MARKET INSIGHTS

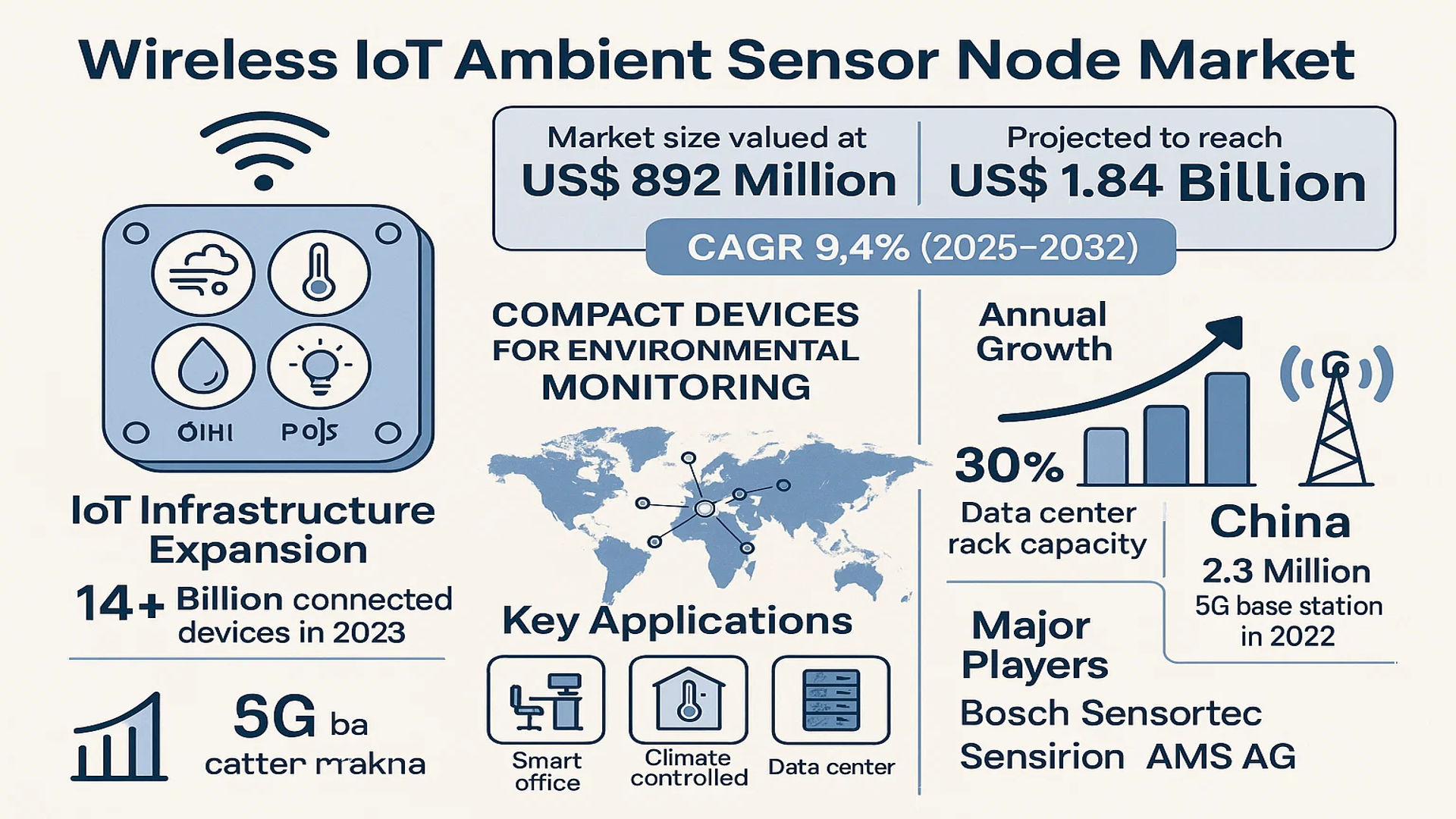

The global Wireless IoT Ambient Sensor Node Market size was valued at US$ 892 million in 2024 and is projected to reach US$ 1.84 billion by 2032, at a CAGR of 9.4% during the forecast period 2025-2032.

