MARKET INSIGHTS

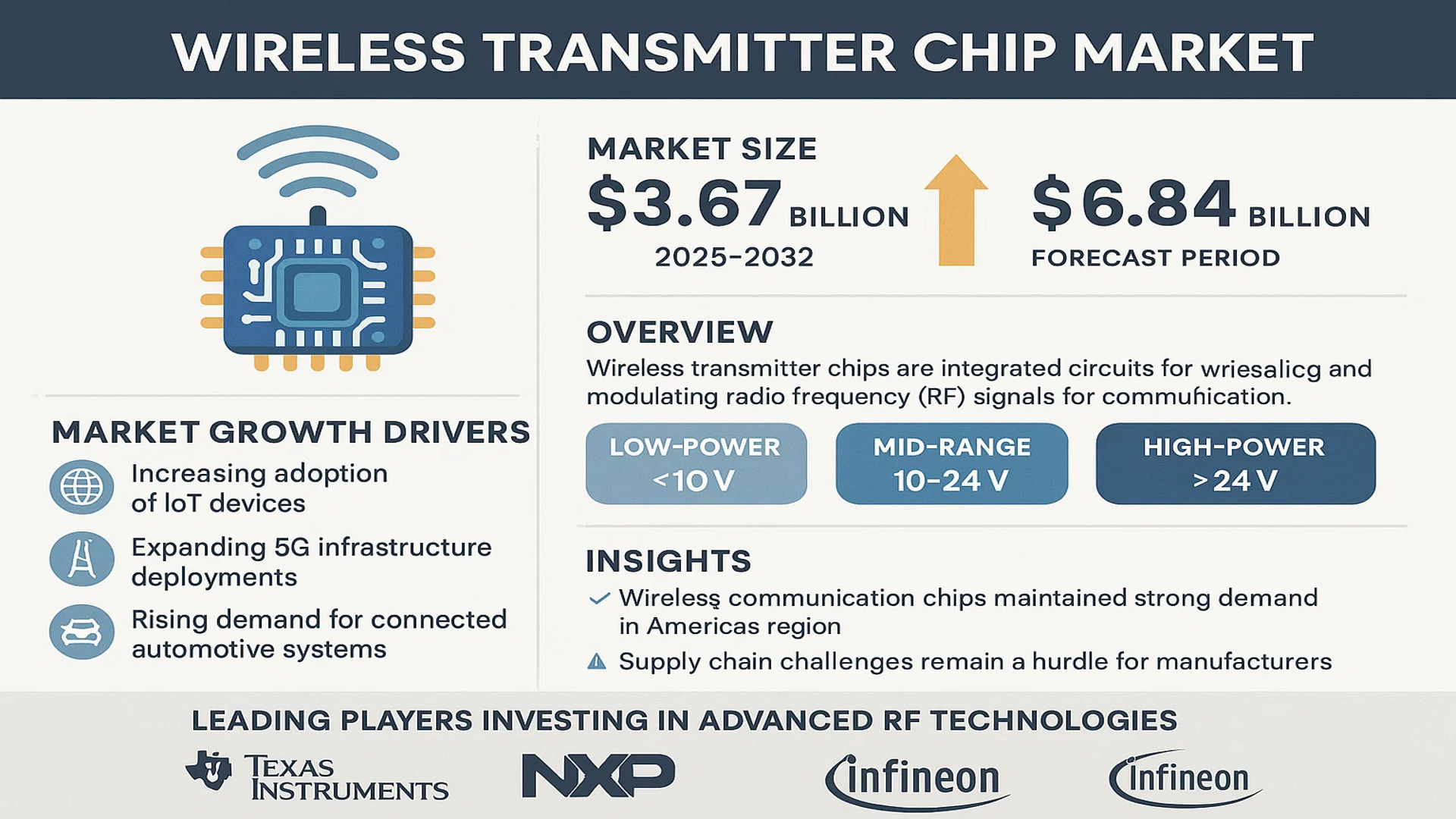

The global Wireless Transmitter Chip Market size was valued at US$ 3.67 billion in 2024 and is projected to reach US$ 6.84 billion by 2032, at a CAGR of 8.0% during the forecast period 2025-2032.

Wireless transmitter chips are integrated circuits designed to generate and modulate radio frequency (RF) signals for wireless communication. These chips typically incorporate an oscillator, modulator, amplifier, and other supporting circuits to enable data transmission across various wireless protocols, including Wi-Fi, Bluetooth, Zigbee, and cellular technologies. Key variants include low-power (<10V), mid-range (10-24V), and high-power (>24V) transmitter chips catering to different application requirements.

