MARKET INSIGHTS

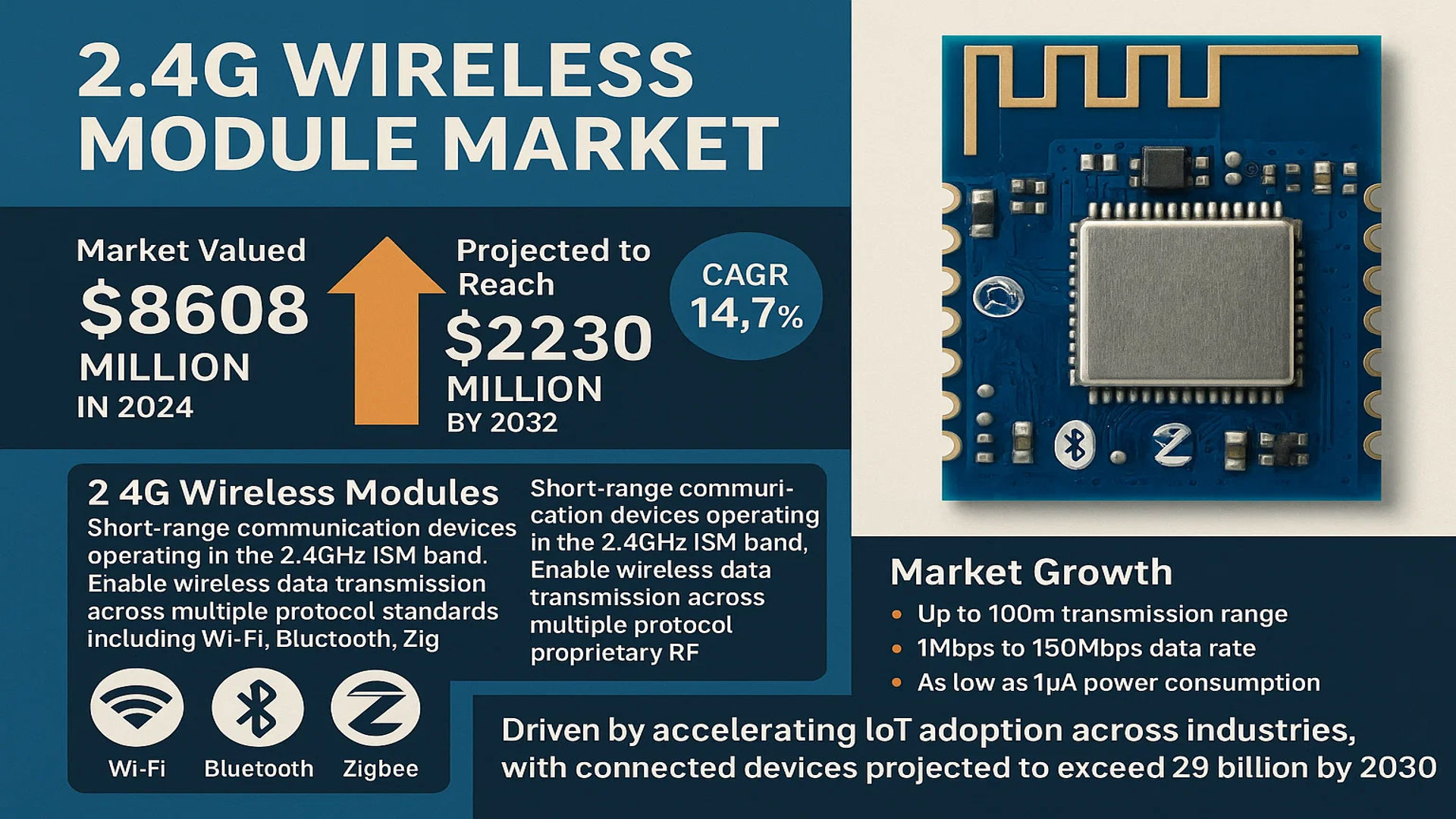

The global 2.4G Wireless Module Market was valued at 8608 million in 2024 and is projected to reach US$ 22300 million by 2032, at a CAGR of 14.7% during the forecast period.