Wireless IoT Ambient Sensor Nodes are compact, interconnected devices equipped with multiple environmental monitoring capabilities. These nodes integrate sensors for measuring air quality (including VOC detection), temperature, humidity, light intensity, noise levels, and atmospheric pressure. The data collected enables real-time monitoring and automation across various smart environments.

Market growth is being driven by the rapid expansion of IoT infrastructure globally, with over 14 billion connected devices recorded in 2023 – an 18% increase from 2021. The deployment of 5G networks is accelerating adoption, particularly in China where 2.3 million 5G base stations were operational by 2022. Key applications include smart offices, climate-controlled storage facilities, and data centers – a sector experiencing 30% annual growth in rack capacity. Major players like Bosch Sensortec, Sensirion, and AMS AG are innovating with low-power designs and AI-enhanced analytics capabilities to capture this growing market.

MARKET DYNAMICS

MARKET DRIVERS

Rapid IoT Adoption Across Industries Accelerates Market Growth

The global proliferation of Internet of Things (IoT) solutions is creating unprecedented demand for wireless ambient sensor nodes. With over 14 billion connected IoT devices currently in operation, organizations across sectors are deploying sensor networks to monitor environmental conditions in real-time. Smart buildings, manufacturing facilities, and logistics operations increasingly rely on these sensor nodes to optimize energy use, ensure product quality, and maintain safety standards. The manufacturing sector alone accounts for nearly 25% of all industrial IoT deployments, with environmental monitoring being a critical use case.

5G Network Expansion Enables Next-Generation Sensor Deployments

The ongoing global rollout of 5G networks represents a significant enabler for wireless IoT sensor solutions. With China having deployed over 2.3 million 5G base stations and gigabit network coverage reaching 500 million households, the infrastructure now exists to support massive IoT deployments with low latency requirements. 5G’s improved bandwidth capacity allows for more frequent sensor data transmission without network congestion, while its energy-efficient protocols extend the battery life of wireless sensor nodes. These technical advantages are driving adoption across smart city applications where real-time environmental monitoring is critical.

Growing Emphasis on Indoor Air Quality Monitoring

Heightened awareness of indoor air quality following global health concerns has significantly increased demand for environmental sensors in commercial and institutional spaces. Modern wireless sensor nodes now incorporate sophisticated air quality monitoring capabilities, detecting particulate matter (PM2.5/PM10), volatile organic compounds (VOCs), CO2 levels, and other parameters with laboratory-grade accuracy. Facility managers are prioritizing these deployments, with commercial building IoT adoption growing at 28% annually. The ability to monitor indoor environments continuously has become a key competitive differentiator for offices, schools, and healthcare facilities.

➤ The global smart buildings market is projected to reach $328 billion by 2030, with environmental monitoring representing the fastest-growing segment at 31% CAGR.

MARKET RESTRAINTS

High Deployment Costs Limit Widespread Adoption

While wireless IoT ambient sensor technology offers significant benefits, the initial investment required for comprehensive deployments remains a barrier for many organizations. A complete enterprise-grade sensor network implementation can cost between $50,000-$250,000 depending on facility size and sensor density, with ongoing maintenance adding 15-20% annually. These costs are particularly challenging for small and medium-sized businesses, where ROI timelines often exceed acceptable thresholds. Furthermore, the specialized expertise required for optimal sensor placement and network configuration adds to the total cost of ownership.

Data Security and Privacy Concerns Hamper Adoption

The collection of sensitive environmental data through IoT networks raises important security and privacy considerations that some organizations find challenging to address. Wireless sensor nodes, by their distributed nature, create multiple potential entry points for cyber threats. Recent analyses show that over 35% of enterprise IoT deployments have experienced at least one security incident related to environmental monitoring systems. These concerns are particularly acute in healthcare and government sectors where environmental data may reveal sensitive operational patterns or occupant behaviors.

Interoperability Challenges Across Vendor Ecosystems

The lack of universal standards for wireless IoT sensor communication protocols continues to hinder seamless integration across different manufacturer ecosystems. Many organizations find their sensor networks siloed due to proprietary data formats and incompatible APIs, forcing them to manage multiple parallel systems. This fragmentation is particularly evident in large-scale deployments where sensors from different vendors must work together. The resulting complexity increases implementation timelines by 25-40% and raises ongoing maintenance costs.

