MARKET INSIGHTS

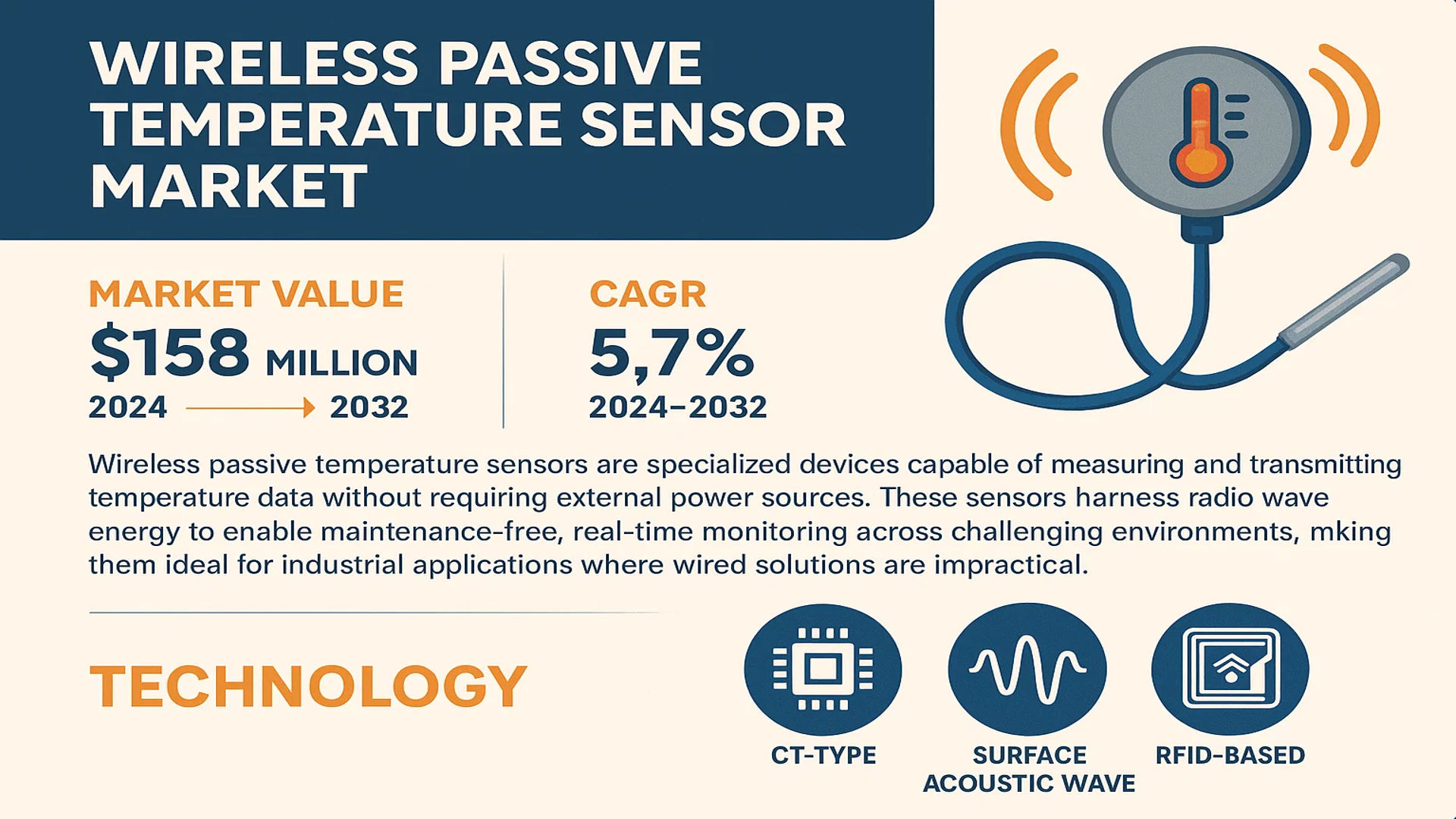

The global Wireless Passive Temperature Sensor Market was valued at 158 million in 2024 and is projected to reach US$ 229 million by 2032, at a CAGR of 5.7% during the forecast period.

Wireless passive temperature sensors are specialized devices capable of measuring and transmitting temperature data without requiring external power sources. These sensors harness radio wave energy to enable maintenance-free, real-time monitoring across challenging environments, making them ideal for industrial applications where wired solutions are impractical. The technology includes CT-type, surface acoustic wave, and RFID-based variants, each serving distinct operational needs.

The market growth is driven by increasing industrial automation and stringent safety regulations, particularly in sectors like electrical infrastructure and petrochemical plants. The U.S. dominates regional adoption with advanced IoT integration, while China’s market expands rapidly due to smart manufacturing initiatives. Key players like Texas Instruments, Siemens, and Schneider Electric are accelerating innovation, with recent developments focusing on extended-range sensors for extreme temperature monitoring in energy applications.