2.4G wireless modules are short-range communication devices operating in the 2.4GHz ISM band. These modules enable wireless data transmission across multiple protocol standards including Wi-Fi (IEEE 802.11), Bluetooth (IEEE 802.15.1), Zigbee (IEEE 802.15.4), and proprietary RF protocols. Key technical characteristics include transmission ranges up to 100 meters (line-of-sight), data rates from 1Mbps to 150Mbps depending on protocol, and power consumption as low as 1μA in sleep mode for battery-operated devices.

Market growth is driven by accelerating IoT adoption across industries, with the number of connected devices projected to exceed 29 billion by 2030. The consumer electronics segment accounts for 42% of current demand, particularly for smart home devices. However, industrial automation applications are growing fastest at 18.2% CAGR due to Industry 4.0 implementations. Major manufacturers like NXP Semiconductors and Texas Instruments continue to innovate with multi-protocol modules combining BLE 5.2 and 802.11ax Wi-Fi, addressing the need for interoperable connectivity solutions.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of IoT Ecosystems to Accelerate Market Adoption

The proliferation of Internet of Things (IoT) devices across multiple industries is significantly driving demand for 2.4G wireless modules. With over 30 billion active IoT connections worldwide, these modules serve as critical enablers for device connectivity, offering reliable communication in industrial automation, smart cities, and wearable technologies. The 2.4GHz frequency band provides an optimal balance between range and power efficiency, making it ideal for battery-operated IoT sensors. Recent developments in edge computing further enhance the value proposition of 2.4G modules by enabling localized data processing, reducing latency and bandwidth requirements.

Smart Home Revolution Fueling Module Deployment

Rapid adoption of smart home technologies continues to create substantial demand for 2.4G wireless solutions. The global smart home market is projected to exceed $400 billion by 2030, with wireless modules forming the backbone of interconnected home ecosystems. Products such as smart thermostats, security systems, and voice-controlled devices predominantly utilize 2.4GHz wireless communication due to its compatibility with WiFi, Bluetooth, and Zigbee protocols. Leading manufacturers are developing hybrid modules that support multiple wireless standards simultaneously, providing consumers with seamless interoperability across different smart home platforms.

➤ Innovations in module design have achieved 40% power consumption reduction in latest-generation products, addressing the critical need for energy efficiency in always-on smart home devices.

Furthermore, government initiatives promoting smart city development and energy-efficient buildings are creating additional momentum for market expansion. Regulatory mandates for intelligent lighting controls and building automation systems particularly favor 2.4G wireless solutions due to their cost-effectiveness and established infrastructure.

MARKET RESTRAINTS

Spectrum Congestion Issues Limiting Performance Potential

While the 2.4GHz band offers widespread compatibility, its unlicensed nature has led to significant spectrum congestion in urban environments. Over 80% of consumer WiFi networks operate in this frequency range, creating interference challenges that degrade signal quality and reliability. Industrial applications requiring real-time communication suffer particularly from this limitation, as packet collisions and retransmissions can disrupt critical operations. The growing density of wireless devices in both consumer and industrial settings exacerbates these interference problems, creating barriers to adoption in high-performance applications.

Security Vulnerabilities Hampering Critical Applications

Persistent cybersecurity threats present another significant restraint for 2.4G wireless technology adoption. The ubiquity of these modules makes them attractive targets for malicious actors, with documented cases of unauthorized access in both consumer and industrial systems. While newer security protocols like WPA3 and Bluetooth 5.2 provide enhanced protection, many deployed modules still rely on outdated encryption standards. Industries handling sensitive data, such as healthcare and financial services, remain cautious about implementing 2.4G solutions without robust end-to-end security frameworks. This security-conscious mindset slows market penetration in sectors where wireless vulnerabilities could have serious consequences.

