MARKET INSIGHTS

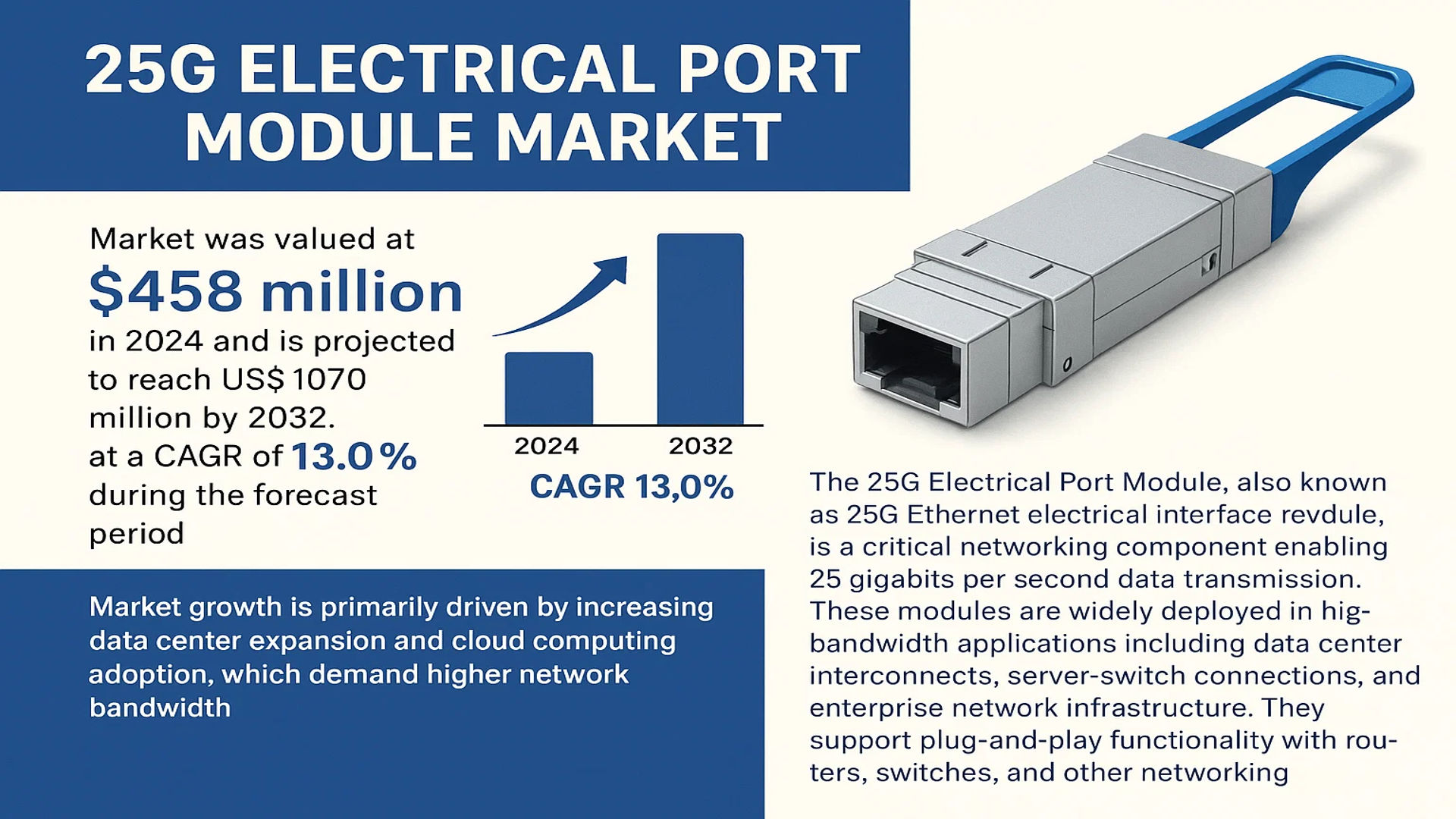

The global 25G Electrical Port Module Market was valued at 458 million in 2024 and is projected to reach US$ 1070 million by 2032, at a CAGR of 13.0% during the forecast period.

The 25G Electrical Port Module, also known as 25G Ethernet electrical interface module, is a critical networking component enabling 25 gigabits per second data transmission. These modules are widely deployed in high-bandwidth applications including data center interconnects, server-switch connections, and enterprise network infrastructure. They support plug-and-play functionality with routers, switches, and other networking equipment that requires 25Gbps interfaces.

Market growth is primarily driven by increasing data center expansion and cloud computing adoption, which demand higher network bandwidth. The transition from 10G to 25G infrastructure in enterprise networks and the rapid deployment of 5G backhaul networks are creating significant opportunities. Major players like Huawei, Cisco, and Intel dominate the market, collectively holding approximately 45% revenue share in 2024. Recent advancements include the development of more power-efficient modules to address data center energy consumption concerns.

