have accelerated adoption across multiple application segments.

The market has witnessed intensified R&D activities as participants race to develop waveguide modules with wider fields of view and reduced thickness. Several leading companies have recently expanded their production capacities to meet the anticipated surge in demand from the AR glasses sector, which is projected to grow substantially through 2032.

While the technology landscape remains competitive, companies such as Beijing Nai Dejia Display Technology and Gudong Technology are carving out specialized niches through customized waveguide solutions. These firms have demonstrated particular strength in industrial applications where ruggedized designs and superior environmental resistance provide critical competitive advantages.

List of Key 2D Pupil Expansion Geometric Optical Waveguide Module Companies

- Lumus (Israel)

- Optinvent (France)

- Shanghai Lipai Optical Crystal Technology Co., Ltd. (China)

- Lohn Optics (China)

- LINGXI (China)

- Gudong Technology (China)

- OPTIX (China)

- Beijing Nai Dejia Display Technology Co., Ltd. (China)

Segment Analysis:

By Type

Resin Segment Leads Due to Its Lightweight and Cost-Effectiveness in AR/VR Applications

The market is segmented based on type into:

- Resin

- Subtypes: Polymer-based, hybrid nanocomposites, and others

- Glass

- Subtypes: High-index glass, low-dispersion glass, and others

By Application

Consumer Electronics Segment Dominates Due to Rising Demand for AR/VR Devices

The market is segmented based on application into:

- Consumer Electronics

- Subtypes: AR glasses, VR headsets, smart eyewear

- Industrial Manufacturing

- Subtypes: Quality inspection, assembly line guidance

- Advanced Medical

- Subtypes: Surgical navigation, medical training

- Military & Defense

- Others

By End-Use Industry

Augmented Reality Sector Holds Significant Potential Due to Growing Commercialization

The market is segmented based on end-use industry into:

- Augmented Reality Devices

- Virtual Reality Systems

- Mixed Reality Solutions

- Head-Up Displays

- Others

Regional Analysis: 2D Pupil Expansion Geometric Optical Waveguide Modules Market

Asia-Pacific

The Asia-Pacific region dominates the 2D Pupil Expansion Geometric Optical Waveguide Modules market, driven by China’s aggressive investments in AR/VR technology and its position as the world’s manufacturing hub for consumer electronics. With major players like Shanghai Lipai Optical Crystal Technology and LINGXI headquartered here, the region benefits from vertically integrated production ecosystems. Japan and South Korea contribute significantly through their advanced display manufacturing capabilities, while Southeast Asia emerges as a cost-competitive production base. The region’s 41.2% market share in 2024 reflects its dual role as both manufacturing center and growing end-user market, particularly for AR glasses in industrial and consumer applications.

North America

North America represents the innovation nucleus for waveguide technology, with U.S.-based firms like Lumus pioneering advanced optical solutions. The region’s strong R&D ecosystem and early adoption of AR in defense, healthcare, and enterprise applications fuel demand. Though manufacturing costs are higher than Asia, the premium positioning of North American waveguide modules in specialized applications commands higher margins. Collaborative projects between tech giants and waveguide manufacturers are accelerating commercialization, with particular growth in medical AR visualization systems and industrial maintenance applications.

Europe

Europe maintains a strong position in the waveguide market through precision optical manufacturing and research excellence. Countries like Germany and France lead in industrial AR applications, where waveguide modules enable hands-free operation in manufacturing and field service. EU funding programs support waveguide development for both consumer and professional use cases. However, the region faces challenges in scaling production to compete with Asian manufacturers on volume. Strategic partnerships between European optical firms and automotive/aerospace industries demonstrate the technology’s growing adoption in high-value sectors.

Middle East & Africa

This emerging market shows early-stage adoption of waveguide technology, primarily driven by smart city initiatives in the UAE and Saudi Arabia. While local manufacturing remains limited, government investments in digital infrastructure create opportunities for waveguide integration in tourism, education and oil/gas applications. The region’s growth potential is tempered by reliance on imported components and limited local expertise in optical engineering. However, partnerships with international AR solution providers are gradually building the necessary ecosystem.

South America

South America represents a developing market for waveguide modules, with Brazil showing the most activity in industrial and medical AR applications. Economic volatility and infrastructure limitations hinder widespread adoption, though niche applications in mining, agriculture and healthcare demonstrate the technology’s potential. The region primarily serves as an importer of waveguide components from Asia and North America, with localized assembly gradually emerging in technology hubs like São Paulo and Buenos Aires.

Report Scope

This market research report provides a comprehensive analysis of the global 2D Pupil Expansion Geometric Optical Waveguide Modules market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 38.9 million in 2024 and is projected to reach USD 393 million by 2032, growing at a CAGR of 41.0%.

- Segmentation Analysis: Detailed breakdown by product type (Resin, Glass), application (Consumer Electronics, Industrial Manufacturing, Advanced Medical, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with the U.S. and China being key growth markets.

- Competitive Landscape: Profiles of leading market participants including Lumus, Optinvent, Shanghai Lipai Optical Crystal Technology, Lohn Optics, and LINGXI, covering their product portfolios, R&D focus, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging waveguide technologies, AR/VR integration, and advancements in optical materials manufacturing.

- Market Drivers & Restraints: Evaluation of factors such as growing AR/VR adoption, display technology advancements, and challenges in manufacturing precision and cost optimization.

- Stakeholder Analysis: Strategic insights for component suppliers, OEMs, AR/VR device manufacturers, and investors regarding market opportunities and challenges.

Primary and secondary research methods are employed, including interviews with industry experts, manufacturer surveys, and analysis of verified market data to ensure accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global 2D Pupil Expansion Geometric Optical Waveguide Modules Market?

-> 2D Pupil Expansion Geometric Optical Waveguide Modules Market was valued at 38.9 million in 2024 and is projected to reach US$ 393 million by 2032, at a CAGR of 41.0% during the forecast period.

Which key companies operate in this market?

-> Key players include Lumus, Optinvent, Shanghai Lipai Optical Crystal Technology, Lohn Optics, LINGXI, Gudong Technology, OPTIX, and Beijing Nai Dejia Display Technology.

What are the key growth drivers?

-> Growth is driven by rising AR/VR adoption, demand for compact display solutions, and advancements in waveguide manufacturing technologies.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth potential, while North America currently leads in technological innovation.

What are the emerging trends?

-> Emerging trends include development of hybrid waveguide solutions, integration with smart glasses, and improved manufacturing processes for higher yields.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...