The market growth is primarily driven by increasing adoption of IoT devices, expanding 5G infrastructure deployments, and rising demand for connected automotive systems. While the semiconductor industry faced moderated growth in 2022 (4.4% overall according to WSTS), wireless communication chips maintained strong demand, particularly in the Americas region which saw 17% year-over-year growth. However, supply chain challenges and fluctuating raw material costs continue to present hurdles for manufacturers. Leading players like Texas Instruments, NXP, and Infineon are investing in advanced RF technologies to capitalize on emerging opportunities in smart cities and industrial IoT applications.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of IoT and Smart Devices Accelerates Wireless Transmitter Chip Demand

The exponential growth of IoT-connected devices is fundamentally transforming the wireless transmitter chip landscape. With over 15 billion active IoT devices worldwide and projections indicating 29 billion connections by 2030, this sector represents a massive growth vector for wireless transmitter solutions. These chips serve as critical enablers for device connectivity across smart homes, industrial automation, and healthcare monitoring systems. The transition to 5G networks, offering lower latency and higher bandwidth, further amplifies this demand as it enables more complex IoT applications. Devices ranging from simple sensors to advanced wearables all require compact, power-efficient transmitter solutions to facilitate seamless wireless communication.

Automotive Connectivity Revolution Drives Component Innovation

Modern vehicle architectures increasingly rely on wireless transmitter chips for multiple applications, with the automotive semiconductor market projected to reach $80 billion by 2026. Key growth areas include vehicle-to-everything (V2X) communication systems, tire pressure monitoring, keyless entry, and in-vehicle infotainment. The rollout of autonomous driving technologies particularly benefits from advanced RF transmitter solutions that enable real-time data exchange between vehicles and infrastructure. Regulations mandating safety features like automatic emergency calling (eCall) in many regions have further institutionalized the need for reliable wireless communication modules in automotive designs.

Additionally, the electrification of vehicles creates new opportunities as electric powertrain monitoring systems increasingly incorporate wireless sensor networks. This eliminates wiring complexity while enabling real-time battery management and performance optimization.

MARKET RESTRAINTS

Semiconductor Shortages and Supply Chain Volatility Limit Market Expansion

The wireless transmitter chip market faces significant constraints from ongoing semiconductor supply chain disruptions. While the overall chip market grew 4.4% in 2022, certain categories experienced double-digit declines due to production bottlenecks. The industry continues grappling with wafer fab capacity limitations, particularly for mature process nodes commonly used in RF transmitter designs. Geopolitical tensions affecting semiconductor trade between major regions exacerbate these challenges, with some countries imposing export controls on critical manufacturing equipment.

Additional Constraints

Design Complexity

Developing wireless transmitter chips that support multiple protocols (Bluetooth, Wi-Fi, cellular) while minimizing power consumption requires substantial R&D investment. This raises barriers to entry for smaller players and extends development cycles for new product introductions. The average design cycle for complex RFICs can exceed 18 months due to rigorous certification requirements across multiple regulatory jurisdictions.

Cost Pressure

Intense competition from Asian semiconductor manufacturers drives aggressive price erosion, particularly in consumer applications. Margins for standard wireless connectivity solutions have compressed significantly, forcing vendors to differentiate through integration or value-added features. This economic pressure discourages investment in next-generation transmitter technologies with longer development horizons.

MARKET CHALLENGES

Spectrum Congestion and Regulatory Hurdles Complicate Product Development

As wireless networks proliferate, spectrum scarcity presents growing technical challenges for transmitter chip designers. The crowded RF environment requires increasingly sophisticated interference mitigation techniques while maintaining strict compliance with regional frequency allocations. Recent regulatory changes, such as the FCC’s 6GHz band reallocation for unlicensed use in the U.S., illustrate both the opportunities and complexities facing wireless chip manufacturers. Companies must navigate disparate global certification processes that can delay time-to-market for new products.

Additionally, power consumption requirements create design trade-offs between range, data rate, and battery life—particularly for IoT edge devices expected to operate for years on small batteries. Thermal management becomes another critical challenge as transmitter power amplifiers approach their efficiency limits in compact form factors.

MARKET OPPORTUNITIES

Emerging Wireless Standards Open New Application Verticals

The introduction of advanced wireless protocols creates significant growth avenues for transmitter chip vendors. Technologies like Wi-Fi 6E (extending into 6GHz spectrum), ultra-wideband (UWB) for precision ranging, and Matter for smart home interoperability each enable new use cases requiring specialized transmitter solutions. The healthcare sector presents particular promise, with medical body area networks and remote patient monitoring systems driving demand for reliable, low-power wireless links. Industrial IoT applications in predictive maintenance and asset tracking similarly benefit from emerging long-range, low-power protocols like LoRa and NB-IoT.

Furthermore, the integration of AI capabilities directly into wireless transmitter chips represents a transformative opportunity. Edge-based signal processing can optimize transmission parameters in real-time, improving spectral efficiency and battery life while reducing latency. Several leading semiconductor firms have already introduced machine learning-enhanced wireless SoCs that adapt to changing RF conditions without host processor intervention.

