MARKET INSIGHTS

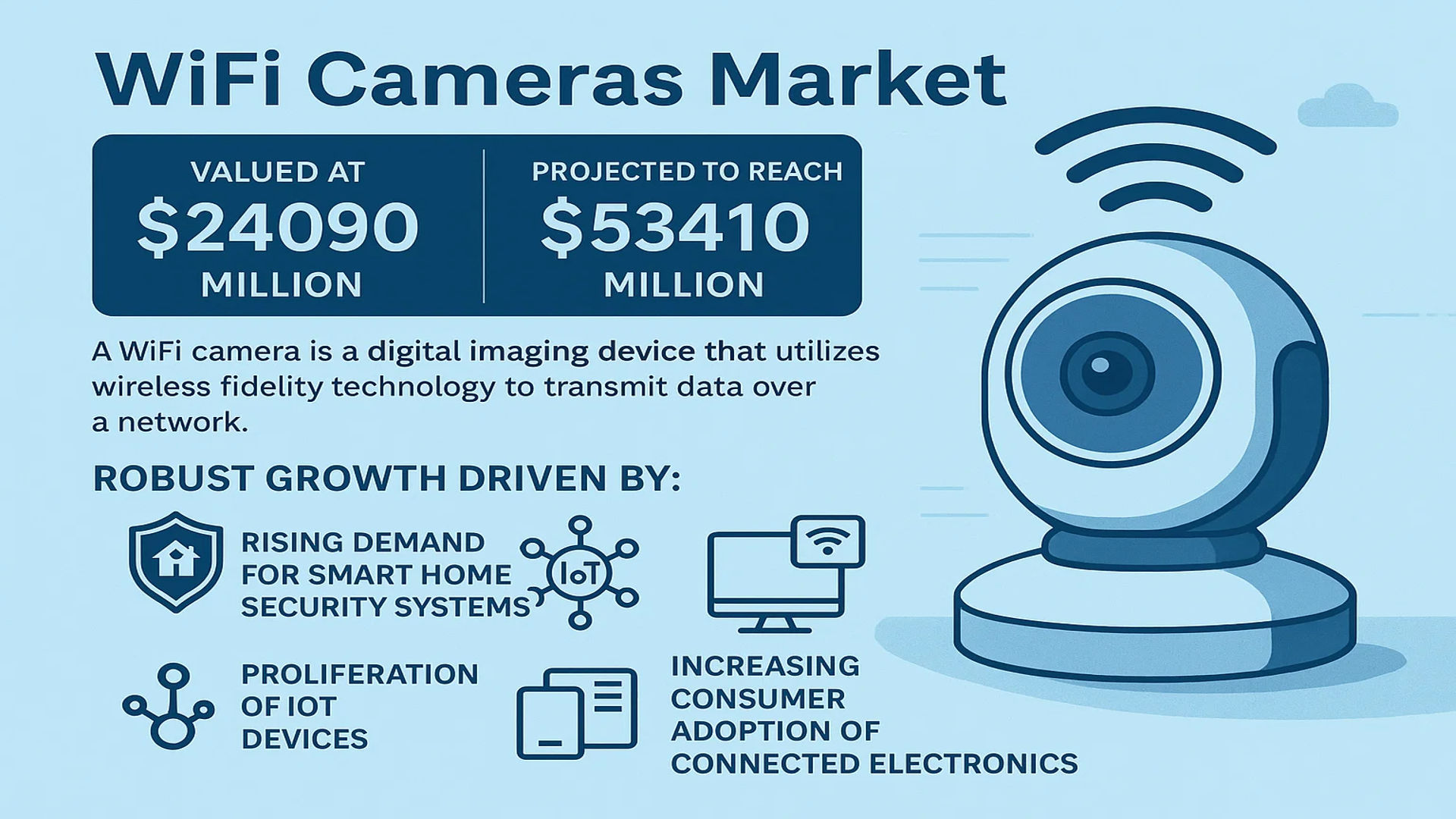

The global WiFi Cameras Market was valued at 24090 million in 2024 and is projected to reach US$ 53410 million by 2032, at a CAGR of 12.3% during the forecast period.

