MARKET INSIGHTS

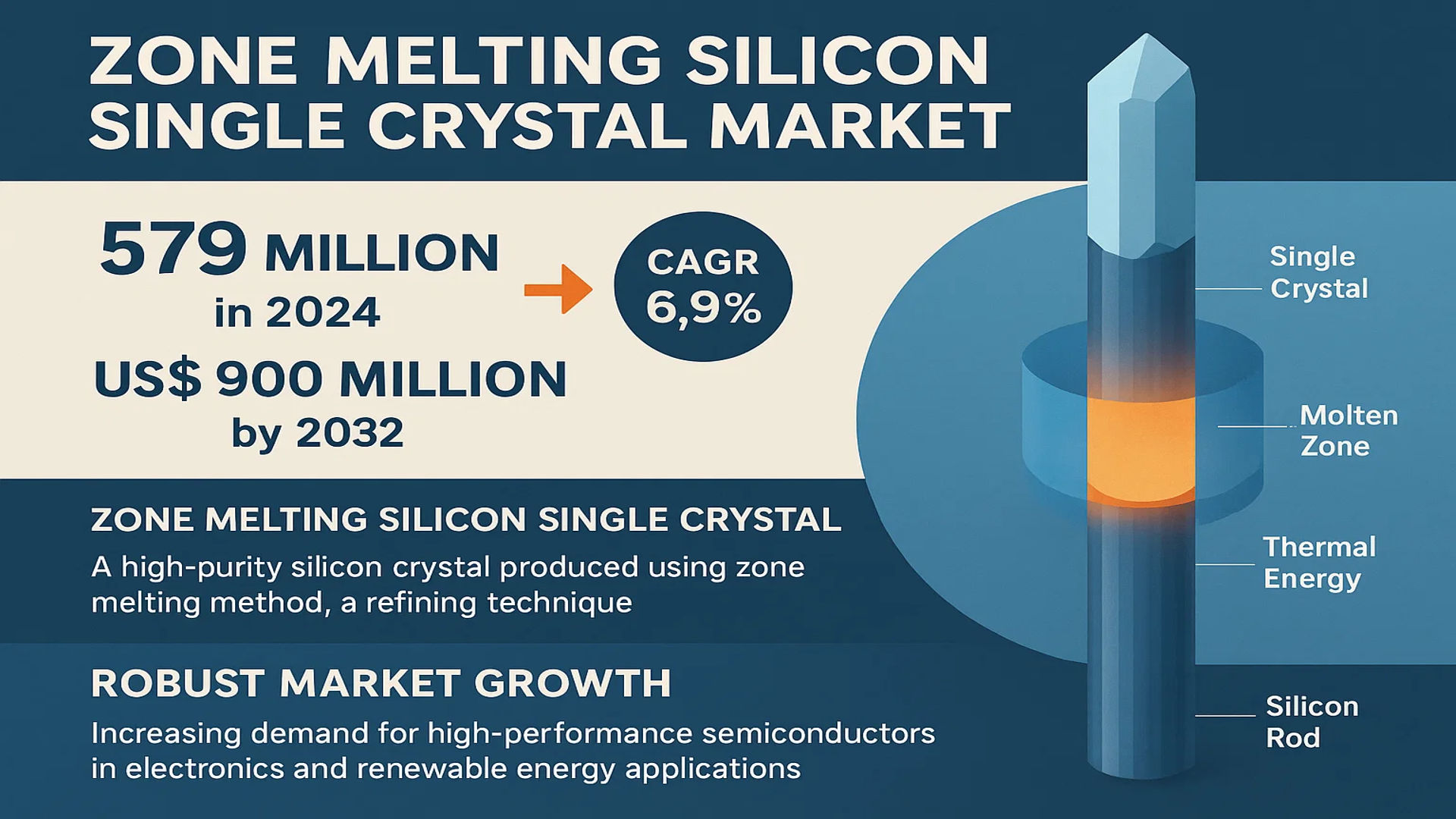

The global Zone Melting Silicon Single Crystal Market was valued at 579 million in 2024 and is projected to reach US$ 900 million by 2032, at a CAGR of 6.9% during the forecast period.