WIRELESS TRANSMITTER CHIP MARKET TRENDS

5G and IoT Expansion Driving Wireless Transmitter Chip Demand

The proliferation of 5G networks and IoT-connected devices is significantly boosting the wireless transmitter chip market. With over 1.3 billion 5G subscriptions globally as of 2023, telecom operators continue expanding infrastructure, requiring advanced transmitter chips that support higher frequencies up to mmWave bands (24-100 GHz). Simultaneously, the rapid adoption of IoT devices – projected to exceed 29 billion connected endpoints by 2027 – necessitates low-power, high-efficiency chips for sensors and edge devices. Manufacturers are responding with innovative solutions integrating beamforming capabilities and adaptive frequency hopping to optimize signal integrity across diverse use cases.

Other Trends

Automotive Connectivity Revolution

The automotive sector is emerging as a major growth driver, with modern vehicles incorporating 50-150 wireless transmitter chips for applications ranging from tire pressure monitoring to autonomous driving systems. The transition towards V2X (Vehicle-to-Everything) communication standards is particularly impactful, requiring chips that maintain stable connections at speeds exceeding 200 km/h. Leading manufacturers are developing specialized automotive-grade chips with extended temperature ranges (-40°C to +125°C) and enhanced EMI resistance to meet stringent automotive safety requirements.

Miniaturization and Power Efficiency Innovations

The industry is witnessing remarkable progress in chip miniaturization and power optimization. Cutting-edge transmitter chips now integrate power amplifier, oscillator and modulation circuits in packages smaller than 2mm² while achieving power consumption below 1mW in standby mode. These advancements are critical for wearables and medical implants, where space and battery life are at a premium. Recent breakthroughs in energy harvesting technologies are enabling self-powered wireless sensors, further expanding application possibilities in industrial IoT and smart infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Semiconductor Manufacturers Drive Innovation in Wireless Transmitter Chips

The global wireless transmitter chip market features a competitive landscape dominated by established semiconductor giants and specialized manufacturers. Texas Instruments and Analog Devices collectively hold over 30% market share in 2024, leveraging their analog and mixed-signal expertise to deliver high-performance RF solutions. These companies benefit from decades of R&D investment and extensive patent portfolios covering wireless communication technologies.

NXP Semiconductors has emerged as a key contender in automotive wireless applications, capturing significant market share through its collaboration with major automakers for vehicle-to-everything (V2X) communication systems. Meanwhile, Infineon Technologies has strengthened its position through strategic acquisitions, including Cypress Semiconductor, enhancing its RF chip capabilities for industrial IoT applications.

The market also features strong competition from Asian manufacturers. ROHM Semiconductor has gained traction in low-power wireless solutions for consumer electronics, while Renesas Electronics continues to expand its wireless portfolio through partnerships with IoT platform providers. These companies are actively developing energy-efficient transmitter chips to meet growing demand for battery-operated devices.

Recent industry developments show a trend toward consolidation, with Microchip Technology acquiring several smaller RF specialists to bolster its wireless offerings. At the same time, STMicroelectronics and Broadcom are investing heavily in next-generation Wi-Fi 6/6E and 5G transmitter chips, positioning themselves for future market growth.

List of Key Wireless Transmitter Chip Manufacturers

- Texas Instruments (U.S.)

- Analog Devices (U.S.)

- NXP Semiconductors (Netherlands)

- Infineon Technologies (Germany)

- ROHM Semiconductor (Japan)

- Renesas Electronics (Japan)

- Microchip Technology (U.S.)

- STMicroelectronics (Switzerland)

- Broadcom Inc. (U.S.)

- ON Semiconductor (U.S.)

- Maxim Integrated (U.S.)

- Hoperf (China)

Segment Analysis:

By Type

10-24V Segment Holds Major Share Due to Wide Compatibility with Consumer Electronics and IoT Devices

The wireless transmitter chip market is segmented based on voltage range into:

- Less than 10V

- 10-24V

- Above 24V

By Application

Wearable Electronic Devices Lead Market Adoption Driven by Smartwatch and Fitness Tracker Demand

The market is segmented based on application into:

- Wearable Electronic Devices

- Medical Devices

- Automobile Devices

- Others

By Communication Technology

RF Transmitter Chips Dominate with High Penetration in Wireless Connectivity Solutions

The market is segmented by communication technology into:

- RF Transmitter Chips

- Bluetooth/Wi-Fi Chips

- Cellular Chips

- Others

By End-User

Consumer Electronics Sector Accounts for Largest Adoption Due to IoT Expansion

The market is segmented by end-user into:

- Consumer Electronics

- Automotive

- Healthcare

- Industrial

Regional Analysis: Wireless Transmitter Chip Market

Asia-Pacific

The Asia-Pacific region dominates the global wireless transmitter chip market, accounting for the largest revenue share in 2024. This leadership position stems from China’s aggressive semiconductor manufacturing expansion and the presence of major consumer electronics manufacturers. Countries like South Korea and Taiwan contribute significantly through their advanced foundry capabilities. The region benefits from high demand for IoT devices, with China alone projected to have over 800 million 5G connections by 2025. However, recent semiconductor sales declines in Asia (-2.0% YoY in 2022) indicate sensitivity to global economic conditions, though long-term growth remains strong due to increasing automation and smart device penetration across industries.