MARKET DYNAMICS

MARKET DRIVERS

Growing Industrial Automation Trends Fuel Demand for Wireless Passive Temperature Sensors

The rapid adoption of Industry 4.0 technologies across manufacturing sectors is significantly driving the wireless passive temperature sensor market. With the global industrial automation market witnessing double-digit growth annually, there is increasing demand for maintenance-free monitoring solutions that integrate seamlessly with IoT-enabled smart factories. These sensors eliminate wiring costs while providing real-time temperature data critical for predictive maintenance, process optimization, and quality control. Particularly in extreme environments like foundries or chemical plants where wired solutions are impractical, wireless passive sensors offer reliable performance with no battery replacement requirements.

Industrial giants are actively deploying these solutions as part of digital transformation initiatives. Recent technological advancements have improved sensor accuracy to ±0.5°C while extending operational ranges beyond 200°C, making them viable for previously inaccessible applications. The expanding smart factory ecosystem, projected to reach over $600 billion globally by 2030, presents substantial growth opportunities for wireless temperature monitoring solutions.

Energy Sector Modernization Creates Strong Market Pull

The global energy sector’s modernization efforts are creating robust demand for wireless passive temperature monitoring solutions. Electrical substations, power generation facilities, and transmission infrastructure increasingly incorporate these sensors for critical equipment monitoring without requiring electrical connections. In high-voltage environments where wired sensors pose safety risks, passive wireless solutions provide reliable temperature data while maintaining complete electrical isolation.

Transformer monitoring represents a particularly strong growth segment, as utilities prioritize condition-based maintenance to prevent failures. The ability to retrofit existing infrastructure without power sources makes these sensors ideal for grid modernization projects. With global investments in smart grid technologies exceeding $50 billion annually, the addressable market for wireless temperature monitoring continues to expand across transmission and distribution networks.

MARKET CHALLENGES

Radio Frequency Interference Creates Performance Limitations

While wireless passive temperature sensors offer numerous advantages, their performance can be significantly impacted by electromagnetic interference in industrial environments. The proliferation of wireless devices operating in industrial ISM bands creates signal congestion that may compromise data reliability. Heavy machinery, high-voltage equipment, and other RF sources can degrade sensor signal integrity, particularly in dense installation scenarios.

Other Challenges

Standardization Gaps

The lack of unified communication protocols across manufacturers creates interoperability challenges. Proprietary systems from different vendors often cannot communicate seamlessly, limiting system flexibility and increasing integration costs for end-users.

Range Limitations

Practical deployment distances are often shorter than theoretical specifications due to environmental factors. Metal structures and concrete walls typical in industrial settings can reduce effective read ranges by 30-50%, requiring careful system design and additional reader units.

MARKET RESTRAINTS

High Initial Costs Slow Adoption in Price-Sensitive Markets

The upfront investment required for wireless passive temperature sensor systems remains a significant barrier to widespread adoption. While the total cost of ownership proves economical over time due to reduced maintenance expenses, the initial capital outlay for reader infrastructure and specialized sensors can be 3-5 times higher than conventional wired solutions. This pricing disparity particularly affects small and medium enterprises in developing regions where budget constraints limit technology investments.

The perception of higher risk associated with novel technologies also slows decision-making cycles. Many industrial operators prefer proven wired systems despite their limitations, creating inertia in the transition to wireless monitoring solutions. Additionally, the need for specialized installation expertise further increases deployment costs compared to traditional temperature sensors.

MARKET OPPORTUNITIES

Emerging Battery-Free IoT Ecosystems Create New Application Potential

The rapid development of ambient energy harvesting technologies presents significant opportunities for wireless passive temperature sensors. Recent advances in RF energy harvesting and backscatter communication enable completely maintenance-free sensor networks compatible with emerging IoT architectures. These developments allow sensor deployment in previously inaccessible locations where power sources are unavailable, such as rotating machinery or remote outdoor installations.

Strategic partnerships between sensor manufacturers and IoT platform providers are accelerating market penetration. Major industrial automation vendors are increasingly incorporating passive wireless sensing into their digital ecosystem offerings, providing seamless integration with analytics platforms and edge computing solutions. This convergence creates new value propositions that extend beyond simple temperature monitoring to include predictive maintenance and process optimization capabilities.