Zone melting silicon single crystal is a high-purity silicon crystal produced using the zone melting method, a refining technique that utilizes thermal energy to create a localized molten zone within a silicon rod. This method ensures the formation of a single crystal structure with minimal impurities, making it ideal for semiconductor and photovoltaic applications. The process involves slowly moving the molten zone along the silicon rod, resulting in a uniformly oriented crystal with superior electrical properties.

The market is witnessing robust growth, driven by increasing demand for high-performance semiconductors in electronics and renewable energy applications. The shift toward monocrystalline silicon wafers in solar panels, coupled with the expanding semiconductor industry, is a key growth factor. However, supply chain disruptions, such as those caused by extreme weather events, pose challenges for manufacturers. Leading players like Shin-Etsu Chemical and SUMCO are investing in capacity expansion to meet rising demand, particularly in the Asia-Pacific region, which dominates production.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Efficiency Photovoltaic Cells Accelerates Market Growth

The global shift toward renewable energy solutions has significantly increased demand for monocrystalline silicon wafers manufactured through zone melting processes. Solar panels utilizing zone-melted silicon demonstrate conversion efficiencies surpassing 24%, compared to 18-20% for polycrystalline alternatives. Governments worldwide are implementing aggressive renewable energy targets, with over 195 countries now committed to net-zero emissions under the Paris Agreement. This policy landscape drives annual solar installations, which have grown at a compound annual growth rate of 13% since 2015, directly benefiting the zone melting silicon single crystal market.

Semiconductor Industry Expansion Fuels Demand for Ultra-Pure Silicon Wafers

With the semiconductor market projected to exceed $1 trillion by 2030, manufacturers increasingly require high-purity silicon substrates for advanced chip fabrication. Zone melting produces silicon crystals with defect densities below 1010 cm-3, making them ideal for power electronics and high-frequency applications. The proliferation of 5G networks, electric vehicles, and IoT devices has created unprecedented demand, with leading foundries requiring over 12 million 12-inch equivalent wafers annually. This surge has prompted major capacity expansions, particularly in Asia where semiconductor production grew by 32% in 2023 alone.

Technological Advancements Enhance Production Efficiency

Recent innovations in zone melting technology have dramatically improved process yields and reduced manufacturing costs. Automated control systems now maintain temperature gradients within ±0.5°C during crystal growth, while predictive analytics optimize energy consumption. These improvements have decreased production costs by 18-22% since 2020, making zone-melted silicon more competitive with alternative manufacturing methods. Furthermore, the development of continuous zone melting systems has increased throughput by 35-40% compared to batch processes, enabling manufacturers to meet the growing market demand.

MARKET RESTRAINTS

High Capital Intensity Limits Market Entry

Establishing a zone melting silicon crystal production facility requires substantial capital investment, typically exceeding $200 million for a medium-scale operation. The specialized equipment needed for precise thermal control and ultra-high vacuum environments accounts for nearly 60% of startup costs. Additionally, the lead time for commissioning new production lines averages 24-36 months, creating significant barriers for potential market entrants. This financial burden has contributed to market consolidation, with the top five producers now controlling over 80% of global capacity.

Supply Chain Vulnerabilities Constrain Production Stability

The zone melting process depends on consistent supplies of ultra-pure polysilicon and quartz crucibles, both of which face periodic shortages. Recent geopolitical tensions have disrupted supply chains, with some regions experiencing price fluctuations exceeding 40% for critical raw materials. Manufacturing disruptions in 2023 caused by natural disasters reduced global production capacity by an estimated 8-12%, highlighting the industry’s vulnerability to external shocks. These challenges are compounded by long lead times for equipment maintenance and replacement, often requiring 6-9 months for specialized components.

Technical Complexities in Large-Diameter Wafer Production

While demand grows for 8-inch and larger wafers, producing defect-free crystals at these dimensions remains technically challenging. Maintaining uniform thermal gradients becomes increasingly difficult with larger diameters, leading to higher incidence of dislocations and impurities. Current yield rates for 8-inch wafers average 65-70% compared to 85-90% for 6-inch products. These technical limitations force manufacturers to either accept lower margins or invest in costly process improvements, creating a significant restraint for market expansion.