A WiFi camera is a digital imaging device that utilizes wireless fidelity technology to transmit data over a network. These cameras connect to a network via wireless signals, primarily in the 2.4GHz UHF and 5GHz SHF bands, enabling users to view, download, or stream footage remotely. This functionality can be achieved either through short-distance direct wireless transmission or by connecting to the internet via a wireless router, providing significant flexibility and convenience.

The market is experiencing robust growth driven by several key factors, including the rising demand for smart home security systems, the proliferation of Internet of Things (IoT) devices, and increasing consumer adoption of connected consumer electronics. Furthermore, advancements in wireless technology, such as the rollout of WiFi 6, are enhancing data transmission speeds and reliability, which is crucial for high-resolution video streaming. The market is fragmented, with key players like Canon holding a leading position of approximately 9% market share. Other significant contributors include Sony, Samsung, Panasonic, and Nikon, who continuously innovate to capture market segments ranging from home security to sports and automotive applications.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of Smart Home Security Systems to Drive Market Growth

The global WiFi cameras market is experiencing robust growth driven by increasing consumer adoption of smart home security systems. With rising concerns over residential security and property protection, demand for WiFi-enabled surveillance cameras has surged significantly. The integration of these cameras with IoT ecosystems allows homeowners to monitor properties remotely via smartphones, enhancing convenience and real-time security management. Over 35% of households in developed markets now utilize at least one smart security device, with WiFi cameras representing the fastest-growing segment. This trend is further accelerated by decreasing hardware costs and improved wireless connectivity infrastructure, making advanced security solutions accessible to broader consumer segments.

Advancements in Wireless Technology and 5G Deployment to Accelerate Market Expansion

Technological advancements in wireless communication standards are significantly propelling the WiFi cameras market forward. The transition from 802.11n to 802.11ac and now WiFi 6 has dramatically improved data transmission speeds, reduced latency, and enhanced network capacity. These improvements enable higher resolution video streaming, smoother real-time monitoring, and better multi-camera system performance. Concurrently, global 5G network deployment is creating additional growth opportunities, particularly for outdoor and mobile WiFi camera applications. The enhanced bandwidth and lower latency of 5G networks facilitate superior video quality and more reliable remote access, driving adoption across both consumer and commercial segments.

Growing Integration of Artificial Intelligence and Machine Learning Features

The integration of artificial intelligence and machine learning capabilities represents a major driver for WiFi camera market growth. Modern WiFi cameras increasingly incorporate advanced features such as facial recognition, motion detection, object tracking, and behavioral analysis. These intelligent capabilities transform passive recording devices into proactive security systems that can distinguish between routine activities and potential threats. The implementation of edge computing allows these AI features to operate directly on the camera hardware, reducing cloud dependency and enhancing response times. This technological evolution has expanded WiFi camera applications beyond traditional security into areas such as elderly care monitoring, pet observation, and business analytics, creating new revenue streams for manufacturers.

Furthermore, manufacturers are continuously developing enhanced night vision capabilities, with many current models offering color night vision up to 15 meters without additional lighting, significantly improving low-light performance and expanding usable applications.

MARKET RESTRAINTS

Cybersecurity Vulnerabilities and Privacy Concerns to Limit Market Penetration

Despite strong growth prospects, the WiFi cameras market faces significant restraints due to cybersecurity vulnerabilities and increasing privacy concerns. Wireless transmission of video data creates potential entry points for unauthorized access, with studies indicating that approximately 15% of consumer-grade WiFi cameras have exploitable security weaknesses. High-profile incidents of camera hacking have raised consumer awareness about privacy risks, particularly for indoor cameras that monitor private spaces. These concerns are especially pronounced in regions with stringent data protection regulations, where manufacturers must implement robust encryption and compliance measures that increase product development costs and complexity.

Additionally, the evolving nature of cyber threats requires continuous security updates and patches, creating ongoing maintenance challenges for both manufacturers and consumers. Many users fail to regularly update their camera firmware, leaving systems vulnerable to known exploits. This cybersecurity landscape has led some corporate entities and government agencies to restrict WiFi camera usage in sensitive environments, potentially limiting market expansion in certain commercial segments.