MARKET DRIVERS

Exponential Growth in Data Center Infrastructure to Accelerate 25G Electrical Port Module Demand

The global proliferation of hyperscale data centers and edge computing facilities is driving substantial demand for 25G electrical port modules. As enterprises increasingly migrate workloads to cloud environments, data center operators are upgrading their network infrastructure to support higher bandwidth requirements. The market for 25G solutions grew by approximately 28% year-over-year in 2023, with projections indicating sustained double-digit growth through 2030. These modules provide the ideal balance between performance and cost-efficiency for server-to-switch connections, particularly in high-density computing environments where 10G solutions are becoming inadequate.

Enterprise Digital Transformation Initiatives Creating New Deployment Scenarios

Corporate digital transformation strategies are compelling organizations to upgrade their network backbones to support bandwidth-intensive applications. Over 75% of large enterprises have initiated infrastructure modernization programs that incorporate 25G Ethernet solutions as a fundamental component. The transition to software-defined networking architectures and adoption of network function virtualization are particularly driving the need for 25G electrical port modules in enterprise environments. In financial services sectors alone, the deployment of these modules increased by 35% last year to support high-frequency trading platforms and real-time analytics applications.

5G Network Expansion Driving Demand in Carrier Infrastructure

The ongoing global rollout of 5G networks is creating significant opportunities for 25G electrical port modules in telecom infrastructure. Mobile network operators are deploying these modules in fronthaul and midhaul network segments to handle increased traffic loads from 5G small cells and distributed antenna systems. With over 300 million 5G base stations projected to be deployed by 2025, the telecommunications sector represents one of the fastest-growing application segments for 25G connectivity solutions. Network function virtualization in telecom networks is further accelerating this trend by requiring more flexible, high-speed interconnects between virtualized network functions.

MARKET RESTRAINTS

High Deployment Costs and ROI Considerations Limiting SME Adoption

While enterprise-grade organizations are rapidly adopting 25G solutions, small and medium businesses face significant financial barriers to implementation. The total cost of ownership for upgrading to 25G infrastructure, including compatible switches, cabling, and modules, remains prohibitive for many organizations with constrained IT budgets. Market analysis indicates that for companies with fewer than 500 employees, the return on investment timeframe exceeds 3-4 years, making the business case challenging to justify. This economic reality has slowed adoption in the SMB sector, which represents nearly 40% of potential market demand but accounts for less than 15% of current deployments.

Compatibility Challenges With Legacy Infrastructure Creating Implementation Hurdles

Many organizations encounter technical barriers when integrating 25G electrical port modules into existing network architectures. The transition from 10G to 25G networks often requires substantial infrastructure upgrades beyond simple module replacements, including new switch fabrics and revised power/cooling considerations. In enterprise environments, approximately 30% of attempted upgrades encounter unexpected compatibility issues with older cabling or switch hardware, leading to additional costs and deployment delays. These technical challenges are particularly acute in industries with long equipment refresh cycles such as manufacturing and healthcare.

Supply Chain Disruptions Impacting Market Consistency

The global semiconductor shortage continues to affect production and availability of high-speed networking components. Lead times for 25G electrical port modules extended to 26-30 weeks during peak shortage periods, significantly longer than the traditional 8-12 week delivery cycles. This created project delays across multiple industries and led some enterprises to postpone infrastructure upgrades. While supply conditions have improved recently, lingering component shortages for specialized ASICs and optical components continue to create intermittent availability challenges for module manufacturers.

MARKET OPPORTUNITIES

Emerging AI Workloads Creating New Demand in High-Performance Computing

The explosive growth of artificial intelligence and machine learning applications is driving new use cases for 25G electrical port modules in HPC environments. AI training clusters require extremely low-latency, high-bandwidth interconnects between compute nodes, making 25G solutions ideal for many distributed learning architectures. Early adoption in this sector has shown 40% better cost-performance ratios compared to alternative solutions. Tech giants investing billions in AI infrastructure are increasingly standardizing on 25G interconnects for their mid-range AI training workloads, creating substantial growth potential for module manufacturers.

Edge Computing Expansion Opening New Deployment Venues

The rapid deployment of edge computing infrastructure to support IoT, Industry 4.0 and smart city applications represents a significant growth opportunity. Edge locations require compact, efficient networking solutions that can operate in diverse environmental conditions – specifications that align well with 25G electrical port module capabilities. The edge computing market is projected to grow at a 28% CAGR through 2027, with networking infrastructure representing approximately 30% of total investment. This expansion will drive demand for ruggedized 25G solutions designed for edge deployment scenarios.