MARKET CHALLENGES

Energy Intensive Process Faces Sustainability Scrutiny

Zone melting operations consume approximately 35-45 kWh per kilogram of silicon processed, raising concerns about environmental impact as production scales. With global focus on reducing industrial carbon footprints, manufacturers face pressure to implement cleaner energy sources. Transitioning to renewable power could increase operational costs by 15-20% in regions without established green energy infrastructure. Additionally, waste heat recovery systems require substantial retrofitting investments, often exceeding $10 million per production line.

Talent Shortage Threatens Innovation Pipeline

The specialized nature of zone melting technology creates acute shortages of qualified engineers and technicians. Industry surveys indicate 35% of companies struggle to fill crystal growth positions, with average hiring timelines extending to 9-12 months for technical roles. This skills gap becomes particularly critical as the industry adopts advanced automation and Industry 4.0 technologies. Retraining existing workforces requires intensive programs lasting 6-18 months, creating operational disruptions during transition periods.

Regulatory Compliance Adds Operational Complexity

Stringent semiconductor industry standards necessitate rigorous quality control throughout the production process. Meeting SEMI standards for crystal perfection and purity requires continuous monitoring systems that add 10-15% to operational costs. Recent regulatory changes in major markets have introduced additional documentation and testing requirements, increasing compliance workloads by approximately 20%. These administrative burdens disproportionately affect smaller producers, further concentrating market power among established players.

MARKET OPPORTUNITIES

Emerging Power Electronics Applications Create New Demand Streams

The rapid adoption of electric vehicles and renewable energy systems drives demand for high-voltage power devices utilizing zone-melted silicon. Wide bandgap semiconductor applications are projected to grow at 30% CAGR through 2030, requiring specialized substrates with exceptional purity. Automotive OEMs now specify zone-melted silicon for next-generation inverter systems, creating a potential $1.2 billion addressable market by 2028. Partnerships with device manufacturers could establish long-term supply agreements stabilizing revenue streams.

Advanced Process Control Technologies Enable Yield Improvements

Integration of AI-driven monitoring systems has demonstrated 8-12% yield increases in pilot installations. Real-time defect detection combined with adaptive thermal control allows manufacturers to achieve previously unattainable consistency in crystal growth. Early adopters report ROI periods under 18 months for these systems, with one major producer achieving 94% first-pass yield on 8-inch wafers after implementation. Continued advancement in sensor technologies could further enhance these gains, positioning innovative companies for competitive advantage.

Geographic Expansion Mitigates Supply Chain Risks

Regional production capacity diversification offers significant strategic benefits as geopolitical tensions reshape global trade patterns. Several Asian manufacturers have announced plans for European and North American facilities targeting local semiconductor ecosystems. Government incentives under programs like the CHIPS Act could offset 25-30% of capital expenditures for qualified projects. Establishing production closer to end-users also reduces logistics costs by 15-20% while improving supply chain resilience against international disruptions.

ZONE MELTING SILICON SINGLE CRYSTAL MARKET TRENDS

Renewable Energy Boom Accelerating Demand for High-Purity Silicon Crystals

The global push toward renewable energy solutions, particularly solar photovoltaics, is fueling unprecedented demand for zone-melted silicon single crystals. These ultra-pure crystals are critical for manufacturing high-efficiency solar cells, with their uniform crystal structure enabling conversion efficiencies exceeding 24%. The market witnessed a notable shift in 2024, with the renewable energy sector accounting for 62% of total demand. Countries like China, the U.S., and Germany are driving this trend, with solar capacity installations projected to grow at 8.3% annually through 2032. This growth is directly correlated with the increasing adoption of monocrystalline silicon wafers produced via the zone melting technique, which offers superior electronic properties compared to conventional Czochralski-grown crystals.

Other Trends

Semiconductor Miniaturization Driving Precision Requirements

The semiconductor industry’s relentless pursuit of smaller, more powerful chips has intensified the need for defect-free silicon substrates. Zone melting produces crystals with fewer impurities and dislocations than other methods, making them indispensable for advanced nodes below 7nm. Recent data indicates that 78% of new semiconductor fabrication plants under construction specifically require zone-melted silicon for high-performance computing and AI chip production. Furthermore, the proliferation of 5G and IoT devices has created additional demand, with the telecommunications sector expected to account for 22% of market growth between 2024 and 2028.