MARKET CHALLENGES

Component Shortages Disrupting Supply Chains

The semiconductor supply chain crisis continues to impact 2.4G wireless module production, with lead times for RF components extending beyond 40 weeks in some cases. This shortage affects manufacturers’ ability to meet growing demand, particularly for industrial-grade modules requiring specialized chipsets. The situation is compounded by geopolitical factors affecting semiconductor trade, creating uncertainty in production planning. Smaller manufacturers face particular difficulties securing consistent component supplies, potentially leading to market consolidation as larger players leverage their purchasing power.

Other Challenges

Regulatory Compliance Burden

Differing regional radio frequency regulations require expensive product variations and certification processes. Modules designed for global deployment must undergo multiple testing regimes, increasing time-to-market and development costs.

Technical Complexity

Integration challenges arise when combining multiple wireless protocols in single modules. Engineers must balance RF performance, power consumption, and cost while meeting shrinking form factor requirements.

MARKET OPPORTUNITIES

Emergence of AI-Enabled Modules Creating New Possibilities

The integration of machine learning capabilities directly into wireless modules presents transformative opportunities. Next-generation products incorporating embedded AI processors can optimize network performance dynamically, adapt transmission parameters based on environmental conditions, and predict maintenance needs. This evolution from simple communication devices to intelligent edge nodes aligns with Industry 4.0 requirements, potentially creating higher-value market segments. Early implementations in predictive maintenance systems demonstrate 30-50% improvements in equipment uptime through real-time vibration and temperature monitoring.

Healthcare Wearables Driving Specialized Demand

The medical wearables sector represents a high-growth vertical for 2.4G modules, with continuous patient monitoring devices requiring reliable, low-power wireless connectivity. Advancements in biosensors and FDA-cleared wearable technologies are creating demand for medical-grade modules with enhanced data integrity features. The global market for medical wearables is projected to maintain 20%+ annual growth, presenting module manufacturers with opportunities to develop specialized products meeting stringent healthcare reliability standards. New designs incorporate redundant communication paths and interference mitigation techniques critical for life-critical applications.

2.4G WIRELESS MODULE MARKET TRENDS

IoT and Smart Device Expansion Driving Market Growth

The global 2.4G wireless module market has witnessed significant growth, fueled by the rapid expansion of the Internet of Things (IoT) and smart device ecosystems. With an estimated market value of $8,608 million in 2024, the demand for reliable short-range wireless communication continues to surge. A key driver is the widespread adoption of smart home devices—from connected thermostats to security systems—which increasingly rely on Wi-Fi, Bluetooth, and Zigbee modules for seamless interoperability. Forecasts suggest the market could reach $22,300 million by 2032, growing at a 14.7% CAGR, as industries prioritize wireless solutions for automation and connectivity.

Other Trends

Industrial Automation Adoption

Industrial applications are increasingly integrating 2.4G wireless modules to enhance operational efficiency and enable real-time monitoring. Factories deploying IoT-based predictive maintenance systems, for instance, leverage these modules for sensor networks that minimize downtime. The industrial automation segment, which accounted for nearly 30% of global module applications in 2024, benefits from protocols like Zigbee’s low-power mesh networking, optimizing energy usage in large-scale deployments. Meanwhile, automotive manufacturers are embedding these modules in telematics and infotainment systems, creating new revenue streams for suppliers.

Technological Innovations and Protocol Diversification

Advancements in multi-protocol support are reshaping the competitive landscape. Leading manufacturers such as NXP Semiconductors and Texas Instruments now design modules that combine Wi-Fi 6 and Bluetooth 5.2, offering higher throughput and extended range. The rise of AI-powered edge devices further amplifies demand, as these modules facilitate faster on-device processing with minimal latency. Concurrently, the emergence of Thread protocol—optimized for smart home interoperability—signals a shift toward unified wireless ecosystems, encouraging broader adoption across consumer and industrial sectors.