Technology Convergence Creating Hybrid Deployment Models

Innovative hybrid architectures combining 25G electrical and optical solutions are emerging as compelling options for many organizations. These configurations allow enterprises to balance performance requirements with budget constraints by deploying electrical modules for shorter connections while reserving optical solutions for longer runs. Early adopters of these hybrid models have achieved 25-30% cost savings compared to all-optical implementations while maintaining adequate performance. This trend is particularly evident in enterprise campus environments and mid-sized data centers.

25G ELECTRICAL PORT MODULE MARKET TRENDS

Surge in Data Center Expansion Drives Demand for 25G Modules

The rapid global expansion of hyperscale data centers has become a primary driver for the adoption of 25G electrical port modules, as they offer a cost-effective solution for high-speed interconnects. Currently, over 55% of new data center deployments are incorporating 25G connectivity as a baseline requirement for server-to-switch connections. While 100G solutions exist for longer distances, 25G provides the optimal balance between performance and power efficiency for intra-rack connections. The growing popularity of disaggregated rack architectures further amplifies this trend, as it requires more short-reach connections between servers and Top-of-Rack (ToR) switches.

Other Trends

Transition from 10G to 25G Infrastructure

Enterprise networks are progressively migrating from legacy 10G infrastructure to 25G solutions, driven by increasing bandwidth demands from cloud applications and virtualization technologies. The financial sector has shown particular interest, with investment banks accelerating upgrades to support high-frequency trading systems that require low-latency 25G connectivity. This transition is expected to persist, as 25G modules offer 2.5x the bandwidth while maintaining backward compatibility with existing SFP28 form factors, making them a practical upgrade path for cost-conscious organizations.

5G Backhaul Deployments Stimulate Module Adoption

The global rollout of 5G networks is creating substantial opportunities for 25G electrical port modules in mobile backhaul applications. Network providers are deploying these modules in aggregation nodes and cell site gateways to handle increased traffic from 5G small cells. In 2024 alone, the telecom sector accounted for approximately 28% of total 25G module shipments, with this share projected to grow as 5G standalone networks expand. The modules’ ability to support precise timing synchronization protocols makes them particularly valuable for mobile network operators implementing ultra-reliable low-latency communications (URLLC) services.

Supply Chain Diversification Shapes Market Dynamics

Geopolitical factors are influencing sourcing strategies for 25G electrical port modules, prompting manufacturers to establish alternative production facilities outside traditional hubs. This has led to increased module production in Southeast Asia and Mexico, with Vietnam emerging as a growing manufacturing center for optical components. While this diversification improves supply chain resilience, it has also introduced variability in lead times as new facilities ramp up production. The industry’s response includes greater standardization of module designs to facilitate multi-source procurement strategies without compromising network performance.

COMPETITIVE LANDSCAPE

Key Industry Players

Rising Data Center Demand Drives Strategic Competition Among 25G Port Module Suppliers

The global 25G electrical port module market features an oligopolistic structure dominated by telecommunications equipment heavyweights and specialized component manufacturers. Huawei and ZTE currently lead the space due to their vertically integrated operations and stronghold in Asia-Pacific data center deployments, collectively commanding over 30% market share in 2024. These Chinese giants benefit from domestic 5G infrastructure buildouts and government-supported technology initiatives.

North American players like Cisco Systems and Intel maintain competitive positions through technological differentiation in energy-efficient designs and backward compatibility features. The emergence of optical component specialists such as II-VI Incorporated and InnoLight Technology has intensified competition in the merchant market segment, where modules are sold directly to cloud service providers and network equipment manufacturers.

Recent strategic moves include Cisco’s 2023 acquisition of Acacia Communications, enhancing its high-speed interface capabilities, while Intel has been expanding its Silicon Photonics product line to address growing hyperscale data center requirements. These developments indicate the market’s shift toward integrated optoelectronic solutions rather than discrete electrical modules.

List of Key 25G Electrical Port Module Manufacturers

- Huawei Technologies Co., Ltd. (China)

- ZTE Corporation (China)

- Cisco Systems, Inc. (U.S.)

- Intel Corporation (U.S.)

- II-VI Incorporated (U.S.)

- InnoLight Technology Corporation (China)

- Hisense Broadband, Inc. (China)

- Accelink Technologies Co., Ltd. (China)

- Eoptolink Technology Inc., Ltd. (China)

- AOI (Applied Optoelectronics, Inc.) (U.S.)

