MARKET INSIGHTS

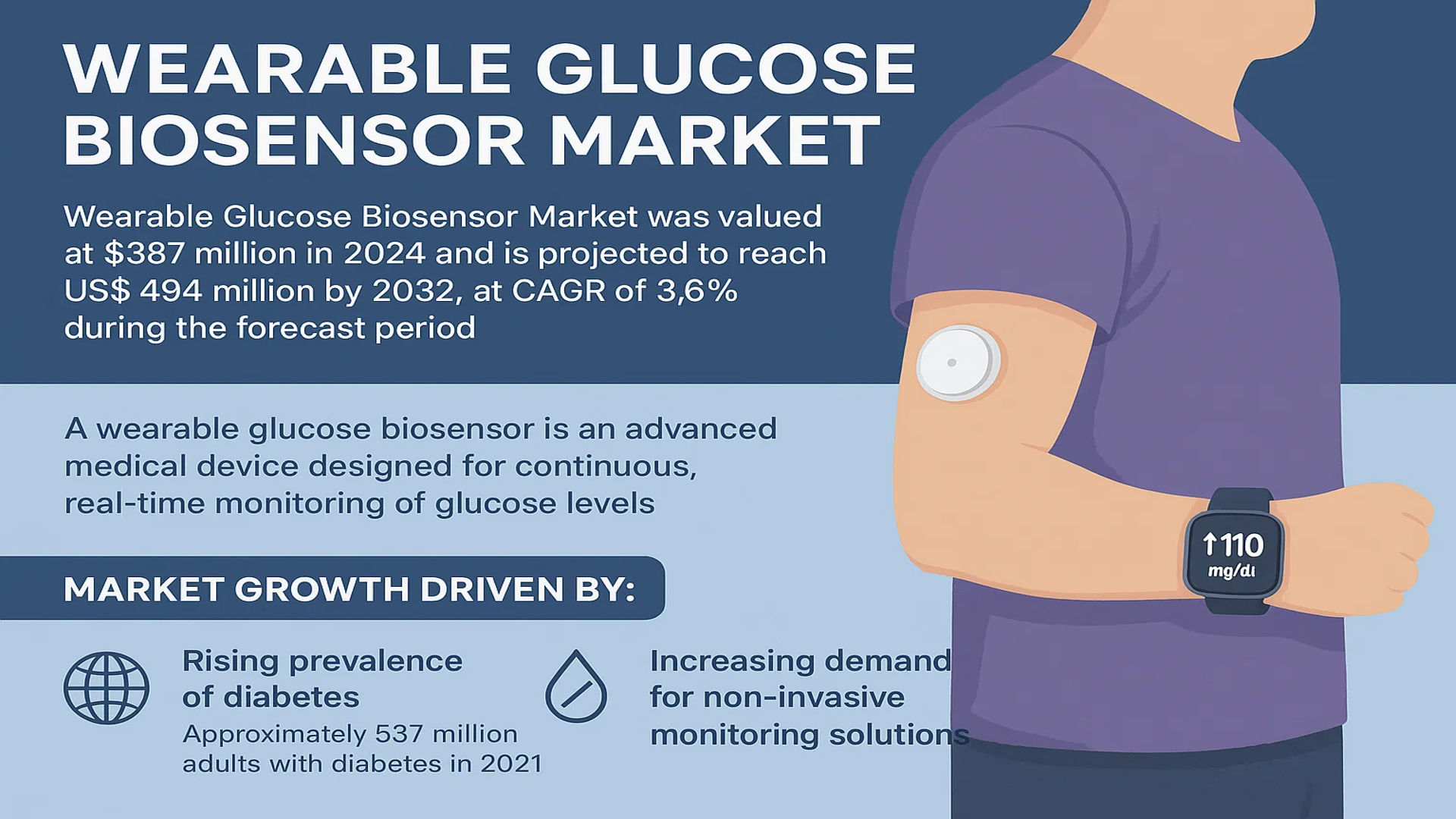

The global Wearable Glucose Biosensor Market was valued at 387 million in 2024 and is projected to reach US$ 494 million by 2032, at a CAGR of 3.6% during the forecast period.

A wearable glucose biosensor is an advanced medical device designed for continuous, real-time monitoring of glucose levels. These biosensors utilize electrochemical and biochemical sensing technologies to detect glucose concentrations in interstitial fluid, sweat, or other biological fluids, eliminating the need for frequent finger-prick blood samples. Typically integrated into discreet skin patches, smartwatches, or adhesive sensors, they provide a convenient and user-friendly solution for diabetes management.