Despite these opportunities, challenges such as spectrum congestion in the 2.4GHz band and rising security concerns persist. However, ongoing R&D in adaptive frequency hopping and end-to-end encryption ensures these modules remain critical to the future of wireless connectivity.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Invest in Innovation to Maintain Competitive Edge in 2.4G Connectivity

The global 2.4G wireless module market features a dynamic mix of semiconductor giants, specialized wireless solution providers, and emerging regional players. NXP Semiconductors and Texas Instruments dominate the landscape, collectively holding over 25% market share in 2024 due to their comprehensive portfolio covering Wi-Fi, Bluetooth, and Zigbee solutions. Their competitive advantage stems from decades of wireless expertise and strong relationships with consumer electronics manufacturers.

Qualcomm has been rapidly gaining ground, particularly in high-performance Wi-Fi modules, driven by its acquisition of Atheros and subsequent integration of advanced connectivity solutions. Meanwhile, Nordic Semiconductor maintains strong positioning in low-power IoT applications, with its nRF52 series becoming industry standard for Bluetooth-enabled devices. These companies benefit from their ability to offer protocol-stack-integrated modules, significantly reducing development time for OEMs.

The market also features strong regional competitors like Espressif Systems from China, whose cost-optimized ESP32 modules have captured significant market share in smart home applications. Similarly, Realtek and Renesas continue to expand their presence through partnerships with Asian device manufacturers. Recent developments show increasing competition in multi-protocol modules, with companies racing to combine Wi-Fi 6 and Bluetooth 5.3 functionality in single-chip solutions.

Consolidation activity has intensified, as evidenced by Infineon’s acquisition of Cypress Semiconductor, which strengthened its wireless portfolio. Smaller innovators like Ebyte and Hope Microelectronics maintain relevance through niche applications and customized solutions. The competitive environment continues to evolve with the emergence of AI-integrated wireless modules, creating new battlegrounds for market leadership.

List of Key 2.4G Wireless Module Manufacturers

- NXP Semiconductors (Netherlands)

- Texas Instruments (U.S.)

- Dialog Semiconductor (UK)

- Broadcom Inc. (U.S.)

- Realtek Semiconductor Corp. (Taiwan)

- Qualcomm Technologies, Inc. (U.S.)

- Nordic Semiconductor (Norway)

- Infineon Technologies (Germany)

- Denvel Intelligent Electronic (China)

- Advantech Co., Ltd. (Taiwan)

- Felicomm (China)

- Agilelight (U.S.)

- DreamLNK (China)

- Ebyte (China)

- Hope Microelectronics (China)

- Quectel Wireless Solutions (China)

- Espressif Systems (China)

Segment Analysis:

By Type

Wi-Fi Module Segment Dominates Due to High Adoption in IoT and Smart Devices

The market is segmented based on type into:

- Wi-Fi Module

- Subtypes: 802.11b/g/n, 802.11ac, and others

- Bluetooth Module

- Subtypes: Bluetooth Classic, Bluetooth Low Energy (BLE), and others

- Zigbee Module

- Others

By Application

Consumer Electronics Segment Leads Due to Increasing Demand for Smart Devices

The market is segmented based on application into:

- Consumer Electronics

- Subtypes: Smartphones, Wearables, Smart Home Devices, and others

- Industrial Automation

- Automotive

- Medical Devices

- Others

Regional Analysis: 2.4G Wireless Module Market

Asia-Pacific

The Asia-Pacific region dominates the global 2.4G wireless module market, accounting for over 40% of global revenue in 2024, led by China’s massive electronics manufacturing ecosystem and India’s growing IoT adoption. China alone contributes approximately 35% of the regional market share, driven by strong government support for smart city projects and 5G infrastructure development. While cost-competitive solutions using Bluetooth and Zigbee modules remain popular, there’s increasing demand for multi-protocol modules that combine Wi-Fi 6 capabilities. Japan and South Korea focus on high-performance modules for automotive and industrial applications, with Japanese manufacturers leading in low-power consumption designs.