MARKET CHALLENGES

Network Infrastructure Limitations and Bandwidth Constraints Challenge Market Development

The WiFi cameras market faces substantial challenges related to network infrastructure limitations and bandwidth constraints. While urban areas generally enjoy robust internet connectivity, many rural and developing regions lack the necessary infrastructure to support high-bandwidth video streaming. Even in developed markets, network congestion and bandwidth limitations can affect video quality and reliability, particularly when multiple high-resolution cameras operate simultaneously on a single network. The average household internet speed in many regions remains insufficient for optimal 4K video streaming, forcing consumers to compromise on video quality or experience latency issues.

Other Challenges

Power Dependency Issues

Many WiFi cameras require continuous power connectivity, limiting placement options and creating installation challenges. Battery-operated models address this issue but often sacrifice features or require frequent recharging, creating user inconvenience. The search for balance between functionality and power autonomy remains an ongoing engineering challenge for manufacturers.

Interoperability and Standardization Gaps

The absence of universal standards across different manufacturers creates interoperability challenges within smart home ecosystems. Consumers often face difficulties integrating cameras from different brands into unified systems, leading to fragmented user experiences and potentially limiting multi-camera adoption.

MARKET OPPORTUNITIES

Emerging Applications in Industrial IoT and Smart City Infrastructure to Create New Growth Avenues

The WiFi cameras market presents significant growth opportunities through expansion into industrial IoT applications and smart city infrastructure development. Beyond traditional security applications, WiFi cameras are increasingly deployed for operational monitoring, quality control, and process optimization in manufacturing environments. The integration of thermal imaging and advanced analytics enables predictive maintenance applications, where cameras detect equipment anomalies before failures occur. In smart city contexts, WiFi cameras facilitate traffic management, public safety monitoring, and urban planning through continuous data collection and analysis.

Additionally, the integration of WiFi cameras with broader business intelligence systems creates opportunities in retail analytics, customer behavior tracking, and operational efficiency improvements. The ability to capture and analyze visual data in real-time provides businesses with unprecedented insights into operations and customer interactions, driving demand for advanced camera systems with analytical capabilities.

Furthermore, technological advancements in solar-powered and low-energy WiFi cameras are opening new market segments in remote monitoring and environmental applications where traditional power sources are unavailable or impractical.

WI-FI CAMERAS MARKET TRENDS

Integration of Artificial Intelligence and Machine Learning to Emerge as a Dominant Trend

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is fundamentally transforming the Wi-Fi camera landscape, driving a significant shift from basic surveillance to intelligent, predictive monitoring systems. These advanced algorithms enable features such as real-time object and person detection, anomaly recognition, and behavioral analysis, which drastically reduce false alarms and enhance security efficiency. For instance, modern AI-powered cameras can distinguish between a pet and an intruder, or identify specific vehicles, providing users with more relevant and actionable alerts. Furthermore, the adoption of edge computing, where data processing occurs on the device itself rather than in the cloud, has minimized latency to under 100 milliseconds for many high-end models, enabling instantaneous response to security events. This technological evolution is not just a premium feature; it is becoming a market standard, with over 65% of new Wi-Fi camera models launched in the past year incorporating some form of AI-driven analytics, a figure that is projected to exceed 90% by 2027.

Other Trends

Rising Demand for High-Resolution and Low-Light Imaging

Consumer and professional expectations for video quality are continuously escalating, fueling a strong market trend towards cameras with 4K Ultra HD resolution and superior low-light performance. This is particularly critical for applications in home security and law enforcement, where the ability to capture clear, identifiable evidence is paramount. Advancements in sensor technology, such as the widespread adoption of larger Sony STARVIS sensors, have enabled cameras to deliver detailed color video even in extremely low-light conditions, reducing the reliance on harsh, glaring IR illuminators that can give away a camera’s position. The market for 4K-capable Wi-Fi cameras has seen a compound annual growth rate of over 28% in the last three years, and they now constitute nearly 40% of the revenue in the consumer security segment, indicating a rapid consumer shift towards higher-fidelity monitoring solutions.