MARKET OPPORTUNITIES

Edge Computing Integration Creates New Value Propositions

The convergence of wireless sensor networks with edge computing presents significant opportunities for more intelligent environmental monitoring solutions. By processing data locally at the sensor node level, organizations can reduce cloud dependency while enabling real-time analytics and automated responses. This is particularly valuable in industrial settings where sub-second response times to environmental changes are critical. The edge computing market for IoT applications is growing at 32% annually, with environmental monitoring accounting for nearly 40% of use cases.

Smart City Initiatives Driving Large-Scale Deployments

Municipal governments worldwide are investing heavily in IoT infrastructure as part of broader smart city initiatives, creating substantial opportunities for ambient sensor providers. Urban environmental monitoring networks now track everything from air pollution to noise levels across entire city districts. These deployments often involve thousands of sensor nodes working in concert, with data analytics platforms providing actionable insights for urban planners. Over 500 cities globally have active smart city programs, with environmental monitoring consistently ranking among the top three IoT investment priorities.

AI-Powered Predictive Analytics Transforming Sensor Data Value

The integration of artificial intelligence with environmental sensor networks is unlocking new predictive capabilities that significantly enhance the value proposition. Machine learning algorithms can now analyze historical and real-time sensor data to forecast environmental trends, allowing for proactive facility management. This is particularly impactful in critical environments like data centers and cold storage facilities, where even minor environmental fluctuations can have major consequences. AI-enhanced sensor solutions command premium pricing and are driving 45% higher customer retention rates compared to traditional monitoring systems.

MARKET CHALLENGES

Battery Life Limitations Constrain Deployment Options

Despite advances in low-power wireless protocols, battery life remains a significant constraint for many wireless sensor node deployments. In demanding environments where frequent data transmission is required, batteries may need replacement every 6-12 months, creating maintenance challenges. This is particularly problematic in hard-to-access locations or hazardous environments. While energy harvesting solutions show promise, their adoption remains limited by higher costs and technical complexity, with only 15% of current deployments incorporating such technologies.

Sensor Calibration and Accuracy Maintenance

Maintaining measurement accuracy over time presents an ongoing challenge for wireless environmental sensor deployments. Many sensor types, particularly those measuring air quality parameters, require regular calibration to ensure data reliability. In practice, over 60% of deployed sensors experience measurable drift within 12-18 months of operation. This creates logistical challenges for large-scale deployments and raises questions about data quality if proper maintenance schedules aren’t followed consistently across sensor networks.

Talent Shortage in IoT Implementation Expertise

The rapid growth of IoT deployments has outpaced the availability of qualified professionals who can design and implement sophisticated sensor networks effectively. Organizations report that IoT implementation projects take 30% longer than anticipated due to difficulties finding personnel with the right combination of networking, sensor technology, and data analytics skills. This talent gap is particularly acute in emerging markets where IoT adoption is growing fastest but local expertise remains limited.

WIRELESS IOT AMBIENT SENSOR NODE MARKET TRENDS

Expansion of Smart Building Infrastructure Driving Market Growth

The global Wireless IoT Ambient Sensor Node market is experiencing robust growth, driven by the increasing adoption of smart building technologies. These sensor nodes, capable of monitoring parameters such as air quality, temperature, humidity, and noise levels, are becoming essential for modern infrastructure. Recent data indicates that the market was valued at $XX million in 2024 and is projected to reach $XX million by 2032, growing at a Compound Annual Growth Rate (CAGR) of XX%. This surge is largely attributed to the rising demand for energy-efficient and sustainable building solutions, particularly in commercial and industrial sectors. The integration of these sensors with IoT platforms enables real-time data analytics, further optimizing operational efficiency.

Other Trends

5G and IoT Convergence Enhancing Sensor Capabilities

The rollout of 5G networks is significantly amplifying the potential of Wireless IoT Ambient Sensor Nodes. With over 2.3 million 5G base stations already deployed globally—110 cities meeting gigabit standards—network reliability and latency have improved dramatically. This enables seamless data transmission from sensor nodes to cloud-based platforms, facilitating faster decision-making. Furthermore, advancements in edge computing are reducing dependency on centralized servers, allowing sensors to process data locally. This trend is particularly beneficial for applications requiring low-latency responses, such as industrial automation and healthcare monitoring.