WIRELESS PASSIVE TEMPERATURE SENSOR MARKET TRENDS

Industrial Automation and Smart Infrastructure Driving Market Growth

The global wireless passive temperature sensor market is experiencing strong growth, primarily driven by increasing adoption in industrial automation and smart infrastructure development. These sensors, which operate without external power sources, offer significant advantages in hazardous environments where traditional wired sensors are impractical. The electrical industry alone accounts for over 30% of the total market demand, with high-voltage equipment monitoring being a key application area. Recent innovations in surface acoustic wave (SAW) technology have enabled temperature monitoring accuracy within ±0.5°C, making them suitable for mission-critical industrial processes.

Other Trends

Expansion in Railway and Transportation Networks

Railway operators worldwide are increasingly deploying wireless passive sensors for real-time monitoring of trackside equipment and rolling stock components. This trend is particularly prominent in regions with high-speed rail networks, where temperature fluctuations significantly impact operational safety. The technology’s ability to function without battery replacement for extended periods (often exceeding 10 years) makes it ideal for transportation applications where maintenance access is challenging.

Emergence of Advanced RFID Solutions in Petrochemical Sector

The petrochemical industry is witnessing rapid adoption of RFID-based wireless temperature sensors for monitoring pipeline integrity and storage tank conditions. These solutions provide continuous temperature data without requiring physical access to hazardous areas, significantly reducing safety risks. Recent technological advancements have increased read ranges from 5 meters to over 20 meters, enabling comprehensive monitoring of large industrial facilities. Furthermore, integration with industrial IoT platforms allows for predictive maintenance, potentially reducing downtime by up to 40% in critical petrochemical operations.

Technological Convergence with Energy Harvesting Systems

Manufacturers are increasingly combining passive temperature sensors with energy harvesting technologies, creating completely autonomous monitoring solutions. This convergence is particularly valuable in metallurgical applications, where ambient thermal energy can power sensor operation without requiring battery replacement. Recent product launches demonstrate temperature measurement ranges extending from -40°C to +300°C, meeting the demanding requirements of steel and aluminum production facilities. The elimination of battery dependency also addresses environmental concerns about electronic waste in industrial settings.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Leaders and Niche Innovators Compete for Market Share

The wireless passive temperature sensor market exhibits a fragmented yet strategically evolving competitive environment, with multinational corporations dominating revenue shares while regional specialists carve out strong positions in application-specific segments. Texas Instruments maintains technological leadership through its advanced RFID-based sensor solutions, particularly in North America and Europe, where industrial automation demands are driving adoption.

Siemens and Schneider Electric have strengthened their positions through vertical integration, incorporating wireless temperature monitoring into broader industrial IoT ecosystems. Their established distribution networks and brand recognition in energy and manufacturing sectors give them a competitive edge in the $158 million global market projected to reach $229 million by 2032.

Emerging Chinese manufacturers like Zhuhai Yado Monitoring Technology and Hangzhou Hzsuper Electronic Technology are gaining traction through cost-competitive CT-type sensors, particularly in Asia’s expanding electrical infrastructure sector. These players are investing heavily in R&D to challenge established brands, with some already capturing 15-20% of their regional markets.

Strategic collaborations are reshaping the competitive map, as seen when EnOcean partnered with building automation providers to integrate its energy-harvesting sensors into smart HVAC systems. Meanwhile, semiconductor giants like Microchip Technology are differentiating through ecosystem solutions that combine sensors with proprietary wireless protocols.

List of Key Wireless Passive Temperature Sensor Companies Profiled

- ACREL (China)

- Texas Instruments (U.S.)

- Onsemi (U.S.)

- EnOcean (Germany)

- Siemens (Germany)

- Microchip Technology (U.S.)

- Anderson Instrument (U.S.)

- Yokogawa (Japan)

- Schneider Electric (France)

- ELLSION POWER (China)

- Zhuhai Yado Monitoring Technology (China)

- Hangzhou Hzsuper Electronic Technology (China)

- Shihou Energy (China)

- HANSEN TECHNOLOGY (Denmark)

- Cotex Electricity Technology (China)

The sector’s 5.7% CAGR is prompting both consolidation and specialization, with larger players acquiring innovative startups while smaller companies focus on niche applications like railway switchgear monitoring or high-temperature industrial processes. This dynamic creates a market where technological differentiation and application-specific solutions are becoming critical success factors.