North America

North America stands as the second-largest market for 2.4G wireless modules, valued at $2.1 billion in 2024, with the U.S. accounting for nearly 85% of regional demand. The market is characterized by stringent FCC regulations and rapid adoption of IoT in healthcare and smart home sectors. Companies like Qualcomm and Broadcom drive innovation in Wi-Fi 6/6E modules, while the region shows the highest penetration of Thread protocol modules for smart home ecosystems. Recent investments in industrial IoT (IIoT) and federal initiatives for smart manufacturing are accelerating demand for robust wireless modules with enhanced security features.

Europe

Europe maintains a strong position in the 2.4G wireless module market, particularly in industrial automation and automotive applications, with Germany, France, and the UK comprising 60% of regional consumption. The region shows the highest adoption rate of Zigbee 3.0 modules for smart home devices, supported by strong standardization efforts from the Connectivity Standards Alliance. Nordic Semiconductor leads in ultra-low-power Bluetooth solutions targeting medical wearables. Strict EU regulations on radio equipment (RED Directive) and emphasis on cybersecurity are shaping module certification processes, adding compliance costs but ensuring market quality.

Middle East & Africa

While still an emerging market, the MEA region shows the fastest growth potential (CAGR 17.5%) for 2.4G wireless modules, driven by smart city initiatives in UAE, Saudi Arabia, and selective African nations. Dubai’s smart city projects and South Africa’s IoT adoption in mining are key demand drivers. However, market growth faces challenges including limited local manufacturing, dependence on imports, and fragmented regulatory frameworks across countries. The region shows particular interest in long-range 2.4GHz solutions adaptable to harsh environmental conditions, with modules requiring wider temperature operating ranges than global averages.

South America

South America represents a nascent but growing market, with Brazil contributing over 50% of regional demand for 2.4G modules. Agricultural IoT applications and increasing smart meter deployments are creating demand for cost-effective wireless solutions. Economic volatility and currency fluctuations remain challenges, pushing manufacturers toward value-engineered module designs. The region shows growing preference for dual-mode Bluetooth/Wi-Fi modules that balance performance and cost, particularly in consumer electronics and retail automation segments. Local players are collaborating with Chinese module manufacturers to develop region-specific solutions.

Report Scope

This market research report provides a comprehensive analysis of the Global 2.4G Wireless Module market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 8,608 million in 2024 and is projected to reach USD 22,300 million by 2032, growing at a CAGR of 14.7%.

- Segmentation Analysis: Detailed breakdown by product type (Wi-Fi, Bluetooth, Zigbee, Others), application (Consumer Electronics, Industrial Automation, Automotive, Medical Devices, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China represent key growth markets.

- Competitive Landscape: Profiles of leading market participants including NXP Semiconductors, Texas Instruments, Qualcomm, Nordic Semiconductor, and Broadcom, covering their product portfolios, market share (top five players held approximately XX% in 2024), and strategic developments.

- Technology Trends & Innovation: Assessment of emerging wireless protocols, integration with IoT ecosystems, power efficiency improvements, and evolving communication standards.

- Market Drivers & Restraints: Evaluation of factors including growing IoT adoption, smart home demand, industrial automation trends, alongside challenges like spectrum congestion and regulatory compliance.

- Stakeholder Analysis: Strategic insights for module manufacturers, OEMs, system integrators, and investors regarding market opportunities and competitive positioning.

The research employs both primary and secondary methodologies, including expert interviews, manufacturer surveys, and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global 2.4G Wireless Module Market?

-> 2.4G Wireless Module market was valued at 8608 million in 2024 and is projected to reach US$ 22300 million by 2032, at a CAGR of 14.7% during the forecast period..

Which key companies operate in Global 2.4G Wireless Module Market?

-> Key players include NXP Semiconductors, Texas Instruments, Qualcomm, Broadcom, Nordic Semiconductor, Infineon, and Realtek, among others.

What are the key growth drivers?

-> Key growth drivers include IoT proliferation, smart home adoption, industrial automation trends, and increasing demand for wireless medical devices.

Which region dominates the market?

-> Asia-Pacific shows the highest growth potential, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include multi-protocol modules, ultra-low power designs, AI-enabled wireless solutions, and enhanced security features.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...