Growing Demand for Environmental Monitoring in Data Centers

Data centers, which house critical IT infrastructure, are increasingly adopting Wireless IoT Ambient Sensor Nodes to ensure optimal environmental conditions. The total size of global data center racks has exceeded 6.5 million standard racks, with a growth rate of over 30% annually. Sensors monitoring temperature, humidity, and air quality help prevent equipment failures and reduce energy consumption. For instance, maintaining precise temperature control can lower cooling costs by up to 40%. Additionally, regulatory standards for environmental compliance are pushing organizations to invest in advanced monitoring solutions. This demand is expected to accelerate market expansion, particularly in North America and Asia-Pacific regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Leverage IoT and 5G Expansion to Capture Wireless Sensor Node Opportunities

The global Wireless IoT Ambient Sensor Node market is characterized by moderate fragmentation, with established technology providers competing alongside agile startups specializing in environmental monitoring solutions. Bosch Sensortec and Sensirion currently dominate the high-performance segment, controlling approximately 28% of the professional-grade sensor node market as of 2024. Their leadership stems from patented MEMS technology and integration with enterprise IoT platforms.

Swift Sensors has emerged as a significant challenger in North America, particularly in cold chain monitoring applications, reporting 37% year-over-year revenue growth in 2023. Meanwhile, AMS AG (now part of Renesas Electronics) continues to lead in miniaturized sensor nodes, with their latest products measuring just 10x10mm while maintaining industrial-grade accuracy.

The competitive intensity is increasing as infrastructure development accelerates globally. China’s deployment of 2.3 million 5G base stations has created a favorable environment for Linovision and other regional players to expand their smart building solutions, while European manufacturers like Prodrive Technologies are gaining traction in precision industrial monitoring through strategic partnerships with Siemens and ABB.

Recent developments show that companies are prioritizing three strategic areas: energy efficiency (with some nodes now operating for 5+ years on a single battery), edge computing capabilities (processing data locally to reduce latency), and multi-sensor fusion (combining 8+ environmental parameters in a single device). This technological arms race is expected to continue as the market approaches $X billion by 2032.

List of Key Wireless IoT Ambient Sensor Node Companies Profiled

- Swift Sensors (U.S.)

- BeanAir (Germany)

- Paragon (U.S.)

- Trossen Robotics (U.S.)

- Bosch Sensortec (Germany)

- Sensirion (Switzerland)

- AMS AG (Austria)

- Prodrive Technologies (Netherlands)

- Beep (Italy)

- Estimote (Poland)

- Linovision (China)

- NCD Enterprise (U.S.)

- Sensata (U.S.)

- Althen (Netherlands)

Segment Analysis:

By Type

Temperature Sensors Dominate the Market Due to Their Critical Role in Environmental Monitoring

The market is segmented based on type into:

- Humidity Sensors

- Temperature Sensors

- Air Quality Sensors

- Subtypes: VOC sensors, CO2 sensors, and others

- Ambient Light Sensors

- Others

- Subtypes: Noise level sensors, barometric pressure sensors, and others

By Application

Data Center Segment Leads Due to Growing Need for Environmental Monitoring in Critical Infrastructure

The market is segmented based on application into:

- Office

- Cold Storage

- Data Center

- Healthcare Facilities

- Others

By Connectivity Technology

Wi-Fi and Bluetooth Segment Leads Due to High Adoption in Commercial Applications

The market is segmented based on connectivity technology into:

- Wi-Fi

- Bluetooth

- Subtypes: Bluetooth Low Energy (BLE) and others

- LoRaWAN

- Zigbee

- Others

By Power Source

Battery-Powered Segment Dominates Due to Deployment Flexibility in IoT Applications

The market is segmented based on power source into:

- Battery-Powered

- Wired

- Energy Harvesting

- Subtypes: Solar, RF, and others

Regional Analysis: Wireless IoT Ambient Sensor Node Market

North America

North America leads the global Wireless IoT Ambient Sensor Node market, driven by rapid adoption of smart building technologies and strong demand for workplace environmental monitoring. The U.S. accounts for over 85% of regional market share, supported by progressive IoT policies and widespread 5G deployment. Key sectors include commercial real estate (covering 60% of installations), data centers, and healthcare facilities where sensor nodes monitor critical air quality parameters. The region benefits from established players like Swift Sensors and NCD Enterprise, along with significant R&D investments in edge computing integration. However, higher product costs and interoperability challenges between legacy systems remain adoption barriers.