The market growth is primarily driven by the rising global prevalence of diabetes, which affected approximately 537 million adults in 2021 according to the International Diabetes Federation, and the increasing demand for non-invasive monitoring solutions. Furthermore, technological advancements in sensor accuracy and miniaturization, coupled with growing health consciousness, are contributing to market expansion. Key players such as Abbott, with its FreeStyle Libre system, and Dexcom are leading the market with significant R&D investments and strategic product launches.

MARKET DYNAMICS

MARKET DRIVERS

Rising Global Diabetes Prevalence to Fuel Demand for Wearable Glucose Biosensors

The increasing global prevalence of diabetes is a primary driver for the wearable glucose biosensor market. Over 537 million adults worldwide were living with diabetes in 2021, and this number is projected to rise to 643 million by 2030. This growing patient population requires continuous glucose monitoring solutions to manage their condition effectively, driving demand for wearable biosensors. These devices offer significant advantages over traditional fingerstick methods, providing real-time glucose readings without the discomfort of frequent blood sampling. The ability to track glucose trends throughout the day enables better glycemic control and reduces the risk of diabetes-related complications. Healthcare providers increasingly recommend continuous glucose monitoring as part of comprehensive diabetes management, further accelerating market adoption.

Technological Advancements and Product Innovation to Accelerate Market Growth

Continuous technological innovations in biosensor technology are significantly driving market expansion. Recent developments have focused on improving sensor accuracy, extending wear time, reducing device size, and enhancing connectivity with digital health platforms. The latest generation of wearable glucose biosensors can now provide glucose readings with accuracy rates exceeding 98% while offering wear periods of up to 14 days. Major manufacturers have introduced systems that eliminate the need for fingerstick calibrations, greatly improving user convenience. The integration of artificial intelligence and machine learning algorithms enables predictive glucose alerts, helping users anticipate and prevent hypoglycemic or hyperglycemic events before they occur. These technological improvements are making wearable glucose biosensors more reliable, user-friendly, and clinically valuable.

Growing Health Consciousness and Preventive Healthcare Trends to Boost Market Adoption

The increasing focus on preventive healthcare and wellness monitoring is creating new growth opportunities for wearable glucose biosensors. Beyond the diabetic population, health-conscious individuals and athletes are adopting these devices to monitor metabolic health and optimize performance. The sports and fitness segment represents one of the fastest-growing application areas, with users leveraging continuous glucose data to understand how different foods, exercise routines, and lifestyle factors affect their glucose levels. This trend is supported by the broader movement toward personalized health monitoring and data-driven wellness decisions. The ability to track glucose responses in real-time provides valuable insights for nutrition planning, workout optimization, and overall metabolic health management.

➤ For instance, regulatory approvals for non-prescription continuous glucose monitoring systems are expanding access beyond clinical applications, enabling broader consumer adoption for wellness purposes.

Furthermore, insurance coverage expansion and reimbursement policies for continuous glucose monitoring systems in many developed countries are making these devices more accessible to patients, supporting market growth across diverse demographic segments.

MARKET CHALLENGES

High Costs and Reimbursement Limitations to Challenge Market Penetration

The wearable glucose biosensor market faces significant challenges related to cost barriers and reimbursement limitations. The average cost of continuous glucose monitoring systems ranges from approximately $300 to $500 per month for sensors and transmitters, creating financial burdens for patients without adequate insurance coverage. While reimbursement policies have improved in many developed markets, coverage remains inconsistent across regions and insurance providers. In developing countries, where out-of-pocket healthcare expenditures are predominant, the high cost of these devices significantly limits market penetration. Additionally, the ongoing expense of sensor replacements and necessary accessories creates long-term financial commitments that many patients cannot sustain.

Other Challenges

Accuracy and Reliability Concerns

Despite technological improvements, accuracy concerns remain a significant challenge for market adoption. Sensor accuracy can be affected by various factors including physiological variations, medication interactions, and environmental conditions. The margin of error, while reduced in newer models, still requires validation through traditional blood glucose measurements in certain clinical situations. This necessity for occasional fingerstick testing undermines the completely non-invasive value proposition and creates user inconvenience.