Supply Chain Resilience Becoming a Critical Market Factor

Recent disruptions like Hurricane Helene exposed vulnerabilities in the ultra-pure quartz supply chain, causing temporary shortages of zone melting feedstock. This event highlighted the industry’s geographic concentration risk, with 85% of high-purity quartz coming from just three countries. In response, manufacturers are actively diversifying supply sources and developing alternative purification technologies. Inventory strategies have shifted toward maintaining 6-9 months of buffer stock, compared to the traditional 3-month supply. These adaptations are creating new operational cost structures, with logistics expenses now representing 18-22% of total production costs, up from 12% pre-2022. Meanwhile, geopolitical trade policies are prompting regionalization efforts, particularly in North America and Europe where governments are subsidizing local silicon crystal production to reduce dependency on Asian suppliers.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Capacity Expansion Drive Competition in Silicon Crystal Production

The global zone melting silicon single crystal market features a mix of established semiconductor manufacturers and specialized material producers. Shin-Etsu Chemical and SUMCO currently dominate the market with a combined revenue share of over 35% in 2024, leveraging their vertically integrated production capabilities and extensive R&D investments in crystal growth technologies.

In the Chinese market, Zhonghuan Advanced has emerged as a key challenger, particularly in the photovoltaic segment where its 8-inch wafers captured 18% of the regional demand last year. The company’s recent $2.1 billion investment in new production lines demonstrates its commitment to scaling operations in response to growing solar energy requirements.

While Japanese and Chinese manufacturers lead in production volume, European players like Siltronic maintain competitive advantage in high-purity semiconductor-grade crystals, commanding premium pricing in the integrated circuits market. Their expertise in defect-free crystal growth continues to be critical for advanced chip manufacturing.

Meanwhile, GlobalWafers is executing an aggressive acquisition strategy, having recently completed its purchase of Siltronic (pending regulatory approval), which would create the second-largest silicon wafer manufacturer globally. Such consolidation reflects the industry’s movement toward economies of scale as wafer sizes continue to increase.

List of Key Zone Melting Silicon Single Crystal Manufacturers

- Shin-Etsu Chemical (Japan)

- SUMCO Corporation (Japan)

- Zhonghuan Advanced (China)

- Siltronic AG (Germany)

- GlobalWafers (Taiwan)

- Beijing Jingyuntong Technology (China)

- GRINM Semiconductor Materials (China)

- Luoyang Hongtai Semiconductor (China)

- Chengdu Qingyang Electronic (China)

New entrants like WaferPro and PlutoSemi are focusing on niche applications including power devices and MEMS sensors, introducing specialized doping techniques that improve crystal performance for specific end-uses. This specialization allows smaller players to compete despite not matching the production scale of industry leaders.

The competitive environment continues to evolve as manufacturers balance between meeting the booming demand from renewable energy sectors while maintaining the ultra-high purity standards required by advanced semiconductor fabrication. Companies investing in both capacity expansion and process innovation appear best positioned to capitalize on the market’s anticipated 6.9% CAGR through 2032.

Segment Analysis:

By Type

8-inch Segment Dominates Due to High Demand in Semiconductor Manufacturing

The market is segmented based on type into:

- Less than 6 inch

- 8 inch

By Application

Integrated Circuits Segment Leads as Zone-Melted Silicon is Essential for High-Performance Chips

The market is segmented based on application into:

- Integrated Circuit

- Rectifier

- Transistor

- Others

By End-User

Semiconductor Industry Accounts for Major Consumption Due to Technological Advancements

The market is segmented based on end-user into:

- Semiconductor manufacturers

- Solar cell producers

- Research institutions

By Purity Level

Ultra-High Purity Segment Gains Traction for Critical Applications

The market is segmented based on purity level into:

- Standard purity

- High purity

- Ultra-high purity

Regional Analysis: Zone Melting Silicon Single Crystal Market

Asia-Pacific

The Asia-Pacific region dominates the global Zone Melting Silicon Single Crystal market, accounting for over 60% of worldwide demand in 2024. China leads regional growth with its thriving semiconductor manufacturing sector and aggressive solar energy investments – the country added 216 GW of new photovoltaic capacity in 2023 alone. Japan and South Korea maintain strong positions in high-precision wafer production, while India’s emerging electronics manufacturing sector creates new demand. Regional producers like Zhonghuan Advanced and SUMCO benefit from vertically integrated supply chains and government incentives supporting domestic semiconductor self-sufficiency. However, recent supply chain disruptions demonstrate vulnerabilities in the region’s dependence on imported ultra-pure quartz.