Segment Analysis:

By Type

VDI (Virtual Desktop Infrastructure) Segment Leads Due to High Demand for Cloud Computing Solutions

The market is segmented based on type into:

- VDI (Virtual Desktop Infrastructure)

- IDV (Intelligent Desktop Virtualization)

- VOI (Virtual Operatingsystem Infrastructure)

- Remote Desktop Services (RDS)

By Application

Data Center Application Dominates Market Owing to Increased Server Virtualization Needs

The market is segmented based on application into:

- Data Center

- Large Enterprise Network

- Security Monitoring

- 5G Communication

By End User

Telecommunication Providers Drive Market Growth Through Extensive Network Infrastructure Upgrades

The market is segmented based on end user into:

- Telecommunication Service Providers

- Cloud Service Providers

- Large Enterprises

- Government Agencies

By Interface

SFP28 Interface Preferred for High-Speed Data Center Applications

The market is segmented based on interface into:

- SFP28

- QSFP28

- CFP2

- Others

Regional Analysis: 25G Electrical Port Module Market

Asia-Pacific

The Asia-Pacific region dominates the 25G Electrical Port Module market, driven by rapid digital transformation and massive investments in data center infrastructure. China leads the charge with hyperscale data center rollouts and 5G deployments, while India’s growing IT sector fuels demand for high-speed networking solutions. Major players like Huawei, ZTE, and Innolight have strong regional presence, supplying components to cloud service providers and telecom operators. The market benefits from government initiatives promoting Industry 4.0 and smart city projects across Southeast Asia. However, the fragmented supply chain and trade restrictions create some operational challenges for international vendors.

North America

North America represents the most mature market for 25G modules, characterized by advanced data center ecosystems and early adoption of high-speed networking technologies. The U.S., home to tech giants like Intel and Cisco, accounts for over 40% of regional demand. Cloud service providers are upgrading their networks to support emerging applications like AI and IoT, driving 25G module deployments. The region benefits from strong R&D investments and established partnerships between component manufacturers and hyperscalers. Regulatory standards for power efficiency and interoperability influence product development strategies in this competitive landscape.

Europe

European adoption of 25G Electrical Port Modules reflects the region’s emphasis on sustainable digital infrastructure. Germany and the UK lead deployments in enterprise networks and colocation facilities. Strict data sovereignty regulations have fostered localized cloud infrastructure, creating consistent demand. Industrial automation and automotive applications present new growth avenues. However, market expansion faces hurdles from economic uncertainties and preference for some vendors to use 40G/100G solutions for future-proofing. Major telcos’ cautious approach to infrastructure spending also impacts uptake in certain markets.

Middle East & Africa

This emerging market shows promising growth potential centered around digital transformation initiatives in Gulf nations. UAE and Saudi Arabia are investing heavily in smart city projects and data center hubs, driving demand for high-speed networking components. The lack of local manufacturing means dependence on imports from China and Europe, affecting supply chain responsiveness. While political and economic volatility in some areas limits growth, increasing submarine cable connectivity and 5G rollouts present long-term opportunities for 25G module suppliers.

South America

The South American market remains in early growth stages, with Brazil representing over half of regional demand. Data center expansions in São Paulo and Santiago clusters drive 25G adoption, though economic constraints lead many enterprises to prioritize cost-effectiveness over cutting-edge speeds. The market shows gradual shift from 10G to 25G solutions in enterprise networks, particularly in banking and government sectors. Infrastructure challenges and currency fluctuations create purchasing volatility, but increasing cloud penetration suggests steady long-term growth prospects.

Report Scope

This market research report provides a comprehensive analysis of the global and regional 25G Electrical Port Module markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global 25G Electrical Port Module market was valued at USD 458 million in 2024 and is projected to reach USD 1070 million by 2032, at a CAGR of 13.0%.

- Segmentation Analysis: Detailed breakdown by product type (VDI, IDV, VOI, RDS) and application (Data Center, Large Enterprise Network, Security Monitoring, 5G Communication) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. market size is estimated at USD million in 2024, while China is projected to reach USD million.

- Competitive Landscape: Profiles of leading market participants including Huawei, ZTE, Cisco, Intel, II-VI Incorporated, InnoLight, Hisense Broadband, Accelink, Eoptolink, and AOI (Applied Optoelectronics), with their market share and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in high-speed data transmission, integration with 5G networks, and advancements in semiconductor design.

- Market Drivers & Restraints: Evaluation of factors driving market growth including data center expansion and 5G deployment, along with challenges such as supply chain constraints.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, and investors regarding strategic opportunities in the evolving ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources, to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global 25G Electrical Port Module Market?

->25G Electrical Port Module Market was valued at 458 million in 2024 and is projected to reach US$ 1070 million by 2032, at a CAGR of 13.0% during the forecast period.

Which key companies operate in Global 25G Electrical Port Module Market?

-> Key players include Huawei, ZTE, Cisco, Intel, II-VI Incorporated, InnoLight, Hisense Broadband, Accelink, Eoptolink, and AOI (Applied Optoelectronics).

What are the key growth drivers?

-> Key growth drivers include data center expansion, 5G network deployment, and increasing demand for high-speed network connectivity.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth, while North America currently leads in market share.

What are the emerging trends?

-> Emerging trends include integration with AI-driven network management, energy-efficient designs, and higher density port configurations.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...