User Compliance and Adherence Issues

Maintaining consistent user adherence presents another challenge for market growth. Some users experience skin irritation or discomfort from prolonged sensor wear, leading to discontinued use. The requirement for regular device changes and continuous data monitoring can create user fatigue over time. Additionally, the learning curve associated with interpreting continuous glucose data and making appropriate lifestyle adjustments can be overwhelming for some users, particularly older patients or those with limited technical proficiency.

MARKET RESTRAINTS

Regulatory Hurdles and Approval Processes to Constrain Market Expansion

Stringent regulatory requirements and lengthy approval processes significantly restrain the wearable glucose biosensor market. These devices are classified as medical devices requiring rigorous clinical validation and regulatory approvals before market entry. The approval process typically involves extensive clinical trials demonstrating safety, accuracy, and effectiveness across diverse patient populations. Regulatory agencies require comprehensive data on sensor performance, biocompatibility, and cybersecurity features, particularly for devices that connect to digital platforms and mobile applications. The complexity of these requirements often extends development timelines by several years and increases product development costs substantially.

Additionally, varying regulatory frameworks across different countries and regions create additional barriers for global market expansion. Manufacturers must navigate distinct regulatory pathways and compliance requirements for each market, further complicating product launches and geographical expansion strategies.

The evolving regulatory landscape for digital health technologies and data privacy adds another layer of complexity. Compliance with data protection regulations such as GDPR in Europe and similar frameworks in other regions requires significant investment in cybersecurity measures and data management protocols.

MARKET OPPORTUNITIES

Expansion into Non-Diabetic Applications to Create New Growth Frontiers

The expansion of wearable glucose biosensors into non-diabetic applications represents a significant growth opportunity for market players. Beyond traditional diabetes management, these devices are finding applications in metabolic health monitoring, sports performance optimization, and preventive healthcare. The wellness and fitness segment is particularly promising, with athletes and health-conscious consumers using continuous glucose data to optimize nutrition, training regimens, and overall metabolic health. This expansion into broader consumer markets could potentially reach millions of users who monitor their glucose levels for lifestyle optimization rather than medical necessity.

Research institutions and pharmaceutical companies are increasingly utilizing wearable glucose biosensors for clinical trials and metabolic research. The ability to collect continuous, real-world glucose data provides valuable insights for studying metabolic disorders, drug efficacy, and nutritional interventions. This research application segment is growing rapidly as the scientific community recognizes the value of continuous glucose data over traditional intermittent measurements.

Furthermore, the integration of glucose monitoring with other health metrics through multi-sensor wearable platforms creates additional opportunities. Combining glucose data with activity tracking, heart rate monitoring, and sleep analysis provides comprehensive health insights that no single metric can offer alone. This holistic approach to health monitoring aligns with the growing trend toward integrated digital health solutions.

WEARABLE GLUCOSE BIOSENSOR MARKET TRENDS

Advancements in Minimally Invasive and Non-Invasive Technologies to Emerge as a Trend in the Market

The evolution of minimally invasive and non-invasive glucose monitoring technologies represents a pivotal trend shaping the wearable glucose biosensor landscape. While traditional Continuous Glucose Monitoring (CGM) systems require subcutaneous insertion of a small filament, recent innovations are pushing the boundaries toward truly non-invasive methods. These include biosensors that measure glucose levels through sweat, interstitial fluid via microneedle arrays, or even through optical sensors embedded in smartwatches. This shift is crucial because it addresses significant user pain points, such as the discomfort and skin irritation associated with long-term sensor wear. The market is responding to a growing demand from a broader user base, including health-conscious individuals and athletes, who seek metabolic insights without the drawbacks of traditional methods. This technological progression is not merely an incremental improvement but a fundamental reimagining of patient-centric care, fostering greater adherence and opening up new market segments beyond the core diabetic population.

Other Trends

Integration with Digital Health Ecosystems and Artificial Intelligence

The powerful integration of wearable biosensors with comprehensive digital health platforms and Artificial Intelligence (AI) is another dominant trend revolutionizing diabetes management. Modern CGM systems are no longer isolated data collectors; they are integral nodes within a connected ecosystem. Real-time glucose data is wirelessly transmitted to smartphones and smartwatches, where sophisticated algorithms and AI-driven analytics provide predictive alerts for hypoglycemia or hyperglycemia, personalized dietary recommendations, and trend analyses. This creates a closed-loop system, or an “artificial pancreas,” where the CGM device can communicate with an insulin pump to automate insulin delivery. The value lies in the transition from reactive to proactive care. By analyzing vast datasets of glucose levels, food intake, and physical activity, these systems empower users and clinicians with actionable intelligence, significantly improving glycemic control and quality of life. This trend is a major driver for market expansion as it delivers tangible, data-driven health outcomes.