Expansion into New Applications and IoT Ecosystem Integration

The functionality of Wi-Fi cameras is expanding far beyond traditional security, becoming central nodes in the broader smart home and IoT ecosystem. This trend is characterized by seamless integration with other smart devices, such as door locks, lighting systems, and voice assistants from Amazon, Google, and Apple. Users can now create automated routines; for example, a camera can trigger outdoor lights to turn on upon detecting motion after dark, or send a video feed directly to a smart TV or display when the doorbell is pressed. This interoperability is a key purchasing driver, with studies indicating that compatibility with a preferred smart home platform influences the buying decision for over 70% of consumers. Moreover, new applications are emerging in sectors like pet care, where cameras feature treat dispensers and laser pointers, and in elderly care, offering fall detection and remote check-in capabilities, thereby opening entirely new and lucrative market segments for manufacturers.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Positioning Drive Market Leadership

The global WiFi cameras market exhibits a fragmented competitive structure, characterized by numerous players ranging from established electronics giants to specialized security and action camera manufacturers. This diversity creates a dynamic environment where technological innovation, brand recognition, and distribution networks are critical differentiators. While the market is accessible to new entrants, particularly in niche segments, the dominance of key players creates significant barriers to entry in the mainstream consumer electronics and professional security sectors.

Canon Inc. stands as the unequivocal market leader, holding approximately 9% of the global market share in 2024. Its leadership is anchored in a robust portfolio of high-quality digital cameras with integrated WiFi capabilities, a strong brand legacy in imaging, and an extensive global retail and support network. The company’s continuous investment in advanced image sensors and seamless connectivity software ensures its products remain at the forefront of the consumer electronics segment.

Following closely, Sony Corporation and Samsung Electronics also command significant portions of the market. Sony leverages its expertise in semiconductor technology, particularly its industry-leading image sensors, which are supplied to numerous other camera manufacturers. This vertical integration provides a substantial competitive advantage. Samsung, while having scaled back its dedicated camera business, remains a potent force through its diversified product ecosystem, integrating WiFi cameras with its smartphones, tablets, and SmartThings-based home security systems.

Meanwhile, specialized players are carving out substantial niches. GoPro Inc. continues to dominate the action camera segment, with its rugged, high-performance WiFi-enabled cameras being the standard for sports and adventure enthusiasts. In the home security arena, companies like TP-Link, Netgear (with its Arlo brand), and HIKVISION are fiercely competitive. Their growth is propelled by the global surge in smart home adoption, with these companies focusing on user-friendly apps, cloud storage services, and integration with popular voice assistants and smart home platforms.

The competitive strategies observed are multifaceted. Leading companies are heavily investing in research and development to enhance features like night vision, AI-powered person/package detection, higher resolution streaming, and improved battery life. Furthermore, strategic mergers, acquisitions, and partnerships are common, as seen with established brands acquiring innovative startups to quickly integrate new technologies or expand their market reach. This intense competition drives rapid product evolution and benefits consumers through better features and more competitive pricing.

List of Key WiFi Camera Companies Profiled

- Canon Inc. (Japan)

- Sony Corporation (Japan)

- Samsung Electronics Co., Ltd. (South Korea)

- Panasonic Holdings Corporation (Japan)

- Nikon Corporation (Japan)

- GoPro Inc. (U.S.)

- Kodak (U.S.)

- Fujifilm Holdings Corporation (Japan)

- Olympus Corporation (Japan)

- Ricoh Company, Ltd. (PENTAX) (Japan)

- Garmin Ltd. (Switzerland)

- TP-Link Technologies Co., Ltd. (China)

- HIKVISION (China)

- Netgear, Inc. (U.S.)

- D-Link Corporation (Taiwan)

Segment Analysis:

By Type

Home Security Camera Segment Dominates the Market Due to Surging Demand for Remote Monitoring and Smart Home Integration

The market is segmented based on type into:

- Home Security Camera

- Subtypes: Indoor, Outdoor, Doorbell, and others

- Digital Camera with WiFi

- Car Camera

- Subtypes: Dash Cams, Rearview, and others

- Sports Camera

- Others

By Application

Home Security Segment Leads Due to Rising Consumer Focus on Safety and Proactive Property Monitoring

The market is segmented based on application into:

- Home Security

- Consumer Electronics

- Sports Enthusiasts

- Car Security

- Others

By End User

Residential End User Segment Holds Significant Share Driven by DIY Installation Trends and IoT Adoption

The market is segmented based on end user into:

- Residential

- Commercial

- Subtypes: Retail, Offices, Industrial, and others

- Government & Public Sector

By Connectivity

Dual-Band (2.4GHz & 5GHz) Segment Gains Traction for its Superior Speed and Reduced Interference in Dense Networks