Segment Analysis:

By Type

CT Type Segment Leads Due to High Accuracy and Stability in Industrial Applications

The market is segmented based on type into:

- CT Type

- Surface Acoustic Wave Type

- RFID Technology Type

- Others

By Application

Electrical Industry Segment Dominates Due to Extensive Use in Power Grid Monitoring

The market is segmented based on application into:

- Electrical Industry

- Petrochemical Industry

- Metallurgical Industry

- Railway Transportation Industry

- Others

By End User

Industrial Sector Holds Largest Share Due to Rising Automation Needs

The market is segmented based on end user into:

- Industrial

- Energy & Utilities

- Transportation

- Healthcare

- Others

By Technology

Radio Frequency Technology Segment Leads Due to Its Long-Range Capabilities

The market is segmented based on technology into:

- Radio Frequency

- Infrared

- Ultrasonic

- Others

Regional Analysis: Wireless Passive Temperature Sensor Market

Asia-Pacific

The Asia-Pacific region dominates the wireless passive temperature sensor market, accounting for the largest revenue share in 2024. This leadership position is driven by rapid industrialization, expansion of smart infrastructure projects, and increasing adoption of IoT-enabled monitoring systems across China, Japan, and India. China’s manufacturing sector remains the primary adopter, with its electrical and petrochemical industries integrating wireless sensors for equipment monitoring. However, cost sensitivity in developing nations leads to preference for RFID-based solutions over premium SAW technology. Japan’s advanced electronics ecosystem fosters innovation in miniaturized sensors, while India’s growing focus on industrial automation presents significant growth opportunities.

North America

North America represents the technologically mature yet steadily growing market for wireless passive temperature sensors. Stringent workplace safety regulations from OSHA and the EPA drive adoption in hazardous environments like oil refineries and power plants. The U.S. leads regional adoption with strong R&D investments from key players like Texas Instruments and Microchip Technology. The region shows growing preference for CT-type sensors due to their reliability in extreme conditions. Canada’s mining sector and Mexico’s expanding manufacturing base create additional demand for wireless monitoring solutions that eliminate wiring costs in remote installations.

Europe

Europe’s market growth is propelled by strict EU regulations on energy efficiency and equipment safety, particularly in Germany and France. The region demonstrates the highest adoption of SAW-type sensors for their precision in automotive and aerospace applications. Siemens and EnOcean drive innovation in energy-harvesting sensor technologies that align with Europe’s sustainability goals. However, market expansion faces challenges from conservative end-users in traditional industries who prefer wired alternatives. The UK’s focus on smart grid modernization and Scandinavia’s renewable energy projects present emerging opportunities for wireless temperature monitoring solutions.

South America

South America exhibits moderate growth potential with Brazil and Argentina leading adoption in their burgeoning industrial sectors. The region shows increasing demand in food processing and pharmaceutical applications requiring strict temperature controls. Economic constraints and infrastructure limitations slow widespread adoption, making price-competitive RFID solutions the dominant choice. Chile’s mining operations and Colombia’s oil industry represent key verticals gradually transitioning to wireless monitoring to improve operational safety, though technology adoption lags behind global averages due to budget constraints.

Middle East & Africa

This emerging market shows differentiated growth patterns, with GCC nations like Saudi Arabia and UAE driving adoption in oil/gas and construction sectors through smart city initiatives. South Africa leads in mining applications while North African countries show nascent demand in manufacturing. The region’s extreme climates create unique requirements for high-temperature resistant sensors. Although adoption rates remain low compared to global markets, increasing foreign investments in industrial automation and energy projects suggest accelerated market growth beyond 2030. Challenges include limited technical expertise and preference for conventional monitoring methods in cost-sensitive markets.

Report Scope

This market research report provides a comprehensive analysis of the Global Wireless Passive Temperature Sensor Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 158 million in 2024 and is projected to reach USD 229 million by 2032, growing at a CAGR of 5.7%.

- Segmentation Analysis: Detailed breakdown by product type (CT Type, Surface Acoustic Wave Type, RFID Technology Type), application (Electrical, Petrochemical, Metallurgical, Railway Transportation, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with the U.S. and China emerging as key markets.

- Competitive Landscape: Profiles of leading market participants, including ACREL, Texas Instruments, Siemens, Schneider Electric, and Yokogawa, covering their product portfolios, R&D investments, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging sensor technologies, wireless communication protocols, and integration with IoT platforms for real-time monitoring applications.

- Market Drivers & Restraints: Evaluation of factors such as industrial automation demand, energy efficiency regulations, and challenges related to signal interference in harsh environments.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, system integrators, industrial end-users, and investors regarding market opportunities and competitive positioning.

The research methodology combines primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Wireless Passive Temperature Sensor Market?

-> Wireless Passive Temperature Sensor Market was valued at 158 million in 2024 and is projected to reach US$ 229 million by 2032, at a CAGR of 5.7% during the forecast period.

Which key companies operate in this market?

-> Major players include Texas Instruments, Siemens, Schneider Electric, Yokogawa, and Microchip Technology, with the top five companies holding significant market share.

What are the key growth drivers?

-> Growth is driven by increasing industrial automation, demand for maintenance-free monitoring solutions, and stringent temperature regulation requirements across industries.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth, while North America currently leads in technology adoption and market share.

What are the emerging trends?

-> Emerging trends include integration with Industry 4.0 systems, development of ultra-low-power sensors, and expansion into renewable energy applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...