Expansion into New Application Segments Beyond Diabetes

While diabetes management remains the primary application, a significant trend is the strategic expansion of wearable glucose biosensors into new and diverse market segments. The sports and fitness industry is a key growth area, where athletes and fitness enthusiasts use these devices to monitor metabolic efficiency and optimize nutrition and training regimens in real-time. Furthermore, clinical and biomedical research institutions are increasingly adopting this technology for studies related to metabolic disorders, drug efficacy trials, and nutritional science. The ability to obtain continuous, high-frequency glucose data provides researchers with unprecedented insights that were previously unattainable with sporadic blood tests. This diversification mitigates market reliance on a single application and taps into the growing consumer wellness movement, driving innovation in product design and functionality to meet the specific needs of these varied user groups.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Drive Market Competition

The global wearable glucose biosensor market is characterized by a moderately consolidated structure, dominated by a few major players while accommodating several emerging innovators. Abbott Laboratories stands as the unequivocal market leader, primarily driven by its revolutionary FreeStyle Libre system. Holding a significant revenue share, Abbott’s success stems from its extensive global distribution network, robust reimbursement coverage across multiple healthcare systems, and continuous product iterations that enhance user experience and accuracy.

Dexcom, Inc. represents another formidable force, renowned for its high-accuracy Dexcom G7 Continuous Glucose Monitoring (CGM) system. The company’s growth is heavily attributed to its strong focus on real-time data integration with digital health platforms and insulin pumps, creating a seamless ecosystem for diabetes management. Its strategic partnerships with insulin delivery system manufacturers have further solidified its position in the automated insulin delivery market segment.

These established players are increasingly challenged by innovative entrants focusing on non-invasive technologies. Afon Technology, for instance, is pioneering a non-invasive, continuous glucose monitoring device integrated into a smartwatch. Their approach eliminates the need for skin penetration, targeting a broader audience including health-conscious individuals and pre-diabetics. Similarly, Biolinq is developing a minimally invasive epidermal biosensing system that measures glucose from interstitial fluid at the surface of the skin, aiming to reduce discomfort and complexity.

Growth strategies across the board involve significant investment in research and development to improve sensor longevity, accuracy, and affordability. Furthermore, companies are aggressively pursuing geographical expansion into emerging markets in Asia-Pacific and Latin America, where the prevalence of diabetes is rising rapidly. Regulatory approvals, such as recent CE marks and FDA clearances for new-generation devices, remain critical milestones that significantly impact market share and competitive positioning.

Meanwhile, the competitive intensity is expected to increase as companies like Medtronic and Roche Diagnostics enhance their CGM offerings, and tech giants explore integrating glucose sensing into broader consumer health platforms. This dynamic environment ensures that continuous innovation, strategic partnerships, and cost-effective manufacturing will be paramount for sustaining competition in this rapidly evolving market.

List of Key Wearable Glucose Biosensor Companies Profiled

- Abbott Laboratories (U.S.)

- Dexcom, Inc. (U.S.)

- Afon Technology Ltd. (U.K.)

- Biolinq (U.S.)

- Medtronic plc (Ireland)

- Roche Diagnostics (Switzerland)

- Senseonics Holdings, Inc. (U.S.)

- Nemaura Medical Inc. (U.K.)

- Profil GmbH (Germany)

Segment Analysis:

By Type

Continuous Glucose Monitoring Segment Dominates the Market Due to its Real-Time Data Capabilities and Growing Adoption

The market is segmented based on type into:

- Self-monitoring of Blood Glucose (SMBG)

- Continuous Glucose Monitoring

By Application

Diabetes Patients Segment Leads Due to High Global Prevalence and Need for Constant Monitoring

The market is segmented based on application into:

- Diabetes Patients

- Clinical Laboratories

- Biomedical Research Institutes

- Sports and Fitness

- Others

By Technology

Electrochemical Biosensors Hold the Largest Share Due to High Accuracy and Reliability

The market is segmented based on technology into:

- Electrochemical Biosensors

- Optical Biosensors

- Thermometric Biosensors

- Piezoelectric Biosensors

By Distribution Channel

Retail Pharmacies Segment is Prominent Due to Wide Accessibility and Product Availability