North America

North America represents the second-largest market, driven by technological innovation and substantial R&D investments. The U.S., with its concentration of semiconductor giants like Texas Instruments and Broadcom, leads in advanced chip design and wireless protocol development. The region shows particular strength in high-performance transmitter chips for automotive and medical applications, supported by stringent FCC regulations that push for efficient spectrum utilization. While inflation has impacted consumer electronics demand, enterprise-level adoption of Industry 4.0 technologies and government initiatives like the CHIPS Act continue to stimulate market growth despite short-term fluctuations.

Europe

Europe maintains steady demand for wireless transmitter chips, particularly for industrial and automotive applications. The region’s emphasis on secure, energy-efficient connectivity solutions drives adoption in smart city deployments and Industry 4.0 applications. Germany remains the technology hub with its strong automotive sector – a major consumer of transmitter chips for vehicle-to-everything (V2X) communication. While EU regulations ensure high quality standards, they also increase time-to-market for new chip designs. The region shows particular interest in sub-GHz frequency chips for industrial IoT due to their superior range and penetration characteristics in manufacturing environments.

South America

South America represents an emerging market with growing but uneven adoption of wireless technologies. Brazil leads in regional demand, particularly for consumer electronics and basic IoT applications, while industrial adoption remains limited by infrastructure challenges. Economic instability has slowed investments in advanced semiconductor solutions, with most chips imported rather than produced locally. However, increasing smartphone penetration and gradual 5G network rollouts are creating opportunities for simple, cost-effective transmitter chips in the consumer segment, though complex designs face adoption barriers due to price sensitivity.

Middle East & Africa

This region shows the highest growth potential but from a smaller base, with adoption centered around smart city initiatives in GCC countries and cellular infrastructure expansion. The UAE and Saudi Arabia drive demand through large-scale digital transformation projects requiring robust wireless connectivity solutions. Africa presents a more fragmented picture, with South Africa and Nigeria showing pockets of demand offset by infrastructure limitations. While not yet a significant market for advanced transmitter chips, the region’s developing telecommunications sector promises long-term opportunities, particularly for energy-efficient designs suited to off-grid applications.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Wireless Transmitter Chip markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Wireless Transmitter Chip market was valued at US$ 3.67 billion in 2024 and is projected to reach US$ 6.84 billion by 2032, growing at a CAGR of 8.0% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (Less than 10V, 10-24V, Above 24V), application (Wearable Electronic Devices, Medical Devices, Automobile Devices, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with Asia-Pacific accounting for 42% of global market share in 2024.

- Competitive Landscape: Profiles of leading market participants including Texas Instruments, NXP Semiconductors, STMicroelectronics, Infineon Technologies, and Analog Devices, covering their product portfolios, market strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies including ultra-low-power wireless solutions, integration with IoT platforms, and advanced modulation techniques for improved signal integrity.

- Market Drivers & Restraints: Evaluation of growth drivers such as rising demand for connected devices and 5G infrastructure, along with challenges like semiconductor supply chain constraints and geopolitical factors affecting raw material availability.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, OEMs, system integrators, and investors regarding market opportunities and the evolving wireless technology ecosystem.

The research methodology combines primary interviews with industry experts and analysis of verified market data from authoritative sources to ensure the accuracy and reliability of findings.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Wireless Transmitter Chip Market?

->Wireless Transmitter Chip Market size was valued at US$ 3.67 billion in 2024 and is projected to reach US$ 6.84 billion by 2032, at a CAGR of 8.0% during the forecast period 2025-2032.

Which key companies operate in Global Wireless Transmitter Chip Market?

-> Key players include Texas Instruments, NXP Semiconductors, STMicroelectronics, Infineon Technologies, Analog Devices, and Broadcom, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption of IoT devices, 5G network deployments, and increasing demand for wireless connectivity in automotive and medical applications.

Which region dominates the market?

-> Asia-Pacific holds the largest market share at 42%, driven by strong electronics manufacturing in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include integration of AI in wireless chips, ultra-low-power designs for wearables, and development of mmWave solutions for 5G applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...