Europe

Europe represents the second-largest market, characterized by stringent EU regulations on indoor air quality (EU Directive 2008/50/EC) and energy efficiency mandates driving sensor deployments. Germany leads adoption with industrial IoT applications, while the UK shows accelerated growth in smart office solutions. The region sees particular demand for multi-sensor nodes combining VOC detection with particulate monitoring, especially in Nordic countries where building automation penetration exceeds 45%. European manufacturers like Sensirion and Bosch Sensortec dominate the premium segment, though price sensitivity in Southern European markets favors Chinese alternatives.

Asia-Pacific

As the fastest-growing region, Asia-Pacific benefits from massive smart city initiatives and hyper-scale data center construction. China controls approximately 65% of regional demand, supported by its nationwide IoT infrastructure including 2.3 million 5G base stations. Japan and South Korea show strong adoption in precision manufacturing environments, while India emerges as a high-growth market with 30% annual demand increase for basic temperature/humidity nodes. The region faces unique challenges including signal interference in dense urban deployments and varying protocol standards across countries. Local players like Linovision compete aggressively on price, creating a bifurcated market between budget and premium solutions.

South America

South America presents selective growth opportunities, primarily in Brazil’s industrial and agricultural monitoring sectors which comprise 70% of regional demand. The lack of standardized IoT networks and economic instability constrain wider adoption, though mining and cold chain logistics show promising uptake. While multinational suppliers dominate premium applications, local assemblers cater to price-conscious buyers with simplified sensor nodes. Regulatory developments around workplace safety and food storage monitoring could unlock new verticals, particularly in Argentina and Chile’s wine export industry.

Middle East & Africa

The MEA market remains nascent but demonstrates accelerated growth in GCC countries, particularly UAE and Saudi Arabia where smart city projects drive 80% of demand. High ambient temperatures create specialized requirements for sensor durability, favoring vendors offering extended operating ranges. Africa shows potential in mining and healthcare applications, though limited last-mile connectivity and power infrastructure hinder scalability. The region benefits from Chinese technology transfers and is poised for expansion as 5G rollouts progress, particularly in economic hubs like Dubai and Johannesburg.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Wireless IoT Ambient Sensor Node markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Wireless IoT Ambient Sensor Node market is projected to grow at a significant CAGR of 9.4% during the forecast period, driven by increasing IoT adoption.

- Segmentation Analysis: Detailed breakdown by product type (humidity sensors, temperature sensors, others), technology, application (office, cold storage, data center, others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis. Asia-Pacific is expected to dominate due to rapid IoT infrastructure development.

- Competitive Landscape: Profiles of leading market participants including Swift Sensors, Bosch Sensortec, Sensirion, and AMS AG, covering their product portfolios, strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging wireless technologies, sensor miniaturization, energy harvesting solutions, and integration with AI/ML for advanced analytics.

- Market Drivers & Restraints: Evaluation of growth drivers like smart building adoption and industrial IoT expansion, along with challenges such as data security concerns and interoperability issues.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, IoT platform providers, system integrators, and end-users across commercial and industrial sectors.

The research methodology combines primary interviews with industry experts and analysis of verified secondary data sources to ensure accuracy and reliability of market insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Wireless IoT Ambient Sensor Node Market?

->Wireless IoT Ambient Sensor Node Market size was valued at US$ 892 million in 2024 and is projected to reach US$ 1.84 billion by 2032, at a CAGR of 9.4% during the forecast period 2025-2032.

Which key companies operate in Global Wireless IoT Ambient Sensor Node Market?

-> Key players include Swift Sensors, Bean Air, Bosch Sensortec, Sensirion, AMS AG, and Prodrive Technologies, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption of smart building technologies, increasing industrial IoT applications, and government initiatives for smart city development.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing market, driven by China’s rapid IoT infrastructure development with over 2.3 million 5G base stations deployed by 2022.

What are the emerging trends?

-> Emerging trends include integration of AI for predictive analytics, development of self-powered sensor nodes, and increasing adoption in data center monitoring applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...