The market is segmented based on distribution channel into:

- Hospital Pharmacies

- Retail Pharmacies

- Online Sales

- Diabetes Clinics

Regional Analysis: Wearable Glucose Biosensor Market

North America

North America represents the largest and most technologically advanced market for wearable glucose biosensors, driven primarily by the United States. The region’s dominance stems from its high diabetes prevalence—affecting over 37 million people—coupled with robust healthcare infrastructure and widespread insurance coverage for Continuous Glucose Monitoring (CGM) systems. Stringent FDA regulations ensure product efficacy and safety, fostering consumer trust. Recent developments include the integration of CGM data with digital health platforms and electronic health records, enhancing personalized diabetes management. Market leaders like Abbott (with its FreeStyle Libre system) and Dexcom are headquartered here, driving innovation through substantial R&D investments. However, high device costs and reimbursement variability present ongoing challenges, though these are partially offset by increasing adoption among type 1 and type 2 diabetes patients seeking improved glycemic control.

Europe

Europe is a significant and growing market, characterized by strict regulatory oversight under the EU’s MDR (Medical Device Regulation) and a strong emphasis on patient safety and data privacy. Countries like Germany, the UK, and France lead in adoption due to well-established healthcare systems and reimbursement policies that often cover CGM devices for specific patient groups. The region shows a rising demand for non-invasive and minimally invasive sensors, driven by increasing health awareness and an aging population. However, market growth faces hurdles from varying reimbursement frameworks across member states and cost containment pressures within national health services. Collaboration between manufacturers and healthcare providers is key to expanding access, particularly as the clinical benefits of real-time glucose monitoring become more widely recognized.

Asia-Pacific

The Asia-Pacific region is poised for the highest growth rate globally, fueled by its large diabetic population—exceeding 200 million—and rapidly improving healthcare access. China and India are the primary drivers, with governments increasingly focusing on diabetes management as part of broader public health initiatives. While cost sensitivity remains a barrier, leading to higher use of traditional finger-stick methods, there is a noticeable shift toward wearable biosensors among urban, affluent consumers. Local manufacturers are emerging, offering more affordable alternatives to international brands, though quality and accuracy vary. The market is also expanding beyond diabetes into fitness and wellness applications, particularly in countries like Japan and South Korea, where tech-savvy consumers adopt these devices for lifestyle monitoring.

South America

South America’s market is emerging, with growth concentrated in countries like Brazil and Argentina. Increasing diabetes prevalence and gradual improvements in healthcare infrastructure are driving demand. However, economic volatility and limited reimbursement for advanced glucose monitoring devices restrict widespread adoption. The market is currently dominated by self-monitoring blood glucose systems due to their lower cost, though awareness of CGM benefits is growing among specialists and patients in urban areas. Challenges include currency fluctuations affecting device affordability and uneven access to diabetes care outside major cities. Nonetheless, long-term potential exists as economies stabilize and public health initiatives prioritize chronic disease management.

Middle East & Africa

The Middle East & Africa region shows nascent but promising growth, particularly in Gulf Cooperation Council (GCC) countries like Saudi Arabia and the UAE, where high diabetes rates and government healthcare investments support market development. South Africa also presents opportunities due to its relatively advanced medical sector. However, across most of Africa, limited healthcare funding, infrastructure gaps, and low awareness hinder adoption. The market is primarily served by international brands targeting private payers and high-income individuals. Efforts to increase access focus on partnerships with global health organizations and pilot programs introducing CGM in clinical settings. While growth is slow, the region’s significant unmet need for diabetes care suggests substantial long-term potential as economic conditions improve.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Wearable Glucose Biosensor markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, biosensor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Wearable Glucose Biosensor Market?

-> Wearable Glucose Biosensor Market was valued at 387 million in 2024 and is projected to reach US$ 494 million by 2032, at a CAGR of 3.6% during the forecast period.

Which key companies operate in Global Wearable Glucose Biosensor Market?

-> Key players include Abbott, Dexcom, Afon Technology, and Biolinq, among others.

What are the key growth drivers?

-> Key growth drivers include rising diabetes prevalence, technological advancements in continuous glucose monitoring, and increasing health consciousness.

Which region dominates the market?

-> North America is the dominant market, while Asia-Pacific is the fastest-growing region.

What are the emerging trends?

-> Emerging trends include non-invasive monitoring technologies, integration with smart wearables, and AI-powered glucose prediction algorithms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...