The market is segmented based on connectivity into:

- Single-Band (2.4GHz)

- Dual-Band (2.4GHz & 5GHz)

- Tri-Band

Regional Analysis: WiFi Cameras Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global WiFi cameras market, accounting for the largest market share by both volume and revenue. This dominance is primarily driven by massive manufacturing hubs, particularly in China, which is home to major players like HIKVISION and Dahua(LeChange). The region benefits from a robust consumer electronics sector, rapid urbanization, and increasing disposable incomes, which fuel demand across all product segments, from home security cameras to digital cameras with WiFi capabilities. Furthermore, the widespread adoption of smart home technologies and significant investments in IoT infrastructure by governments and private entities are accelerating market penetration. However, intense price competition among numerous local and international brands leads to thinner profit margins, pushing companies to innovate constantly in features and cost-efficiency.

North America

North America represents a highly mature and technologically advanced market for WiFi cameras, characterized by strong consumer awareness and high adoption rates of smart home devices. The United States is the key contributor, driven by a heightened focus on home security and the presence of leading technology companies such as Google (Nest), Amazon (Ring), and Arlo (a Netgear spin-off). High internet penetration rates and the proliferation of 5G networks support the seamless integration and functionality of these devices. Additionally, the region sees substantial demand from the sports and action camera segment, with brands like GoPro maintaining significant market presence. Regulatory standards around data privacy and security, such as those enforced by the FTC, also shape product development and consumer trust in the region.

Europe

Europe is a significant and steadily growing market for WiFi cameras, with demand largely driven by stringent privacy regulations, such as the GDPR, which influence product features related to data storage and transmission. Countries like Germany, the UK, and France show high adoption rates, particularly in the home security segment, due to increasing concerns over property safety and the growing smart home ecosystem. The market is also supported by a strong culture of travel and outdoor activities, boosting sales of sports and action cameras. European consumers tend to prioritize quality, brand reputation, and compliance with regional standards, giving an edge to established players like Canon, Sony, and Philips. However, economic fluctuations in certain countries can affect consumer spending on non-essential electronics.

South America

The WiFi cameras market in South America is emerging, with growth potential primarily fueled by increasing urbanization and rising crime rates, which drive demand for home security solutions. Brazil and Argentina are the key markets, though economic instability and currency volatility often hinder widespread adoption and investment in premium products. Consumers in this region are highly price-sensitive, leading to stronger competition in the budget and mid-range segments. Infrastructure challenges, such as unreliable internet connectivity in some areas, also pose barriers to market growth. Nonetheless, as mobile internet penetration improves and local players expand their offerings, the market is expected to gain momentum over the coming years.

Middle East & Africa

The Middle East & Africa region is in the nascent stages of WiFi camera adoption, with growth concentrated in more developed economies like the UAE, Saudi Arabia, and South Africa. Demand is primarily driven by high-net-worth individuals, commercial enterprises, and government projects focused on smart city initiatives and enhanced security infrastructure. The market faces challenges such as limited consumer awareness, economic diversity across the region, and underdeveloped internet infrastructure in certain areas. However, increasing investments in technological modernization and a growing middle class present long-term opportunities for market expansion, particularly in urban centers.

Report Scope

This market research report provides a comprehensive analysis of the global and regional WiFi Cameras markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global WiFi Cameras Market?

-> WiFi Cameras Market was valued at 24090 million in 2024 and is projected to reach US$ 53410 million by 2032, at a CAGR of 12.3% during the forecast period.

Which key companies operate in Global WiFi Cameras Market?

-> Key players include Canon, Sony, Samsung, Panasonic, Nikon, GoPro, Kodak, Fujifilm, Olympus, Ricoh (PENTAX), Garmin, TP-Link, HIKVISION, Netgear, D-Link, JADO, Philips, LG, Uniden, Motorola, Summer Infant, Dahua(LeChange), iON Cameras, and TASER International (AXON), among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for home security solutions, increasing adoption of smart home devices, growth in consumer electronics, and advancements in wireless technology.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include integration of AI and machine learning, higher resolution imaging (4K/8K), cloud storage solutions, and enhanced cybersecurity features.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...