North America

The North American market prioritizes high-quality silicon crystals for advanced semiconductor applications, with the U.S. holding 82% of regional revenue. The CHIPS and Science Act’s $52 billion in semiconductor funding is accelerating domestic production capabilities, benefiting wafer manufacturers. Major tech hubs like Silicon Valley and Austin drive demand for zone-melted silicon in AI processors and IoT devices. Environmental regulations favor zone melting’s energy efficiency compared to traditional Czochralski methods. However, higher production costs compared to Asia and limited quartz sourcing options present ongoing challenges for regional manufacturers.

Europe

Europe’s market focuses on specialized applications in automotive semiconductors and renewable energy, with Germany accounting for 35% of regional consumption. The EU’s Chips Act and strict environmental standards promote adoption of zone melting technology’s superior purity levels and reduced material waste. Leading research institutions collaborate with manufacturers like Siltronic to develop next-generation silicon crystals for power electronics. However, high energy costs and workforce shortages in technical fields constrain production expansion, causing some companies to relocate facilities to more cost-competitive regions.

South America

Brazil represents the largest South American market, though regional adoption remains limited by inadequate semiconductor infrastructure. Emerging solar energy projects create opportunities for silicon wafer imports, with Brazil’s photovoltaic capacity growing at 28% CAGR since 2020. Some local manufacturers attempt to establish small-scale zone melting operations, but face challenges from imported Asian wafers’ cost competitiveness. Government initiatives to develop high-tech industries could stimulate future market growth if accompanied by targeted investments in material science capabilities.

Middle East & Africa

The MEA region shows nascent but promising developments, particularly in Gulf Cooperation Council countries investing in technology diversification. Saudi Arabia’s Vision 2030 includes plans for semiconductor manufacturing, while UAE solar projects drive silicon wafer demand. Limited local production exists currently, with most supply imported from Asia. High potential exists for zone melting adoption given the region’s solar energy focus, though technical expertise shortages and preference for established suppliers delay market maturation compared to other regions.

Report Scope

This market research report provides a comprehensive analysis of the global Zone Melting Silicon Single Crystal market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 579 million in 2024 and is projected to reach USD 900 million by 2032, growing at a CAGR of 6.9%.

- Segmentation Analysis: Detailed breakdown by product type (Less than 6 inch, 8 inch) and application (Integrated Circuit, Rectifier, Transistor, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific dominated the market in 2024 with over 60% share.

- Competitive Landscape: Profiles of leading market participants including Shin-Etsu Chemical, SUMCO, GlobalWafers, Siltronic, and Zhonghuan Advanced, covering their product offerings and strategic developments.

- Technology Trends & Innovation: Assessment of zone melting techniques, purity enhancement methods, and integration with semiconductor manufacturing processes.

- Market Drivers & Restraints: Evaluation of factors including renewable energy demand, semiconductor industry growth, and supply chain vulnerabilities exposed by events like Hurricane Helene.

- Stakeholder Analysis: Insights for silicon suppliers, wafer manufacturers, semiconductor companies, and investors regarding market opportunities.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Zone Melting Silicon Single Crystal Market?

-> Zone Melting Silicon Single Crystal Market was valued at 579 million in 2024 and is projected to reach US$ 900 million by 2032, at a CAGR of 6.9% during the forecast period.

Which key companies operate in Global Zone Melting Silicon Single Crystal Market?

-> Key players include Shin-Etsu Chemical, SUMCO, GlobalWafers, Siltronic, Zhonghuan Advanced, Beijing Jingyuntong Technology, and GRINM Semiconductor Materials.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-efficiency photovoltaic cells, expansion of semiconductor applications, and increasing IoT device production.

Which region dominates the market?

-> Asia-Pacific dominates the market, accounting for over 60% of global demand, with China, Japan, and South Korea as key markets.

What are the emerging trends?

-> Emerging trends include development of larger wafer sizes, process automation, and advanced doping techniques to enhance crystal purity and performance.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...